Analysis of the Cashew Value Chain in Nigeria · ACi is implemented by the African Cashew Alliance...

52

1 Analysis of the Cashew Value Chain in Nigeria African Cashew initiative

-

Upload

nguyenhuong -

Category

Documents

-

view

283 -

download

12

Transcript of Analysis of the Cashew Value Chain in Nigeria · ACi is implemented by the African Cashew Alliance...

1

Analysis of the Cashew Value Chain in Nigeria African Cashew initiative

Published by:

Deutsche Gesellschaft für

Internationale Zusammenarbeit (GIZ) GmbH

International Foundations

Postfach 5180, 65726 Eschborn, Germany

T +49 61 96 79-1438

F +49 61 96 79-80 1438

I www.giz.de

Place and date of publication: Germany,April 2011 Authors:

Alois Große-Rüschkamp,

Clive Topper,

Ernst Grenzebach

Responsible editor:

Rita Weidinger - Executive Director

African Cashew init iative (ACi)

32, Nortei Ababio Street

Airport Residential Area

Accra, GHANA

T + 233 302 77 41 62 F + 233 302 77 13 63 Contact: [email protected]

Acknowledgement:

This study has been implemented as part of

the African Cashew init iative (ACi), a project jointly

financed by various private companies, the Federal German

Ministry for Economic Cooperation and Development

and the Bill & Melinda Gates Foundation.

ACi is implemented by the African Cashew Alliance (ACA),

the German Development Cooperation GIZ, as a lead agen-

cy as well as FairMatchSupport and Technoserve.

This report is based on research funded by the

Bill & Melinda Gates Foundation. The findings and conclu-

sions contained within are those of

the authors and do not necessarily reflect positions

or policies of the Bill & Melinda Gates Foundation.

Design:

© creative republic // Thomas Maxeiner Visual Communic a-

tion,Frankfurt am Main/Germany

T 4969-915085-60

I www.creativerepublic.net

Photos:

© GIZ/Rüdiger Behrens, Dr. Clive Topper, Thorben Kruse & creative republic, iStock, Shutterstock

and private sector partners

African Cashew Initiative is funded by:

Implemented by: In cooperation with:

Analysis of the Cashew Value Chain in Nigeria April 2011

4

Table of Contents

Executive Summary .................................................... 5

1 Introduction ...................................................... 9

2 Aspects of the Cashew sector ............................. 10

2.1 Global aspects .................................................. 10

2.2 Nigerian Cashew acreage and production ....... 10

2.3 Regional distribution of production ................. 13

3 The Cashew value chain in the three states

visited ............................................................. 16

3.1 Production ........................................................ 16

3.1.1 Importance of Cashew ............................ 16

3.1.2 Cashew production systems ................... 16

3.1.3 Cashew acreage per farm ....................... 17

3.1.4 Ownership and availability of land for Cashew production .................................. 17

3.1.5 Yields/ha of raw Cashew nut .................. 17

3.2 Marketing and Processing ................................ 18

3.2.1 The marketing chains ............................. 18

3.2.2 Processing operations ............................ 20

3.2.3 Cashew exports ...................................... 24

3.2.4 Use of Cashew by-products .................... 24

3.3 The Institutional environment of Cashew production and sector policy ............................ 25

3.3.1 Agricultural policy relating to Cashew .... 25

3.3.2 Export promotion of non-oil products .... 25

3.3.3 Cashew research ..................................... 26

3.3.4 Agricultural extension ............................. 27

4 SWOT Analysis of the Cashew Sector ................. .28

4.1 Strengths .......................................................... 28

4.2 Weaknesses ...................................................... 28

4.3 Opportunities ................................................... 30

4.4 Threats ............................................................. 30

5 Specific issues relevant for reinforcing Cashew

production, marketing and processing ................ 31

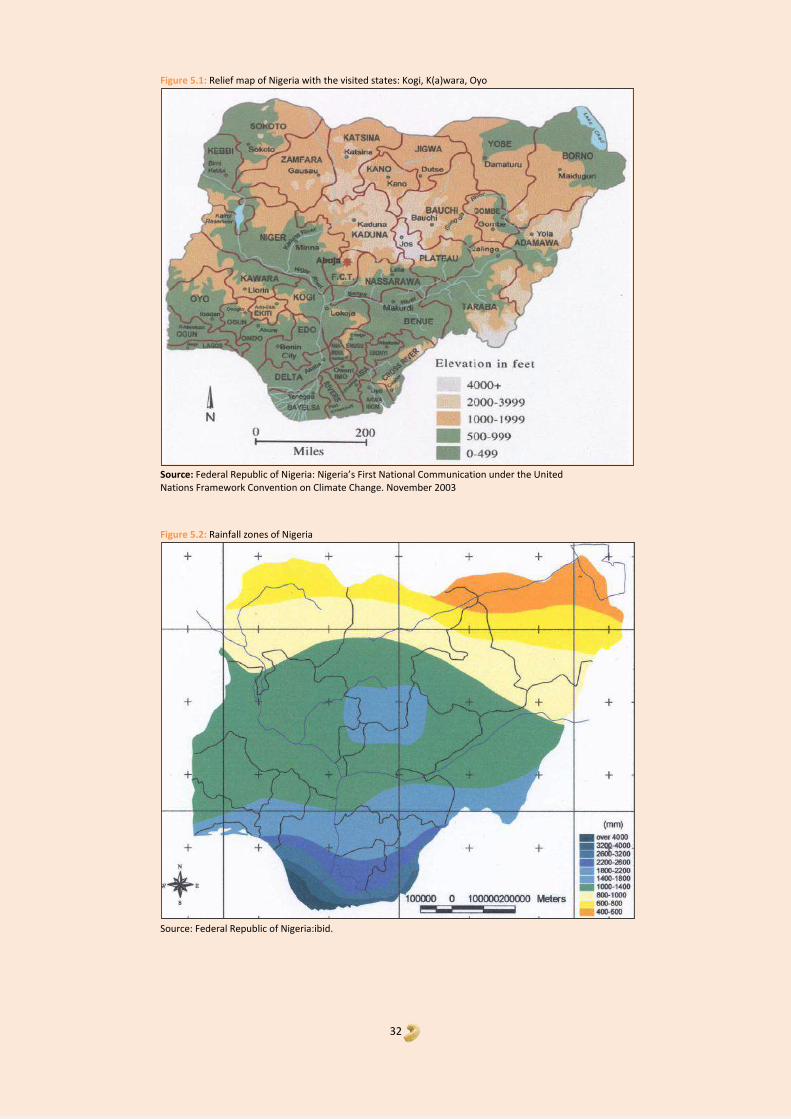

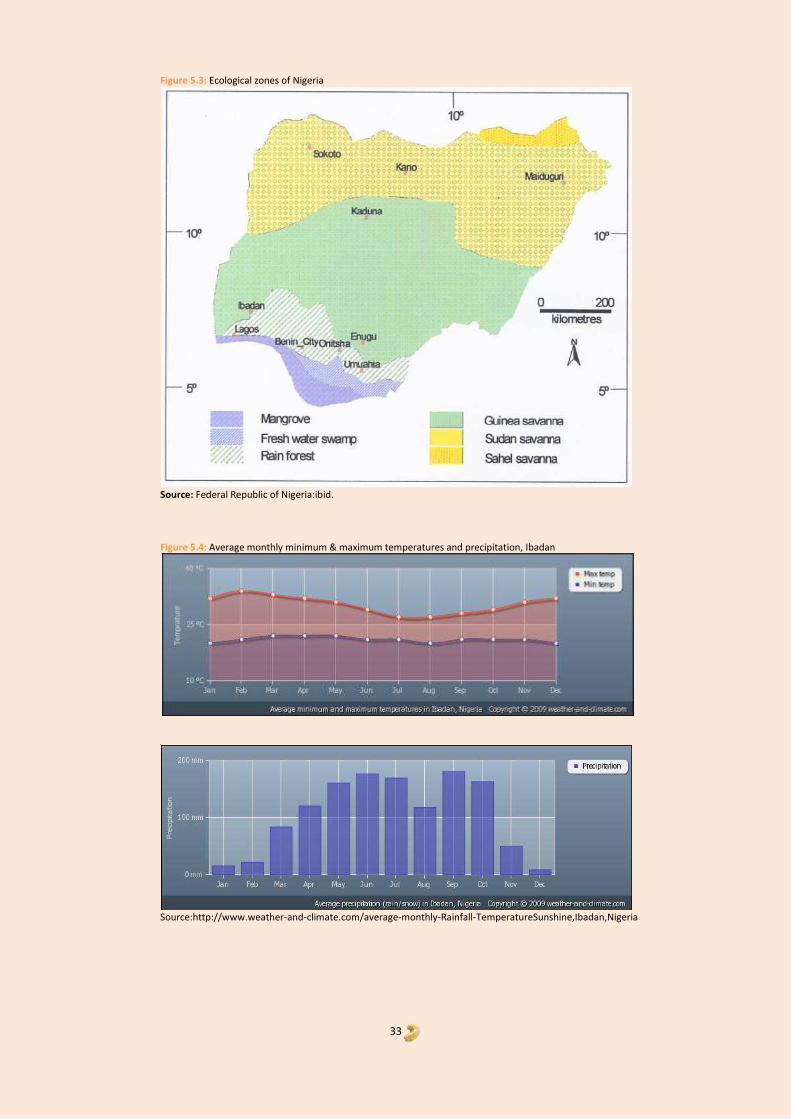

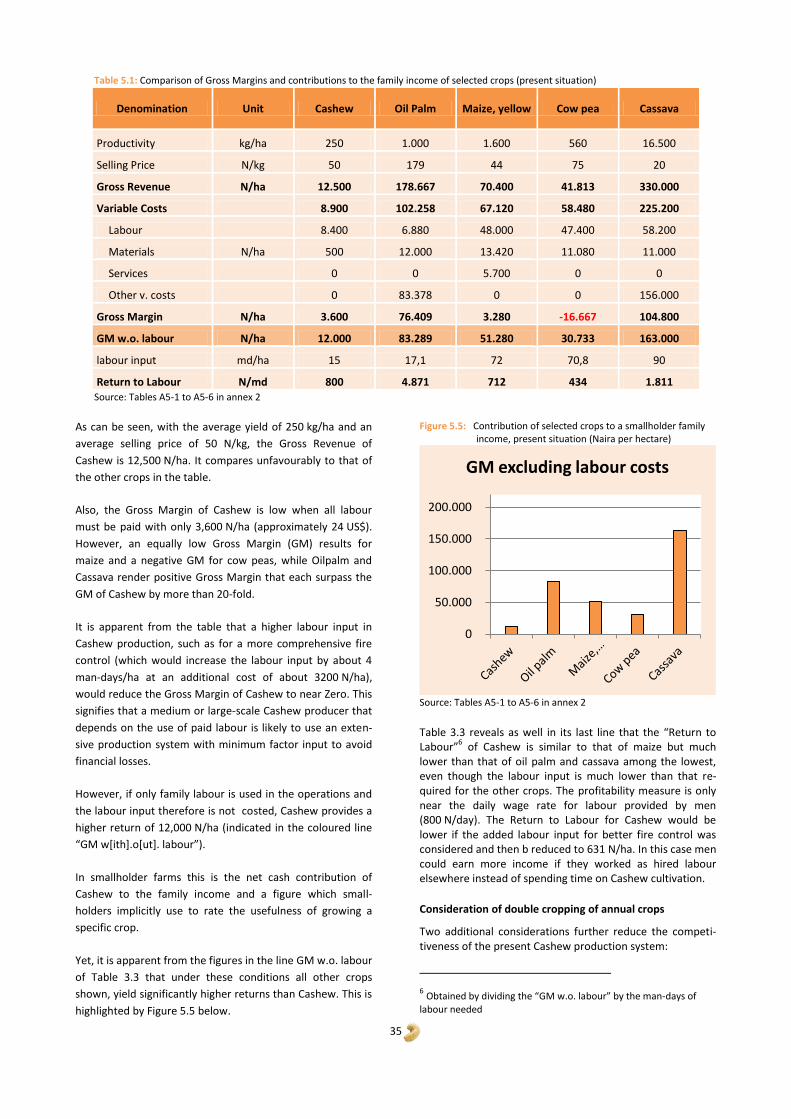

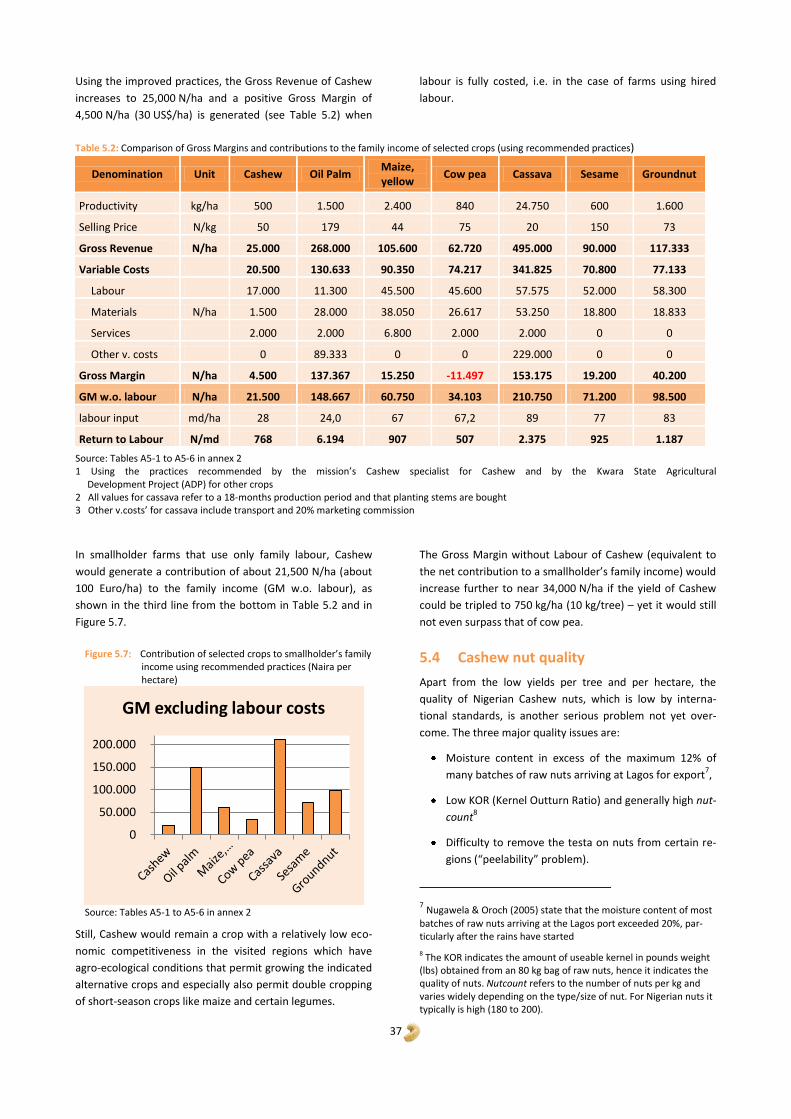

5.1 Environmental conditions of Cashew production..……………………………………….……………31

5.2 Geographical location of Cashew production in Nigeria…………………………………………………………… 31

5.3 Economics of Cashew production .................... 34

5.4 Cashew nut quality ........................................... 37

5.5 Use of unproven planting material .................. 38

5.6 The domestic market ....................................... 38

6 General Conclusions ......................................... 40

Acronyms ................................................................ 41

Literature ................................................................ 42

Annex 1 - List of Contacts .......................................... 43

Annex 2 - Economic Data ........................................... 45

List of Figures

Figure 2.1: Global production of RCN 1965 – 2007 10

Figure 2.2: Map of Nigeria showing Cashew activity areas ..15

Figure 3.1: Percentage of Kwara state farmers growing

specific crops .....................................................16

Figure 3.2: Frequency distribution of the Cashew acreage of

the respondents ................................................17

Figure 3.3: Marketing Channels of Nigerian Cashew Nuts ...18

Figure 3.4: Cashew Processing (Raw Nut Warehouse

Operations) .......................................................21

Figure 5.1: Relief map of Nigeria with the visited states: Kogi,

K(a)wara, Oyo ....................................................32

Figure 5.2: Rainfall zones of Nigeria .....................................32

Figure 5.3: Ecological zones of Nigeria .................................33

Figure 5.4: Average monthly minimum & maximum

temperatures and precipitation, Ibadan ...........33

Figure 5.5: Contribution of selected crops to a smallholder

family income, present situation (Naira per

hectare) .............................................................35

Figure 5.6: Calendar of recommended activities in Cashew

production in the Central Belt ...........................36

Figure 5.7: Contribution of selected crops to smallholder’s

family income using recommended practices

(Naira per hectare) ............................................37

List of Tables

Table 2.1: Cashew production, marketing, processing and

export volumes estimates (MT).........................11

Table 2.2: History/Development of the Cashew Sector in

Nigeria ...............................................................12

Table 2.3: Estimated Cashew areas, production volumes,

shares of the national total and yields ..............14

Table 3.1: Actors in the Marketing and Processing Chain of

Nigerian Cashew ................................................19

Table 3.2: Installed and used processing capacity for

Cashew ..............................................................22

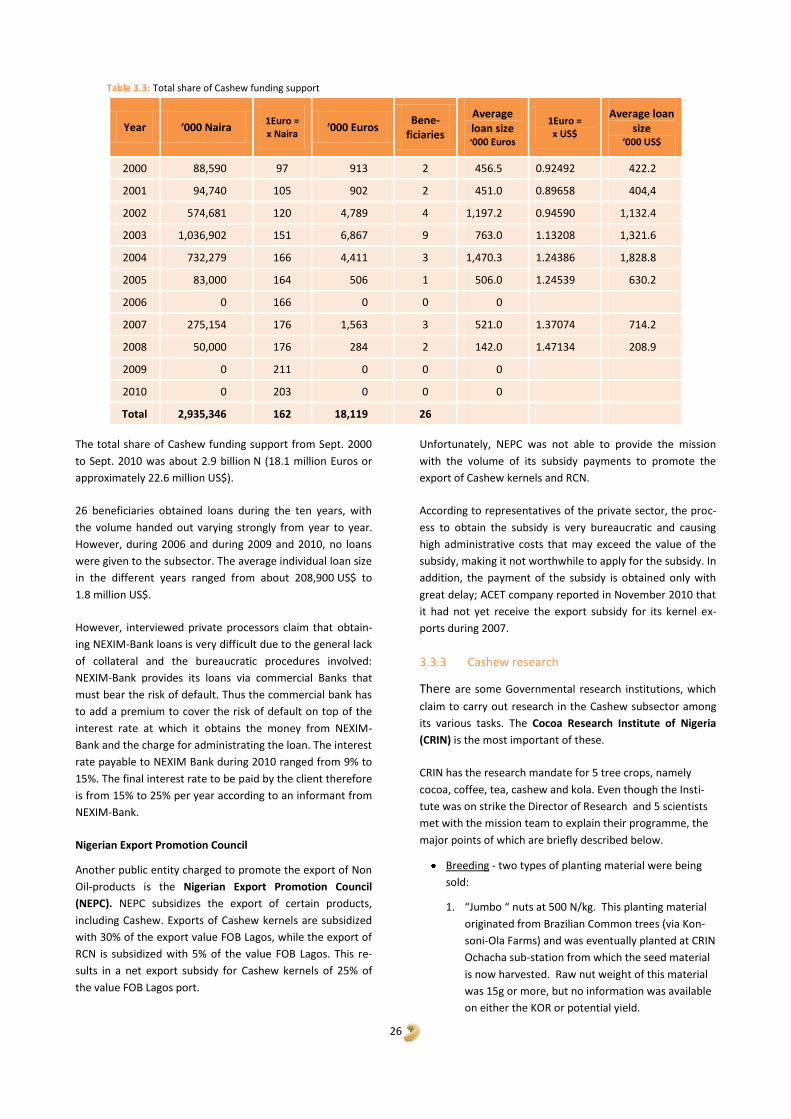

Table 3.3: Total share of Cashew funding support .............26

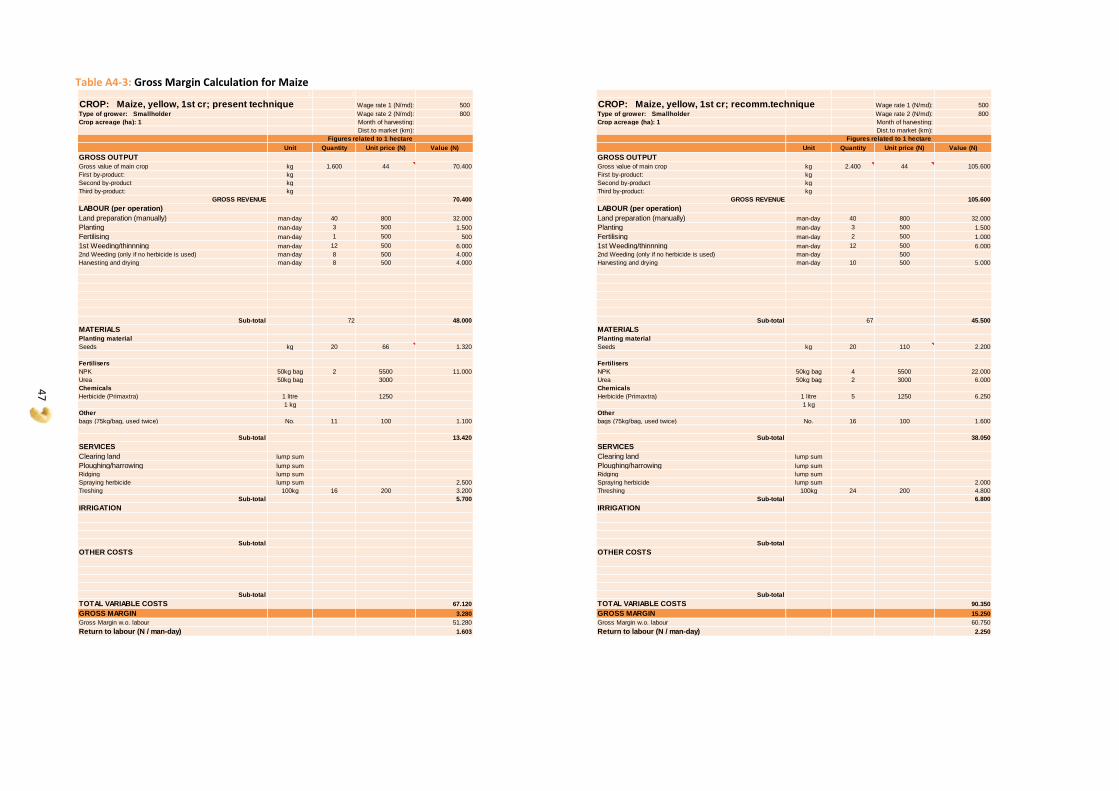

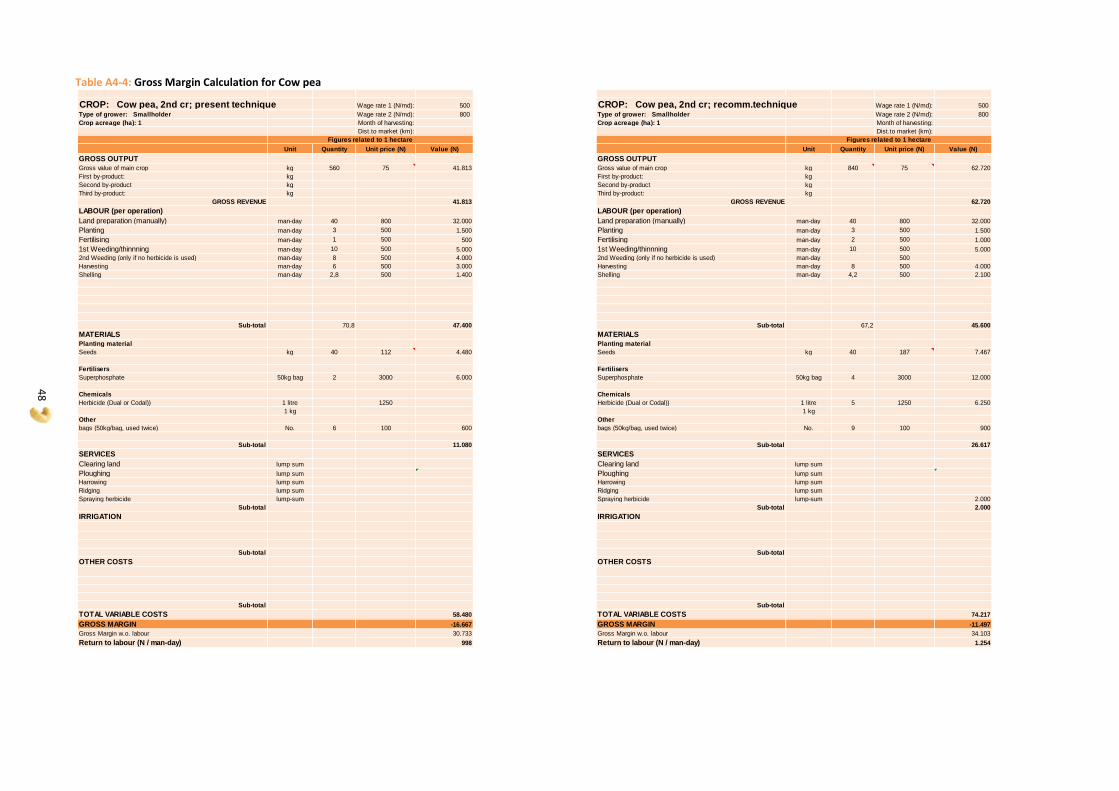

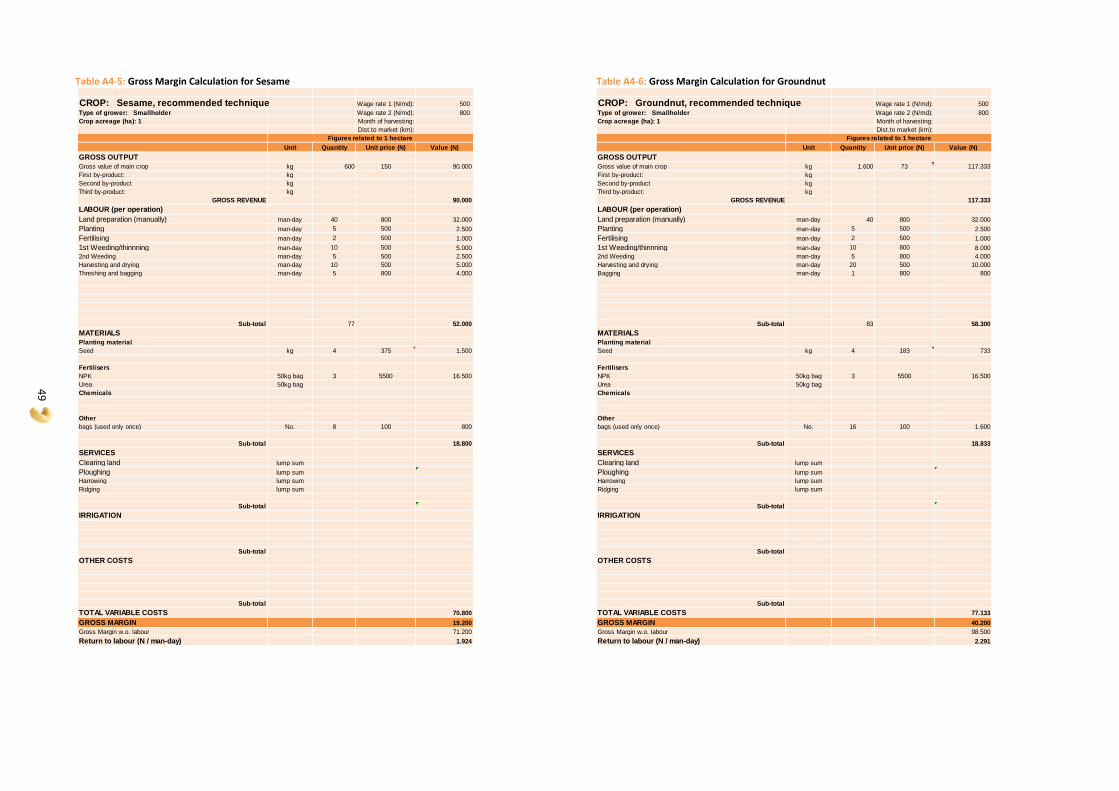

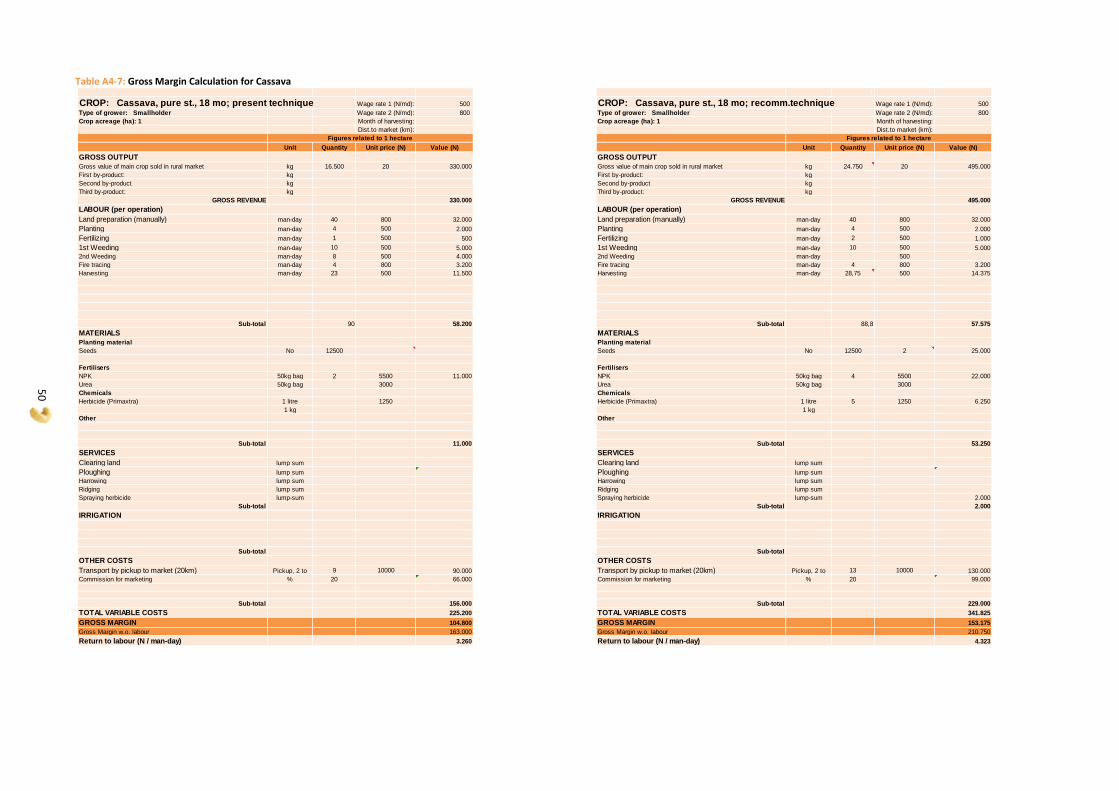

Table 5.1: Comparison of Gross Margins and contributions

to the family income of selected crops (present

situation) ...........................................................35

Table 5.2: Comparison of Gross Margins and contributions

to the family income of selected crops (using

recommended practices) ..................................37

5

Executive Summary

Focus of the study and approach

The study is based on field work by a mission consisting of 3

international experts during October/November 2010 that

analysed Cashew production in Kogi, Kwara and Oyo states

in Nigeria. The report contains the conclusions of the analy-

sis and observations how the productivity of smallholder

Cashew production can be raised and the market potential

be used better.

After a brief look at the development of the global Cashew

Sector and the role Nigeria plays, the Cashew value chain

and Cashew production in the visited three states are ana-

lysed and described. This description contains the results of

the mission’s data collection in the field, specifying the

causes of the observed present-day low productivity, and

the results of visits to processors of different size, compiling

the difficulties they encounter.

Possibilities for the improvement of the productivity of

smallholder Cashew production are then presented, based

on technologies readily available in the country. These im-

provements include changes in the treatment and care of

the trees, their renewal and the planting of new Cashew

trees. A check of the economic feasibility of the proposed

improvements at the producer’s level (micro-economic

feasibility) and its impact on the income of smallholders

completes the analysis.

The present Cashew sector policy is also discussed and some

recommendations are given regarding the support of small-

holder Cashew production and Cashew processing in the

country.

The present situation

Value Chain Analysis

The analysis of the Cashew sector in Nigeria is hampered by

a lack of reliable data that prevents establishing clearly the

present production levels and clear trends. The development

of the sector in the past is briefly described in the main text

of this report (see Box 1). There is general agreement,

though, that Nigeria is a major producer with an estimated

80,000 to 100,000 metric tons (MT) of raw Cashew nuts

(RCN) produced annually, and that about 10% of production

is consumed in the country and the rest exported.

Secondary and primary data collected by the team lead to

the following abstract of the situation regarding production:

Since no up-to-date statistical data regarding the number of

Cashew producers and Cashew production could be ob-

tained, not even the number of large-scale growers can be

determined with confidence. Since small-scale farmers pre-

dominate in the country, most of which established Cashew

trees without advice by or knowledge of the Ministry of

Agriculture and Natural Resources (MANR) or other corre-

sponding state bodies, the total number of Cashew growers

may be near 200,000 or even be considerably higher, as the

results of a sample survey by Kwara State Agricultural De-

velopment Project (ADP) – the state extension service, which

is named according to the project that supported or still

supports it – for the season 2008/09 imply: if ADP is correct

in stating that 61.5% of the sample farmers own Cashew

trees, then projected to the state level there are over

172,000 Cashew growers in Kwara state alone.

Equally, the exact size of the Cashew acreage is not clear. An

acreage of about 100,000 hectares was most frequently

indicated. However, the concept of ‘acreage’ appears suit-

able only when relating to plantation-type Cashew estab-

lishments. Attempts to represent smallholders’ Cashew trees

– that range from single trees to plantation-type plantings

and encompass as well situations of a few trees dispersed

throughout a field with another crop, hedgerows of Cashew

trees and irregular lumps of trees without other crops grown

underneath – in terms of the acreage they occupy may be

responsible for the variation of the acreage figures.

Productivity varies from near zero to near 2,000 kg/ha.

Statistical figures provided by the Ministry of Commerce that

unfortunately appear to contain some gross errors result in

an average yield of near 1 MT/ha. However, the field data

collected suggest it is most frequently around 250 kg/ha. It

appears likely that this figure can be improved through the

transfer of production technology knowledge to the produc-

ers.

According to primary and secondary data, the visited three

provinces belong to the central belt of the country in which

the bulk of the national Cashew tree population is found.

The somewhat dubious figures provided by the Ministry of

Commerce (average yield in Kwara state of about 2 MT/ha!)

even indicate that almost 40% of the national production

originated from Kwara state in 2008/09. This is in stark con-

trast to the ranking of states indicated in earlier studies,

such as that of Ezeagu published in 2002.

The marketing chain of Cashew is long, involving several

actors that buy and partly process RCN, before these reach

the exporter (see Figure 5 in the main text). This is due to

the structure of production, in which many producers fur-

nish small amounts during a 3-months period in areas, many

of which are remote and difficult to reach, leading to high

marketing costs.

About 90% of Nigerian Cashew nuts are exported, and the

bulk of this volume as raw nuts. Only about 15% of the vol-

ume destined for export is processed into graded nut kernels

in the country and then exported. Still, the final processing

and packaging of the kernels for the consumer is almost

exclusively done in the consuming countries in Europe

and/or the USA. Because of this, only a fraction of the total

value added accrues inside Nigeria, and the producers have

6

a low share of the price the final consumers in the importing

countries pay.

The present installed processing capacity in the country is

about 18,000 MT, most of it that of one company, which is

at the present time in the process of doubling its capacity.

The use of the planned increased total processing capacity of

then approximately 33,000 MT would raise the value added

in the country significantly. However, competing processors

have stopped or have temporarily interrupted their activity

during recent years for lack of access to capital needed for

investments and to buy and store RCN.

The internal market in Nigeria is not saturated and demand

appears to be growing. It is now exploited by a few small

processors that use low-level technology. The less rigid

quality requirements of this market offer an opportunity for

small and medium sized processors to expand their opera-

tions and would open a way for marketing locally produced

RCN, most of which are internationally traded at a price

discount of up to 20% (e.g. compared to RCN from Benin)

because of lower quality and peeling problems. The peeling

problem (difficulty to remove the ‘testa’ around the nut

kernel) is due to as yet unidentified causes and regionally

more or less prevalent, while the nut quality measured by

the ‘KOR’ and the ‘nutcount’ (see the main text for an expla-

nation of these terms) depends on the production technique

and the type/variety of Cashew grown, hence vary widely

and can therefore likely be improved significantly through

technology transfer to the producers.

The Institutional framework

The Nigerian Federal and State Governments have played

roles of varying importance over time in regard to the pro-

motion of the Cashew sector, specifically through measures

intended to increase production and exports. Cashew as a

crop has been included in various programs. An earlier one is

the National Accelerated Industrial Crops Production Pro-

gram (NAICPP) started in 1994, a later one the Cashew De-

velopment Program (under the Tree Crops Development

Program), intended initially for the period 2001 to 2004, and

the establishment of 3 Commodity Development and Mar-

keting Companies, with one of these for tree crops (see also

Box 1 in the main text).

MANR’s Tree Crops Development Units (TCDUs) of various

states have in the past supported Cashew production activi-

ties linked to the Cashew Development Program. In Oyo

state some new plantations were created, have since been

rented out to private persons. Little support is provided to

producers by the units visited in the three states – most

often it is limited to establishing contact to potential suppli-

ers of seed nuts of the lately favoured Brazilian Jumbo type,

seedlings of which mature more quickly than the traditional

types and which also produces larger kernels that processors

say they pay a premium for.

A major role is played by the Cocoa Research Institute of

Nigeria (CRIN), which was charged with measures to pro-

mote the selection and breeding of local types and introduc-

tion of improved varieties/types of Cashew, development of

production technology for large-scale production, and pro-

motion of improved production techniques.

A visit to CRIN revealed that Cashew is only one of several

crops of interest and apparently not the one receiving a high

attention. The activities regarding Cashew suffer from lack of

funding, vision & purpose and a missing definition of re-

search priorities, plus the loss of experienced staff. In conse-

quence, CRIN’s present Cashew activities appear limited to

furnishing seed nuts to interested producers from its various

plots of trees that also include the Brazilian Jumbo type.

Other public entities in the research sector are the Raw

Materials Research and Development Council, which recently

funded a 1-ton-a-day processing facility installed at Kogi

State University that uses mostly locally made equipment

and the Federal Institute of Industrial Research (FIRO), which

developed some tools and equipment for Cashew processing

that did, however, not yet pass from the test phase to that

of commercial distribution.

Two entities are important for the promotion of Cashew

exports: The Nigerian Export-Import Bank (NEXIM Bank)

provided the equivalent of approximately 18 million Euros as

investment loans to 25 borrowers in the Cashew sector

through commercial banks since the year 2000. However,

the loan volume has dwindled since a peak in 2004 and no

loans were given at all during 2006, 2009 and 2010 – sup-

posedly due to either lack of collateral of the applicants and

the interest rate of up to 25% the final borrower must pay.

The Nigerian Export Promotion Council (NEPC) subsidizes the

export of certain products, including Cashew. There is an

export subsidy of 30% on processed kernel exports and one

of 5% on RCN exports, but the bureaucratic procedures

involved are tedious and the costs involved to obtain the

subsidy make it uninteresting for exporters of smaller vol-

umes.

While subsidies are (potentially) given on one hand, on the

other hand a ‘grading fee’ is collected per ton of RCN at

state level and the key agents in the marketing chain (Li-

censed Buying Agents - LBAs) need to pay a ‘registration fee’

and an annual ‘licensing fee’.

Economics of Cashew production

If smallholders are to benefit from Cashew production there

must be benefits, either tangible (i.e. measurable in financial

terms) or non-tangible (i.e. other benefits that are not val-

ued in monetary terms). The analysis of the present situation

in the three visited states revealed the following:

With the present productivity of money or financial terms or

improvements in the management of the existing Cashew

7

tree population have been assumed that will result in a

doubling of the productivity from 2.5 kg/tree and 250 kg/ha

in the mostly too dense stands to 500 kg/ha in thinned out

and properly pruned tree populations that are also con-

trolled better against damage by fire and insects.

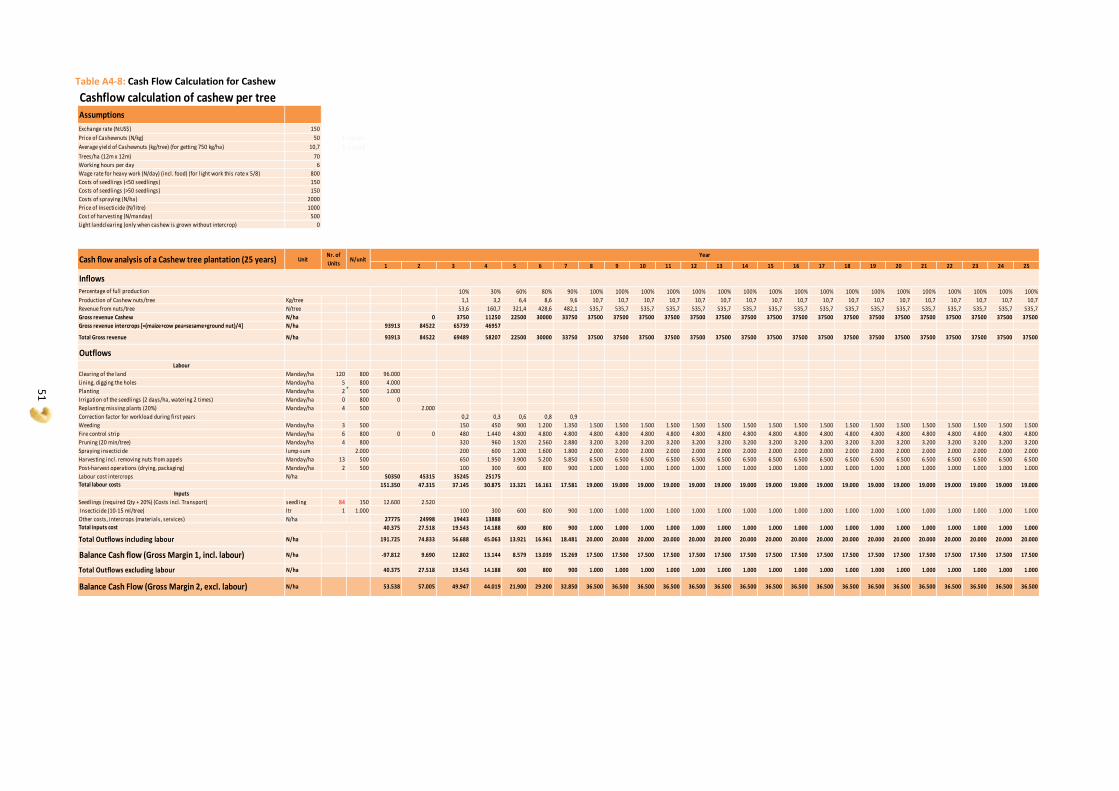

A cash flow analysis for replanting or newly planting Cashew

trees was also undertaken.

Both exercises consider two types of grower: (1) assuming all

labour must be paid (medium-sized grower with several

hectares of Cashew) and (2) assuming all labour input is

done by family labour (situation of the smallholder owning

about 2 ha of Cashew or less). Identical production methods

and yields were assumed for the two types of grower.

Not surprisingly, the labour costs prove to be the largest cost

factor for the medium sized grower, constituting over 90% of

all costs. These costs are not accruing for the smallholder.

Under present circumstances the Gross Margin (Market

Value of production minus variable costs) of Cashew is 3,600

Naira/ha for the grower using hired labour and 12,000 N/ha

for the smallholder using family labour. After improvements

in the management and with a doubled productivity of

existing Cashew, these values change to 4,500 N/ha and

21,500 N/ha.

If Cashew is newly established and bush is cleared for this

purpose, the productivity is supposed to climb to 750 kg/ha

(10 kg/tree when the spacing is 12m x 12m). The average

annual net cash flow (comparable to the Gross Margin of an

annual crop) over a 25-year calculation period is

11,588 N/ha for the medium-sized grower and 37,818 N/ha

for the smallholder using family labour. These figures con-

sider growing annual crops among the cashew trees during

the first 4 years of the plantation.

In the present situation and after improvements, Cashew

proves to be a crop that has low economic competitiveness

compared with annual crops in the study area. This situation

is compounded by the possibility to grow two short-season

crops per year in most parts of the visited three states due

to annual rainfall exceeding 1000 mm. Other perennial crops

like oil palm, cocoa and citrus that thrive in the region also

yield much higher returns than Cashew.

Even though the investment in itself is feasible, new Cashew

plantations can in purely economical terms neither compete

with most annual crops (especially vegetables) nor with the

mentioned alternative tree crops in the three states visited.

Here, the benefits would rather be (i) risk mitigation due to

diversification of the cropping system, (ii) the additional

utilization of existing labour capacity during periods of low

labour demand by other crops, and (iii) the generation of

some income during a period when other crops do not pro-

vide one.

Conclusions

The present, generally low productivity of most Cashew

production seen in the three visited states can be raised

through improvements in the pre- and post-harvest produc-

tion techniques. In many cases the changes required include

the thinning out of too dense stands of trees and/or the

reshaping and/or rejuvenation of trees. However, in general

the productivity can already be improved noticeably through

proper pruning and better protection of the trees against

damage by insects and fire.

In the visited states, Cashew is at present not competitive in

purely financial terms with perennial or annual cash crops,

and not even with the staples yellow maize or beans which

can be double-cropped due to the high rainfall levels in

Kwara, Kogi and Oyo as is shown in section 5.3 of the main

report which contains the economic analysis. Even assuming

a triplication of the yield from 250 kg/ha to 750 kg/ha (i.e. to

about 10 kg/tree) does not change the competitiveness of

Cashew compared with other crops so much that installing

new Cashew plantations (though an economically feasible

investment) would be the preferable alternative for some-

one keen on maximising his income.

In the visited regions Cashew is only of interest for produc-

ers that use predominantly unpaid family labour and appre-

ciate that Cashew requires labour input and provides an

income mainly during the respective off-seasons.

Therefore, any expansion of the Cashew acreage appears

better justified in regions where double cropping is not

possible, alternative crops are less productive while Cashew

remains productive due to its draught tolerance, i.e. in re-

gions with 700 mm or less annual rainfall.

In order to exploit existing market potentials better, it seems

worthwhile to consider attending to the growing demand in

the national market. This would create opportunities for

local processors that cannot easily meet the quality re-

quirements of the international market and would stimulate

local economies.

Regarding the institutional field, it seems worthwhile review-

ing the system of fees asked and subsidies granted by Gov-

ernment entities, as these now create distortions in the

market. The priorities of the public entities concerned with

Cashew research ought to be redefined.

8

9

1 Introduction

The African Cashew Initiative (ACi) project is an activity

supported by the Bill and Melinda Gates Foundation and the

Private Sector with the purpose to strengthen the global

competitiveness of Cashew production and processing in

Africa. Its aim is to create additional income for over

600,000 small farmers in 5 African countries during a period

of ten years by intensifying the production of Cashew in

smallholder farms and by increasing value added through

supporting the whole value chain of Cashew especially proc-

essing and increase the Cashew kernel exports to over

10,000 MT by 2012.

The project pursues five objectives in order to achieve the

overall project goal:

Increase quality and quantity of Raw Cashew Nut (RCN)

production, thus ensuring the competitiveness of Afri-

can Cashew production on global markets,

Strengthen local medium and large-scale Cashew proc-

essing industries,

Improve market linkages along the value chain and

promote African Cashew on the world market

Support an enabling business environment for Cashew

production and processing,

Identify and analyse learning areas and implement in-

novative projects on a pilot basis.

The ACi Cashew project is implemented by GIZ in coopera-

tion with three sub grantees: Technoserve, an US non-

governmental organization; FairMatch Support, a not – for –

profit foundation based in the Netherlands; and the African

Cashew Alliance, a supranational platform of private and

public partners involved in the Cashew value chain. At pre-

sent ACi supports the Cashew value chain in five pilot coun-

tries: Mozambique, Ghana, Benin, Cote d’Ivoire and Burkina

Faso.

According to the Terms of Reference the present study is to:

describe and analyse comprehensively the Cashew

value chain in Nigeria,

determine strengths and weaknesses of the major

stakeholders in the value chain,

focus on Cashew growing areas particularly in the

Western, but as well in the Eastern and Southern part

of Nigeria.

However, due to security concerns, the study team had to

limit its analysis to the three Western Central Belt states of

Kogi, Kwara and Oyo, apart from meeting with stakeholders

operating at or near Lagos. The analysis was additionally

hampered by the general lack of reliable data on the Cashew

sector, especially primary production (see chapter 1) and

partly by a then ongoing strike of research station employ-

ees.

The three mentioned states are among the major producing

areas of raw Cashew kernels in the country. The results of

the economic analysis obtained here are supposed to be

transferable to other Cashew-producing areas of the country

in the same climatic zone, while the results and conclusions

regarding the quality of production and those regarding the

value chain’s part of marketing and processing are consid-

ered representative for all regions of the country.

In the analysis, the strengths and weaknesses in the value

chain are identified and the potentials for enhancement are

explored. Threats that might hamper or impede the devel-

opment are discussed. Together this covers the four ele-

ments of a SWOT analysis.

10

2 Aspects of the Cashew sector

2.1 Global aspects

Global production of RCN has since the 1980s increased

from around 0.5 million metric tons (MT) to over 3 million

MT today. West African countries including Nigeria are con-

sidered major producers, contributing 29% to the total vol-

ume in 2007 according to FAO statistical data (see Figure

2.1). According to these data,1 in 2008 Vietnam was the

leading producer with 1.2 million MT, followed by India with

665,000 MT.

Figure 2.1: Global production of RCN 1965 – 2007

Source: based on FAO STAT figures

Even though some doubts are justified as to the production

figures of some countries that are estimates, the general

trend is undeniable: Global production has multiplied several

fold since the early eighties of the past century, and growth

has continued to be strong even after the turn of the cen-

tury, obviously following a strong growth of global demand

for Cashew kernels.

1 Nov.11 Website search data on web page

http://faostat.fao.org/site/339/default.aspx

2.2 Nigerian Cashew acreage and produc-tion

Official Nigerian statistics regarding the Cashew production

volume are not existing, as the marketing is largely unregu-

lated and includes local sales to agents at two different

levels and acting either on their own behalf or on that of

processors and/or exporter (see the section below on the

marketing chain). Also, home consumption and direct sales

to local customers must be considered in addition.

In 2005, Nugawela and Oroch2 maintained that no system-

atic data was being collected for the Cashew sub-sector,

particularly at the state level and that any data available, for

example, the acreage of Cashew, were based on very gen-

eral estimates and varied widely, e.g.:

375,000 ha according to the “Government of Nigeria”,

200,000 ha under “effective production” according to

the Cocoa Research Institute of Nigeria (CRIN),

Under 200,000 ha according to several other, not speci-

fied studies.

According to data furnished to the mission team by the

Ministry of Commerce the Cashew acreage in 2008/09 was

only about 112,000 ha (see chapter 2.2).

The FAO STAT database contains an ‘estimate’ of 660,000

MT for 2008, which is a figure that seems grossly out of

range and the credibility of which is undermined further by

an unexplained triplication of the volume from 1998 to

1999.

Table 2.1 below contains figures on produced and processed

volumes that have been published in studies during recent

years or have been indicated by the resource persons met by

the members of the assessment team during October 2010.

They are considered to be more realistic, also when taking

into account the volumes processed in the country and

those declared exported.

2 NUGAWELA, Patrick and OROCH, R.: Cashew sub-sector Strategic Framework – Using Cashew sector Markets for Pro-poor Growth in Nigeria. Draft. Abuja, March-April 2005

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

20

09

Mill

ion

to

nn

es

Global production of RCN 1965-2009

Others Mozambique West Africa

Brazil India Viet Nam

% of total 2009 production: West Africa 30% Viet Nam 29% India 21% Brazil 7% Mozambique 2%

11

Table 2.1: Cashew production, marketing, processing and export volumes estimates (MT)

Reference year Marketed pro-

duction Processed in

Nigeria

Source

(see Annex 3 - Literature Consulted)

2000/2001 184.000 ... FAO acc. to Chemonics 2002,

1

2001 80.000

... Chemonics 2002,1 -100.000

2003 60.000 ... New Nigerian Foundation

(NNF)

2003 90.000 ... Chemonics 2002, 2

2006 100.000

10.000 -15.000

Mr. Tunde (Abod Success Investment Co.) at the 2007 annual Meeting of the Afri-

can Cashew Alliance (ACA) in Maputo

2006

14.750

West Africa Trade Hub Cashew Market Study, Part 2

Planned:

2007: 21.900

2012: 45.000

2010 105.000 – 125.000*

... Nigerian Ministry of Com-

merce

2010 80.000

15.060 Resource persons met dur-

ing the mission -100.000

*) “Estimated Production”

The ambiguity of these figures stems from several factors:

Although the planting of Cashew trees was promoted

at certain times, a large part of the existing trees were

planted by individual farmers in an ad-hoc, generally

unplanned and piecemeal way (see Table 2.2);

There is no governmental body responsible for the sec-

tor that would integrate all actors and establish a prior-

ity for determining exact figures. The National Cashew

Association of Nigeria (NCAN) which is representing

processors and traders lacks the resources to do the

needed monitoring;

The processing sector is dominated by one major

player, OLAM, which a number of national companies

compete with and the company did not furnish data on

the volume of its exports of raw nuts and the prices;

Nigeria is a country with an estimated 135 million in-

habitants which constitute an increasing target market

for Cashew nuts as a snack, especially for nuts of lesser

quality. Some producers and backyard processors cater

directly to this local market and their sales volumes

cannot be estimated reliably.

12

Table 2.2: History/Development of the Cashew Sector in Nigeria

According to Ezeagu (2002)* and Nugawela & Oroch (2005), cultivation of Cashew started in the early 1950s, through the efforts of the then, Eastern And Western Nigeria Agricultural Development Associa-tions. The initial objective of these planting programmes was to use Cashew trees for soil erosion con-trol. Very little commercial attention was paid to Cashew due to the prominence of cocoa in the south west and oil palm in the south east.

Cashew is mainly a smallholder crop and supplements the incomes of many thousands of farmers across 18 States. A large number of people, mostly in low-income groups, generate an income from Cashew as growers, labourers, harvesters, local merchants/buyers, etc. Women play a vital role in the whole proc-ess, from Cashew harvesting to the labour intensive processing of nuts. In-addition, some large private plantations have been established, which are not particularly profitable.

In the 1970’s the old Eastern and Western regional governments established Cashew processing units to process the harvest from these government-owned plantations but the factories were unsustainable. Similarly, in the early 1980s the Oyo State government in partnership with private interests including Ol-tremare, the Italian Cashew machinery company, established a processing factory (Cashew Processing Industries Ltd.) in Ibadan to process the harvest from government-owned farms. The project could not be sustained because of infrastructural and management problems, and inefficiencies caused by gov-ernment bureaucracy (NNF, 2004).

During the 1990s, there have been a number of processing initiatives by private entrepreneurs. OLAM Nigeria Limited, (a subsidiary of OLAM International Limited) was established in 1989. It is a major ex-porter and processor of raw nuts and is extensively involved with other agricultural commodities in Ni-geria including cocoa, sesame, rice, cotton, sorghum and ginger. From Nigeria the company started to expand its business with Cashew processing and –trade and in the meantime is the biggest processor and trader of Cashew with a share of about 25% of the world market.

According to Ezeagu (2002), Cashew exports were not significant until the Nigerian economy was de-regulated in 1986, when fixed exchange rates and price fixing of commodities abolished, and commodity boards were wound up. After 1986 a large number of companies and individuals entered the Cashew market, resulting in an increase of production and exports. By 1995, an estimated 16,000 MT were ex-ported and the area under Cashew cultivation was estimated to be in the region of 40,000 hectares. In 2002, according to the Federal Ministry of Agriculture and Rural Development, annual production was 30,000 MT from a total area of 50,000 hectares.

However, for the year 2008/09 the Ministry of Commerce furnished estimates on the acreage and pro-duction of the individual states of the Federation that add up to 112,000 ha total acreage and a produc-tion volume of 105,000 MT (see Table 2), while some key informants of the mission estimated the acre-age to be higher, yet estimated similar production volumes of about 100,000 MT of raw Cashew nuts, with 15,000 to 20,000 MT processed in Nigeria and about 60,000 to 80,000 MT exported as RCN (see the following chapters).

*) For the indicated literature see Annex 3 – Literature Consulted

13

One link in the marketing chain that could theoreti-

cally be used to register marketed volumes are the

Produce Inspection Units for cash crops of the relevant

units of the MANR of the State Governments, which

do the ‘grading’ of the products at the point of bulk-

ing. However, data on the graded volumes were not

available due to a strike in part of the public sector at

the time of the mission. Also, since there is a grading

charge (1000 N/MT in Kwara state), any resulting data

would most likely be understated.

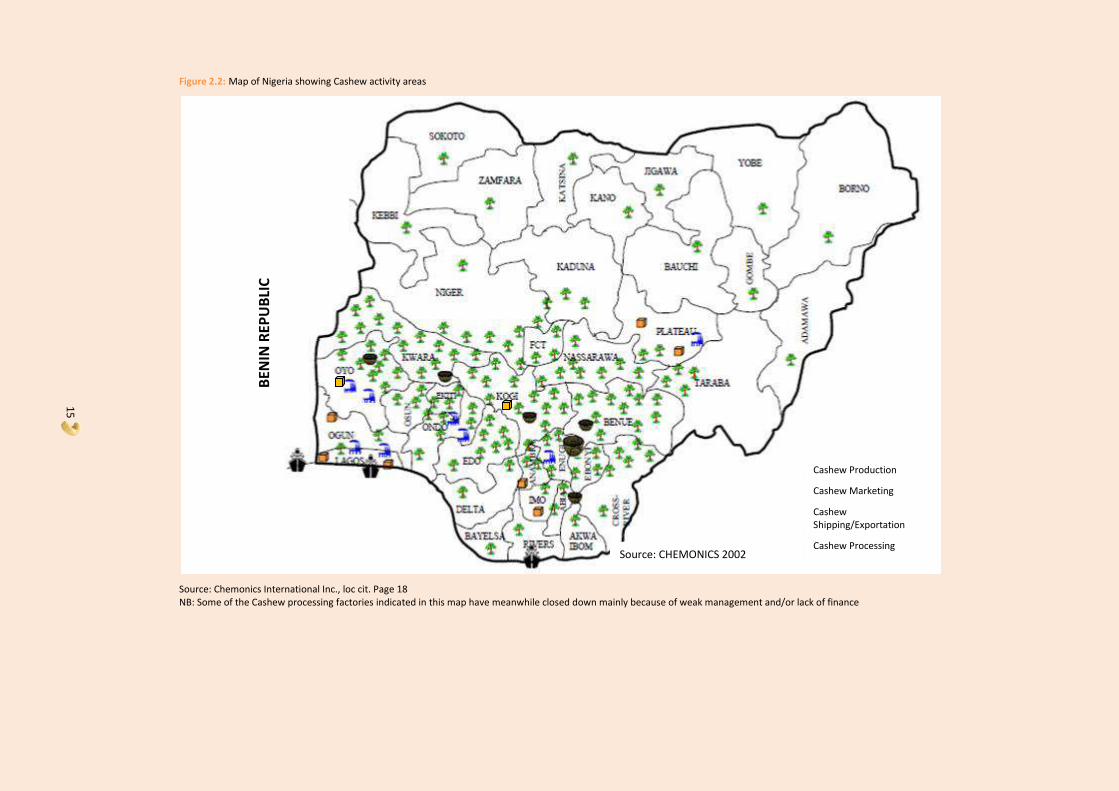

2.3 Regional distribution of production

According to the National Cashew Association of Nige-

ria (NCAN), the Cashew area is generally grouped into

3 blocks:

The South West, including of Edo, Ondo,

Osun, Ekiti and part of Oyo,

The South East, including of Imo, Anambra,

Enugu, Cross River and Ebonyi,

The North or Middle Belt, including Kwara,

Kogi, Benue, part of Oyo and other northern

states.

Resource persons linked to NCAN estimated that

roughly 30% of production comes from the South

West, 30% from the South East and 40% from the

Middle Belt and indicated Benue, Kogi, Kwara, Oyo,

Enugu, Abia, Anambra, Ekiti and Imo as major Cashew

producing states. The Cashew acreage for Oyo state

alone was indicated as being near 172,000 ha.

This information deviates in part from information

received after the mission’s end, which originates

from the Ministry of Commerce (MoC - see Table 2.3

on the following page). MoC furnished estimates of

the acreage and production data of the individual

states during the seasons 2007/08 and 2008/09 (Table

2.3, columns B to F). They combine to a national

Cashew acreage of 100,000 and 112,000 ha for the

agricultural years 2007/08 and 2008/09 respectively,

and corresponding national production volumes of

125,000 and 105,000 MT.

In the ranking of the states according to the produc-

tion volume estimates of MoC for 2008/09 (column J),

Kwara appears as the primary producer with 38% of

the total production, followed by Imo, Enugu, Kaduna

and Edo. Oyo contributed 1% only (but 7% in the

previous year) and Kogi a similarly insignificant volume

of 0.8%.

If ranked according to the Cashew acreage, in 2008/09

(column E) Kwara is followed by Imo, Edo, Enugu and

Ondo. Based on the acreage, Oyo and Kogi gain in

significance, then belonging to the 10 most important

Cashew growing states with 5.2% and 3.2% of the

national total.

However, lacking information on the way in which

these data have been collected and information that

would explain the obvious inconsistencies (marked in

red in the table), the data must be considered with

caution: There are missing figures (e.g. for Taraba),

out-of-range production figures for some states (e.g.

for Sokoto and Rivers) and unexplained large changes

in the acreage or the production volume between the

two years for some states (e.g. Edo, Oyo, Anambra,

Osun and Kogi). Some of these inconsistencies seem to

be caused by unchecked printing errors.

However, the MoC data correspond to the general

information on the regional distribution of Cashew

production: Even though Cashew is a plant that thrives

in semi-arid climates and can therefore be considered

more competitive compared to alternative crops when

grown in low rainfall areas, its production in Nigeria is

for historic reasons (see Box 1) concentrated in the

South and the Middle Belt, which receive over

1000 mm of precipitation per year. This means that

Cashew is competing there with cocoa or oil palm.

The concentration of production and the location of

processing facilities are visualised in the following map

taken from an earlier study (Figure 2.2; source

Chemonics 2).

14

Table 2.3: Estimated Cashew areas, production volumes, shares of the national total and yields

Rank State 2007/08 2008/09 Change C/E & D/F Share 2008/09 Yield 2008/09

Area Prod. Area Prod. Area (%) Prod. (%) ha (%) MT(%) (kg/ha)

A B C D E F G H I J K

1 Kwara 22.010 40.500 21.910 40.530 -0,5 0,1 19,6 38,6 1.850

2 Imo 12.910 8.560 12.920 8.570 0,1 0,1 11,5 8,2 663

3 Enugu 7.060 8.220 7.520 8.130 6,5 -1,1 6,7 7,8 1.081

4 Kaduna 4.390 8.070 4.370 7.690 -0,5 -4,7 3,9 7,3 1.760

5 Sokoto - - 730 5.680 0,7 5,4 7.781

6 Edo 1.190 5.730 7.620 5.560 540,3 -3,0 6,8 5,3 730

7 Kano 2.280 7.680 2.280 4.680 0,0 -39,1 2,0 4,5 2.053

8 Ebonyi 3.220 2.800 3.230 2.820 0,3 0,7 2,9 2,7 873

9 Ekiti 3.250 2.380 3.260 2.340 0,3 1,7 2,9 2,2 718

10 Delta 2.160 2.320 1.710 2.300 -20,8 -0,9 1,5 2,2 1.345

11 Niger 1.260 2.010 3.430 2.050 172,2 2,0 3,1 2,0 598

12 Kebbi 850 1.670 850 1.660 0,0 -0,6 0,8 1,6 1.953

13 Ogun 880 1.160 880 1.150 0,0 -0,9 0,8 1,1 1.307

14 Ondo 7.560 1.120 7.400 1.130 -2,1 0,9 6,6 1,1 153

15 Cross River 1.590 1.080 1.550 1.080 -2,5 0,0 1,4 1,0 697

16 Oyo 5.860 7.050 5.780 1.050 -1,4 -85,1 5,2 1,0 182

17 Nasarawa 2.240 1.190 2.310 1.040 3,1 -12,6 2,1 1,0 450

18 Anambra 5.190 6.010 5.200 1.010 0,2 -83,2 4,6 1,0 194

19 Osun 4.660 7.020 5.000 1.000 7,3 -85,8 4,5 1,0 200

20 FCT Abuja - 970 2.450 970 0,0 2,2 0,9 396

21 Lagos 1.540 900 1.470 900 -4,5 0,0 1,3 0,9 612

22 Plateau 930 870 980 890 5,4 2,3 0,9 0,8 908

23 Katsina 590 980 590 860 0,0 -12,2 0,5 0,8 1.458

24 Kogi 2.480 1.100 3.630 830 46,4 -24,5 3,2 0,8 229

25 Benue 2.430 1.480 2.450 480 0,8 -67,6 2,2 0,5 196

26 Abia 1.810 3.300 1.800 300 -0,6 -90,9 1,6 0,3 167

27 Akwa-Ibom - - 550 150 0,5 0,1 273

28 Rivers - - 10 40 0,0 0,0 4.000

29 Adamawa - - - - - -

30 Bauchi - - - - - -

31 Bayelsa - - - - - -

32 Borno - - - - - -

33 Gombe - - - - - -

34 Jigawa - - - - - -

35 Taraba 1.480 1.180 - - - -

36 Yobe - - - - - -

37 Zamfara - - - - - -

Total 99.820 125.350 111.880 104.890 12,1 -16,3 938

Source: Ministry of Commerce data, Dec. 2010 NB: Figures in red mark unexplained inconsistencies in the data Points are separators for figures with more than three digits; Commas mark fractions

15

Figure 2.2: Map of Nigeria showing Cashew activity areas

Source: Chemonics International Inc., loc cit. Page 18 NB: Some of the Cashew processing factories indicated in this map have meanwhile closed down mainly because of weak management and/or lack of finance

Cashew Production

Cashew Marketing

Cashew Shipping/Exportation

Cashew Processing

BEN

IN R

EPU

BLI

C

Source: CHEMONICS 2002

16

3 The Cashew value chain in the three states visited

3.1 Production

3.1.1 Importance of Cashew

As described above, obtaining reliable data on the Cashew

sector of individual states proved difficult. Especially the

number and percentage of farmers who grow Cashew is not

or only approximately known in the three states visited.

Figure 3.1 with the results of a random sample survey by the

ADP in Kwara state covering 20 farmers in each of the state’s

16 Local Government Areas (LGA) indicates how many of the

interviewed farmers grow certain perennial crops.

Figure 3.1: Percentage of Kwara state farmers growing specific crops

Source: Kwara State ADP 2009 Sample Survey

More farmers in the Kwara sample grow Cashew than any

other perennial type of plant, with Mango in a close second

place and Banana coming third. Extrapolated to the state

level, the percentage of farmers growing Cashew in the

sample corresponds to 173,000 Cashew growers state-wide.

One can therefore conclude that Cashew is of importance

for almost two thirds of the producers in Kwara state.

However, since no corresponding data could be obtained

for the other two visited states, the percentage of Cashew

producers in these remains unknown.

Apart from some of the large growers that are specialized on

Cashew production, usually a smallholder farm’s acreage

dedicated to other crops exceeds the Cashew acreage and is

used to grow annual food crops (e.g. cassava, yams, maize,

guinea corn/sorghum, beans, etc.) and some or other of the

remaining tree crops mentioned, e.g. cocoa, oil palm, citrus,

as well as banana and plantain.

3.1.2 Cashew production systems

In smallholder farms, various forms of growing Cashew can

be identified:

Around homesteads, providing shade and apples/nuts,

As hedgerows or boundaries,

As trees of variable number (5 to 30 per ha) in fields of

annual crops,

As isolated trees or clumps of trees without another

crop,

As regularly spaced tree monoculture with 70 or more

trees per hectare, depending on the spacing.

In the visited farms Cashew was grown either in the form of

clumps of trees or as more or less densely and regularly

spaced monoculture. Most often – and due to the lack of

advice before planting Cashew – the spacing observed in

plantation-style Cashew monocultures was too dense (less

than 10x10m) with tree canopies interlocking, which reduces

the yield per tree because the fruits mainly develop on the

outside of each tree’s canopy.

Operations are minimised in most smallholder farms and

include slashing of weeds once in the rainy season if trees

are more widely spaced and the removal of low branches

that impede weeding and harvesting. A second weeding

under the trees at the start of the harvesting period in Feb-

ruary is optional and obviously not carried out rigorously. It

also is hardly necessary when the trees form a dense can-

opy.

In a few widely spaced Cashew plantations the slashing

between the rows is done by tractor, and as well the slash-

ing and incorporation of vegetation around the Cashew

acreage to form a fire control strip. Most smallholders do

not carry out this operation at all or only haphazardly due to

the high manual labour input required and damage by fire is

an experience made by many interviewed growers unless

rigid community laws prevent fires, which are often started

by cattle herders in an effort to stimulate new growth of

grasses for their animals.

Also, the control of insects was found to be carried out as

needed only in exceptional cases. Several Cashew planta-

tions were encountered that showed insect damage, yet no

control measures were undertaken.

Most growers reported that they collect nuts fallen to the

ground and separating the apples and nuts at this moment

by twisting them apart. Few admitted to also pick or knock

fruits from the trees.

62% 57%

30%

5% 3% 1% 0%

10%

20%

30%

40%

50%

60%

70%

17

Most, but not all smallholders, report to dry the nuts on the

ground and some on cement pads for one or two days when

needed before selling them.

3.1.3 Cashew acreage per farm

Most of the producers interviewed individually grow Cashew

on only part of the acreage they exploit, ranging from a few

scattered trees to several tens of hectares. The farmers

interviewed indicated Cashew acreages ranging from 0.5 ha

to 270 ha (see Figure 3.2 below).

Figure 3.2: Frequency distribution of the Cashew acreage of the respon-dents

Source: Mission’s field data

Looking at this Cashew acreage distribution, the following

factors must be kept in mind:

Due to their better access to information and transport

facilities it is more common for the owners of larger

farms to attend meetings like the team’s kick-off meet-

ing for the visits in Kogi state, which was organized by

MANR in Lokoja.

Some visits to farms were pre-arranged by members of

the MANR or their direct regional contacts. This and

the wish to meet farmers who might keep records of

yields and inputs led to having more large farmers

among those visited.

Some smallholder farmers did not know their Cashew

acreage and most could only estimate approximately

the number of Cashew trees owned.

Based on additional information obtained during the mis-

sion, the percentage of farmers with Cashew acreages of

5 ha or less seems to exceed the 56% of the total, which the

combined total of the lowest three size groups in Figure 3.2

represents, and probably even is in excess of 75%.

Also, if the percentage of Cashew growers reported for the

sample survey in Kwara is projected to the state level (61.5%

of 280,000 farm families in total) and related to the acreage

reported for Kwara by the Ministry of Commerce, the aver-

age acreage per grower is even lower and only between 0.1

and 0.2 ha.

For the purposes of the study, the Cashew acreage of a

typical smallholder that produces RCN for sale and has an

established proper Cashew plot, is estimated at 2 ha.

3.1.4 Ownership and availability of land for Cashew production

The majority of the surveyed Cashew farmers own their

land, while about one third lease it. Those leasing were

either immigrant farmers, or farmers leasing Cashew plots

established previously by MANR.

All informants said that availability of additional land to

expand the Cashew acreage was not a problem. This is no

surprise as most smallholders have difficulties to obtain

fertiliser at the official subsidised price and therefore prac-

tice shifting cultivation, in which part of the land is at any

time recovering during the fallow period as bush-land.

3.1.5 Yields/ha of raw Cashew nut

There is an obvious discrepancy between the average yields

that can be calculated with the data provided by the Minis-

try of Commerce and the data reported to the mission by

key informants and smallholders. The MoC data lead to

productivity figures ranging from 153 kg/ha to about

2000 kg/ha (with still higher figures considered to be due to

typing errors), and a national average of around 900 kg/ha

results from these (see Table 2, last column).

In contrast, the interviewed farmers that were able to re-

spond to the question reported yields ranging from virtually

“zero” to 750 kg/ha. Over half indicated yields of 250 kg/ha

and less, about a quarter yields between 250 and 500 kg/ha

and another quarter yields between 500 and 750 kg/ha.

All these numbers must be seen as approximations, high-

lighted by the finding that almost half of the contacts in Kogi

State and a quarter in Oyo State could not indicate their

Cashew production volume at all - even for the present year

2010, which is seen as an indication that the yields they

obtained were most likely in the lower range.

The inability to provide yield data is understandable for two

reasons: (1) the total amounts harvested weekly over a

period of almost 3 months from February to April are in

some cases quite small as most smallholders immediately

sell the collected nuts after harvesting. Also the growers do

not possess any written sales records and therefore cannot

provide a reliable estimate of the cumulative total sold.

Often volumes are measured in containers - “mudu” – the

size of which varies from farm to farm. (2) Since the Cashew

trees on smallholder farms are often not established as a

plantation-type monoculture it is difficult to estimate the

0

1

2

3

4

5

6

No

. of

case

s

18

area and usually these farmers do neither know the area,

nor the number of trees, nor the production volume.

Based on the MoC data for the season 2008/09, low yields of

around 200 kg/ha result for Kogi and Oyo, while for Kwara

the computed value is 1850 kg/ha. The reported high pro-

ductivity for Kwara clashes with figures obtained during the

interviews conducted by the team and interviews conducted

in 2008 in Kwara and Nasarawa by Topper, which also indi-

cated low productivities of around 250 kg/ha.

The conclusion drawn by the mission and confirmed by the

visual verification of Cashew plots, is that the overwhelming

majority of Cashew plots are low yielding, producing around

250 kg/ha or even less. Therefore, in the following we as-

sume an average yield of 250 kg/ha on a smallholder farm

with the present production practices.

3.2 Marketing and Processing

3.2.1 The marketing chains

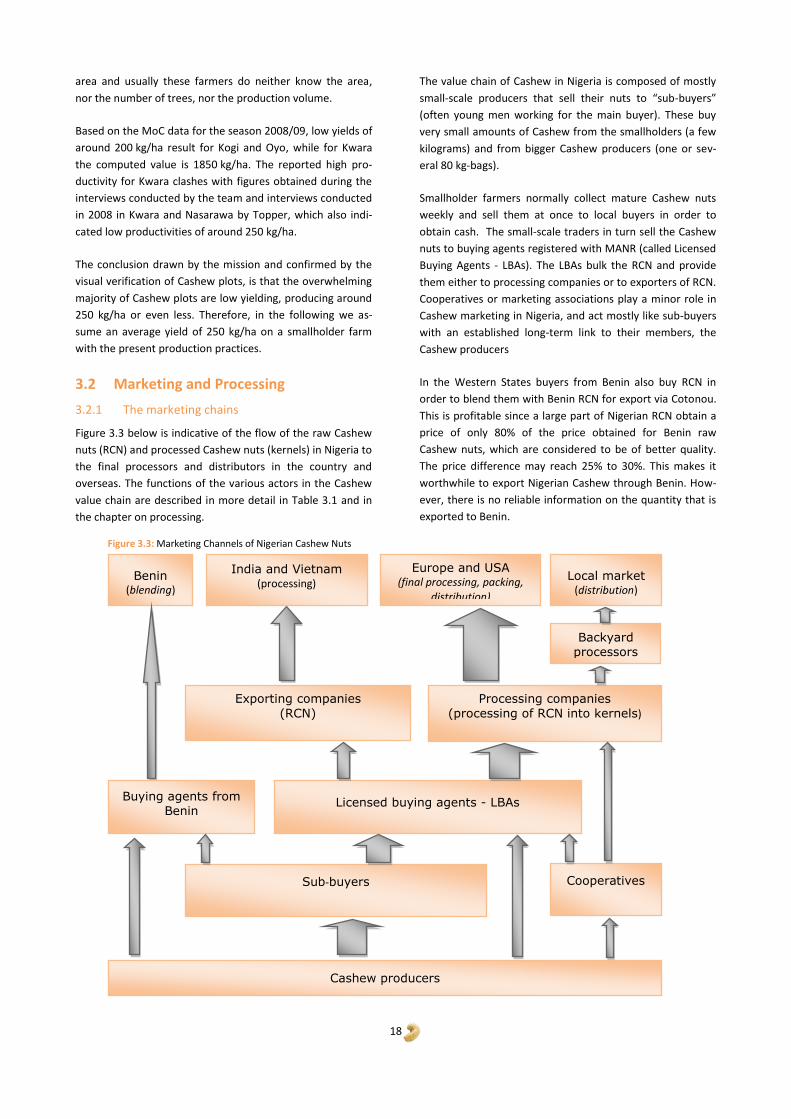

Figure 3.3 below is indicative of the flow of the raw Cashew

nuts (RCN) and processed Cashew nuts (kernels) in Nigeria to

the final processors and distributors in the country and

overseas. The functions of the various actors in the Cashew

value chain are described in more detail in Table 3.1 and in

the chapter on processing.

The value chain of Cashew in Nigeria is composed of mostly

small-scale producers that sell their nuts to “sub-buyers”

(often young men working for the main buyer). These buy

very small amounts of Cashew from the smallholders (a few

kilograms) and from bigger Cashew producers (one or sev-

eral 80 kg-bags).

Smallholder farmers normally collect mature Cashew nuts

weekly and sell them at once to local buyers in order to

obtain cash. The small-scale traders in turn sell the Cashew

nuts to buying agents registered with MANR (called Licensed

Buying Agents - LBAs). The LBAs bulk the RCN and provide

them either to processing companies or to exporters of RCN.

Cooperatives or marketing associations play a minor role in

Cashew marketing in Nigeria, and act mostly like sub-buyers

with an established long-term link to their members, the

Cashew producers

In the Western States buyers from Benin also buy RCN in

order to blend them with Benin RCN for export via Cotonou.

This is profitable since a large part of Nigerian RCN obtain a

price of only 80% of the price obtained for Benin raw

Cashew nuts, which are considered to be of better quality.

The price difference may reach 25% to 30%. This makes it

worthwhile to export Nigerian Cashew through Benin. How-

ever, there is no reliable information on the quantity that is

exported to Benin.

Cashew producers

Sub-buyers

Licensed buying agents - LBAs

Cooperatives

Backyard processors

Processing companies

(processing of RCN into kernels)

Local market (distribution)

Europe and USA (final processing, packing,

distribution)

Benin (blending)

Exporting companies (RCN)

India and Vietnam (processing)

Buying agents from Benin

Figure 3.3: Marketing Channels of Nigerian Cashew Nuts

19

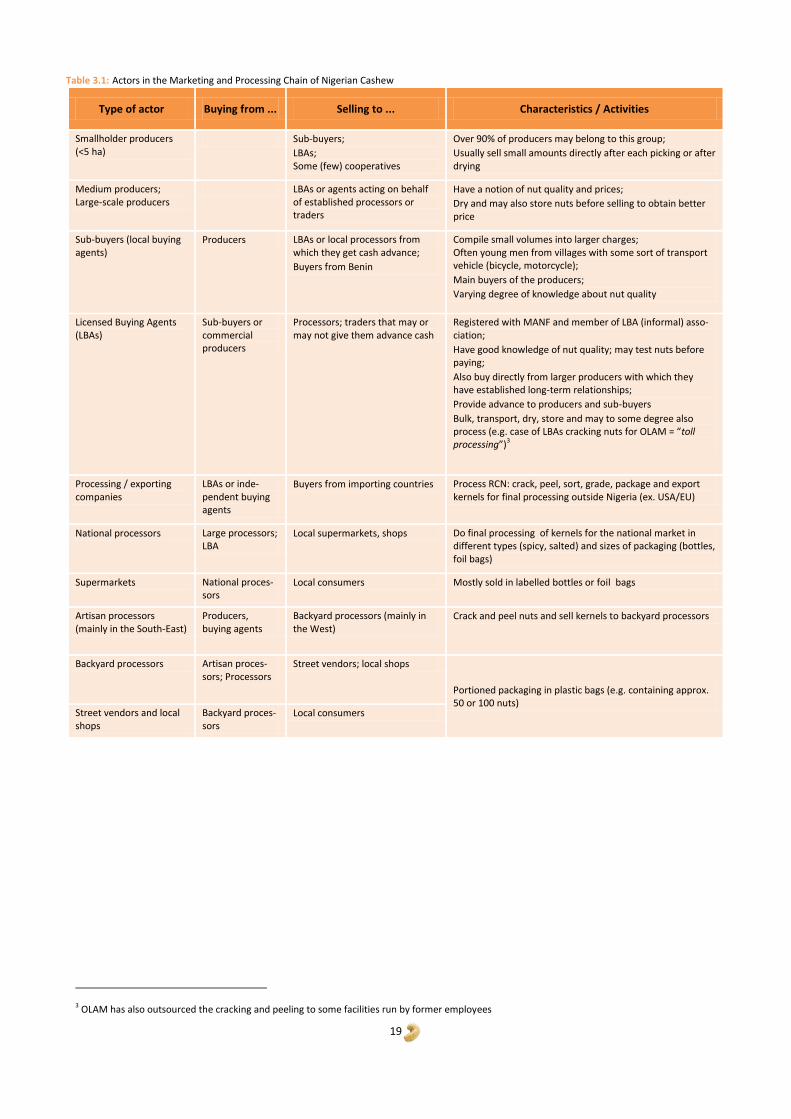

Table 3.1: Actors in the Marketing and Processing Chain of Nigerian Cashew

Type of actor Buying from ... Selling to ... Characteristics / Activities

Smallholder producers (<5 ha)

Sub-buyers;

LBAs; Some (few) cooperatives

Over 90% of producers may belong to this group;

Usually sell small amounts directly after each picking or after drying

Medium producers; Large-scale producers

LBAs or agents acting on behalf of established processors or traders

Have a notion of nut quality and prices;

Dry and may also store nuts before selling to obtain better price

Sub-buyers (local buying agents)

Producers LBAs or local processors from which they get cash advance;

Buyers from Benin

Compile small volumes into larger charges; Often young men from villages with some sort of transport vehicle (bicycle, motorcycle);

Main buyers of the producers;

Varying degree of knowledge about nut quality

Licensed Buying Agents (LBAs)

Sub-buyers or commercial producers

Processors; traders that may or may not give them advance cash

Registered with MANF and member of LBA (informal) asso-ciation;

Have good knowledge of nut quality; may test nuts before paying;

Also buy directly from larger producers with which they have established long-term relationships;

Provide advance to producers and sub-buyers

Bulk, transport, dry, store and may to some degree also process (e.g. case of LBAs cracking nuts for OLAM = “toll processing”)3

Processing / exporting companies

LBAs or inde-pendent buying agents

Buyers from importing countries Process RCN: crack, peel, sort, grade, package and export kernels for final processing outside Nigeria (ex. USA/EU)

National processors Large processors; LBA

Local supermarkets, shops Do final processing of kernels for the national market in different types (spicy, salted) and sizes of packaging (bottles, foil bags)

Supermarkets National proces-sors

Local consumers Mostly sold in labelled bottles or foil bags

Artisan processors (mainly in the South-East)

Producers, buying agents

Backyard processors (mainly in the West)

Crack and peel nuts and sell kernels to backyard processors

Backyard processors Artisan proces-sors; Processors

Street vendors; local shops

Portioned packaging in plastic bags (e.g. containing approx. 50 or 100 nuts)

Street vendors and local shops

Backyard proces-sors

Local consumers

3 OLAM has also outsourced the cracking and peeling to some facilities run by former employees

20

The described marketing chains reflect the most common

cases but also include less frequent market linkages, e.g.

LBAs buying RCN directly from commercial producers and

medium sized growers. Not shown are specific and less

frequent cases, e.g. backyard processors buying cracked nuts

from small artisanal cracking enterprises.

The processing companies process RCN into Cashew kernels

which they export to the world market - mainly to Europe

and the USA. Exporters of RCN sell the product mainly to

India and Vietnam, where the nuts are processed and the

kernels are then exported to Asian countries such as China

and Australia, but to Europe and the USA as well.

As mentioned above, most smallholders are cash-strapped

and sell the nuts directly after each round of collection. Few

are financially able to store the nuts and sell after the end of

the harvesting season or still later in the year when the price

of RCN increases. This requires proper harvesting and post-

harvesting techniques, and adequate facilities for drying and

storing the raw nuts.

In the actual system the nuts are sold by the smallholder

producers to any sub-buyer that procures nuts in the villages

and is offering an acceptable price. Thus, a producer’s buyer

may vary from batch to batch that has been collected. The

possibility of the producers receiving advance payments to

pay hired labour for weeding and/or harvesting are minimal

in this system.

The case is often different when the nuts are sold to LBAs or

Sub-buyers of the major processors or traders (OLAM or

national companies like ABOD Success Co.). These do often

provide producers with which they have longer-lasting rela-

tionships with advance money. Such advance payments are

deducted at the time of delivery of the produce. For the

producer they signify an obligation to sell at least corre-

sponding volumes of production to the provider of the short-

term credit and this limits their choice of action. For the

buyer they is some form / method of ensuring to obtain a

foreseeable / the agreed volume of nuts. Even though farm-

ers and LBAs claim that the farmers do not have to pay

interest in this system it can be assumed that interest is

indeed paid in the form of a lower price that farmers obtain.

Since there are no written contracts or invoices or receipts,

the system is not transparent.

3.2.2 Processing operations

Raw Cashew Nuts can be processed in order to produce

kernels that can be exported to the main consuming markets

in North America or Europe, where the final processing

(salting/ seasoning and packaging) is done before their dis-

tribution to wholesalers and retailers.

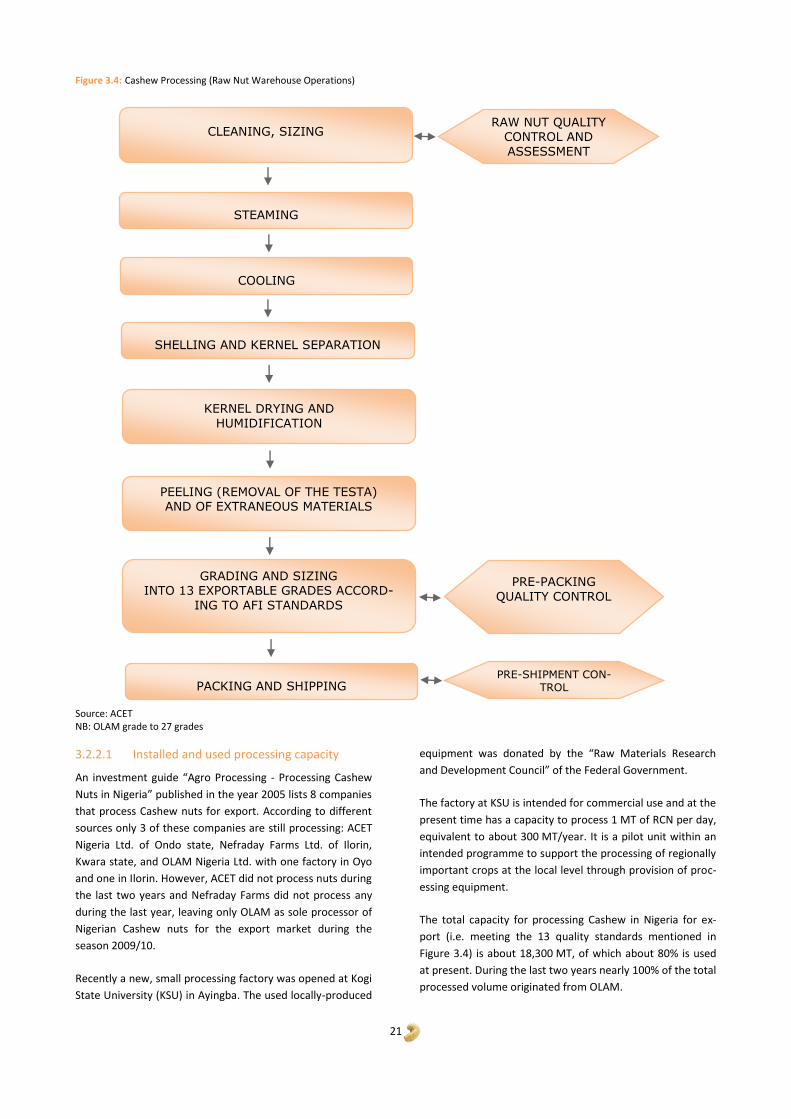

The processing of RCN to kernels creates value added but

this is a labour intensive process that involves several dis-

tinct steps (see Figure 3.4 – Cashew Processing). About 6 to

7 labour days are needed to produce 20 kg of exportable

kernels. Labour costs are therefore a major cost item of the

processors and the processing cost depends in large part on

the wage level and the worker’s efficiency, two factors that

favour processing in Asia.

According to OLAM, the multi-national processing/trading

company of Indian/Singapore origin, the lower efficiency of

the workers and the existence of a minimum wage rate in

Nigeria results in higher unit costs for cracking, peeling or

grading than in India or Vietnam.

Since work in Cashew processing is considered demanding,

staff turnover has initially been high in Nigeria. OLAM has

recently managed to reduce the turnover rate by hiring

mainly female labour for processing and by outsourcing the

cracking and peeling of RCN. This has helped to improve the

efficiency and to lower the cost differential between proc-

essing in Nigeria and Asia.

21

Figure 3.4: Cashew Processing (Raw Nut Warehouse Operations)

Source: ACET NB: OLAM grade to 27 grades

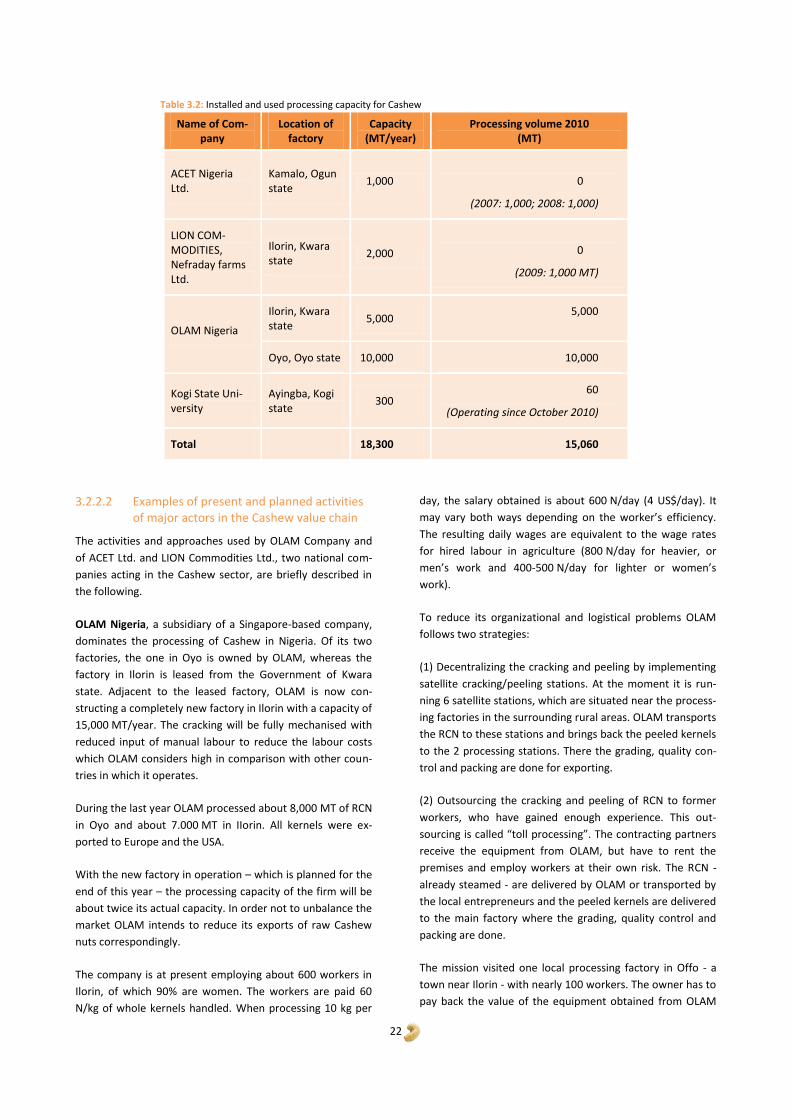

3.2.2.1 Installed and used processing capacity

An investment guide “Agro Processing - Processing Cashew

Nuts in Nigeria” published in the year 2005 lists 8 companies

that process Cashew nuts for export. According to different

sources only 3 of these companies are still processing: ACET

Nigeria Ltd. of Ondo state, Nefraday Farms Ltd. of Ilorin,

Kwara state, and OLAM Nigeria Ltd. with one factory in Oyo

and one in Ilorin. However, ACET did not process nuts during

the last two years and Nefraday Farms did not process any

during the last year, leaving only OLAM as sole processor of

Nigerian Cashew nuts for the export market during the

season 2009/10.

Recently a new, small processing factory was opened at Kogi

State University (KSU) in Ayingba. The used locally-produced

equipment was donated by the “Raw Materials Research

and Development Council” of the Federal Government.

The factory at KSU is intended for commercial use and at the

present time has a capacity to process 1 MT of RCN per day,

equivalent to about 300 MT/year. It is a pilot unit within an

intended programme to support the processing of regionally

important crops at the local level through provision of proc-

essing equipment.

The total capacity for processing Cashew in Nigeria for ex-

port (i.e. meeting the 13 quality standards mentioned in

Figure 3.4) is about 18,300 MT, of which about 80% is used

at present. During the last two years nearly 100% of the total

processed volume originated from OLAM.

CLEANING, SIZING

STEAMING

COOLING

SHELLING AND KERNEL SEPARATION

KERNEL DRYING AND

HUMIDIFICATION

PEELING (REMOVAL OF THE TESTA) AND OF EXTRANEOUS MATERIALS

GRADING AND SIZING

INTO 13 EXPORTABLE GRADES ACCORD-

ING TO AFI STANDARDS

PACKING AND SHIPPING

PRE-PACKING

QUALITY CONTROL

RAW NUT QUALITY CONTROL AND

ASSESSMENT

PRE-SHIPMENT CON-TROL

22

Table 3.2: Installed and used processing capacity for Cashew

Name of Com-pany

Location of factory

Capacity (MT/year)

Processing volume 2010 (MT)

ACET Nigeria Ltd.

Kamalo, Ogun state

1,000

0

(2007: 1,000; 2008: 1,000)

LION COM-MODITIES, Nefraday farms Ltd.

Ilorin, Kwara state

2,000

0

(2009: 1,000 MT)

OLAM Nigeria

Ilorin, Kwara state

5,000 5,000

Oyo, Oyo state 10,000 10,000

Kogi State Uni-versity

Ayingba, Kogi state

300 60

(Operating since October 2010)

Total 18,300 15,060

3.2.2.2 Examples of present and planned activities

of major actors in the Cashew value chain

The activities and approaches used by OLAM Company and

of ACET Ltd. and LION Commodities Ltd., two national com-

panies acting in the Cashew sector, are briefly described in

the following.

OLAM Nigeria, a subsidiary of a Singapore-based company,

dominates the processing of Cashew in Nigeria. Of its two

factories, the one in Oyo is owned by OLAM, whereas the

factory in Ilorin is leased from the Government of Kwara

state. Adjacent to the leased factory, OLAM is now con-

structing a completely new factory in Ilorin with a capacity of

15,000 MT/year. The cracking will be fully mechanised with

reduced input of manual labour to reduce the labour costs

which OLAM considers high in comparison with other coun-

tries in which it operates.

During the last year OLAM processed about 8,000 MT of RCN

in Oyo and about 7.000 MT in IIorin. All kernels were ex-

ported to Europe and the USA.

With the new factory in operation – which is planned for the

end of this year – the processing capacity of the firm will be

about twice its actual capacity. In order not to unbalance the

market OLAM intends to reduce its exports of raw Cashew

nuts correspondingly.

The company is at present employing about 600 workers in

Ilorin, of which 90% are women. The workers are paid 60

N/kg of whole kernels handled. When processing 10 kg per

day, the salary obtained is about 600 N/day (4 US$/day). It

may vary both ways depending on the worker’s efficiency.

The resulting daily wages are equivalent to the wage rates

for hired labour in agriculture (800 N/day for heavier, or

men’s work and 400-500 N/day for lighter or women’s

work).

To reduce its organizational and logistical problems OLAM

follows two strategies:

(1) Decentralizing the cracking and peeling by implementing

satellite cracking/peeling stations. At the moment it is run-

ning 6 satellite stations, which are situated near the process-

ing factories in the surrounding rural areas. OLAM transports

the RCN to these stations and brings back the peeled kernels

to the 2 processing stations. There the grading, quality con-

trol and packing are done for exporting.

(2) Outsourcing the cracking and peeling of RCN to former

workers, who have gained enough experience. This out-

sourcing is called “toll processing”. The contracting partners

receive the equipment from OLAM, but have to rent the

premises and employ workers at their own risk. The RCN -

already steamed - are delivered by OLAM or transported by

the local entrepreneurs and the peeled kernels are delivered

to the main factory where the grading, quality control and

packing are done.

The mission visited one local processing factory in Offo - a

town near Ilorin - with nearly 100 workers. The owner has to

pay back the value of the equipment obtained from OLAM

23

“on credit” within three years. This is done without a formal

credit contract, so the local entrepreneur does not know the

total investment of his business. The repayment is done by

deducting the principal and unknown interest from the

amount payable for the processing.

The entrepreneur in Offo town is only doing the cracking and

is paid 100 N/kg of RCN by OLAM. After deducting 75 N/kg

for salaries, 25 N/kg remain to cover the rent for the prem-

ises, the supervisor, the costs for the transport of RCN and

the kernels and overhead costs such as energy and his en-

trepreneur’s income.

Even though the agreement appears not very transparent,

the factory owner pronounced himself satisfied with it and

reported that this way he earns much more than as a worker

of OLAM. The difficulties with the employees, of which also

90% are female, are reportedly less than those OLAM faced

because of a more intimate relationship between manager

and workers and a resulting higher commitment of the

employees to the factory.

ACET Ltd. started to process Cashew in the late 1990s. Its

factory was built in 2005 for a capacity of 4 MT RCN per day.

With 250 working days per year the total annual capacity is

about 1000 MT. During the seasons 2007 and 2008 the

company processed about 1000 MT per year and exported

the kernels.

However, during the last two years ACET did not process any

Cashew since it could not finance the purchase of raw mate-

rials. This was due to two reasons: ACET could not obtain

credit from a commercial bank and also has not yet received

the export subsidy for its 2007 exports from the Nigerian

Export Promotion Council (NEPC) on which it counted. Based

on an announcement that during the next few weeks the

outstanding payments would be paid the company owner

intends to resume processing in the 2011 season.

The company owner is convinced quality problems can be

overcome by a more direct relationship between producers

and processors in which the Buying Agents are bypassed.

ACET plans to buy raw nuts from the farmers directly in the

future by setting up four collection centres. The owner also

plans to contract the Sustainable Tree Crops Program (Africa

- STCP) at the Cocoa Research Institute of Nigeria (CRIN) in

Ibadan to provide extension support to the cooperating

farmers, specifically to improve nut quality.

While this is a laudable approach, some doubts remain as to

its feasibility, which depends on the capacity of CRIN to

provide extension services to several hundred farmers and

regarding the capacity of ACET to finance such extra services

to the farmers:

Assuming the actual average yield of 250 kg/ha and a

planned volume of 1,000MT RCN/year, ACET would

have to purchase the entire production of about

4,000 ha. Even if the company cooperated mainly with

the bigger farmers with an average Cashew acreage of

10 ha, it would need 400 cooperating partners. In order

to provide the extension services efficiently, these 400

persons would have to be grouped. With 20 members

per group about 20 groups would have to be trained

and/or accompanied. This training can be done by one

full time technician under condition that transport is

available and that extension material has been pre-

pared and is ready for use.

Another challenge is the grouping of the farmers be-

cause the members of a group have to live near to each

other in one or two villages. Experience shows that

farmers do not easily trust each other and that effec-

tive cooperation among group members is often diffi-

cult to achieve.

Also, the extension system’s costs are significant for a

comparatively small processing factory.

Lastly, ACET might be unable to benefit sufficiently

from this strategy because in addition to the costs of

the extension system it would also have to pay its pro-

ducers a higher price for the raw nuts of better quality,

which might eat up / erode the price differential now

reaped by the Buying Agents.

In Ilorin there is also a Cashew processing facility of the

group “LION Commodities Ltd.” with a capacity of about

2,000 MT of RCN/year. This processing facility also was not

producing during 2009 because of financing problems. In

previous years processed kernels were exported to the UK,

the Netherlands and the RSA.

The General Manager told the mission that he intends to

resume processing in the coming season but would probably

concentrate on the final processing (salting and spicing of

already processed kernels) for the domestic market. As yet

this seems to be a first idea and there was no clear strategy

yet on how to realise this option.

3.2.2.3 Processing for the domestic market

Besides industrial processing for export markets, some low-

volume processing is already done for the domestic market

by so-called ‘backyard processors’. These may undertake all

operations themselves or get supplies of kernels. Most com-

panies have different sources of kernels: some buy the ker-

nels from OLAM (normally the lower qualities, i.e. broken,

small or not white or spotted kernels) and some from ar-

tisanal processors, mainly in the South-East. After cracking

and peeling the nuts, the produced kernels are sold by street

vendors or in local shops – usually without any salting and

spicing.

24

The artisanal processors - in the South-East of the country

that could not be visited by the mission - are said to roast

the nuts on open fires and crack them using hammers

and/or knives.

However, one such processor visited in Ilorin was equipped

with a simple boiler for conditioning of the nuts and four

locally manufactured crackers (copies of imported Indian

crackers) and processed about 30 tons of RCN per year. This

female entrepreneur is selling the kernels to shops in Ilorin

and Lagos. Production was said to be restricted to a period

of three to four months per year because financial con-

straints limit the volume of raw nuts that can be bought and

stored.

The procurement of the kernels appears to be a big problem

for the small-scale processors and it is one of the factors

limiting expansion of their operations.

There are some other processors that do only the final proc-

essing, i.e. the salting and/or the spicing of kernels. The

kernels are bought from OLAM and/or from small-scale

processors. After the salting or spicing the kernels are

manually filled into bottles which are also capped and la-

belled manually. The quality of the samples bought by the

mission in the market was low due to a high percentage of

spotted, undersize, broken or not properly cleaned kernels.

The small scale processors do the final processing such as

salting and/or spicing and packing and sell the final to the

local market, supermarkets, hotels or restaurants.

All interviewed small-scale processors told us, that they

could sell three to five times more processed kernels on the

domestic market if they could get kernels and financing for

expansion. The total quantity of RCN, which is sold as finally

processed kernels on the domestic market was estimated by

some small scale processors to be about 5,000 MT to 10,000