NatCatSERVICE, Jan Eichner

55

NatCatSERVICE Introduction and Methodology Jan Eichner, Geo Risks Research, Head of NatCatSERVICE October 2016

-

Upload

oecd-governance -

Category

Government & Nonprofit

-

view

105 -

download

0

Transcript of NatCatSERVICE, Jan Eichner

NatCatSERVICE

Introduction and Methodology

Jan Eichner,

Geo Risks Research, Head of NatCatSERVICE

October 2016

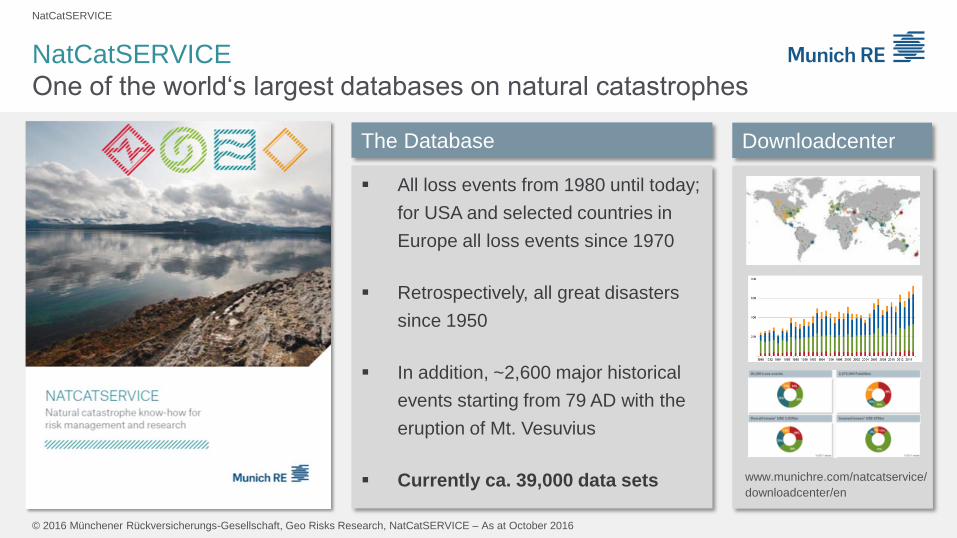

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

NatCatSERVICE

One of the world‘s largest databases on natural catastrophes

The Database

All loss events from 1980 until today;

for USA and selected countries in

Europe all loss events since 1970

Retrospectively, all great disasters

since 1950

In addition, ~2,600 major historical

events starting from 79 AD with the

eruption of Mt. Vesuvius

Currently ca. 39,000 data sets

Downloadcenter

www.munichre.com/natcatservice/

downloadcenter/en

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

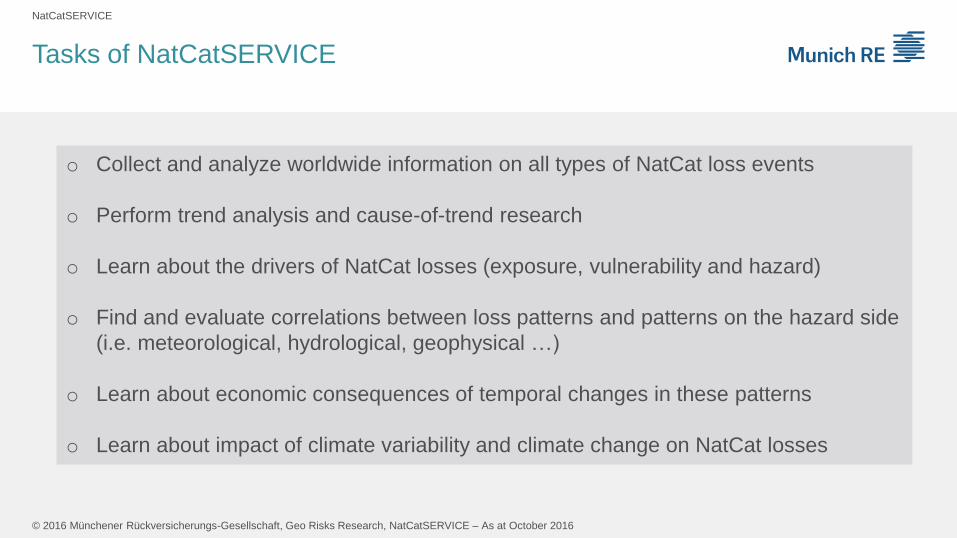

Tasks of NatCatSERVICE

o Collect and analyze worldwide information on all types of NatCat loss events

o Perform trend analysis and cause-of-trend research

o Learn about the drivers of NatCat losses (exposure, vulnerability and hazard)

o Find and evaluate correlations between loss patterns and patterns on the hazard side

(i.e. meteorological, hydrological, geophysical …)

o Learn about economic consequences of temporal changes in these patterns

o Learn about impact of climate variability and climate change on NatCat losses

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

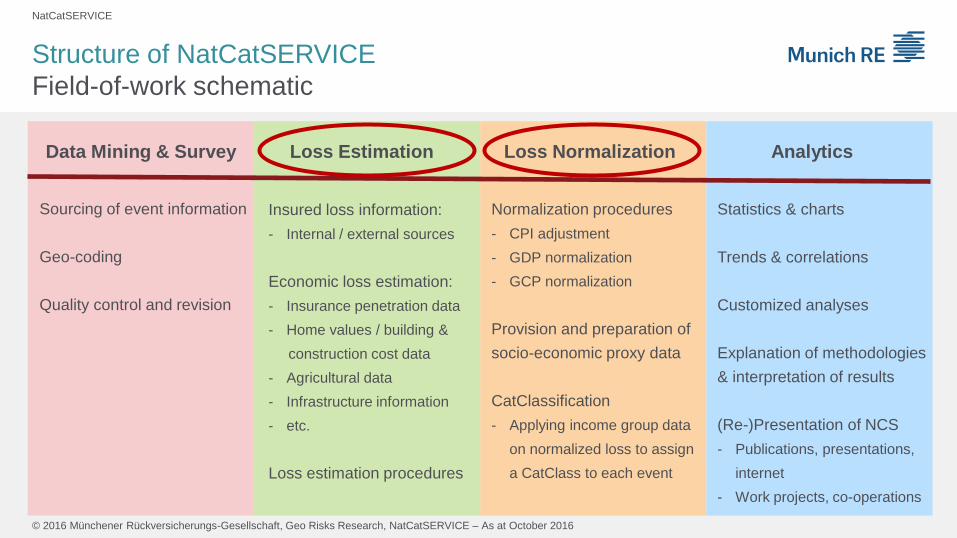

Structure of NatCatSERVICE

Field-of-work schematic

Data Mining & Survey Loss Estimation Loss Normalization Analytics

Sourcing of event information

Geo-coding

Quality control and revision

Insured loss information:

- Internal / external sources

Economic loss estimation:

- Insurance penetration data

- Home values / building &

construction cost data

- Agricultural data

- Infrastructure information

- etc.

Loss estimation procedures

Statistics & charts

Trends & correlations

Customized analyses

Explanation of methodologies

& interpretation of results

(Re-)Presentation of NCS

- Publications, presentations,

internet

- Work projects, co-operations

Normalization procedures

- CPI adjustment

- GDP normalization

- GCP normalization

Provision and preparation of

socio-economic proxy data

CatClassification

- Applying income group data

on normalized loss to assign

a CatClass to each event

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Estimation

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

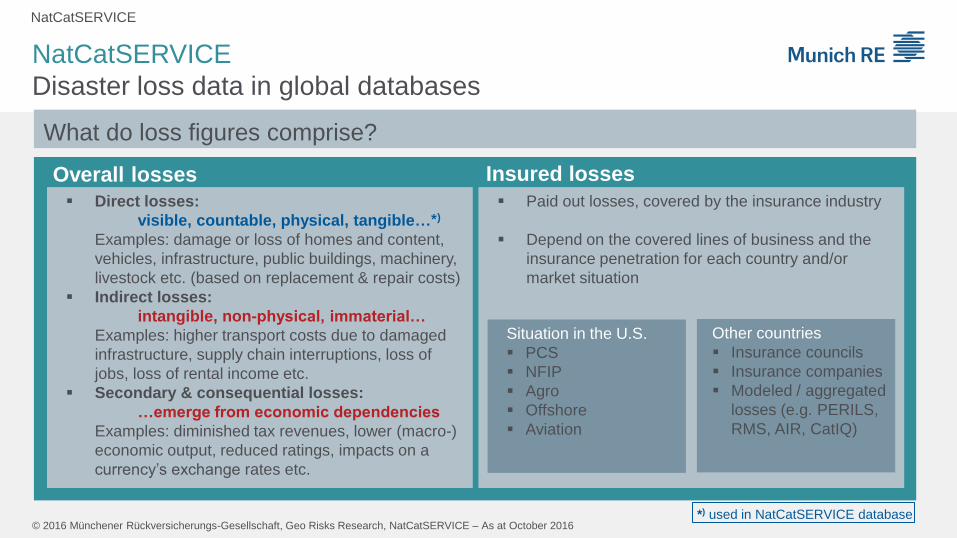

Overall losses

Direct losses:

visible, countable, physical, tangible…*)

Examples: damage or loss of homes and content,

vehicles, infrastructure, public buildings, machinery,

livestock etc. (based on replacement & repair costs)

Indirect losses:

intangible, non-physical, immaterial…

Examples: higher transport costs due to damaged

infrastructure, supply chain interruptions, loss of

jobs, loss of rental income etc.

Secondary & consequential losses:

…emerge from economic dependencies

Examples: diminished tax revenues, lower (macro-)

economic output, reduced ratings, impacts on a

currency’s exchange rates etc.

Paid out losses, covered by the insurance industry

Depend on the covered lines of business and the

insurance penetration for each country and/or

market situation

Situation in the U.S.

PCS

NFIP

Agro

Offshore

Aviation

Other countries

Insurance councils

Insurance companies

Modeled / aggregated

losses (e.g. PERILS,

RMS, AIR, CatIQ)

What do loss figures comprise?

NatCatSERVICE

NatCatSERVICE

Disaster loss data in global databases

Insured losses

*) used in NatCatSERVICE database

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

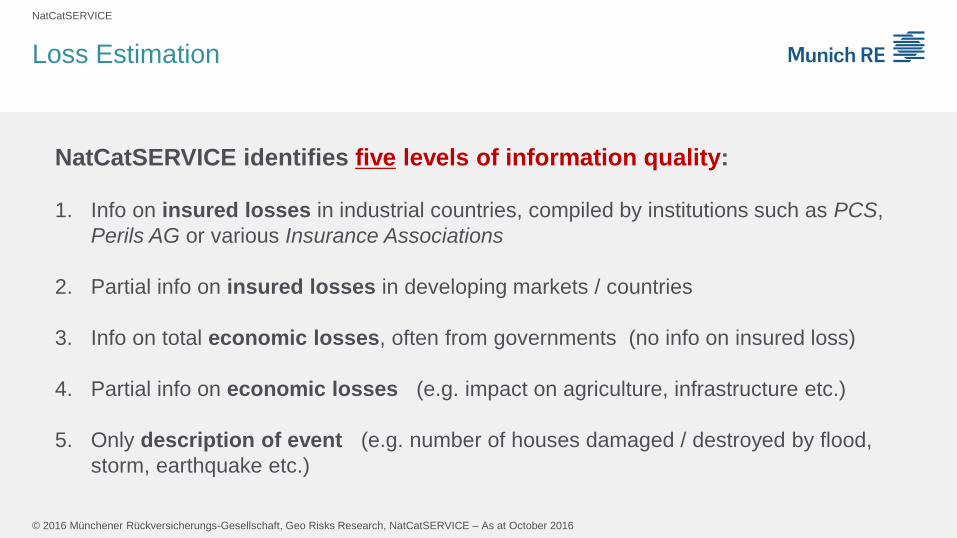

Loss Estimation

NatCatSERVICE identifies five levels of information quality:

1. Info on insured losses in industrial countries, compiled by institutions such as PCS,

Perils AG or various Insurance Associations

2. Partial info on insured losses in developing markets / countries

3. Info on total economic losses, often from governments (no info on insured loss)

4. Partial info on economic losses (e.g. impact on agriculture, infrastructure etc.)

5. Only description of event (e.g. number of houses damaged / destroyed by flood,

storm, earthquake etc.)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Estimation

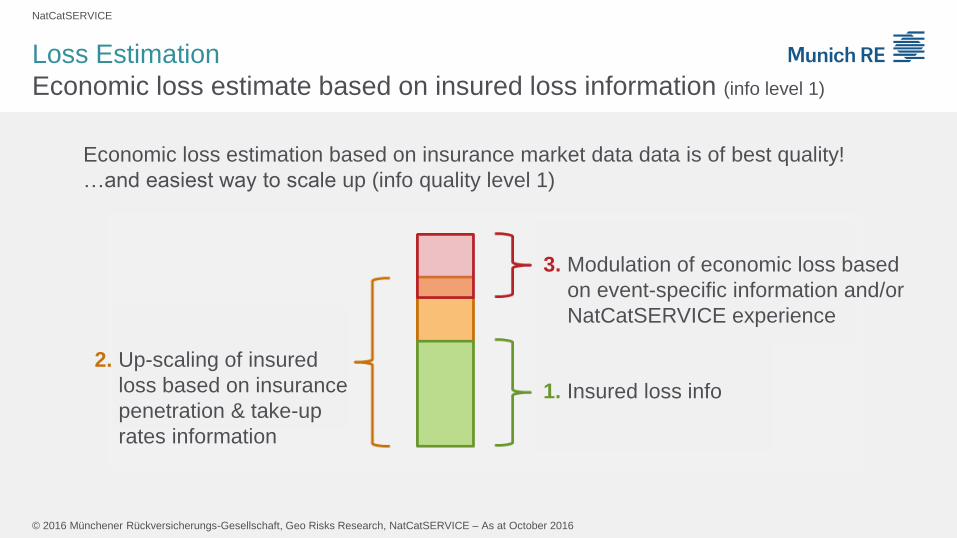

Economic loss estimate based on insured loss information (info level 1)

2. Up-scaling of insured

loss based on insurance

penetration & take-up

rates information

3. Modulation of economic loss based

on event-specific information and/or

NatCatSERVICE experience

1. Insured loss info

Economic loss estimation based on insurance market data data is of best quality!

…and easiest way to scale up (info quality level 1)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Estimation

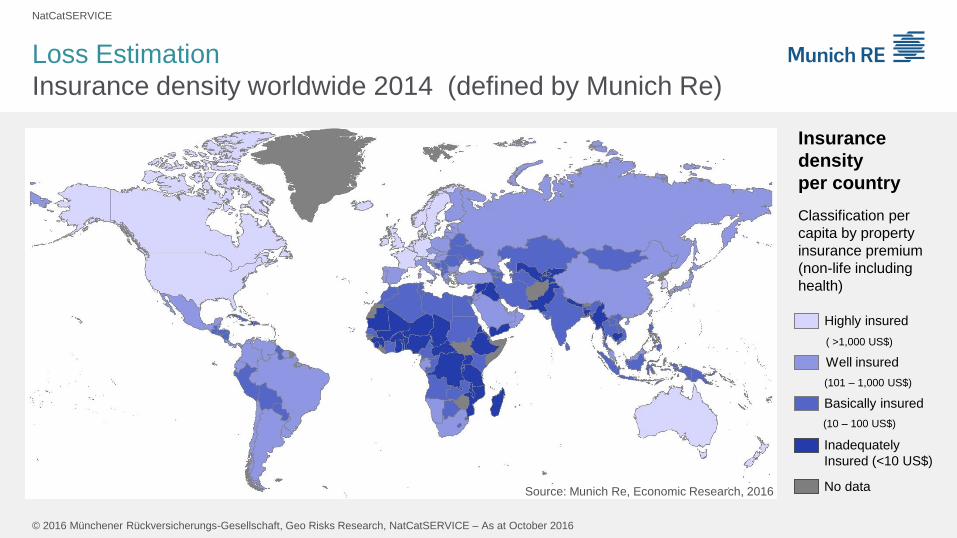

Insurance density worldwide 2014 (defined by Munich Re)

Insurance

density

per country

Classification per

capita by property

insurance premium

(non-life including

health)

Highly insured

( >1,000 US$)

Well insured

(101 – 1,000 US$)

Basically insured

(10 – 100 US$)

Inadequately

Insured (<10 US$)

No data Source: Munich Re, Economic Research, 2016

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Estimation

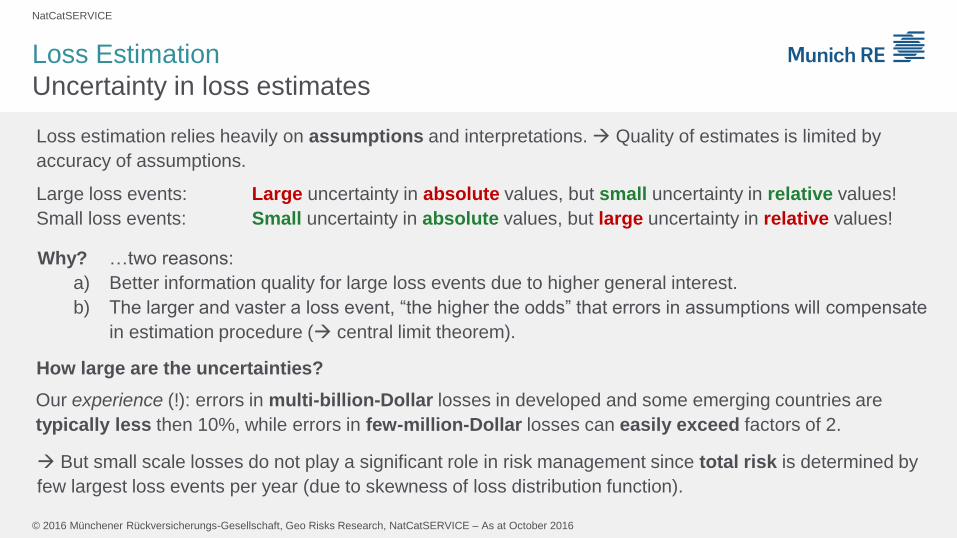

Uncertainty in loss estimates

Loss estimation relies heavily on assumptions and interpretations. Quality of estimates is limited by

accuracy of assumptions.

Large loss events: Large uncertainty in absolute values, but small uncertainty in relative values!

Small loss events: Small uncertainty in absolute values, but large uncertainty in relative values!

Why? …two reasons:

a) Better information quality for large loss events due to higher general interest.

b) The larger and vaster a loss event, “the higher the odds” that errors in assumptions will compensate

in estimation procedure ( central limit theorem).

How large are the uncertainties?

But small scale losses do not play a significant role in risk management since total risk is determined by

few largest loss events per year (due to skewness of loss distribution function).

Our experience (!): errors in multi-billion-Dollar losses in developed and some emerging countries are

typically less then 10%, while errors in few-million-Dollar losses can easily exceed factors of 2.

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Data Normalization

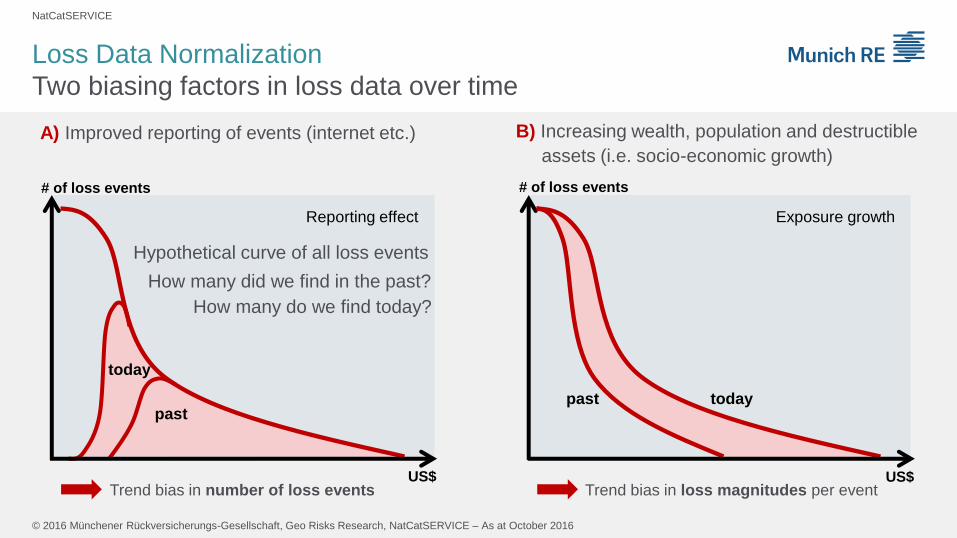

Two biasing factors in loss data over time

Reporting effect

US$

# of loss events

Trend bias in number of loss events

today

past

Exposure growth

US$

# of loss events

past today

Trend bias in loss magnitudes per event

A) Improved reporting of events (internet etc.) B) Increasing wealth, population and destructible

assets (i.e. socio-economic growth)

Hypothetical curve of all loss events

How many did we find in the past?

How many do we find today?

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

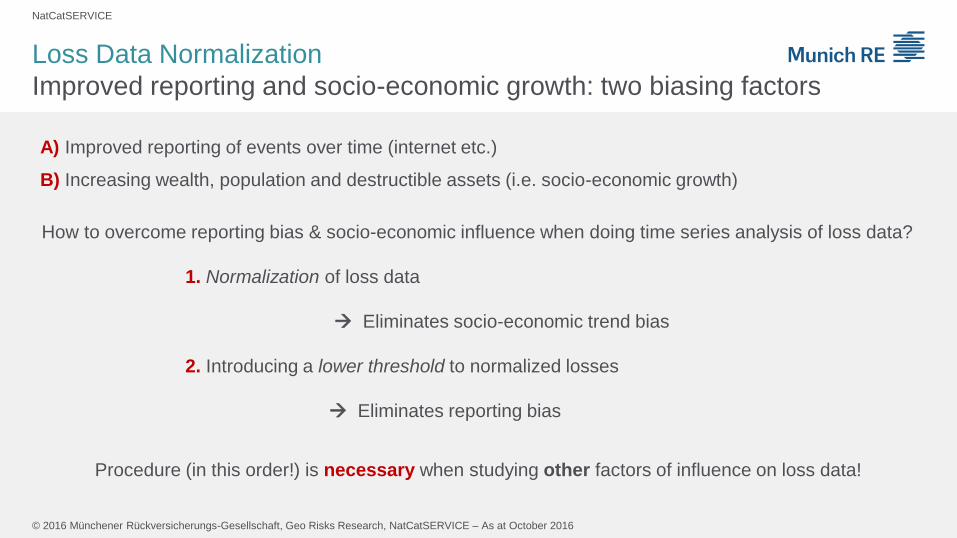

Loss Data Normalization

Improved reporting and socio-economic growth: two biasing factors

How to overcome reporting bias & socio-economic influence when doing time series analysis of loss data?

1. Normalization of loss data

Eliminates socio-economic trend bias

2. Introducing a lower threshold to normalized losses

Eliminates reporting bias

Procedure (in this order!) is necessary when studying other factors of influence on loss data!

A) Improved reporting of events over time (internet etc.)

B) Increasing wealth, population and destructible assets (i.e. socio-economic growth)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Data Normalization

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Data Normalization

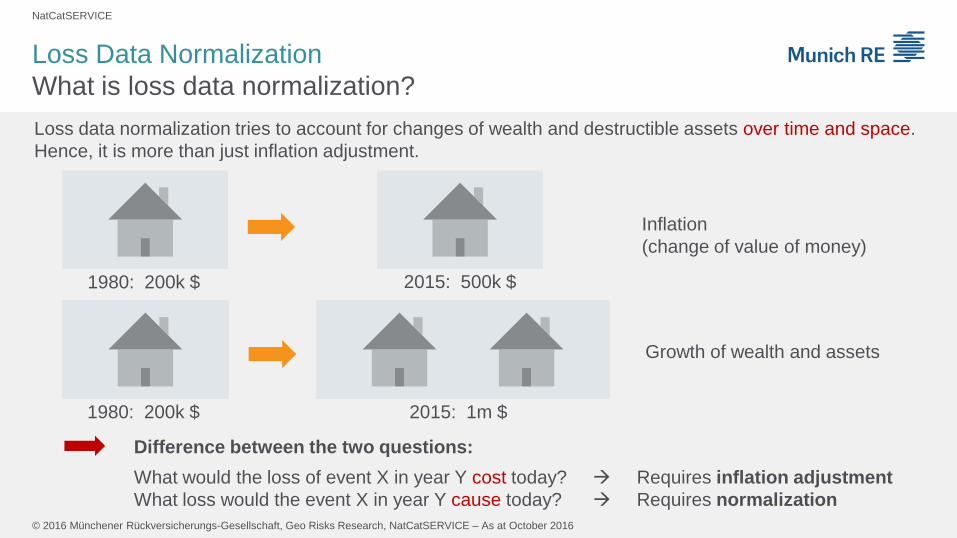

What is loss data normalization?

Loss data normalization tries to account for changes of wealth and destructible assets over time and space.

Hence, it is more than just inflation adjustment.

1980: 200k $ 2015: 500k $

Inflation

(change of value of money)

2015: 1m $ 1980: 200k $

Growth of wealth and assets

Difference between the two questions:

What would the loss of event X in year Y cost today? Requires inflation adjustment

What loss would the event X in year Y cause today? Requires normalization

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Data Normalization

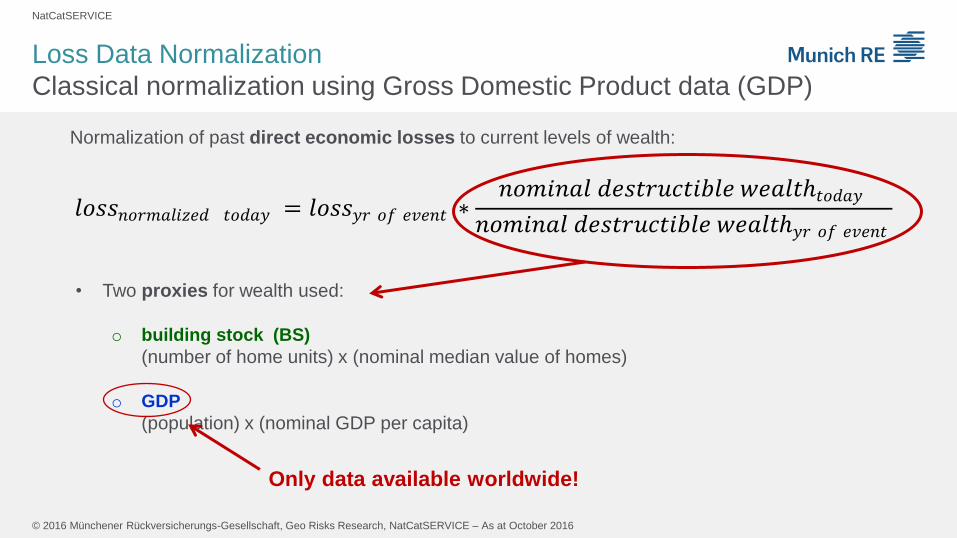

Classical normalization using Gross Domestic Product data (GDP)

• Two proxies for wealth used:

o building stock (BS)

(number of home units) x (nominal median value of homes)

o GDP

(population) x (nominal GDP per capita)

Normalization of past direct economic losses to current levels of wealth:

𝑙𝑜𝑠𝑠𝑛𝑜𝑟𝑚𝑎𝑙𝑖𝑧𝑒𝑑 𝑡𝑜𝑑𝑎𝑦 = 𝑙𝑜𝑠𝑠𝑦𝑟 𝑜𝑓 𝑒𝑣𝑒𝑛𝑡 ∗𝑛𝑜𝑚𝑖𝑛𝑎𝑙 𝑑𝑒𝑠𝑡𝑟𝑢𝑐𝑡𝑖𝑏𝑙𝑒 𝑤𝑒𝑎𝑙𝑡ℎ𝑡𝑜𝑑𝑎𝑦

𝑛𝑜𝑚𝑖𝑛𝑎𝑙 𝑑𝑒𝑠𝑡𝑟𝑢𝑐𝑡𝑖𝑏𝑙𝑒 𝑤𝑒𝑎𝑙𝑡ℎ𝑦𝑟 𝑜𝑓 𝑒𝑣𝑒𝑛𝑡 1

Only data available worldwide!

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

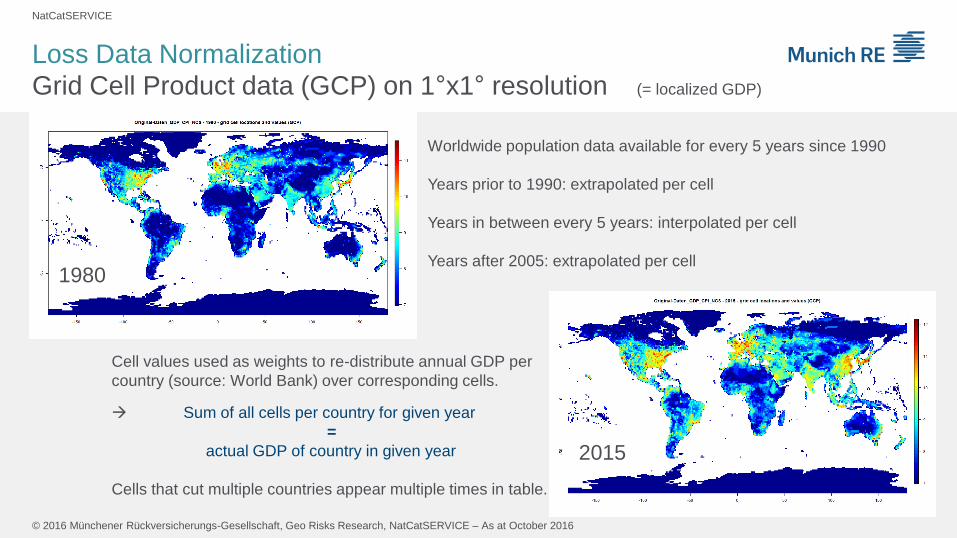

Loss Data Normalization

Grid Cell Product data (GCP) on 1°x1° resolution (= localized GDP)

1980

2015

Worldwide population data available for every 5 years since 1990

Years prior to 1990: extrapolated per cell

Years in between every 5 years: interpolated per cell

Years after 2005: extrapolated per cell

Cell values used as weights to re-distribute annual GDP per

country (source: World Bank) over corresponding cells.

Sum of all cells per country for given year

=

actual GDP of country in given year

Cells that cut multiple countries appear multiple times in table.

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Loss Data Normalization

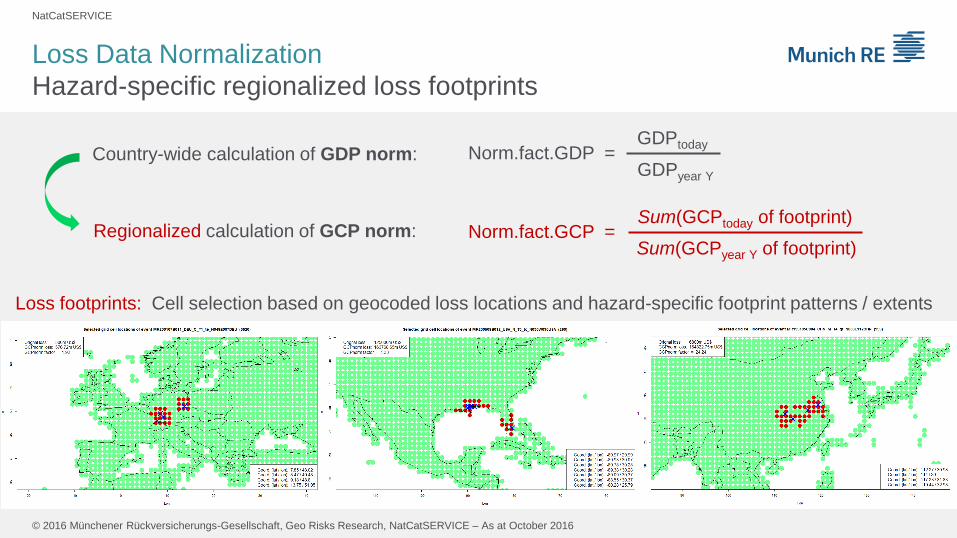

Hazard-specific regionalized loss footprints

Loss footprints: Cell selection based on geocoded loss locations and hazard-specific footprint patterns / extents

Norm.fact.GDP = GDPtoday

GDPyear Y

Country-wide calculation of GDP norm:

Norm.fact.GCP = Sum(GCPtoday of footprint)

Sum(GCPyear Y of footprint) Regionalized calculation of GCP norm:

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

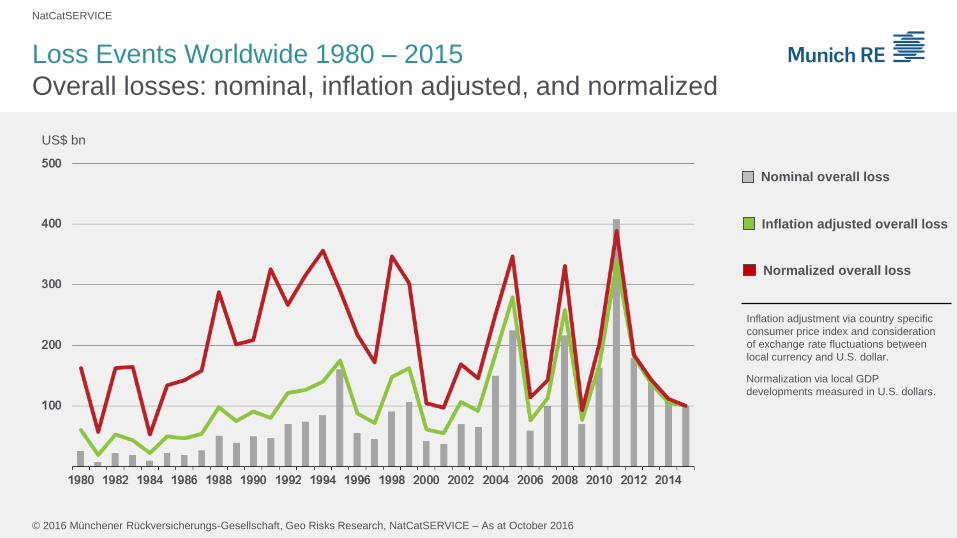

Loss Events Worldwide 1980 – 2015

Overall losses: nominal, inflation adjusted, and normalized

Nominal overall loss

Inflation adjusted overall loss

Normalized overall loss

Inflation adjustment via country specific

consumer price index and consideration

of exchange rate fluctuations between

local currency and U.S. dollar.

Normalization via local GDP

developments measured in U.S. dollars.

US$ bn

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Classification of Loss Events

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

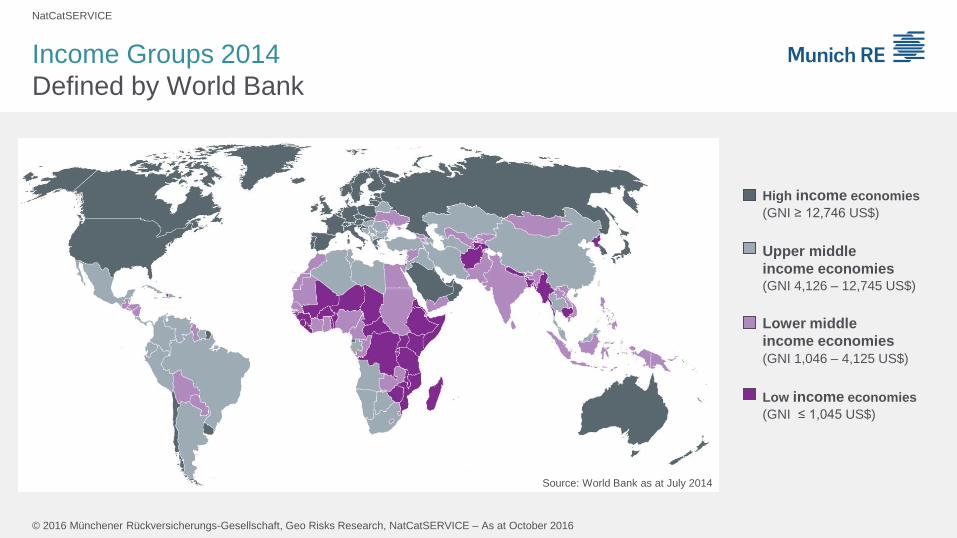

Income Groups 2014

Defined by World Bank

High income economies

Upper middle

income economies

Lower middle

income economies

Low income economies

(GNI ≥ 12,746 US$)

(GNI 4,126 – 12,745 US$)

(GNI 1,046 – 4,125 US$)

(GNI ≤ 1,045 US$)

Source: World Bank as at July 2014

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

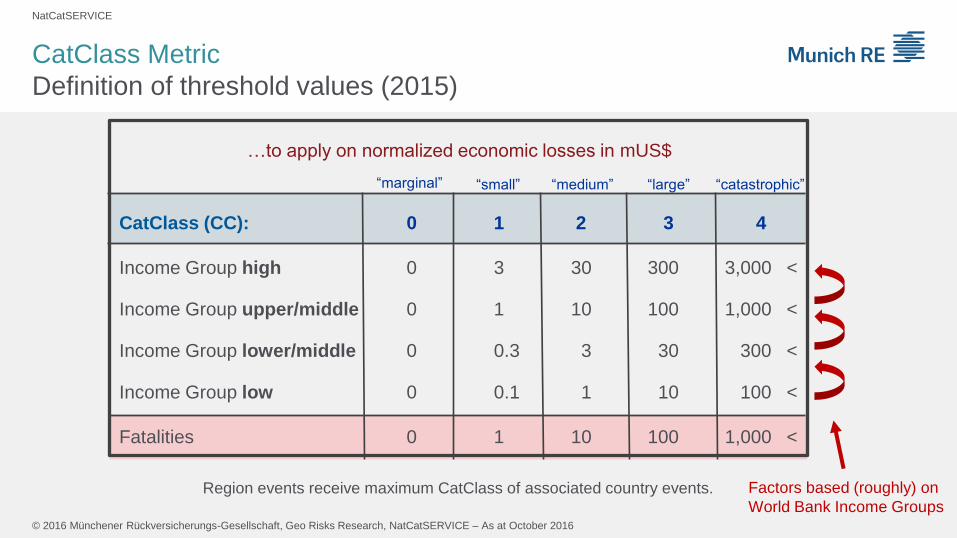

CatClass Metric

Definition of threshold values (2015)

Region events receive maximum CatClass of associated country events.

CatClass (CC): 0 1 2 3 4

Income Group high 0 3 30 300 3,000 <

Income Group upper/middle 0 1 10 100 1,000 <

Income Group lower/middle 0 0.3 3 30 300 <

Income Group low 0 0.1 1 10 100 <

Fatalities 0 1 10 100 1,000 <

Factors based (roughly) on

World Bank Income Groups

…to apply on normalized economic losses in mUS$

“marginal” “small” “medium” “large” “catastrophic”

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

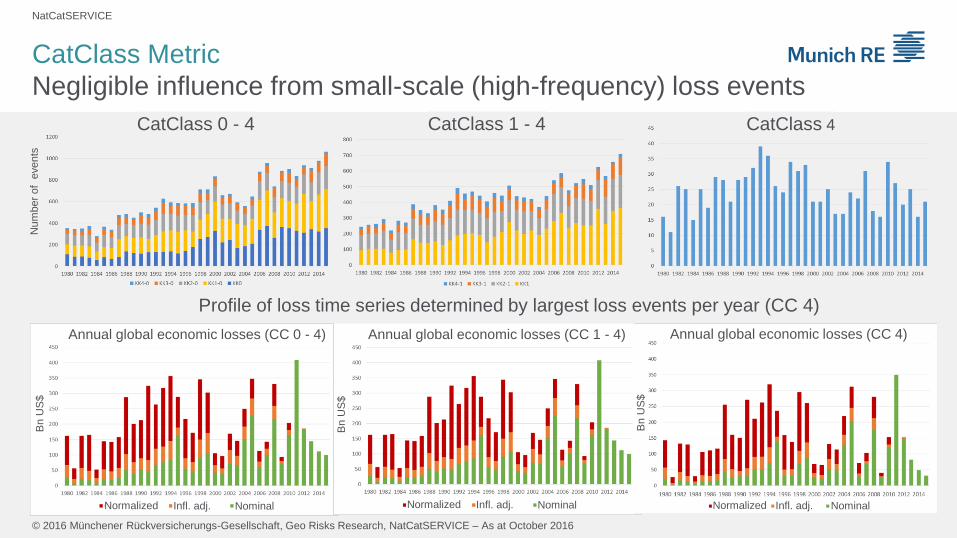

CatClass Metric

Negligible influence from small-scale (high-frequency) loss events

CatClass 0 - 4 CatClass 1 - 4 CatClass 4

Annual global economic losses (CC 0 - 4)

Bn U

S$

Normalized Infl. adj. Nominal

Annual global economic losses (CC 1 - 4) B

n U

S$

Normalized Infl. adj. Nominal

Profile of loss time series determined by largest loss events per year (CC 4)

Annual global economic losses (CC 4)

Normalized Infl. adj. Nominal

Bn U

S$

Num

ber

of

events

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

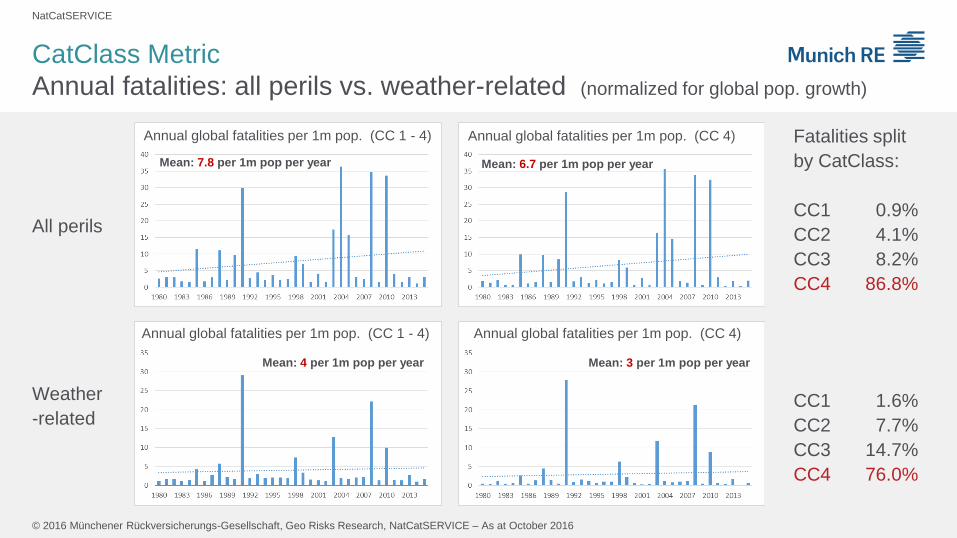

CatClass Metric

Annual fatalities: all perils vs. weather-related (normalized for global pop. growth)

Fatalities split

by CatClass:

CC1 0.9%

CC2 4.1%

CC3 8.2%

CC4 86.8%

Annual global fatalities per 1m pop. (CC 1 - 4)

Mean: 7.8 per 1m pop per year

Annual global fatalities per 1m pop. (CC 4)

Mean: 6.7 per 1m pop per year

All perils

Annual global fatalities per 1m pop. (CC 1 - 4) Annual global fatalities per 1m pop. (CC 4)

Mean: 4 per 1m pop per year Mean: 3 per 1m pop per year

Weather

-related CC1 1.6%

CC2 7.7%

CC3 14.7%

CC4 76.0%

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

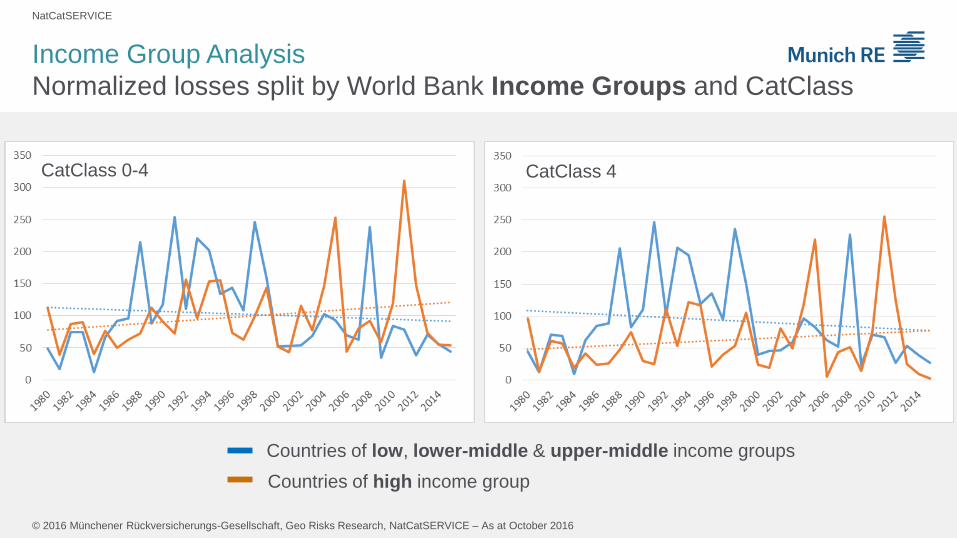

Income Group Analysis

Normalized losses split by World Bank Income Groups and CatClass

Countries of low, lower-middle & upper-middle income groups

Countries of high income group

CatClass 0-4 CatClass 4

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Thank You!

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Example: correlation with meteorological indices

Loss Data Analytics

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

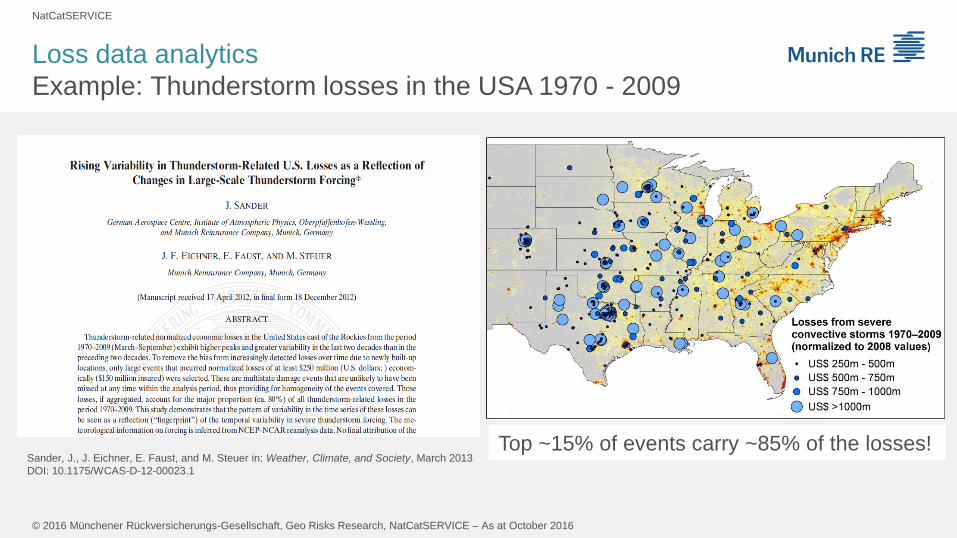

Sander, J., J. Eichner, E. Faust, and M. Steuer in: Weather, Climate, and Society, March 2013

DOI: 10.1175/WCAS-D-12-00023.1

Top ~15% of events carry ~85% of the losses!

Loss data analytics

Example: Thunderstorm losses in the USA 1970 - 2009

NatCatSERVICE

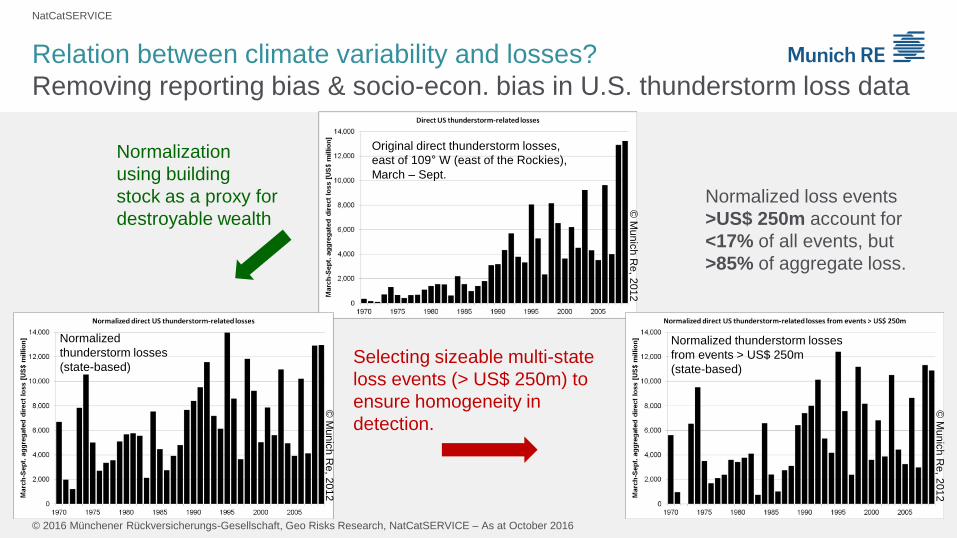

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

© M

unic

h R

e, 2

012

Original direct thunderstorm losses,

east of 109° W (east of the Rockies),

March – Sept.

© M

unic

h R

e, 2

012

Normalized

thunderstorm losses

(state-based)

© M

unic

h R

e, 2

012

Normalized thunderstorm losses

from events > US$ 250m

(state-based) Selecting sizeable multi-state

loss events (> US$ 250m) to

ensure homogeneity in

detection.

Normalization

using building

stock as a proxy for

destroyable wealth

Normalized loss events

>US$ 250m account for

<17% of all events, but

>85% of aggregate loss.

Relation between climate variability and losses?

Removing reporting bias & socio-econ. bias in U.S. thunderstorm loss data

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Relation between climate variability and losses?

NCEP/NCAR reanalysis data

NCEP/NCAR reanalysis data: symbiosis of climate model and measurements

• Worldwide grid with 1.875° x 1.915° spatial and

6h temporal resolution

• Selected data: 1970 – 2009, March – September

Chosen grid points for analysis:

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

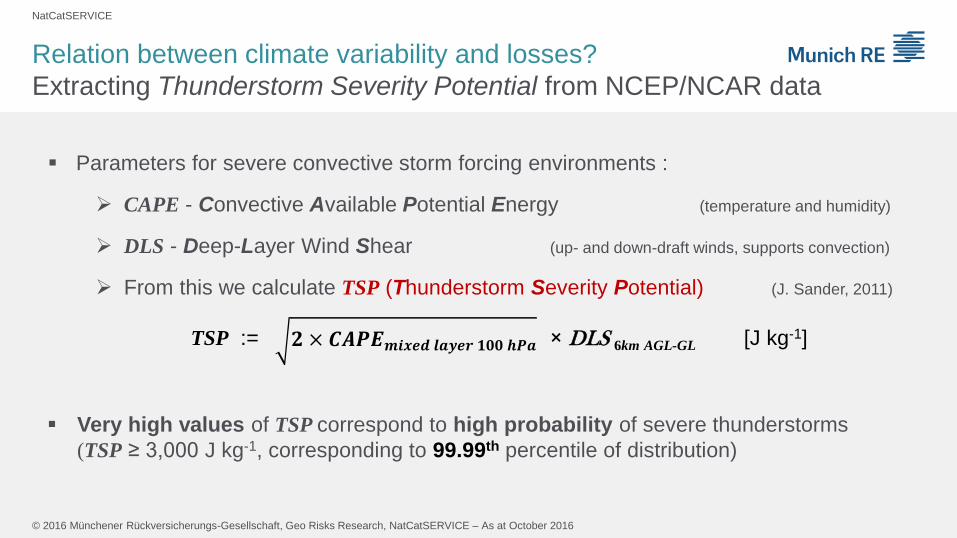

𝟐 × 𝑪𝑨𝑷𝑬𝒎𝒊𝒙𝒆𝒅 𝒍𝒂𝒚𝒆𝒓 𝟏𝟎𝟎 𝒉𝑷𝒂 1

Parameters for severe convective storm forcing environments :

CAPE - Convective Available Potential Energy (temperature and humidity)

DLS - Deep-Layer Wind Shear (up- and down-draft winds, supports convection)

From this we calculate TSP (Thunderstorm Severity Potential) (J. Sander, 2011)

TSP := × DLS 6km AGL-GL [J kg-1]

Very high values of TSP correspond to high probability of severe thunderstorms

(TSP ≥ 3,000 J kg-1, corresponding to 99.99th percentile of distribution)

Relation between climate variability and losses?

Extracting Thunderstorm Severity Potential from NCEP/NCAR data

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Correlations may appear in…

…FREQUENCY of events or

…INTENSITY of events or

…BOTH

Hence, we have to look at both at the same time:

• NUMBERS of threshold exceedances per time step (counts)

• SUMS of INTENSITIES exceeding the thresholds per time step (aggregated values)

Relation between climate variability and losses?

Correlation between TSP environment and loss data

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Sta

nd

ard

ize

d s

easona

l

co

un

t

Sta

nd

ard

ize

d s

easona

l

ag

gre

gate

d v

alu

e

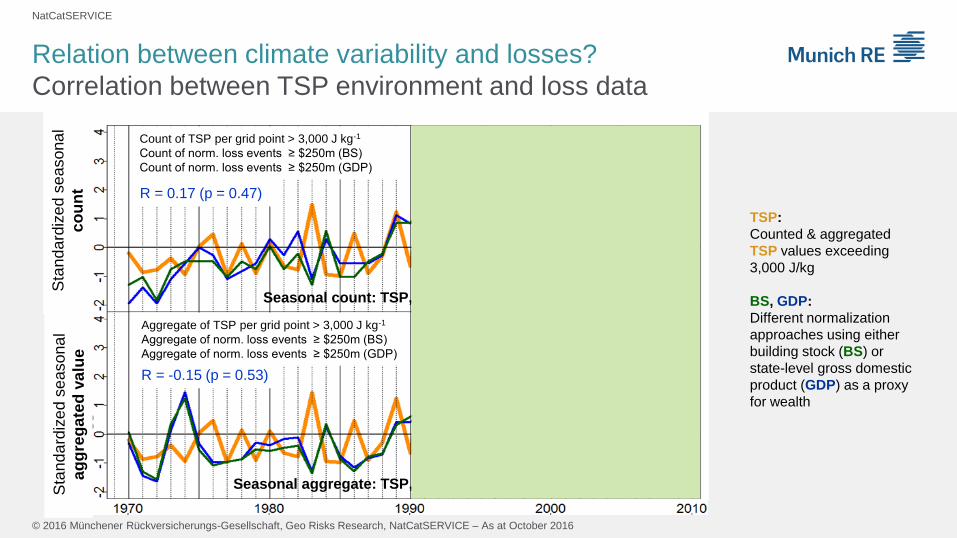

Seasonal count: TSP, norm. economic losses

Seasonal aggregate: TSP, norm. economic losses

Count of TSP per grid point > 3,000 J kg-1

Count of norm. loss events ≥ $250m (BS)

Count of norm. loss events ≥ $250m (GDP)

Aggregate of TSP per grid point > 3,000 J kg-1

Aggregate of norm. loss events ≥ $250m (BS)

Aggregate of norm. loss events ≥ $250m (GDP)

TSP:

Counted & aggregated

TSP values exceeding

3,000 J/kg

BS, GDP:

Different normalization

approaches using either

building stock (BS) or

state-level gross domestic

product (GDP) as a proxy

for wealth

Relation between climate variability and losses?

Correlation between TSP environment and loss data

R = 0.43 (p = 0.058)

R = 0.64 (p = 0.002)

R = 0.17 (p = 0.47)

R = -0.15 (p = 0.53)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

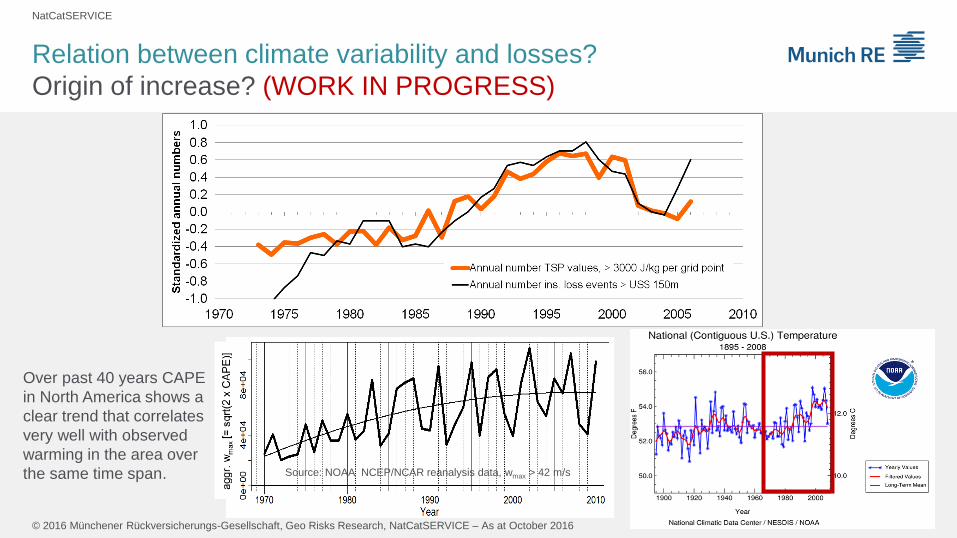

Over past 40 years CAPE

in North America shows a

clear trend that correlates

very well with observed

warming in the area over

the same time span. Source: NOAA NCEP/NCAR reanalysis data, wmax > 42 m/s

Relation between climate variability and losses?

Origin of increase? (WORK IN PROGRESS)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

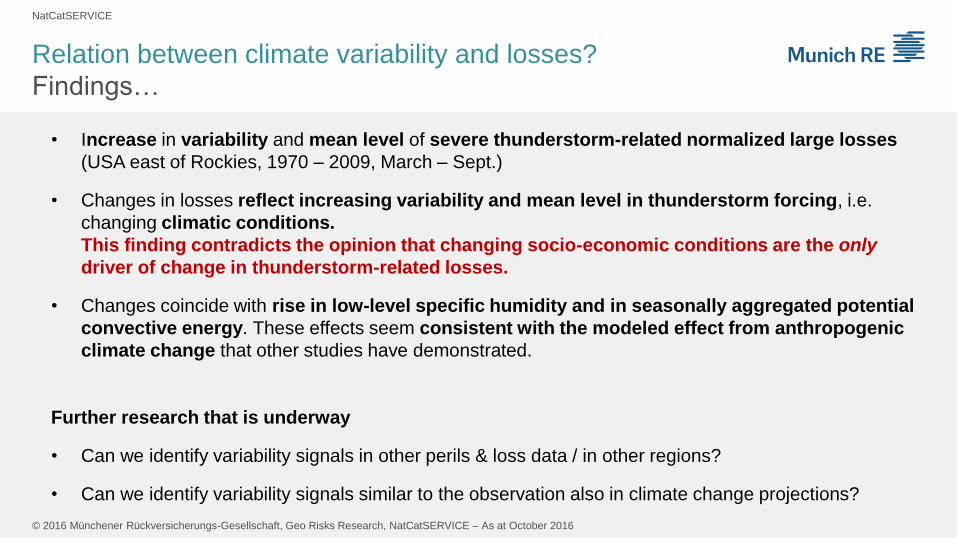

• Increase in variability and mean level of severe thunderstorm-related normalized large losses

(USA east of Rockies, 1970 – 2009, March – Sept.)

• Changes in losses reflect increasing variability and mean level in thunderstorm forcing, i.e.

changing climatic conditions.

This finding contradicts the opinion that changing socio-economic conditions are the only

driver of change in thunderstorm-related losses.

• Changes coincide with rise in low-level specific humidity and in seasonally aggregated potential

convective energy. These effects seem consistent with the modeled effect from anthropogenic

climate change that other studies have demonstrated.

Further research that is underway

• Can we identify variability signals in other perils & loss data / in other regions?

• Can we identify variability signals similar to the observation also in climate change projections?

Relation between climate variability and losses?

Findings…

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Back-up slides

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

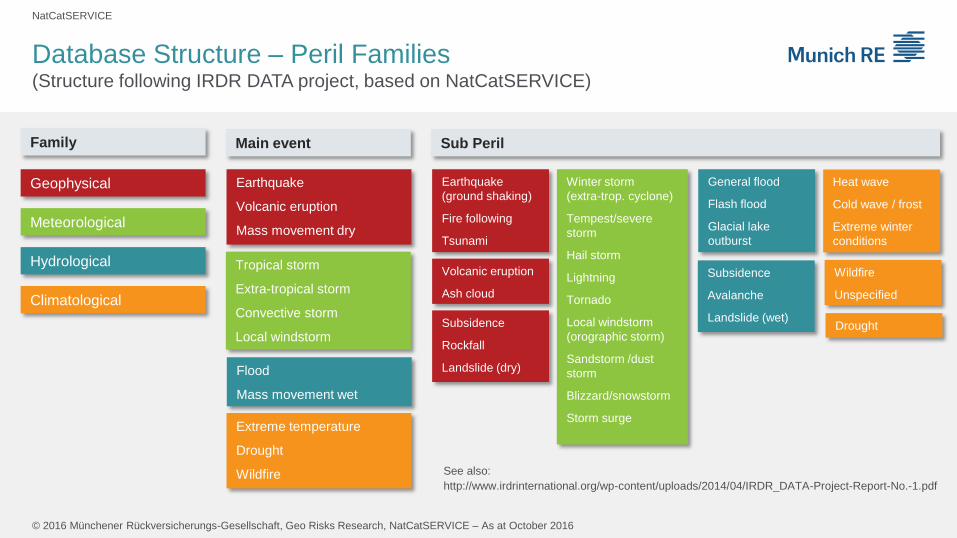

Database Structure – Peril Families (Structure following IRDR DATA project, based on NatCatSERVICE)

Geophysical

Meteorological

Hydrological

Climatological

Family Main event

Earthquake

Volcanic eruption

Mass movement dry

Tropical storm

Extra-tropical storm

Convective storm

Local windstorm

Flood

Mass movement wet

Extreme temperature

Drought

Wildfire

Sub Peril

Earthquake

(ground shaking)

Fire following

Tsunami

Volcanic eruption

Ash cloud

Subsidence

Rockfall

Landslide (dry)

Winter storm

(extra-trop. cyclone)

Tempest/severe

storm

Hail storm

Lightning

Tornado

Local windstorm

(orographic storm)

Sandstorm /dust

storm

Blizzard/snowstorm

Storm surge

General flood

Flash flood

Glacial lake

outburst

Subsidence

Avalanche

Landslide (wet)

Heat wave

Cold wave / frost

Extreme winter

conditions

Drought

Wildfire

Unspecified

See also:

http://www.irdrinternational.org/wp-content/uploads/2014/04/IRDR_DATA-Project-Report-No.-1.pdf

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

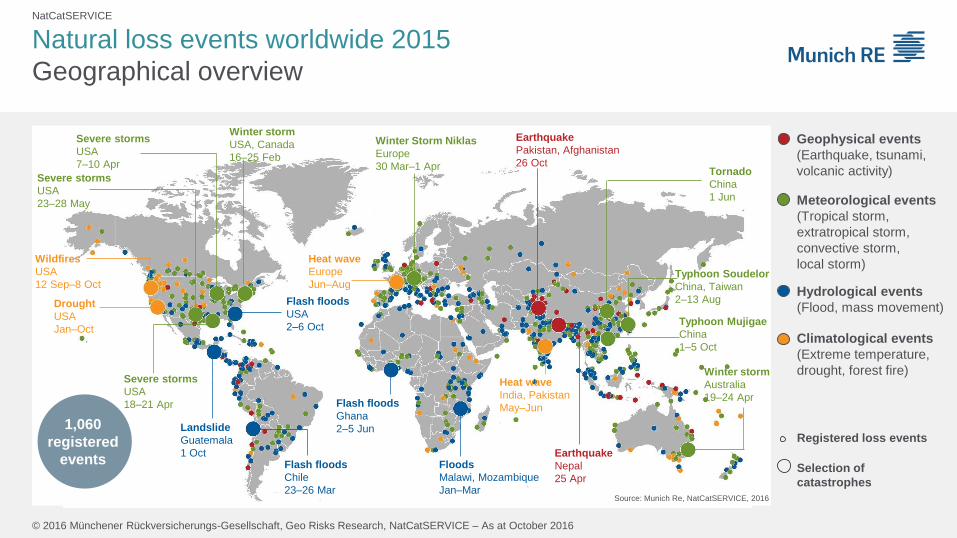

Natural loss events worldwide 2015

Geographical overview

1,060

registered

events

Source: Munich Re, NatCatSERVICE, 2016

Drought

USA

Jan–Oct

Earthquake

Nepal

25 Apr

Winter Storm Niklas

Europe

30 Mar–1 Apr

Severe storms

USA

7–10 Apr

Typhoon Mujigae

China

1–5 Oct

Severe storms

USA

23–28 May

Earthquake

Pakistan, Afghanistan

26 Oct

Heat wave

India, Pakistan

May–Jun

Tornado

China

1 Jun

Winter storm

Australia

19–24 Apr

Flash floods

Chile

23–26 Mar

Flash floods

Ghana

2–5 Jun

Floods

Malawi, Mozambique

Jan–Mar

Landslide

Guatemala

1 Oct

Flash floods

USA

2–6 Oct

Winter storm

USA, Canada

16–25 Feb

Severe storms

USA

18–21 Apr

Wildfires

USA

12 Sep–8 Oct

Heat wave

Europe

Jun–Aug Typhoon Soudelor

China, Taiwan

2–13 Aug

Meteorological events

(Tropical storm,

extratropical storm,

convective storm,

local storm)

Hydrological events

(Flood, mass movement)

Climatological events

(Extreme temperature,

drought, forest fire)

Geophysical events

(Earthquake, tsunami,

volcanic activity)

Selection of

catastrophes

Registered loss events

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

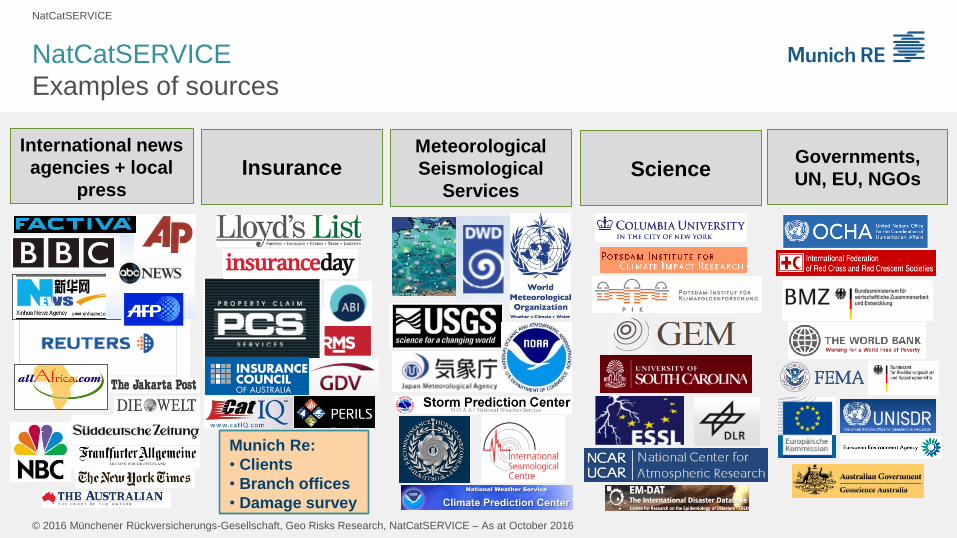

NatCatSERVICE

Examples of sources

Science Governments,

UN, EU, NGOs

International news

agencies + local

press

Meteorological

Seismological

Services

Insurance

Munich Re:

• Clients

• Branch offices

• Damage survey

NatCatSERVICE

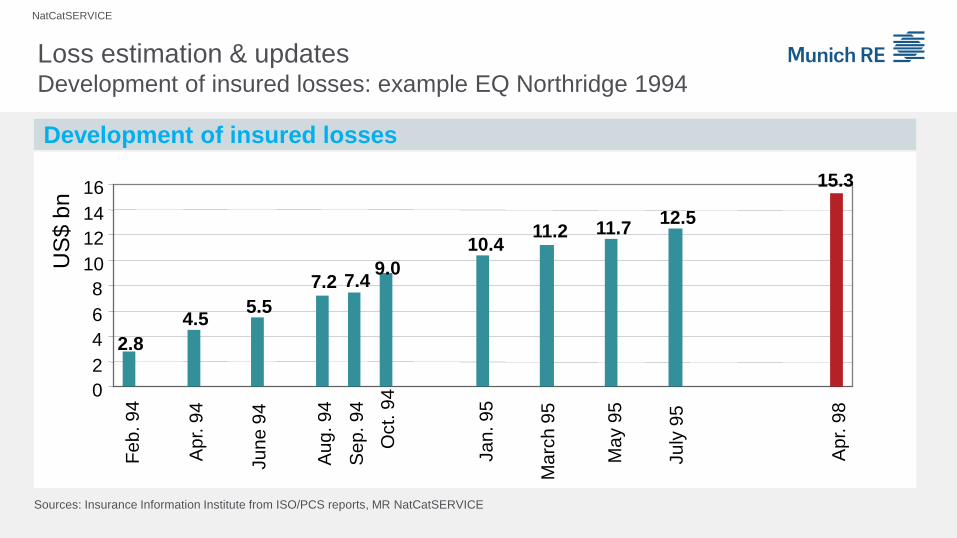

Loss estimation & updates Development of insured losses: example EQ Northridge 1994

Development of insured losses

Sources: Insurance Information Institute from ISO/PCS reports, MR NatCatSERVICE

2.8

7.2 7.4 9.0

11.2

15.3

4.5 5.5

10.4 11.7

12.5

0

2

4

6

8

10

12

14

16

Fe

b. 9

4

Ap

r. 9

4

Ju

ne

94

Au

g. 9

4

Se

p. 9

4

Oct.

94

Ja

n. 9

5

Ma

rch

95

May 9

5

Ju

ly 9

5

Ap

r. 9

8

US

$ b

n

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

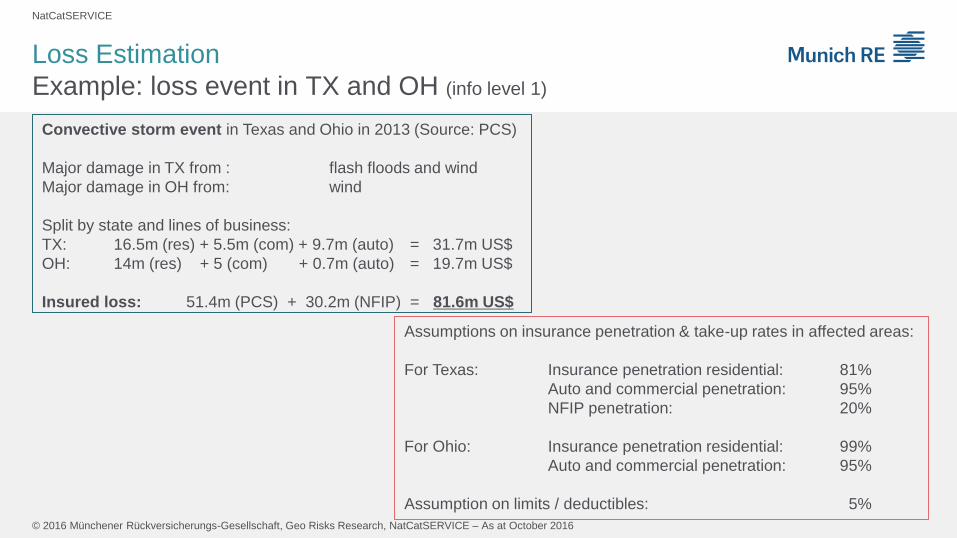

Convective storm event in Texas and Ohio in 2013 (Source: PCS)

Major damage in TX from : flash floods and wind

Major damage in OH from: wind

Split by state and lines of business:

TX: 16.5m (res) + 5.5m (com) + 9.7m (auto) = 31.7m US$

OH: 14m (res) + 5 (com) + 0.7m (auto) = 19.7m US$

Insured loss: 51.4m (PCS) + 30.2m (NFIP) = 81.6m US$

Assumptions on insurance penetration & take-up rates in affected areas:

For Texas: Insurance penetration residential: 81%

Auto and commercial penetration: 95%

NFIP penetration: 20%

For Ohio: Insurance penetration residential: 99%

Auto and commercial penetration: 95%

Assumption on limits / deductibles: 5%

Loss Estimation

Example: loss event in TX and OH (info level 1)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

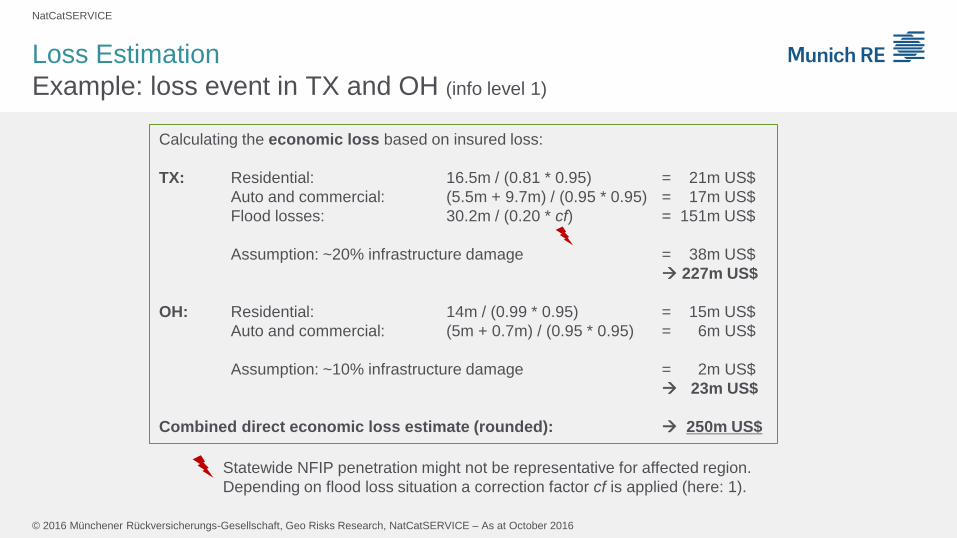

Statewide NFIP penetration might not be representative for affected region.

Depending on flood loss situation a correction factor cf is applied (here: 1).

Calculating the economic loss based on insured loss:

TX: Residential: 16.5m / (0.81 * 0.95) = 21m US$

Auto and commercial: (5.5m + 9.7m) / (0.95 * 0.95) = 17m US$

Flood losses: 30.2m / (0.20 * cf) = 151m US$

Assumption: ~20% infrastructure damage = 38m US$

227m US$

OH: Residential: 14m / (0.99 * 0.95) = 15m US$

Auto and commercial: (5m + 0.7m) / (0.95 * 0.95) = 6m US$

Assumption: ~10% infrastructure damage = 2m US$

23m US$

Combined direct economic loss estimate (rounded): 250m US$

Loss Estimation

Example: loss event in TX and OH (info level 1)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

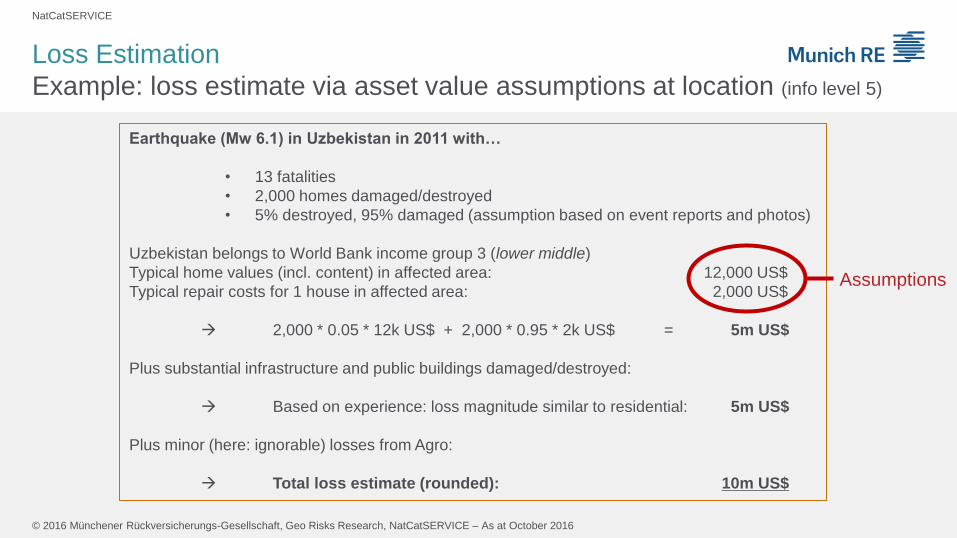

Earthquake (Mw 6.1) in Uzbekistan in 2011 with…

• 13 fatalities

• 2,000 homes damaged/destroyed

• 5% destroyed, 95% damaged (assumption based on event reports and photos)

Uzbekistan belongs to World Bank income group 3 (lower middle)

Typical home values (incl. content) in affected area: 12,000 US$

Typical repair costs for 1 house in affected area: 2,000 US$

2,000 * 0.05 * 12k US$ + 2,000 * 0.95 * 2k US$ = 5m US$

Plus substantial infrastructure and public buildings damaged/destroyed:

Based on experience: loss magnitude similar to residential: 5m US$

Plus minor (here: ignorable) losses from Agro:

Total loss estimate (rounded): 10m US$

Loss Estimation

Example: loss estimate via asset value assumptions at location (info level 5)

Assumptions

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

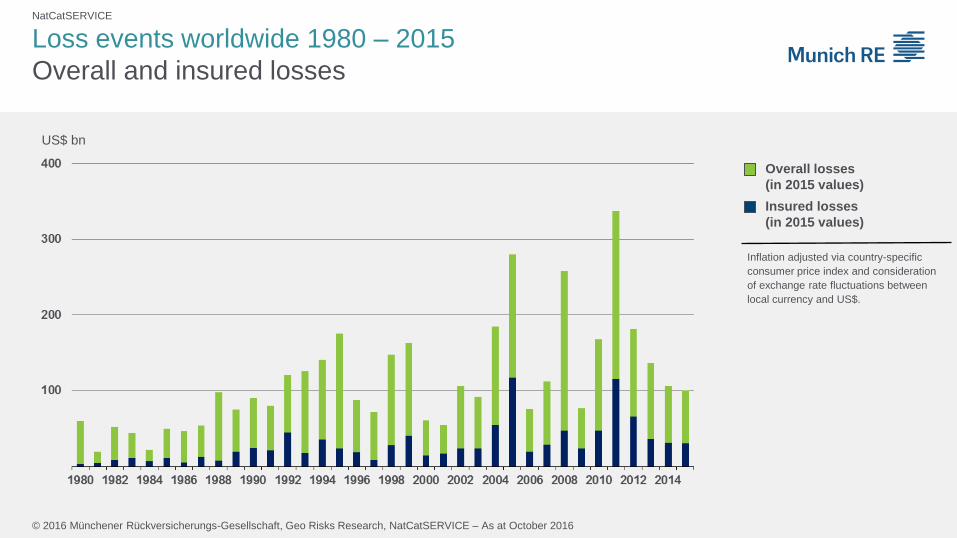

Loss events worldwide 1980 – 2015

Overall and insured losses

US$ bn

Overall losses

(in 2015 values)

Insured losses

(in 2015 values)

Inflation adjusted via country-specific

consumer price index and consideration

of exchange rate fluctuations between

local currency and US$.

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

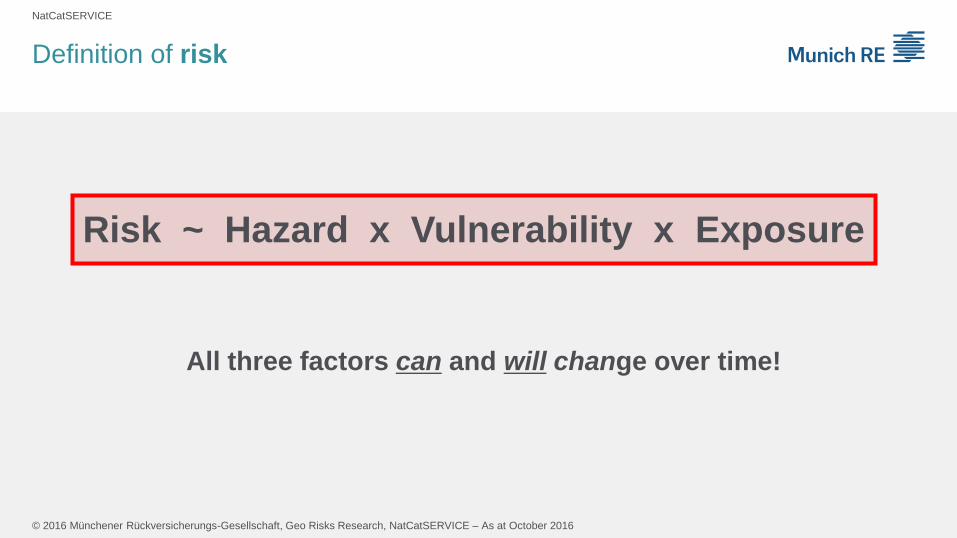

Definition of risk

All three factors can and will change over time!

Risk ~ Hazard x Vulnerability x Exposure

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

Examples of drivers of NatCat losses

Exposure:

Inflation, increase of wealth, increase of building stock, population increase/shift etc.

1914

2012

Vulnerability:

Building codes, improved and hardened materials, expensive materials, flood zones etc.

Hazard:

Natural variability (rather short time scales)

Climate change (long time scales)

El Niño La Niña

Jet stream

during La Niña:

Shift of tornado

Activity in U.S.

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

NatCatSERVICE

Limitations of GDP norm

“Natural hazards don’t know borders!”

Socio-economic development can be very different within the same country.

Economic disparity may lead to over-/under-normalization of losses because

macro-economic proxy data is not representative for regional / local conditions.

Strongest effects observed in China:

Most of the economic development in China has happened along coast lines and

major cities, and to a much lesser extent inland.

Loss data from many severe river flood events inland in the 1990s would be

normalized with economic proxy rather valid for the coastal areas.

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

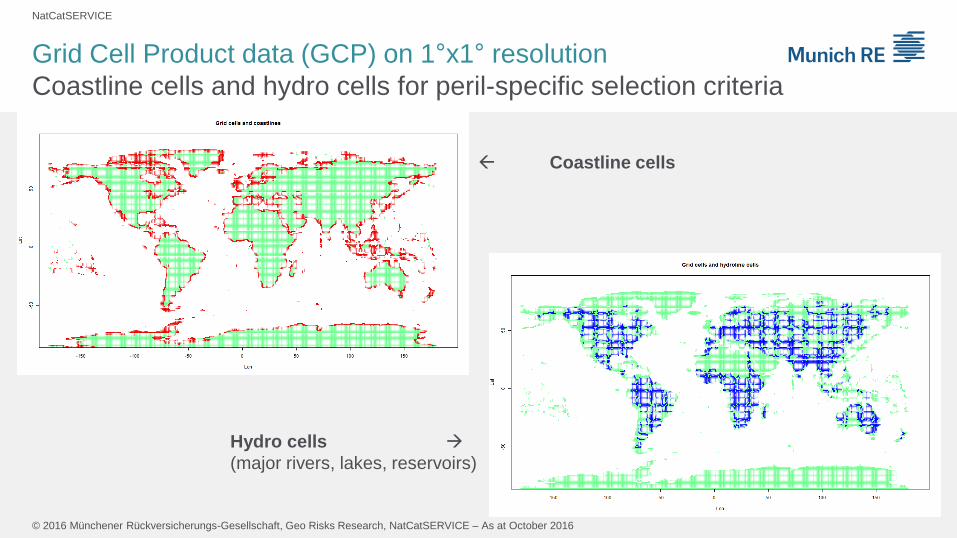

Grid Cell Product data (GCP) on 1°x1° resolution

Coastline cells and hydro cells for peril-specific selection criteria

Coastline cells

Hydro cells

(major rivers, lakes, reservoirs)

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

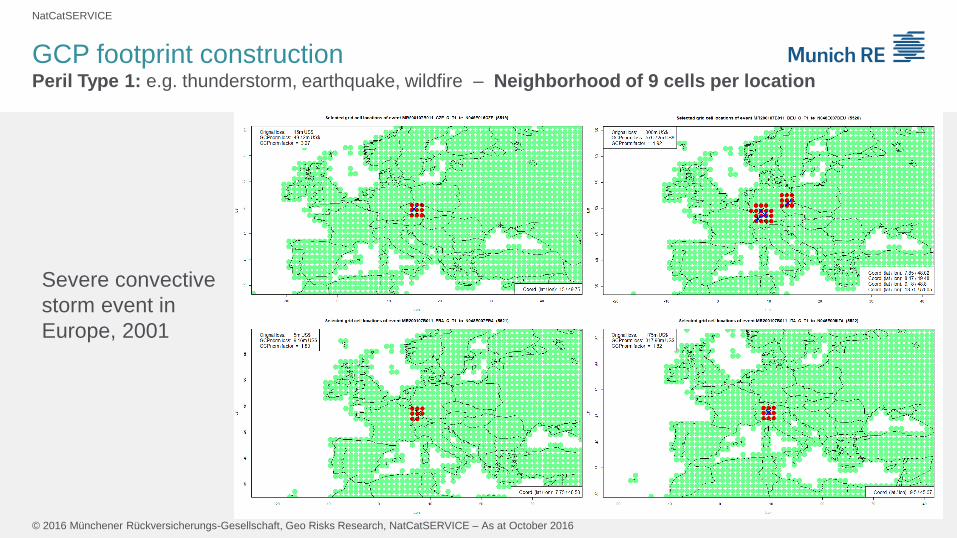

GCP footprint construction Peril Type 1: e.g. thunderstorm, earthquake, wildfire – Neighborhood of 9 cells per location

Severe convective

storm event in

Europe, 2001

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

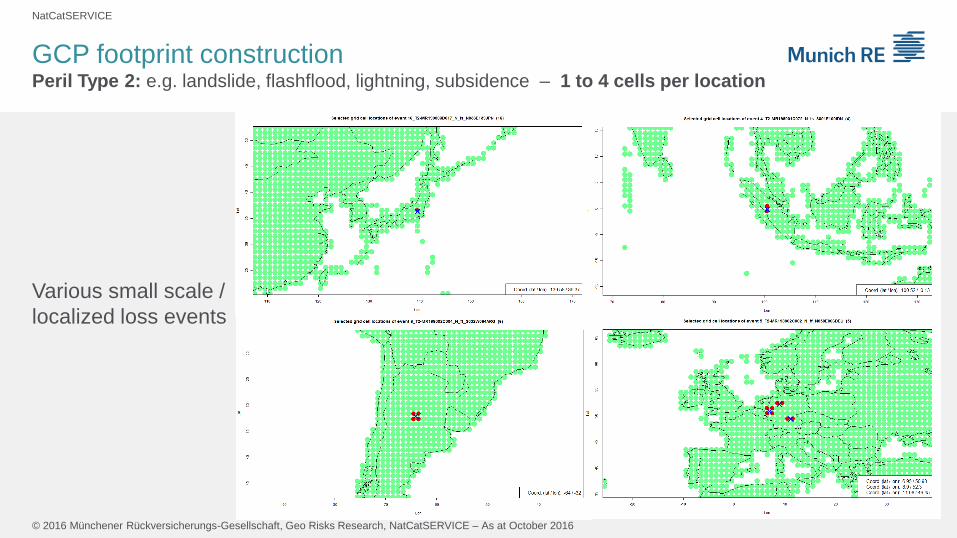

Various small scale /

localized loss events

GCP footprint construction Peril Type 2: e.g. landslide, flashflood, lightning, subsidence – 1 to 4 cells per location

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

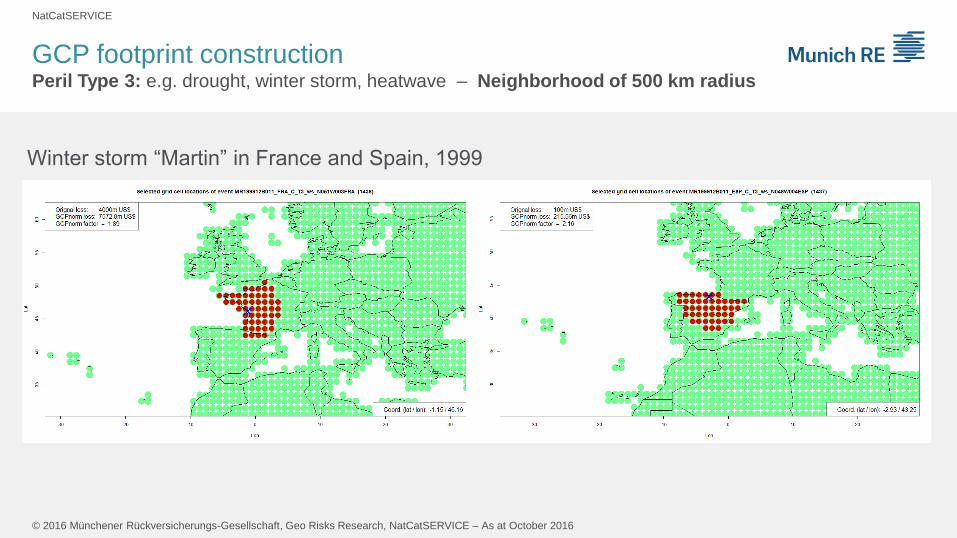

Winter storm “Martin” in France and Spain, 1999

GCP footprint construction Peril Type 3: e.g. drought, winter storm, heatwave – Neighborhood of 500 km radius

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

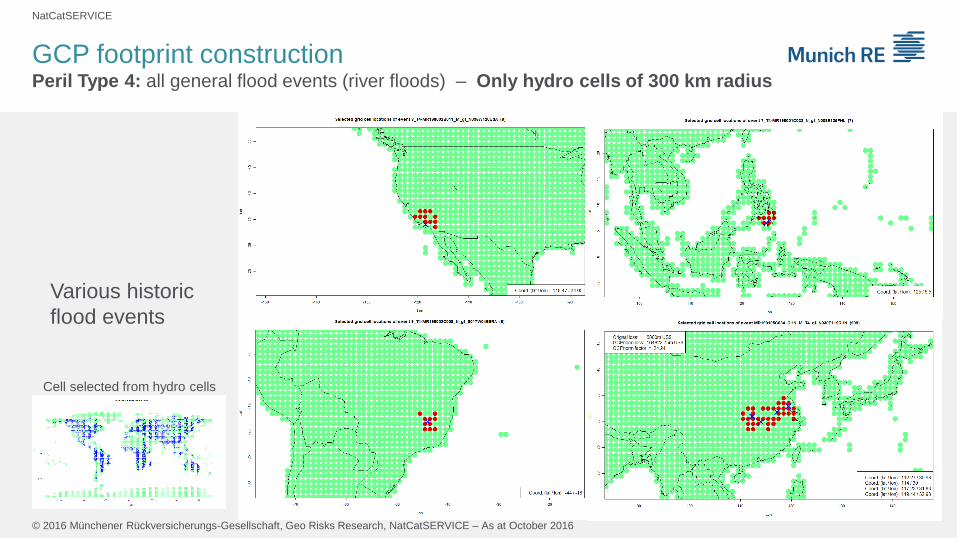

Various historic

flood events

Cell selected from hydro cells

GCP footprint construction Peril Type 4: all general flood events (river floods) – Only hydro cells of 300 km radius

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

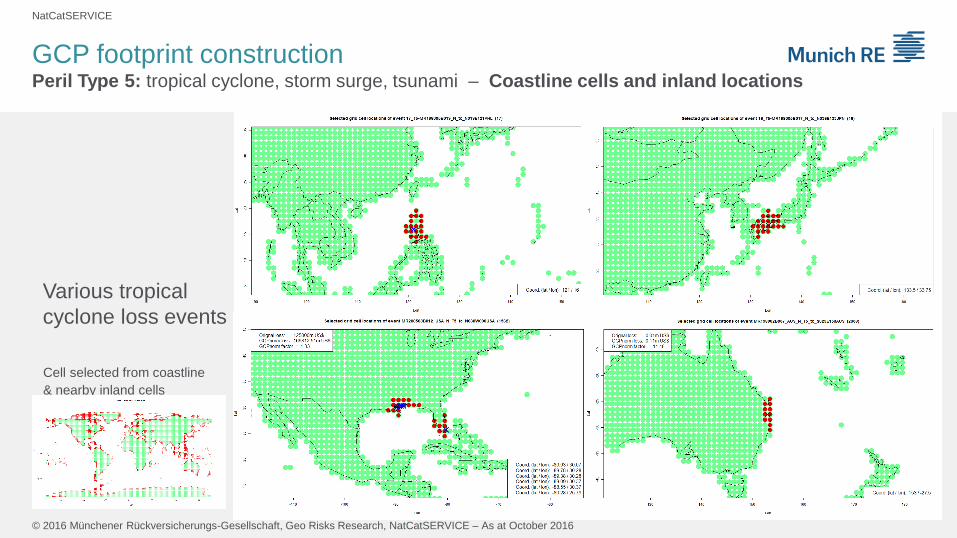

GCP footprint construction Peril Type 5: tropical cyclone, storm surge, tsunami – Coastline cells and inland locations

Various tropical

cyclone loss events

Cell selected from coastline

& nearby inland cells

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

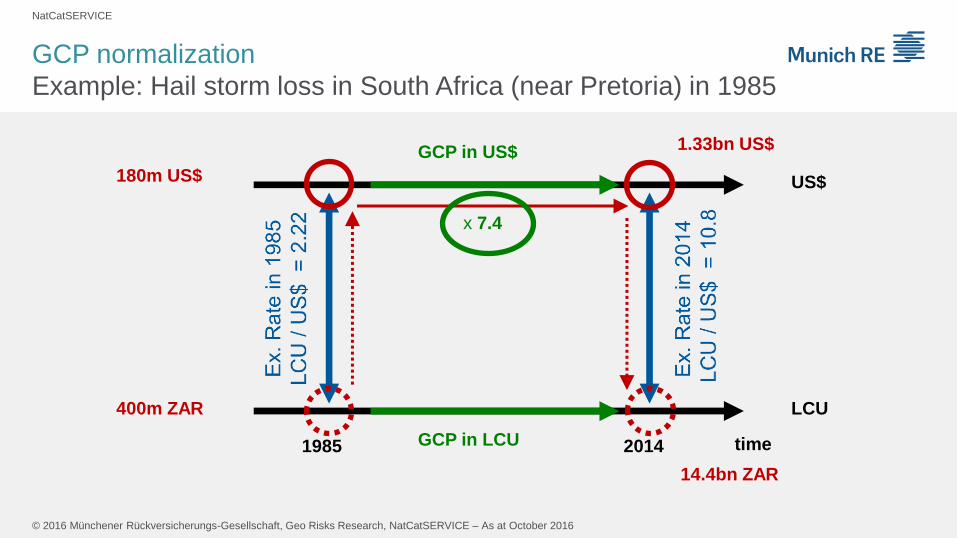

GCP normalization

Example: Hail storm loss in South Africa (near Pretoria) in 1985

time

US$

LCU

1985 2014

GCP in US$

GCP in LCU

400m ZAR

180m US$

1.33bn US$

x 7.4

14.4bn ZAR

NatCatSERVICE

© 2016 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As at October 2016

GCP normalization

Top 10 loss events after normalization

x 24

![170321 Eichner AAPV-SAPV WS-1.ppt [Kompatibilitätsmodus] · (E. Eichner 2010, phil. Dissertation, noch unveröffentlicht ) Verordnung von SAPV Dr. Eckhard Eichner Augsburger Hospiz-und](https://static.fdokument.com/doc/165x107/60609454bd5cd41a4c0b187b/170321-eichner-aapv-sapv-ws-1ppt-kompatibilittsmodus-e-eichner-2010-phil.jpg)

![Stadtwerke Gütersloh GmbH - Startseite – Gütersloh · Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Jan. 11 Jan. 12 Jan. 13 Jan. 14 Jan. 15 Jan. 16 mg/l el.LF in [mS/m] Entwicklung](https://static.fdokument.com/doc/165x107/6028370154309631231c90b8/stadtwerke-gtersloh-gmbh-startseite-a-gtersloh-jan-06-jan-07-jan-08-jan.jpg)