Jahresbericht 2004 Pantone - FINMA - Willkommen€¦ · 2 Bundesamt für Privatversicherungen BPV...

36

www.bpv.admin.ch Bundesamt für Privatversicherungen BPV Office fédéral des assurances privées OFAP Ufficio federale delle assicurazioni private UFAP Swiss Federal Office of Private Insurance FOPI Annual report 2004

Transcript of Jahresbericht 2004 Pantone - FINMA - Willkommen€¦ · 2 Bundesamt für Privatversicherungen BPV...

www.bpv.admin.ch

Bundesamt für Privatversicherungen BPVOffice fédéral des assurances privées OFAPUfficio federale delle assicurazioni private UFAPSwiss Federal Office of Private Insurance FOPI

Annual report

2004

2

Bundesamt für Privatversicherungen BPVOffice fédéral des assurances privées OFAPUfficio federale delle assicurazioni private UFAPSwiss Federal Office of Private Insurance FOPI

PublisherBundesamt für Privatversicherungen BPVFriedheimweg 14CH-3003 Bernewww.bpv.admin.ch

DesignBasel West Unternehmenskommunikation AG, Basel

PrintingDietschi AG, Waldenburg

DistributionSFBL, Distribution of Publications, CH-3003 Bernewww.bbl.admin.ch/bundespublikationenNo 622.104.eng

Order by Internetwww.bbl.admin.ch/bundespublikationen

Annual report 2004

3

Index

IntroductionInsurance supervision in Switzerland: from the old world to the new world 4

Report on activitiesTotal revision of the ISL / Partial revision of the ICL: Implementation can begin 8

Swiss Solvency Test – first trial run conducted in 2004 10

Supervision of insurance brokers 12

Reorientation of non-life insurance supervision 13

Group and conglomerate supervision 14

Implementation of the transparency requirements for the insurance of occupational pensions 16

Compulsory transfer of portfolios / Supervision problems with bankrupt health insurance schemes 18

Market overviewSwiss private insurers – a market overview 20

The worldwide business of the five largest insurance-based groups – an overview 33

4Introduction

BackgroundTwo and a half years ago, in the summer and autumn of2002, insurance supervision was a highly charged politi-cal issue. The basic question concerned whether the ex-isting system of supervision could still meet the demandsof the greatly changed economic environment. Thisquestion was largely answered in the negative, and anew orientation was called for. Today, the definition of this new orientation is largelycomplete. We not only know where the journey is head-ed, but the essential elements have also been devel-oped. This annual report is part of this effort and aims toincrease transparency. It serves to account for our activi-ties and the status of implementation of the new orien-tation. I am pleased that we may present ourselves tothe public with this publication and brief you on our coreactivities. And not only that: For the first time, we areable to give you a current market overview. In a simpleand clear manner, the overview shows how the sectorperformed in 2004. With this overview, we are fulfillinga need that has been communicated to us repeatedlyover the last three years, but that we had until now onlybeen able to fulfil in the second half of the year.

Why is there a need for supervision?Insurance companies and banks, unlike most other busi-ness sectors, are supervised by the State. Why? In thecase of insurance companies, the main reason is that in-surance protection is often of great, even existential im-portance for individual insured persons. At the sametime, the processes in these companies are very complexand difficult to grasp.The economic importance for the individual in our coun-try is also demonstrated by the fact that, for example,the Swiss are ranked number one worldwide in per capi-ta expenditures for insurance: They spend about 7000Swiss francs per year on insurance – not including socialsecurity contributions. In return, they are entitled tocompensation for insured damage, payment of hospitalbills, and actual payment of occupational pensions forwhich they have paid premiums over the course of theirworking life. In short: They are entitled to a high level ofsecurity. And of course, the appropriate premium shouldbe paid for this security, namely exactly as much as isnecessary to cover potential damage.

Herbert Lüthy, Director

The central responsibility of supervision is to protectthese fundamental interests of insured parties. Since the beginnings of insurance supervision, this has result-ed in the definition of a dual task for the responsibleauthority:

� protection of the insured party from abuse � protection of the insured party from insolvency ofan insurance institution.

As facile as this task may seem at first glance, as com-plex and time-consuming it ultimately is in practice: Pro-tection from insolvency in particular, which must beguaranteed over the long term, places high demands onthe responsible supervisory authorities.

Supervision in the past: from the old world…Until now, this task in Switzerland has primarily been ful-filled through prior approval of the insurance productsby the supervisory authority. The focus was on approvalof the premium; i.e. a premium that was neither abusivenor a threat to solvency.But the „right“ premium alone does not suffice to pre-vent insolvencies of insurance institutions; not, for ex-ample, if the insurer’s reserves plummet below the nec-essary minimum due to unforeseen developments, or ifits equalization fund is not adequate, i.e., its capital re-sources are insufficient. In addition, the functioning mar-ket has an effect. For reasons of competition, individualmarket participants may decide to reduce their premi-ums to a minimum and simultaneously distribute sur-pluses rather than retain them. These mechanisms led tothe understanding that the central element of effectiveinsurance supervision cannot be preventive productmonitoring, but rather comprehensive solvency monitor-ing, in conjunction with general protection from abuse.

Insurance supervision in Switzerland:from the old world to the new world

5

…to the new worldIn practically all countries, these insights have led to afundamental rethinking of the supervision philosophyand of supervision law. Also in Switzerland: with thenew Insurance Supervision Law (ISL), our country is re-ceiving modern legislation. This legislation takes into ac-count the developments of recent years in three ways:

� Maintenance of preventive product monitoring insocially sensitive areas, namely occupational pen-sions („collective life“) and in supplemental healthinsurance pursuant to the Insurance Contract Law(ICL). Product monitoring will therefore continue tobe an important activity.� Extension of protection from abuse, especially byintroducing broker supervision and extending re-quirements with respect to corporate governance.However, expectations should not be too high in thisarea. The over 12’000 brokers and insurance agentswho operate in Switzerland cannot be supervised„up close“. Broker supervision must therefore limititself to the monitoring of key points such as regis-tration (as a seal of approval of relevant expertise),training, and appropriate liability insurance. In thearea of corporate governance, i.e. the monitoring ofgood business management, the law only providesfor general requirements. The focus here is currentlyon the step-by-step implementation of a process ofnewly developed quality review.� Greater emphasis on solvency protection, espe-cially by introducing the legislative requirement totake into account the risk profile of the insurance en-terprise. This is at the heart of the new supervisoryphilosophy – accordingly, the following discussionwill pay special attention to it.

The „new“ risk-based solvency supervisionThe central question for solvency supervision is how sol-vency can be ensured in the first place. The first step is tosecure the appropriate reserves. Then, the correct equal-ization fund must be provided, which essentially corre-sponds to equity capital. The solvency margin providesinformation on the amount of this equalization fund.The monitoring of correctly structured reserves and thesolvency margin of the insurance institutions accordinglyshift into the focus of risk-based supervision activity. Aspart of its risk-based supervision, FOPI will therefore is-sue very specific guidelines for calculating reserves. Espe-cially in the case of damage insurers, the process for cal-

culating the correct reserves is defined as a risk processthat should lead to the evaluation of the fundamentaldata. The plan is to implement this process through self-assessments of insurers themselves, subject to monitor-ing by the supervisory authority. In addition – as will beexplained in more detail below – an additional solvencyvalue will be introduced on a completely new basis.

Solvency IIThe rules currently applicable to the calculation of sol-vency, i.e. the equity capital of the insurance institution,are based on the so-called „Solvency I“ process of theEU. Switzerland implemented these rules throughamendments to the old ISL. These Solvency I principleswill continue to hold and have been integrated into thenew ISL.At the same time, it is undisputed both within the EUand in Switzerland that the definitions for calculatingsolvency in accordance with Solvency I do not suffice.They are insufficiently differentiated and, in particular,do not take into account the risk profile of the insuranceportfolio. The corresponding capital deposit require-ments therefore also do not reflect the risk-oriented cap-ital need. International rating agencies have thereforelong consulted risk-based measures in order to evaluatethe financial strength of insurance companies. How nec-essary such an approach is was demonstrated to thebroader public in a dramatic way when the stock mar-kets collapsed (approximately March 2000 to March2002): Many insurance companies worldwide ran intosevere difficulties, since their equalization funds had notadequately taken the capital risk into account.The discussions in this regard are being conducted in theEU under the name „Solvency II“ – in a certain analogyto Basel II in the field of bank supervision. At the sametime, important differences between insurance compa-nies and banks must be taken into account. In the caseof insurance, the dependencies between risk concentra-tions, risk aggregations, and risk diversifications play asignificantly greater role. In addition, insurance supervi-sion is in general also subject to the desire of politics and society that insurers take on parts of the social secu-rity net.

6

The questions to be dealt with are accordingly complex.The Solvency II discussion has already led to very good,generally accepted principles, but has not yet led to anyconcrete implementation. As always, the devil is in thedetails, and it should therefore be expected that muchwork remains to be undertaken in the EU until the Sol-vency II rules can be adopted as general directives andattain the force of law in the EU States. This will likelynot be the case before 2008 and could even take until2010 or 2012. Switzerland does not want to and cannotwait that long.

The situation in Switzerland: new ISL and new Supervision OrdinanceThe principles of Solvency II that are already available,the pilot projects undertaken in Switzerland, and therisk-based models used in other countries (such asAustralia, Canada, the United Kingdom, and the UnitedStates) show that the consideration of risk in calculatingnecessary capital resources not only results in many dif-ferentiated solutions, but also deepens the understand-ing of the risk situation of an insurance company.This circumstance is not only of utmost importance forsupervision, but also – and this is probably even morecrucial – for the companies themselves. FOPI thereforetook up the principles of Solvency II and staked out thegoal of elaborating the corresponding application andimplementation of risk-based solvency supervision evenbefore entry into force of the new ISL. Such a large andambitious goal was only achievable with the support ofall affected actors in Switzerland (and some actorsabroad) who possessed the relevant know-how. In thespring of 2003, FOPI therefore launched a project thatwas supported by specialists from the insurance industry,management consultant companies, and universities.The project succeeded in elaborating the appropriate ap-plications and mathematical models by the summer of2004 to the extent that a first field test with ten selectedinsurance companies could be undertaken. The Swissvariant of risk-based supervision, named Swiss SolvencyTest (SST), has also attracted attention abroad.

Initially, the main result of the 2004 field test was that itcould even be conducted. Although this may soundtrite, it was of fundamental importance to FOPI. In addi-tion, it was shown that SST demonstrates a favourablecost/benefit ratio for insurance institutions as well, andthat it leads to very good and plausible figures. The re-sults of the field test helped further develop SST, so thata new field test can be conducted in the early summer of 2005, this time with 45 insurance companies.FOPI is therefore well-prepared for the scheduled entryinto force of the new ISL on 1 January 2006. The rele-vant provisions of the Supervision Ordinance can be sup-ported by the experiences of two field tests. At the sametime, a step-by-step enactment of SST is intended, dueto the extraordinary complexity of the risk categories tobe calculated, but also due to the related learningprocess among all involved actors.SST therefore creates a considerably better understand-ing of the risks entered into and the necessary capitalresources, both for supervision and for the companiesthemselves. But why doesn’t FOPI wait for the corre-sponding Solvency II rules of the EU? The answer issimple: An introduction of SST as soon as possible notonly will increase the effectiveness of supervision, as is demanded in any event by the legislative power with the new ISL. Due to the more in-depth knowledge oftheir own risk structure, it will also help affected insur-ance institutions achieve a competitive advantage overcompanies that do not have this knowledge.

Introduction

7

Comprehensive qualitative supervisionIn addition to central questions of reserves and solvency,the new law contributes an additional dimension of su-pervision that has already been applied conceptually inSST: the increased attention of supervision to qualitativereview of the various risks. But this requires additional,qualitatively oriented models.These models complementing SST are therefore deliber-ately embedded in an overall concept of comprehensiveassessment of the general risk management of compa-nies. The central question in this regard is how new ac-tuarial, but also operational risks can be managed in ad-vance. The goal is therefore to have a set of instrumentsthat meet the demands of the insurance industry in thefield of tension between protection of insured partiesand solvency supervision. The goal is also to attain a ho-listic overview of the market and to identify the risks forinsurers early on that are relevant to success. At thesame time, FOPI wants to ensure that the very limitedhuman resources of supervision are developed in a tar-geted manner and can be employed efficiently.Against this backdrop, FOPI has developed a generalmodel for qualitatively oriented supervision that can alsobe tested with the companies and then modified if nec-essary. The supporting idea behind this model is self-monitoring and self-assessment based on relevantguidelines provided by the supervisory authority. Inter-ventions by the authority will only occur if the self-as-sessment leads to obviously or strikingly divergent re-sults compared with general „benchmark values“ basedon experience. This form of qualitative supervision is par-ticularly suited to the processes of risk management,corporate governance, the provision of reserves, and theuse of information technologies, and can be expandedto other risk-relevant business processes as needed.

Foundation established for the futureThe expansion of consumer protection, the implementa-tion of risk-based solvency protection with the Swiss Sol-vency Test, and the complementary attention paid toqualitative supervision are the cornerstones of the newsystem of supervision. This new orientation in the qualityaimed for meanwhile entails that the supervisory author-ity must have sufficient quantitative and qualitative re-sources.The new system of supervision will strengthen the secu-rity of the insurance market and thereby also the inter-ests of the insured parties. The task of FOPI over the nextfew years will be to implement this new supervision phi-losophy and the newly created supervision instrumentsstep-by-step and to continuously adapt them to the cur-rent demands and circumstances. At the same time, thesupervision activities that are no longer necessary as aconsequence of the expansion of solvency monitoringwill be reduced, so that supervision can increasingly fo-cus on what is essential. During the implementation ofthe new supervision strategy, FOPI will therefore also en-sure that innovation and competition are not thwartedby over-regulation. In this way, supervision will make anessential contribution both to the protection of insuredparties and to the stability of the Swiss financial centre.

8

Total revision of the ISL / Partial revisionof the ICL: Implementation can begin

sation with the law in EU member States. Parliamentendorsed this idea only in part. It decided to maintainpreventive product control in the ”socially sensitive“areas of occupational pensions and the supplementaryinsurance to mandatory health insurance.

b) The area of occupational pensions took up a largepart of the parliamentary debates.

� The „transparency requirements“ for life insurance adopted as part of the second PensionLaw* revision, which entered into force on 1April 2004, were included in the draft of the newISL, but were viewed with great suspicion. Parlia-ment demanded in particular an enshrinementof the „legal quote“ in the Law and not only inthe Ordinance, as this had been the case since 1April 2004. „Legal quote“ is understood to bethe minimum share of returns on assets and anyrisk or cost profits, that must be credited to the insured parties in accordance with life insuranceagreements. Parliament fixed the legal quote, inaccordance with the existing ordinance provision,at 90%.� The procedure for reconciling the versions ofthe two chambers focused almost exclusively onthe business activities of life insurers with respectto occupational pensions. The National Councildemanded that all occupational pension schemesentered in the register for occupational pensionsbe subject to supervision in accordance with thePension Law, not insurance supervision. TheCouncil of States ultimately agreed to this de-mand. In addition, the National Council had proposedthat the provisions of the Pension Law trump theprovisions of the ISL if life insurers engage inbusiness activities relating to occupational pen-sions by concluding collective agreements, andthat Federal Office of Private Insurance (FOPI)should take into account any mandatory insurancerules when monitoring premium rates. The National Council subsequently dropped both demands due to disagreement with the Councilof States.

* Federal Law on Occupational Old Age, Survivors’ and Invalidity PensionFund = Bundesgesetz über die berufliche Alters-, Hinterlassenen- undInvalidenvorsorge (BVG)

After intensive debates in both chambers, theSwiss Parliament adopted the draft bills on 17 De-cember 2004. The new provisions are expected toenter into force on 1 January 2006. The main goalsof the revision were to secure the long-term sta-bility of the insurance companies and to improvethe protection of the insured parties.

1. Consideration by ParliamentThe new supervision rules were a topic of discussion inall parliamentary sessions of the year under review: Afterthe Council of States, which was the first chamber toconsider the proposal in December 2003, the NationalCouncil considered the draft bills in the spring session;the Council of States considered the draft bills again inthe summer session in June to reconcile the differencesbetween the versions of the two chambers, the NationalCouncil again in the autumn, and both chambers onelast time in the winter session. Just prior to convening aharmonisation conference, the two chambers finallyagreed on the proposals, so that the draft bills could beadopted by both chambers unanimously in the final voteon 17 December 2004.

Despite the long and intensive debates, the new InsuranceSupervision Law (ISL) was praised overall in Parliament asa good foundation for effective insurance supervision.The so-called „new supervision strategy“ was not calledinto question in any way. The new system of risk-basedsolvency supervision, the introduction of group and con-glomerate supervision, the increased observance of theprinciples of good corporate governance, the creation ofthe function of a responsible actuary, the strengtheningof consumer protection through the expansion of infor-mation obligations in accordance with supervision law,the obligation incumbent upon independent insurancebrokers to enter themselves in an official register, andthe tightening of penalties were broadly endorsed andremained uncontroversial. Over the course of the parlia-mentary debates, the proposal of the Federal Council of9 May 2003 nevertheless was subject to not insignificantchanges in some other equally important points:

a) One of the goals of the revision of the supervisionrules was the replacement of preventive productcontrol through a tightened solvency control.Through this liberalisation, the Federal Council aimsto increase competition and accordingly the diversityof insurance products at lower premiums. At thesame time, this shift is intended to achieve harmoni-

Report on activities 2004

9

3. Money Laundering Ordinance of FOPI**The Money Laundering Ordinance of FOPI will continueto remain outside the Supervision Ordinance. It is notbased on the Insurance Supervision Law but on theMoney Laundering Law***. The Money Laundering Ordinance is also in need of revision. One reason for thisrevision is the new ISL itself, the final clauses of whichamended the Money Laundering Law for the purpose oftransferring the responsibility for monitoring measuresfor combating money laundering by independent in-surance brokers from the Money Laundering ControlAuthority to FOPI. A further reason is the ongoing adjustment of the Money Laundering Law to the revisedrecommendations of the Financial Action Task Force ofthe OECD. A final reason is the revision of 17 December2003 of the insurance agreement with the Principality ofLiechtenstein, which further specified the powers andthe applicable law for the supervision of due diligence inconcluding contracts via foreign branches and free move-ment of services across borders. The work on revision ofthe Money Laundering Ordinance is being undertaken inparallel with the revision of the Supervision Ordinance.

c) The partial revision of the Insurance Contract Law(ICL) also took up much discussion time. As an ex-pert commission is currently undertaking a draft fora total revision of the ICL, the draft bill therefore onlyenvisaged amendments that arose necessarily fromthe revision of the ISL or that had to be viewed asurgent due to repeated parliamentary initiatives. Parliament, however, also considered it necessary toregulate certain questions of consumer protectionalready on the basis of the partial revision and not to wait for the results of the expert commission. Inparticular, this affected the strengthening of infor-mation obligations for insurance companies vis-à-visinsured parties in the area of business activities relating to occupational pensions.

2. Supervision Ordinance*The new Law requires new ordinance provisions. The efforts in this regard have been underway for quite sometime. In 2003, FOPI project groups outlined the contentof a new ordinance; in the first half of the year under re-view, it developed a concept for the legislative procedureand a specific draft ordinance on the basis of thispreparatory work. The preliminary draft was circulatedfor consultation to interested circles in the middle of August, including in particular the Swiss Insurance Association, the consumer protection organisation, andthe associations of insurance brokers. The numerous andin part very substantial comments resulted in the reviewof various points of the draft. The concept for a new Supervision Ordinance envisages the unification of allexisting provisions, which are currently distributedamong more than a dozen ordinances, in a single ordinance. The plan is to have the new Supervision Ordinance enter into force at the same time as the Law,i.e. on 1 January 2006, after the conclusion of the externaland administration-internal consultation processes.

* Aufsichtsverordnung (AVO)** Geldwäschereiverordnung des BPV (VGW)

*** Geldwäschereigesetz (GWG)

10Report on activities 2004

Swiss Solvency Test – first trial run conducted in 2004

2. Consequences for the insurersIn developing the SST, attention was paid that the addi-tional work required of the insurers when conductingthe solvency tests will be appropriate.A significant consequence of the SST will be that moreresponsibilities will be transferred to the managementand to the responsible actuary. The responsible actuaryor other offices in the insurance enterprise responsiblefor risk management must submit an SST report to themanagement, which may then be requested by the supervisory authority. The SST report serves to documentboth the risk situation and the calculation of the targetcapital. The SST report must be drafted in a way that themanagement and the supervisory authority can assessthe true risk situation of the insurance company, but alsothat an external actuary can reproduce the calculation ofthe target capital.With the help of the SST, supervision will increasingly orient itself according to the actual risk situation of theinsurance enterprises and also analyse the market-consistent, i.e. economic, evaluation of the assets andobligations, in addition to the statutory figures. The verification of the internal models used will be a challengefor supervision.

3. Swiss supervisory authority engages in pioneering work The SST gears itself to international developments, takinginto account, however, the specific circumstances of theSwiss insurance market. Risk-based solvency systemshave already existed for quite some time in Canada, Fin-land, and the United States. Australia, the Great Britain,the Netherlands, and Singapore have recently introducedsystems similar to SST or are close to introducing them.For the last few years, the EU has worked on Solvency II,and an EU-wide introduction is expected in about 5years.The SST was conceived as compatible with the futureEuropean solvency test in accordance with Solvency II, tothe extent this is already foreseeable. Since Switzerlandwill begin the introduction of the SST earlier than the EU,Switzerland is playing a pioneering role within Europe.

The risks to which insurance companies are exposedare manifold: tight stock markets, terrorist attacks,natural disasters, and demographic developments,to name only a few. A new approach for ascertainingthe ability of insurers to handle risks – their „security“– is the Swiss Solvency Test (SST) conducted by theFederal Office of Private Insurance (FOPI). In theyear under review, a first trial run was carried outwith the model developed for the SST.

1. Objectives of the SSTIn short, the SST determined a target capital that is necessary for an insurer to survive the risks assumedwith adequate security. The Swiss Solvency Test primarilypursues two objectives:

� One aim is to promote risk management in insurancecompanies. The outcome of the SST is therefore morethan merely the target capital. Just as important isthe path to this outcome, individual interim results,scenarios, and assessments of the responsible actuaryor the offices responsible for risk management in theinsurance enterprise.� In addition, the target capital has the function of awarning signal: If the available risk-bearing capital isless than the necessary target capital, this does notentail the insolvency of the enterprise. Rather, eitherthe necessary capital must be built up over a certainperiod of time, or the risks are to be reduced in such a way – e.g. through improved asset liability man-agement (ALM) – that the resulting target capitalcan be covered by the available risk bearing capital.The SST is to a large extent formulated on the basisof principles. This means that, where possible, nostrict formulas are given for the calculation of thetarget capital, but rather the supervisory authoritydefines guidelines that must be respected. Companiesare at liberty to choose the path adapted to their circumstances for the calculation. For the supervisoryauthority, this requires increased insight into thecompany-specific models and gives the insuranceenterprises the incentive to quantify and managetheir risks themselves.

11

5. Future developmentsIn the summer and autumn of 2005, a further trial runwill be conducted. Participation is open to all insuranceenterprises that would like to participate. This trial runwill again serve to determine individual parameters andmodels and to test the applicability of the SST to smallerinsurance enterprises. In contrast to 2004, the SST willnot only refer to business activities in Switzerland, but will also encompass the foreign branches of Swissinsurers. For this purpose, the internal risk models of theinsurers will be used.The use of internal risk models is also envisaged for rein-surers. The reason is that the portfolios of the reinsurersare too disparate to be described by a standard modelprovided by the supervisory authority. The discussion inthis sector deals first of all with the question of how therisks can be measured for legal entities in Switzerland,but also for global corporate groups, and second of allhow the effect of diversification within a group (profitsin country X together with losses in country Y) can betaken into account and passed on to subsidiaries. Thismust happen in a way that takes into consideration thatcapital within a corporate group cannot be movedaround completely freely.With the entry into force of the revised Insurance Super-vision Law (ISL), expected on 1 January 2006, the SSTwill also be introduced. Transitional periods are envisagedfor adapting capital reserve requirements to the resultsof the SST for each individual insurance enterprise aswell as in particular for the calculation of the necessaryvalues, such as the market-consistent evaluation of assets and liabilities or the amount of the necessary risk-bearing capital.

4. Status of work The development of the SST began in the spring of 2003and was conducted in close collaboration with represen-tatives of the Swiss Actuary Association, the insuranceindustry, and the universities, as well as with auditingcompanies and consulting offices. By the end of 2003,the SST methodology had been fixed, and by the summerof 2004, a number of working groups were developinga model. The result was a model for the probabilities ofthe available economic capital within a year (stochasticmodel), which was combined with a series of extremescenarios (e.g. worldwide flu epidemic).In the second half of 2004, a number of life and non-lifeinsurers applied this model in a trial run to their own individual situation. This trial run served to determineparameters, to estimate the time investment necessaryfor the individual insurer, and to recognise inconsistenciesin the model. Although this was only a first trial run, the results were such that all participants rated them asplausible.Some gaps were discovered in the model, however.Since the winter of 2004, mixed working groups haveagain been taking measures to improve the model.These measures include the evaluation of guarantees,the assessment of the reserve risks, and the manner inwhich extreme scenarios are dealt with.

12Report on activities 2004

Supervision of insurance brokers

� In the area of professional qualifications, rules onthe acquisition of the relevant new professionalqualifications were established in collaboration withthe insurance industry. The rules govern the organi-sation of examinations and dispensations in additionto training curricula. Upon successful completion ofwritten and oral exams, the insurance intermediariesreceive the title of „Insurance Broker VBV“ (Berufs-bildungsverband der Versicherungswirtschaft).� With respect to the question of financial guarantees,the focus is primarily on professional liability insurancefor economic loss. At the present time, only a few insurance companies offer coverage in this regard.The Swiss Insurance Association (SIA) has begun toaddress this problem and will create special sampleinsurance contract terms and conditions for a product for insurance brokers this year.

Work beginning in 2005In the current year, solutions must be found in the areasof register management, management of accounts receivable, and archiving. Since, according to the newISL, the register must be open to the public, the optionof querying the register will be made available via Internet. Preparations for this service are underway.In addition preliminary work is being carried out onother points in intermediary supervision. This is mainly to do with questions on distribution, collaborationagreements, treatment of client complaints, and com-mission systems.With the planned introduction of the new ISL on 1 January2006, insurance brokers will be given six months time to submit an application for entry into the register to thesupervisory authority.

Insurance intermediaries now subject to federal supervisionOn 9 December 2002, the European Parliament and theCouncil of the European Union decided to supervise insurance mediation in the EU (cf. Directive 2002/92/EC).With the introduction of the new Insurance SupervisionLaw (ISL), expected to enter into force on 1 January2006, Switzerland will also have established an equi-valent supervision mechanism. The background is theharmonisation of the regulatory environment through-out Europe: Swiss insurance intermediaries should notbe comparatively disadvantaged by comparison with insurance intermediaries abroad with respect to trans-national activities. At the same time, a greater control ofinsurance brokers is being demanded in Switzerland forthe benefit of consumer protection.

The legislative basisThe Federal Office of Private Insurance (FOPI) is responsiblefor the supervision of insurance brokers provided for inthe new ISL. Articles 40 et seq. of the new ISL inter aliarequire FOPI to manage a public register. The Law regu-lates the preconditions for inscription into the registerand determines the information duties of all insurancebrokers vis-à-vis insured parties. These information dutiesmust now be fulfilled by every insurance intermediary, independently of whether the intermediary is bound toan insurance company or not. Amongst other things, the person must now be indicated who can be held liable for negligence, errors, or incorrect information.Around 3000 independent insurance intermediaries operate in Switzerland and will be subject to compulsoryregistration. An additional 10’000 agents of insurancecompanies will be subject to voluntary registration. Thevoluntary registration of the agents of insurance compa-nies will be basically welcomed by the insurance industry,because a registration will be considered as necessary inorder to be able to keep up with the insurance brokers.

Preparatory work in 2004After reorganisation of the entire Office as of 1 July2004, the Insurance Intermediaries Supervision Servicewas able to begin its work. Its primary responsibility isthe establishment of an insurance intermediary register.First, the preconditions for registration into the registerwere determined: According to the legal provisions, insurance brokers can only be registered if they candemonstrate sufficient professional qualifications andadequate financial guarantees.

13

Risk management is also being given a central rolein the new supervision over non-life insurers (here-after non-life supervision): Art. 22 of the revised Insurance Supervision Law (ISL) requires that companies be able to assess, limit, and monitor allrisks. The Federal Office of Private Insurance (FOPI)is undertaking to realign non-life supervision according to these risk analyses of the insurancecompanies. First projects were initiated in the yearunder review.

In the area of non-life insurance supervision, the „Non-life Insurance“ division was created as part of the re-structuring of FOPI as of 1 July 2004. About 100 insur-ance companies that are supervised as non-life insurershave been newly allocated to this division.In addition to the traditional supervision of non-life in-surers, the new division also had to deal with the re-alignment of non-life supervision. The revised ISL shiftsrisk management to the centre of supervision activities.Art. 22 requires that insurance companies organisethemselves in a way that they are able to assess, limit,and monitor all substantial risks. In addition to tradition-al insurance risk, many other risks play a role, such asoperational risks, financial risk, or strategic risk. With aview toward risk-oriented supervision, FOPI has integrat-ed this risk philosophy into the consideration of the re-ports submitted by the supervised institutions in the yearunder review.

1. Results of the SST are includedThe results and conclusions from the first field test of theSwiss Solvency Test (SST) will be included in the newnon-life supervision; in the year under review, 10 largenon-life and life insurers took part in the SST. For thecoming year, 45 additional non-life insurers have indicat-ed their desire to participate in the second field test. Theevaluations of this test series will provide important indi-cators for optimising the SST as well as the new non-lifesupervision.

2. New supervision strategyWith these changes, non-life supervision will in the fu-ture not only ensure solvency protection and compliancewith the tightened legal provisions, but will also monitorthe entire organisation of the insurance company, alsoon the basis of the existing risk landscape. For the defini-tion and implementation of the new legal point of de-parture, a number of larger projects were launched inthe autumn of 2004 and are being launched in the first

half of 2005. It was essential for FOPI to take an invento-ry of the risks of the dynamic market environment, toreconcile them with already existing knowledge of riskmanagement of the insurance companies, and to refinethem. The projects also aimed at a national and interna-tional market comparison (benchmarking) of possibleevaluations of insurance risks (risk assessment, risk limi-tation, and risk monitoring), in order to achieve a „bestpractice“.The new non-life supervision will deal with the analysisof core processes. As a priority, non-life supervision willfocus on topics, such as with the settlement of claimsand reserve processes.The objective of the supervision is to verify the most im-portant points of risk management and, where neces-sary, to define steps on the basis of deficiencies identi-fied.

Reorientation of non-life insurance supervision

14

Group and conglomerate supervision

Report on activities 2004

2004, provides an explicit legal basis for the supervisionof groups and conglomerates, resulting also in the con-solidated supervision of insurance groups in the future.In the second half of 2003 and the first half of 2004, theordinances on group and conglomerate supervisionwere drawn up, as part of the comprehensive ordi-nances on the new ISL. The ordinances are compatibleboth with regulations already issued as well as with thenew EU directives (cf. regulation in the EU).

� Credit Suisse Group (bank-dominated conglomer-ate with Winterthur as insurance component)� Zurich Financial Services � Swiss Life� Bâloise � Swiss Re

Since conglomerates constitute an economic unit thatencompasses both insurance companies and banks, su-pervision cannot be the sole responsibility of FOPI. Withrespect to consolidated supervision, FOPI thereforeworks together with the responsible authority for banksupervision.

4. Consolidated supervision compared with individ-ual supervisionConsolidated supervision complements solo supervision.In contrast to individual supervision, where an insurancecompany of Switzerland is subject to supervision, con-solidated supervision encompasses all companies of aSwiss group, worldwide.

5. Practical supervision activitiesIn addition to developing the regulation on consolidatedsupervision of Swiss Re, the practical supervision activi-ties in 2004 included analysis of the reports received andthe figures the conglomerates had to achieve; discussionof these reports with the responsible offices in thegroups; and visits to the conglomerates for the purposeof deepening understanding of supervision topics.Contacts with other regulators in Switzerland andabroad took up a further large part of the supervisoryactivities: In 2004, 8 meetings took place with the SwissFederal Banking Commission and 6 meetings with for-eign supervisory authorities dedicated to the supervisedconglomerates. The high demand for coordination ofgroup and conglomerate supervision also required numerous telephone conferences with foreign supervisoryauthorities, in addition to the personal meetings. Moreover, FOPI was invited to two coordination meet-ings of foreign insurance groups that own subsidiaries inSwitzerland.

1. BackgroundThe economic development in the direction of globalisa-tion has also affected the insurance industry. An increas-ing number of Swiss insurance companies have boughtor founded subsidiaries in Switzerland and abroad andhave developed into international insurance groups. Al-though this trend has slowed somewhat in the last threeto four years due to the poor stock market developmentand the focus has been on the core markets, the slumpin globalisation should probably be regarded as a tem-porary development.In addition, there has been a noticeable trend towardsbankassurance in recent years. Large insurers increasing-ly not only want to offer a broad insurance range, butthey also have become active in the banking sectorthrough acquisitions or formations. Banks have alsoshown the desire to benefit from the synergies of bank-assurance, by buying or founding insurance companies.These developments have led to the creation of the fivefinance conglomerates in Switzerland, four of which areinsurance-dominated conglomerates and one of whichis a bank-dominated conglomerate. About fourteen so-called insurance groups exist in Switzerland. This numberalso includes the conglomerates, since a sub-group canalways be identified within a conglomerate that consti-tutes an insurance group.

2. The risks of insurance groupsSupervision of these comparatively young entities musttake into account the developments on the market andthe related new risks: risks that can arise with such an in-ternationally active economic entity are, for instance,group-internal „risks of contagion“, supervision arbi-trage between financial activities that are regulated dif-ferently, unrecognised risk concentrations, or „falsifica-tions“ of the picture of a single company by double useof the same funds, to name only a few.It is therefore indispensable that the supervisory authori-ty is able to gain an overall picture of the group and thatit exchanges information with regulators in other coun-tries, in order to prevent distortions of competition andto achieve greater stability of the financial market. This isimportant not least in view of enhanced protection of in-sured parties.

3. Consolidated supervision in Switzerland On the basis of individual decrees, the finance conglom-erates have been made subject to consolidated supervi-sion, through interpretation of the current Insurance Su-pervision Law (ISL). The new ISL, adopted in December

15

Regelung in der EU und Konsequen-zen für die schweizerischen Konzerne

Konsolidierte Aufsicht: Richtlinie 1998verabschiedetAuch die EU erkannte den Bedarf für eine konsolidierte Aufsicht schon frühund verabschiedete im Jahre 1998 eineRichtlinie zur Beaufsichtigung der Ver-sicherungsunternehmen, die Teil einerVersicherungsgruppe sind. Die Richtliniemusste bis im Juni 2000 in nationalesRecht umgesetzt werden. Gemäss diesen Vorgaben und dem da-zugehörenden Ermächtigungsprotokollwird für jede Versicherungsgruppe innerhalb der EU ein Land bestimmt(meistens dasjenige, in welchem derKonzern die grösste Geschäftstätigkeitausübt), das die Koordination der Auf-sicht übernimmt. Die Aufgaben des Koordinators bestehen darin, Informa-tionen der EU-Aufsichtsbehörden, in denen der Konzern tätig ist, zu sammelnund die jährliche Koordinationssitzungzu leiten. Er übernimmt jedoch keineVerantwortung für die zusätzliche Auf-sicht.Da die Schweiz nicht Mitglied der EU ist,wird sie einerseits theoretisch von diesemProzess ausgeschlossen, und anderer-seits wird auch für die schweizerischenVersicherungsgruppen ein Koordinatorinnerhalb der EU gesucht. Praktischkann die schweizerische Aufsichts-behörde jedoch an diesen Koordinations-sitzungen teilnehmen, hat jedoch keinMitbestimmungsrecht, und es ist ihr

auch nicht erlaubt, die Rolle des Koordi-nators zu übernehmen.Da diese Vorgehensweise weder für dieAufsichtsbehörden noch für die Gesell-schaften eine befriedigende Lösungdarstellt, ist das BPV seit Mitte 2004daran, eine Vereinbarung mit der EU zu treffen, um für diese Aufgabe gleich-wertige Rechte und Pflichten wie die EU-Mitgliedstaaten zu erhalten.

Verabschiedung der Konglomerats-richtlinieIm Jahr 2002 folgte die Verabschiedungder Richtlinie für die Konglomeratsaufsicht, deren Umsetzung in den Mitgliedstaaten bis am 1.1.2005 zu erfolgen hatte. Auch gemäss dieserRichtlinie muss die Aufsichtsbehörde eines Landes als Koordinator bestimmtwerden. Seine Aufgabe ist jedoch umfassender. Zusätzlich zur Koordinati-onsfunktion übernimmt er auch die generelle Aufsicht über den Konzern. Er erhält somit die Funktion des führen-den Aufsehers („Lead Regulator“). Die Konglomeratsrichtlinie ist nicht nurin Bezug auf die Funktion des Koordina-tors breiter definiert, sondern sie istauch offener gegenüber Nicht-EU-Ländern. So besteht die Möglichkeit,dass die Konglomeratsaufsicht einesDrittlandes als äquivalent qualifiziertwird, und somit ein Drittland die Funkti-on des „Lead Regulator“ übernehmenkann.

ÄquivalenzanforderungenGemäss einer allgemeinen Empfehlungdes Finanzkonglomerats-Komitees derEU vom Juli 2004 erfüllt die Schweiz dieÄquivalenzanforderungen. Diese – fürdie schweizerischen Konzerne sehrwichtige Aussage – kann verhindern,dass die Konglomerate einer doppeltenAufsicht durch die Schweiz und die EUunterstellt werden. Jedes Mitgliedlandder EU, in dem ein schweizerisches Fi-nanzkonglomerat Aktivitäten ausübt,muss nun prüfen, ob es dieser Empfeh-lung folgen kann. Erst nach Abschlussdieses Prozesses, der für jedes Konglomerat einzeln durch-geführt wird, können die schweizeri-schen Konzerne davon ausgehen, dasssie nicht einer doppelten Aufsicht unter-stehen werden.

Regelung in der EU und Konsequen-zen für die schweizerischen Konzerne

Konsolidierte Aufsicht: Richtlinie 1998verabschiedetAuch die EU erkannte den Bedarf für eine konsolidierte Aufsicht schon frühund verabschiedete im Jahre 1998 eineRichtlinie zur Beaufsichtigung der Ver-sicherungsunternehmen, die Teil einerVersicherungsgruppe sind. Die Richtliniemusste bis im Juni 2000 in nationalesRecht umgesetzt werden. Gemäss diesen Vorgaben und dem da-zugehörenden Ermächtigungsprotokollwird für jede Versicherungsgruppe innerhalb der EU ein Land bestimmt(meistens dasjenige, in welchem derKonzern die grösste Geschäftstätigkeitausübt), das die Koordination der Auf-sicht übernimmt. Die Aufgaben des Koordinators bestehen darin, Informa-tionen der EU-Aufsichtsbehörden, in denen der Konzern tätig ist, zu sammelnund die jährliche Koordinationssitzungzu leiten. Er übernimmt jedoch keineVerantwortung für die zusätzliche Auf-sicht.Da die Schweiz nicht Mitglied der EU ist,wird sie einerseits theoretisch von diesemProzess ausgeschlossen, und anderer-seits wird auch für die schweizerischenVersicherungsgruppen ein Koordinatorinnerhalb der EU gesucht. Praktischkann die schweizerische Aufsichts-behörde jedoch an diesen Koordinations-sitzungen teilnehmen, hat jedoch keinMitbestimmungsrecht, und es ist ihr

auch nicht erlaubt, die Rolle des Koordi-nators zu übernehmen.Da diese Vorgehensweise weder für dieAufsichtsbehörden noch für die Gesell-schaften eine befriedigende Lösungdarstellt, ist das BPV seit Mitte 2004daran, eine Vereinbarung mit der EU zu treffen, um für diese Aufgabe gleich-wertige Rechte und Pflichten wie die EU-Mitgliedstaaten zu erhalten.

Verabschiedung der Konglomerats-richtlinieIm Jahr 2002 folgte die Verabschiedungder Richtlinie für die Konglomeratsaufsicht, deren Umsetzung in den Mitgliedstaaten bis am 1.1.2005 zu erfolgen hatte. Auch gemäss dieserRichtlinie muss die Aufsichtsbehörde eines Landes als Koordinator bestimmtwerden. Seine Aufgabe ist jedoch umfassender. Zusätzlich zur Koordinati-onsfunktion übernimmt er auch die generelle Aufsicht über den Konzern. Er erhält somit die Funktion des führen-den Aufsehers („Lead Regulator“). Die Konglomeratsrichtlinie ist nicht nurin Bezug auf die Funktion des Koordina-tors breiter definiert, sondern sie istauch offener gegenüber Nicht-EU-Ländern. So besteht die Möglichkeit,dass die Konglomeratsaufsicht einesDrittlandes als äquivalent qualifiziertwird, und somit ein Drittland die Funkti-on des „Lead Regulator“ übernehmenkann.

ÄquivalenzanforderungenGemäss einer allgemeinen Empfehlungdes Finanzkonglomerats-Komitees derEU vom Juli 2004 erfüllt die Schweiz dieÄquivalenzanforderungen. Diese – fürdie schweizerischen Konzerne sehrwichtige Aussage – kann verhindern,dass die Konglomerate einer doppeltenAufsicht durch die Schweiz und die EUunterstellt werden. Jedes Mitgliedlandder EU, in dem ein schweizerisches Fi-nanzkonglomerat Aktivitäten ausübt,muss nun prüfen, ob es dieser Empfeh-lung folgen kann. Erst nach Abschlussdieses Prozesses, der für jedes Konglomerat einzeln durch-geführt wird, können die schweizeri-schen Konzerne davon ausgehen, dasssie nicht einer doppelten Aufsicht unter-stehen werden.

Regulation in the EU and conse-quences for Swiss groups

Consolidated supervision: Directiveadopted in 1998 The EU also recognised the need forconsolidated supervision early on andadopted a directive in 1998 on the su-pervision of insurance companies thatare part of an insurance group. The di-rective had to be implemented into na-tional law by June 2000.In accordance with these requirementsand the accompanying enabling proto-col, a country is determined for the co-ordination of the supervision of each in-surance group within the EU (usually thecountry in which the group engages inthe most extensive business activities).The responsibilities of the coordinatorconsist in compiling the information ofthe EU supervisory authorities to whichthe group is subject and to chair the an-nual coordination meeting. The coordi-nator does not, however, assume re-sponsibility for the additional supervi-sion.Since Switzerland is not a member ofthe EU, it is theoretically excluded fromthis process, on the one hand, and onthe other hand, a coordinator within theEU is also sought for the Swiss insurancegroups. In practice, however, the Swisssupervisory authority can participate inthese coordination meetings, but with-out a formal vote, and the Swiss author-ity is also not allowed to take on the roleof coordinator.

Since this approach is not a satisfactorysolution either for the supervisory au-thorities or for the companies, FOPI hasbeen engaged since the middle of 2004in reaching an agreement with the EU inorder to receive equivalent rights andduties as the EU member States for thistask.

Adoption of the conglomerate directiveThe adoption of the directive on con-glomerate supervision followed in2002, the implementation of which hadto be completed by 1 January 2005 inthe member States. Also according tothis directive, the supervisory authorityof a country must be determined as acoordinator. Its responsibilities are morecomprehensive, however. In addition tothe coordination function, it also as-sumes general supervision of the group.It therefore is given the function of thelead supervisor („lead regulator“).The conglomerate directive is not onlydefined more broadly with respect tothe function of the coordinator, but it isalso more open vis-à-vis non-EU coun-tries. Accordingly, the possibility existsthat the conglomerate supervisory au-thority of a third country can be quali-fied as equivalent, so that the thirdcountry can assume the function of leadregulator.

Equivalence requirementsAccording to a general recommenda-tion of the finance conglomerate com-mittee of the EU issued in July 2004,Switzerland fulfils the equivalence re-quirements. This statement – of greatimportance for the Swiss groups – canprevent that the conglomerates are sub-ject to double supervision by Switzer-land and the EU: Each member countryof the EU in which a Swiss finance con-glomerate undertakes activities mustnow review whether it can comply withthis recommendation. Only upon con-clusion of this process, which is under-taken individually for each conglomer-ate, will Swiss groups be able to assumethat they will not be subject to doublesupervision.

1616Report on activities 2004

In the year under review the „Life Insurance“ de-partment was primarily involved in implementingthe prescriptions which came into force on 1 April2004 on transparency and the minimum quota onprofits achieved in occupational pensions in favourof the insured persons. In a first step a review wasundertaken with respect to the separation of thesafety fund for all life and pension insurance activi-ties into one fund for occupational pensions andanother one for the remaining business activitiesof each life and pension insurer. The next step fol-lowing this separation consisted in initiating andaccompanying the implementation of the newtransparency requirements.

1. Implementation of the legislative requirementsby FOPI

1.1 Separation of the safety fund When implementing the legislative requirements theprotection of all insured persons has to be respected(Art. 1 of the Insurance Supervision Law, ISL). This meansthat the separation of the safety fund and the allocationof investments to the new safety fund for occupationalpensions must be undertaken in a way that neither theinsured persons for occupational pensions nor the onesfor other life insurance policies are unilaterally advan-taged or disadvantaged. For this purpose FOPI compileda detailed description of the principles and the processfor separating the safety fund available to the life insur-ers.In the year under review the details of the allocations ofinvestments in the safety fund for occupational pensionsas proposed by the life and pension insurers were thoroughly examined. After some considerable modifi-cations, the proposals were all approved. Subsequent tothe approval, the auditing companies of the life andpension insurers started to examine the implementation– a process that will continue into the year 2005.

1.2 Further changes in accordance with the 1st Pension Act* revision� The second major task concerns the introductionof a separate profit and loss account for occupation-al pensions. Different levels of information must befollowed: The account must be structured in a waythat its content serves to inform the insured persons,all institutions administering pension funds and FOPIas the supervisory authority. In particular, compliancewith the legally prescribed minimum quota to the insured persons must be proven. � If an employer cancels its association agreementwith an institution administering pension funds, themanner of pension payments must be regulated inparticular. In this regard the new legal prescriptionsin accordance with Art. 53e of the Pension Act arenow subject to legal and technical supervision byFOPI.

2. Financial reporting within the scope of the trans-parency requirements

Due to the new transparency requirements, which willsustainably improve information provided by funds(foundations and institutions administering pensionfunds) and life and pension insurers to insured persons,FOPI must now undertake more in-depth reviews compared to reviews in the past. These reviews concernsafety fund cover, the calculation of policy settlementvalues, the development of the surplus funds and thepayment of surpluses as well as other transparency datain the occupational pension business. A revised ques-tionnaire on pension funds (specially drawn up for theyear 2004) and the newly drafted presentation of theseparate profit and loss account (starting in 2005) serveas the basis for the in-depth reviews. Their completion isbased on the statutory statement of account require-ments in accordance with the rules of the Swiss Code ofObligations and the overlapping rules of supervision law.

* Federal Acton Occupational Old Age, Survivors’ and Invalidity PensionFund = Bundesgesetz über die berufliche Alters-, Hinterlassenen- undInvalidenvorsorge (BVG)

Implementation of the transparency requi for the insurance of occupational pensions

17

rements

International Financial Reporting Standards(IFRS) and statutory accounts statementThe goal of the International Financial ReportingStandards (IFRS) is to harmonise financial reportingfor the purpose of better information and compara-bility, also among life and pension insurers. Withinthe insurance sector as a whole, life and pension in-surers are hit most. In the statement of account ac-cording to the IFRS guidelines, assets and liabilitiesand the various options and guarantees, such as capi-tal option and interest guarantee, are valuated ac-cording to fair value, i.e. according to market valuesor values close to the market.In Switzerland a statutory statement of account, i.e. astatement of account according to the Code ofObligations must still be compiled. Contrary to theIFRS guidelines, this type of statement of account isbased on the lower-value principle for the assets andthe valuation according to the insurance tables at thetime of policy conclusion for the liabilities. This typeof valuation is self-consistent and is very suitable forthe system of direct life and pension insurance aspractised in Switzerland, but does not indicate anymarket values. It is, however, mandatory to provideinformation on market values in the appendix to thestatement of account.In particular, FOPI was able to demonstrate on thebasis of enquiries concerning financial reporting thatthe use of the statutory statement of account cannotlead to profits for the insurer that exceed the legalthreshold – the minimum quota and the related re-quirements concerning transparency are accordinglyfulfilled extensively when applying the statutorystatement of account.

3. Transitional provisionsA number of legislative amendments, such as in particu-lar the new requirements on transparency and the mini-mum quota, entered into force during the fiscal year, i.e.on 1 April 2004. Equally, investments for covering thesafety funds for both occupational pensions and otherlife and pension business activities could only be dividedand reviewed by FOPI in the course of 2004. It is there-fore not possible to compile precise statements of ac-count for occupational pensions for 2004. Estimatesand, accordingly, simplified statements of account shalltherefore be accepted for 2004, before a precise proce-dure will be available as of 2005.

18Report on activities 2004

Compulsory transfer of portfolios / Supervision problems with bankrupt healt

1. Measures in accordance with supervision lawInsured parties have an interest in concluding theirmandatory basic health insurance and their supplementaryhealth insurance with a single insurer. In the insolvencycases mentioned above, both supervisory authoritieshave therefore endeavoured to find a single health insurerwilling to provide organisational support to the insolventhealth insurance scheme and to take over the entirepool of insured persons. The objective is for the pool ofinsured persons of the insolvent health insurancescheme to find a health insurer that provides the neces-sary financial and organisational guarantee that theclaims of the insured persons can continue to be fulfilledin the future.Among the applications received, the application receivesthe support of the supervisory authorities which offersthe best guarantees with respect to protection of the insured persons, i.e. seamless transition of the pool ofinsured persons, sufficient solvency, continuation of theexisting products or offering equivalent products, financialmeans for any price to be paid for taking over the insuredpool, continuing employment of the former staff membersof the insolvent health insurance scheme to the extentpossible (know-how of business operations, settlementof benefits, data processing, etc.). Additional criteriamay play a role in individual cases, such as the geo-graphic area of operations.Such a transfer of an insured pool is relatively unproble-matic for the area of mandatory health insurance sinceacceptance is compulsory for the insurer and since standardised products exist. In the area of supplementaryinsurance, a diversity of products and freedom of contract exist, which does not make the transfer parti-cularly easy.

The insolvency of three health insurance schemesoffering supplementary health insurance policiesalso occupied the Federal Office of Private Insurance(FOPI) in the year under review: The responsible division was mandated to accompany the transferof insured pools to other companies and to under-take securing measures for the protection of insured parties and other creditors. Some problemsarose under supervision law in this regard.

Three health insurance schemes that offer private supple-mentary health insurance policies in addition to socialhealth insurance have become insolvent in recent years:For the KBV health insurance scheme and the Accordahealth insurance scheme, adjudication in bankruptcy isimminent; bankruptcy proceedings have already beeninitiated for the Zurzach health insurance scheme. In allthree cases, the reasons for the insolvencies lie in thesector of mandatory health insurance. These cases also affected FOPI: For health insuranceschemes operating social health insurance and privatesupplementary health insurance within the same legalentity, shared supervision applies. Supervision of socialhealth insurance (Health Insurance Law) and institutionalsupervision are the responsibility of the Swiss Federal Office of Public Health (SFOPH); supervision of supple-mentary health insurance activities is the responsibility ofFOPI. In the event of insolvency, recognition as a healthinsurance scheme is withdrawn; this has a reflexive effect on the supplementary health insurance activities.Approval for the undertaking of supplementary healthinsurance activities is tied to the condition that approvalfor undertaking social health insurance has been granted.Accordingly, as soon as the Federal Department of Home Affairs withdraws a health insurance operation’srecognition as a health insurance scheme and its authori-sation to engage in business activities due to insolvency,FOPI must act immediately and apply for withdrawal ofapproval in the supplementary health insurance sectorfrom the Federal Department of Finance and initiate themeasures for the protection of persons provided for inthe Non-life Insurance Law*.

* Schadenversicherungsgesetz (SchVG)

19

th insurance schemes

2.2 Blocking of tied assetsUntil the time that the compulsory portfolio transfer isapproved, the tied assets are blocked. This measure aimsto secure the special assets that have been earmarked tocover obligations vis-à-vis insured parties with supple-mentary health insurance in accordance with Art. 8 ofthe Non-life Insurance Law, also with a view to preparinga compulsory portfolio transfer. Withdrawals may onlybe made with the approval of FOPI.

The tied assets are special assets that are accorded pri-vileged use for the payment of the claims of insured persons with additional health insurance subject to theInsurance Contract Law in the case of bankruptcy. Any surplus is allocated to the bankruptcy estate.

2.3 Deferment of bankruptcyThis option is based on Art. 21 of the Non-life InsuranceLaw, according to which the initiation of adjudication ofbankruptcy for an insurance institution requires theagreement of the Federal Department of Finance. Theadjudication of bankruptcy is deferred until the transferof the portfolio has been completed and a large share ofthe benefit claims has been settled successfully.

2.4 Measures to protect the interests of other creditorsFOPI is also required to ensure that it does not grant approval to any transactions that disadvantage the othercreditors in the bankruptcy. In the case of compulsorytransfer of portfolios, FOPI ordered that the value of thetransferred portfolios be determined by means of an expert assessment. Evaluation of the portfolio is intendedto ensure that FOPI does not agree to a transaction inwhich services rendered and consideration received aregrossly disproportionate and in which funds are extractedfrom the bankruptcy estate through the creation of excessive profits.

2. Protection of insured parties and equal treat-ment of creditors in bankruptcy

In the chapter entitled „Securing Measures“ of the Non-life Insurance Law, a series of measures are provided thatFOPI and the Federal Department of Finance may orderfor the protection of insured parties with supplementaryhealth insurance in the case of insolvent health insurers.In addition to the protection of the insured parties, FOPImust also observe the principle of equal treatment ofcreditors in bankruptcy. This did in fact occur in the threeinsolvency cases:

2.1 Compulsory transfer of insured pools to supple-mentary health insurancesArt. 15, para. 2 of the Non-life Insurance Law stipulatesthat the supervisory authority take measures necessaryfor the protection of insured parties ex officio. The verba-tim provision is: „It (The supervisory authority) may, inparticular, transfer the insured pool and the correspon-ding tied assets to another insurance facility or order thecompulsory liquidation of the values of the tied assets.“

Insurance contracts expire four weeks after adjudicationin bankruptcy of the insurer has been initiated (Art. 37 ofthe Insurance Contract Law). So that insured persons donot lose their coverage, the entire portfolio of supple-mentary health insurance policies of the insolvent healthinsurance scheme with the corresponding values of tiedassets is transferred to the health insurer willing to assume the portfolio. The insured parties receive theguarantee that they may continue their insurance con-tracts with the new health insurer at the same or at leastequivalent conditions, without review of risk or additionof new health or age conditions. This provision is doublyimportant in the area of supplementary health insurancepolicies, since persons above the age of 50 and young,sick insured persons would, as a rule, not be able to obtain a contract with a new insurer.

In the case of a compulsory portfolio transfer, insuredpersons are not, however, given an exceptional right tocancel the contract, as is the case for a voluntary port-folio transfer in accordance with Art. 39 of the InsuranceSupervision Law. This point is the object of an appeal before the Federal Appeals Commission for Private Insurance. The case is still pending.

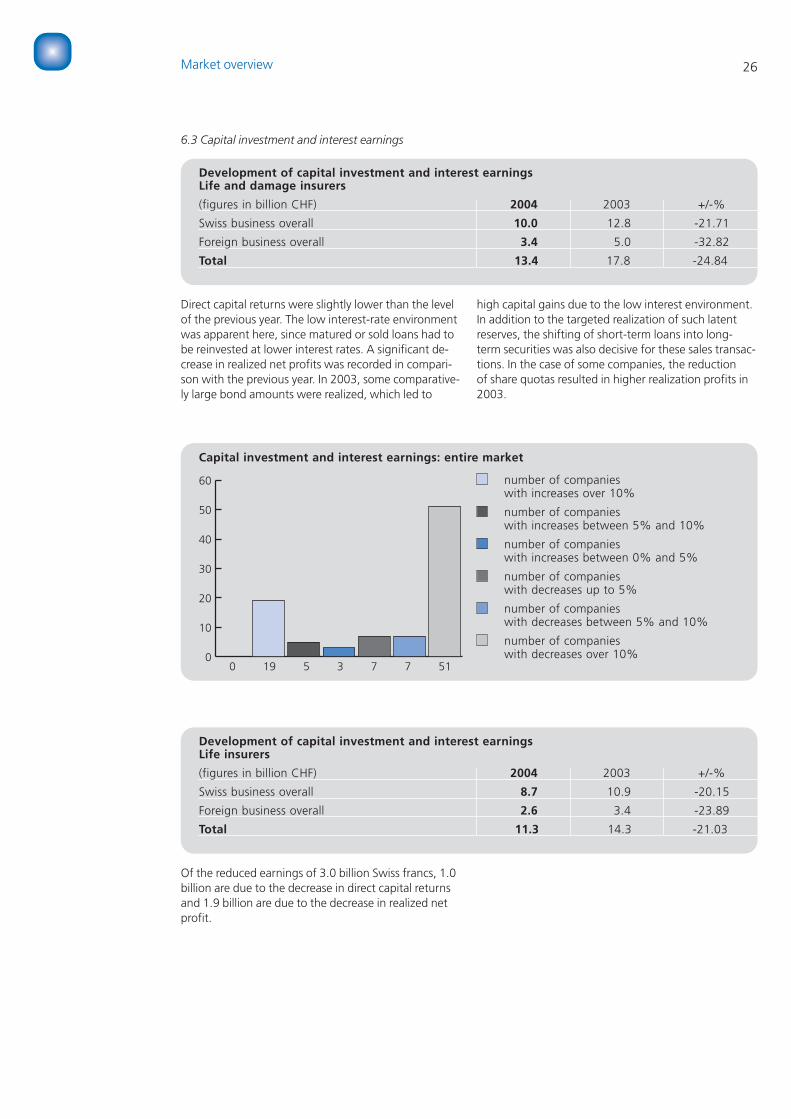

20

1. IntroductionFor reporting year 2004 (with previous year figuresfrom 2003), FOPI obtained comprehensive data on thebusiness developments of life and damage insurers dur-ing an early phase prior to compilation of the definitivereport. Along with financial data and solvency figures,additional information on asset values was requested(including conversion of amounts reported accordingto regulations into a market-oriented presentation).This data was obtained with the goal of compiling amarket overview. In individual cases, adjustments weremade to enable an adequate comparison with the datafrom the previous year.

2. Accounting principlesThe supervised insurance companies balance theirbooks according to the principles of the Swiss Law ofObligations. An exception is made for fixed-interest se-curities, which may be entered on the assets side asamortized cost. The obtained provisional data of the in-surance companies is therefore based on careful ac-counting. In addition, however, a conversion was re-quired for asset values into a market-oriented presenta-tion, and the resulting differential values were com-pared with the allowability of valuation differences forsolvability. Individual statutory account statements serve as the ba-sis for the supervisory instruments, since the demandsof insured parties primarily exist vis-à-vis the legal unit.The assessment of the surplus allocations is also basedon the statutory account statement of the individual in-surance company.In addition to this detailed review of the financial andearnings situation of an individual legal unit, FOPI inparticular also reviews the overall solvency of an insur-ance group. In this connection, statements are request-ed that comply with international accounting principles(IFRS, US GAAP). In individual cases, the insurance com-pany must justify significant differences to FOPI be-tween statutory financial statements in accordancewith the Law on Obligations and statements in accord-ance with international accounting principles.

3. Summary of the results of the market overviewThe overall picture shows that the insurance sector inSwitzerland has clearly recovered from the difficultyears of 2001 and 2002. An overview of the most im-portant results:

� The equity capital basis was significantly streng-thened, especially in the case of life insurers, whichled to a corresponding improvement of the averagesolvency indicator.� The premium volume shrank in the case of lifeinsurers, primarily due to the decrease in singlepremiums.� In the case of damage insurers, costs were redu-ced effectively, and in some sectors, premiums wereadjusted. For these reasons, the premium volumeincreased by 6%, and the combined ratio is nowsignificantly below 100% on average.� The earnings from capital investments could notbe maintained at the level of the previous year. Thedecrease resulted primarily from the lower directearnings and the lower profits from realizations.The low interest-rate environment affected directearnings, since matured or sold loans had to bereinvested at lower interest rates. Realized profitswere affected by the fact that the low interest-rateenvironment in 2003 was in part actively utilized to realize latent reserves into bonds. In addition,restructuring of bond portfolios in 2003 and thereduction of the share quota led to high realizationprofits.

Market overview

Swiss private insurers – a market overview

21

Schaden-versicherer

Lebens-versicherer1996 11.82% 9.18%

2000 14.96% 8.29%2001 14.98% 7.09%2002 15.19% 7.46%2003 14.11% 7.41%

Messung der Konzentration 2

Lebensversicherer Schadenversicherer

Tabelle 4

Life insurers Damage insurers

(figures in billion CHF) 2004 2003 +/-%* 2004 2003 +/-%*

Earned gross premiums 37.7 41.2 -8.38 45.8 43.4 +5.83

Expenditures for insurance cases (gross) 41.5 41.6 -0.24 31.0 30.2 +2.75

„Claims Ratio“** N/A N/A N/A 67.73% 69.76% -2.03

Capital investment and interest earnings 11.3 14.3 -21.03 2.1 3.5 -40.28

Expenditures for insurance operations for own account 3.3 3.6 -7.68 10.0 10.1 -1.05

„Cost ratio“** 10.30% 10.19% +0.11 25.57% 28.88% -3.31

„Combined ratio“** N/A N/A N/A 93.30% 98.64% -5.34

Reported equity capital*** 6.8 5.7 +18.02 17.2 16.3 +5.68

Solvency ratio** 205% 177% +28.00 312% 328% -16.00

Cover margin of the safety fund (life insurers) / fixed reserve (damage insurers) 6.1 7.0 -11.99 7.4 7.4 -0.43

* also in the following tables, percentage deviations are calculated using the non-rounded figures** actual deviation, not in percent

*** before allocation of profits

22Market overview

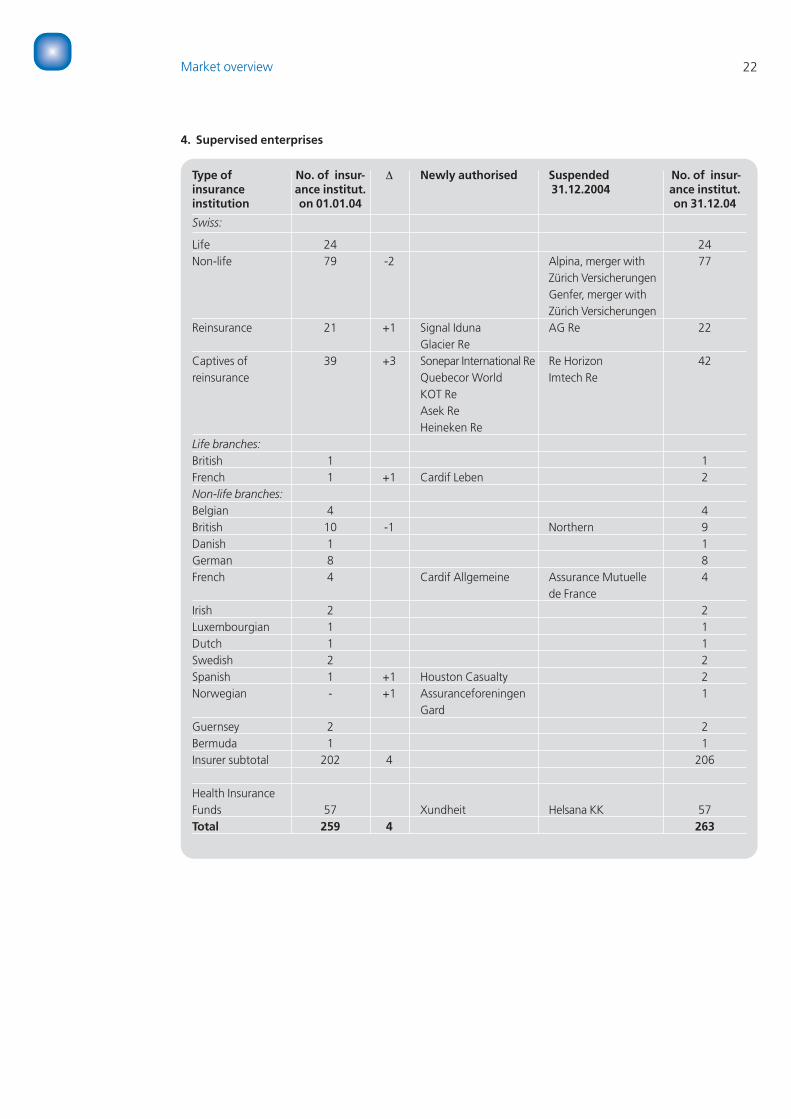

4. Supervised enterprises

Type of No. of insur- ∆ Newly authorised Suspended No. of insur-insurance ance institut. 31.12.2004 ance institut.institution on 01.01.04 on 31.12.04

Swiss:

Life 24 24Non-life 79 -2 Alpina, merger with 77

Zürich VersicherungenGenfer, merger withZürich Versicherungen

Reinsurance 21 +1 Signal Iduna AG Re 22Glacier Re

Captives of 39 +3 Sonepar International Re Re Horizon 42reinsurance Quebecor World Imtech Re

KOT ReAsek ReHeineken Re

Life branches:British 1 1French 1 +1 Cardif Leben 2Non-life branches:Belgian 4 4British 10 -1 Northern 9Danish 1 1German 8 8French 4 Cardif Allgemeine Assurance Mutuelle 4

de FranceIrish 2 2Luxembourgian 1 1Dutch 1 1Swedish 2 2Spanish 1 +1 Houston Casualty 2Norwegian - +1 Assuranceforeningen 1

GardGuernsey 2 2Bermuda 1 1Insurer subtotal 202 4 206

Health Insurance Funds 57 Xundheit Helsana KK 57Total 259 4 263

23

5. Most important supervision instruments for monitoring business activity

The insurance companies must submit a comprehen-sive annual report on the year under review as of 31December, as well as separate reports on fixed reserves,derivative financial instruments, and financial data onthe group results. In addition, FOPI conducts periodicsurveys of the year under review. In the event of specialbusiness incidents, the insurance company must informFOPI immediately (e.g. if the acquisition of borrowed orequity capital is planned).Private insurance companies domiciled in Switzerlandmust fulfil certain solvency criteria, so that the claims ofinsured parties are guaranteed at all times. FOPI cur-rently has at its disposal two legally enshrined instru-ments in particular: fixed reserves and the solvencymargin.

5.1 Fixed reservesCapital investments in fixed reserves (in the case of lifeinsurers, the safety fund) cover the necessary technicalreserves (obligations vis-à-vis insured parties) and arekept in a separate deposit. In the case of bankruptcy ofan insurance company, these reserves are liable for theclaims of insured parties above all other demands. FOPIspecifies investment and assessment requirements forthe capital investments in fixed reserves. This helpsachieve an appropriate diversification and preventsrisks of over-concentration. The investments must fulfilthe principles of appraisability and convertibility. Asafety margin of 1% (2% in the case of non-life insur-ers) is added to the total amount of necessary technicalreserves.Deficient cover of the fixed reserves is already reachedwhen the target amount (technical reserves + safetymargin) is no longer completely covered by the fixed re-serves. In this case, the insurance company is requiredto remedy the deficient cover immediately.

5.2 Solvency marginEquity capital resources are a determinative value in as-sessing the solvency of an insurance company. In the in-surance sector, equity capital plays a different role thanin industrial companies, for instance. In an industrialcompany, equity capital can be considered operationalcapital in a certain sense, while in an insurance compa-ny, it is more like safety capital, which is drawn upon inexceptional damage years to support the annual result.

The higher the capital resources, the more risks an in-surance company can assume. In an exceptional cata-strophic case, the survival of the company largely de-pends on its own resources. While the relation betweenequity and borrowed capital is of considerable interestin the industrial sector, the relation between own re-sources and risks on the asset and liability side of thebalance sheet is of foremost importance in the insur-ance sector.The solvency margin of an insurance company covers apart of the enterprise risks and is intended to secure thesurvival of the enterprise in an exceptional damageyear. This general measure is determined by a pre-scribed model calculation and is based on the standardsapplicable in the EU. The entire amount of the solvencymargin must be backed up by equity capital or bor-rowed capital with the character of equity capital. Ifthis provision is no longer met, the insurance companymust submit a restructuring plan to FOPI. FOPI deter-mines what requirements the restructuring plan mustfulfil and by what deadline the measures provided fortherein must be undertaken. Along with fixed reserves,the solvency margin provides an additional protectionof the insured parties from insolvency of the company.All of the following statistical data and evaluations arebased on the solvency definitions in accordance withSolvency I. However, this does not yet adequately takeinto account the risk profile of the individual insurancecompanies. A comprehensive evaluation will be cov-ered by risk-based solvency supervision (in this context,see the introductory article to this Annual Report onpage 4 and the article on the Swiss Solvency Test onpage 10).

5.3 Early warning systems In addition to the annual, comprehensive report, provi-sional account statement data are requested in ad-vance. Along with the submission of provisional state-ment data, FOPI required supervised insurance compa-nies to demonstrate the changes of certain balancesheet items for 2004 on the basis of three provided sce-narios. The anticipated distribution quotas to share-holders also had to be reported. The equity capital basisof the companies was already significantly strength-ened in 2003 after 2001 and 2002, years that involvedheavy losses. FOPI continues to monitor the distributionpractice, in order to continue to guarantee an appropri-ate strengthening of the equity capital quota in thefuture.

24

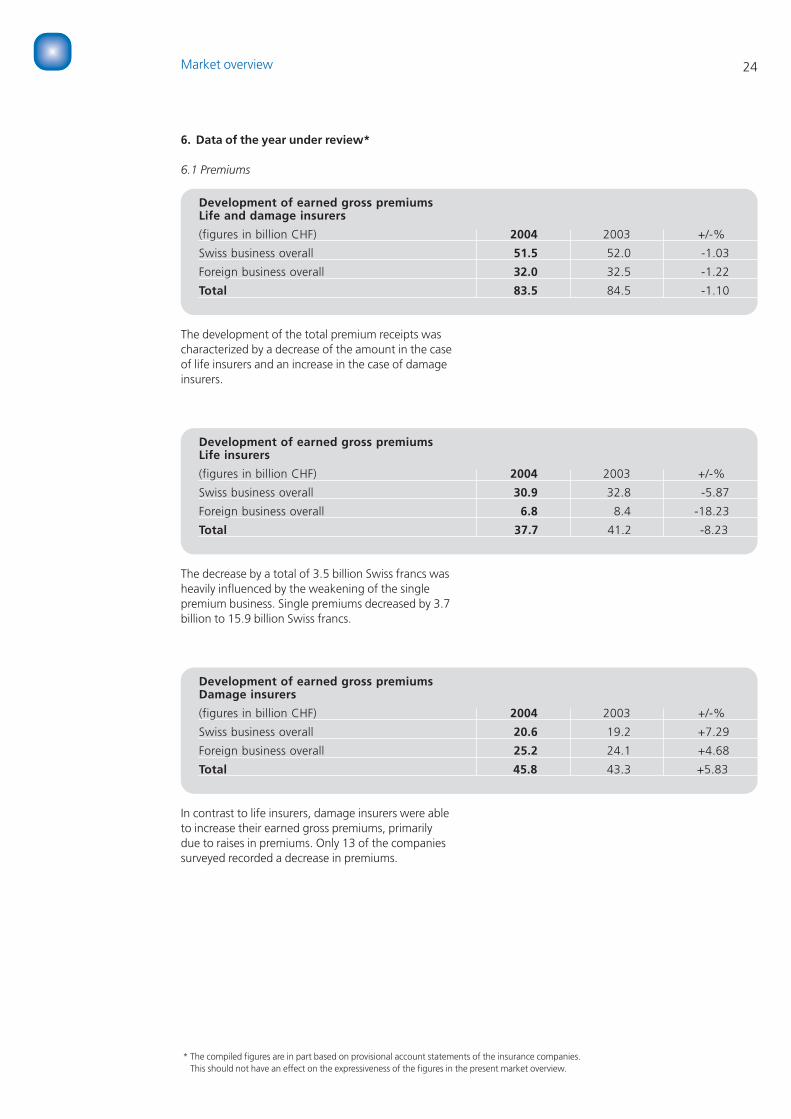

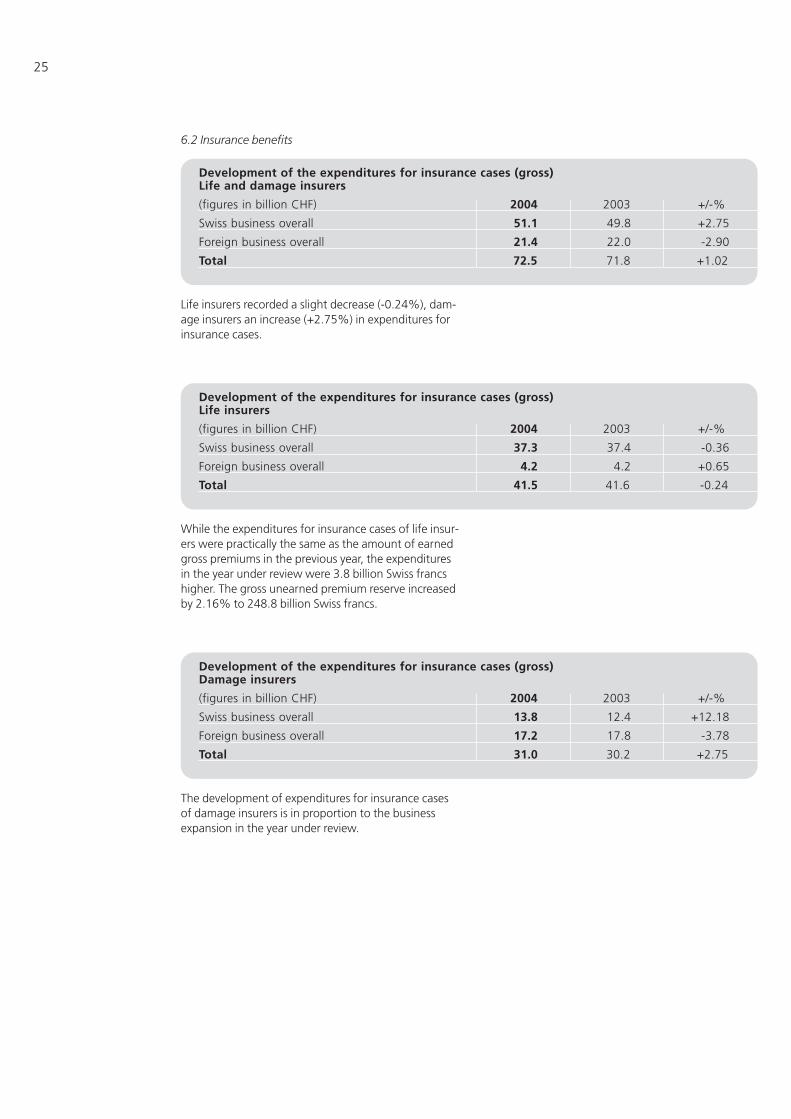

6. Data of the year under review*

6.1 Premiums

Market overview

The development of the total premium receipts wascharacterized by a decrease of the amount in the caseof life insurers and an increase in the case of damageinsurers.

The decrease by a total of 3.5 billion Swiss francs washeavily influenced by the weakening of the singlepremium business. Single premiums decreased by 3.7billion to 15.9 billion Swiss francs.

In contrast to life insurers, damage insurers were ableto increase their earned gross premiums, primarily due to raises in premiums. Only 13 of the companiessurveyed recorded a decrease in premiums.