Understanding futures markets - USC Dana and …...Understanding Futures Markets Michael J. P....

21

Understanding Futures Markets Michael J. P. Magill Zusammenfassung Die Arbeit besteht aus drei Teilen: Der erste enth~lt einige empirische Eigenschaften von Terminm~irkten; der zweite gibt einen kurzen 0berblick 0ber die "klassischen" Theorien von Keynes, Kaldor und Working; und der dritte (Haupt-)Teil ist der modernen Theode die- ser M~irkte gewidmet. Die moderne Theorie unterscheidet sich von der klassischen u. a. durch eine explizite BerQcksichtigung der Informationsstruktur und Erwartungsbildung so- wie durch die systematische Verwendung von Gleichgewichtsbegriffen. Gesti3tzt auf neu- ere Resultate verschiedener Autoren wird gezeigt, wie die moderne Theorie zur Klw einer Reihe von Fragen dienen kann, z. B. der Bedingungen, unter denen Terminm~rkte zu einer Pareto-effizienten AIIokation fQhren, des Zusammenhangs zwischen Terminpreis- schwankungen und Informationsstruktur, des Einflusses von Terminm~irkten auf Produk- tionsentscheidungen, des Ausma6es, in dem die Preise auf Terminm~rkten private Informa- tion aggregieren, usw. 1. Introduction A basic characteristic of resource allocation over time is that the agents in an economy (consumers and producers) lack information about future endowments, tastes, and tech- nology. This lack of information, or more briefly uncertainty reflects the limitations of both individual and collective knowledge about the future. In an effort to cope with this uncer- tainty and with the risks that it implies for the agents, the major market economies of the West have over the last two hundred years developed three market institutions on which risk and information can be traded in a systematic and efficient way -- these are the mar- kets for insurance and the organized security and commodity exchanges. While these market institutions have been in existence for a long time, attempts to develop formal theoretical models that explain how they function are of much more recent origin. The first general theory of resource allocation under uncertainty was developed by Arrow (1964) and Debreu (1959): This is the so-called complete contingent markets model, a can- onical model of great generality to which more specialized models with apparently more restrictive structure can often be reduced by suitable transformation. Thus, Malinvaud (1972) has shown how the Arrow-Debreu model may be used as a model of insurance mar- kets: He shows that if there is no social risk (the aggregate endowment is non-random via the law of large numbers), then in equilibrium each consumer is offered actuarily fair insur- ance and hence by risk aversion seeks complete insurance. 125

Transcript of Understanding futures markets - USC Dana and …...Understanding Futures Markets Michael J. P....

Understanding Futures Markets

Michael J. P. Magill

Zusammenfassung

Die Arbeit besteht aus drei Teilen: Der erste enth~lt einige empirische Eigenschaften von Terminm~irkten; der zweite gibt einen kurzen 0berblick 0ber die "klassischen" Theorien von Keynes, Kaldor und Working; und der dritte (Haupt-)Teil ist der modernen Theode die- ser M~irkte gewidmet. Die moderne Theorie unterscheidet sich von der klassischen u. a. durch eine explizite BerQcksichtigung der Informationsstruktur und Erwartungsbildung so- wie durch die systematische Verwendung von Gleichgewichtsbegriffen. Gesti3tzt auf neu- ere Resultate verschiedener Autoren wird gezeigt, wie die moderne Theorie zur Klw einer Reihe von Fragen dienen kann, z. B. der Bedingungen, unter denen Terminm~rkte zu

einer Pareto-effizienten AIIokation fQhren, des Zusammenhangs zwischen Terminpreis- schwankungen und Informationsstruktur, des Einflusses von Terminm~irkten auf Produk- tionsentscheidungen, des Ausma6es, in dem die Preise auf Terminm~rkten private Informa- tion aggregieren, usw.

1. Introduction

A basic characteristic of resource allocation over time is that the agents in an economy (consumers and producers) lack information about future endowments, tastes, and tech- nology. This lack of information, or more briefly uncertainty reflects the limitations of both individual and collective knowledge about the future. In an effort to cope with this uncer- tainty and with the risks that it implies for the agents, the major market economies of the West have over the last two hundred years developed three market institutions on which risk and information can be traded in a systematic and efficient way - - these are the mar- kets for insurance and the organized security and commodity exchanges.

While these market institutions have been in existence for a long time, attempts to develop formal theoretical models that explain how they function are of much more recent origin. The first general theory of resource allocation under uncertainty was developed by Arrow (1964) and Debreu (1959): This is the so-called complete contingent markets model, a can- onical model of great generality to which more specialized models with apparently more restrictive structure can often be reduced by suitable transformation. Thus, Malinvaud (1972) has shown how the Arrow-Debreu model may be used as a model of insurance mar- kets: He shows that if there is no social risk (the aggregate endowment is non-random via the law of large numbers), then in equilibrium each consumer is offered actuarily fair insur- ance and hence by risk aversion seeks complete insurance.

125

Radner (1972) subsequently extended the exchange model of Arrow-Debreu to a model of sequential market equilibrium in which the markets need no longer be complete. This model has been used to interpret security markets and can also be used to analyse com- modity markets as we shall find in the analysis that follows. At a more structured level we should mention the theory of portfolio selection (i. e., the demand for risky assets) develop- ed by Markowitz (1959) and Tobin (1958) which led to the capital asset pricing model of Sharpe (1964) and Lintner (1965) and the linear factor model of asset pricing of Ross (1978). These two models represent the modern theory of the pricing of assets on security exchanges. The basic message of the theory has its origin in Markowitz's emphasis on di- versification of risk and asserts that the risk premium on an asset does not depend on its idiosyncratic risk (as would be predicted by a naive partial equilibrium analysis of the asset) but depends only on its covariance risk with the common underlying factor, normally inter- preted as the overall level of economic activity. It remains to consider the third of the mar- ket institutions mentioned above, namely commodity exchanges. Before examining the economic theory of these markets I shall briefly lay out some of their more firmly estab- lished empirical properties.

2. Empirical properties of futures markets

Good theory helps us to understand data and more importantly helps us to understand the data that are relevant. The theory of futures markets is still at too rudimentary a stage to en- able us to assert with much confidence which are the important empirical data. With this warning here at least are some of the empirical properties that seem to be of importance.

2.1 Open interest (the number of contracts outstanding at any instant) is in large measure determined by hedging needs. In short a primary determinant of activity on a futures market is the amount of the cash commodity that hedgers need to protect from price risk. This has been documented in many ways. In the case of storable commodities this property was first recognized by observing the relation between commercial stocks, short hedging, and open interest (Hoffman, 1941, pp. 33-37). Agents trading on futures markets are said to be long (short) if they are buyers (sellers) of futures contracts. Short (long) hedgers are agents who use the futures market to hedge their future spot market sales (purchases). The relation between long (short) speculation and short (long) hedging was the subject of a careful analysis by Working (1961) - - he discovered a remarkable empirical regularity in the continuous response of long (short) speculation to short (long) hedging: Long (short) speculation equals short (long) hedging plus a small positive term where the magnitude of this positive term depends upon the divergence of price expectations of speculators. This dependence is not trivial since there is a substantial variation in the magnitude of short (long) hedging during the year. Short hedging mirrors the inverted U-shape of commercial stocks during the crop year; there is no such systematic seasonal variation for long hedg-

126

ing. Thus, futures markets cannot be viewed as purely speculative markets - - indeed there is ample evidence that when hedging needs disappear (as a result, say, of technical innova- tion in the production of the good) the futures market disappears.

2.2 On futures markets with a substantial volume of open interest, the futures price does not under normal conditions exhibit significant bias when viewed as a predictor of the sub- sequent spot price. For such markets the Keynesian theory of normal backwardation (the futures price lies below the expected spot price) is not supported by the data. However, markets with a small volume of open interest can develop a systematic bias (Rockwell, 1967, Gray, 1960). In such cases if the hedging is predominantly short (long) and if the downward (upward) bias becomes excessive, the market ceases to be used by the hedgers (price insurance becomes too expensive) and the futures market disappears.

2.3 On futures markets with a substantial volume of open interest, the futures price viewed as a stochastic process has the martingale property - - today's futures price is thus the best predictor of its value at a later time. At any instant the expected price change is thus zero. This property is interpreted as follows: The random character of changes in fu- tures prices reflects the random arrival of new information and the price changes can be viewed as the appropriate market response to changes in information regarding future de- mand and supply prospects.

2.4 There is a systematic seasonal pattern in the volatility of many futures prices. For har- vested commodities the variability is greatest at those times of the year when the most significant information regarding crop yields is revealed (Anderson, 1982).

The properties of futures markets for harvested storable commodities have been thor- oughly documented (Working, 1933, 1948, Brennan, 1958).

2.5 For harvested storable commodities, inter-option spreads (the difference between a later and an earlier maturing contract) depend upon the level of inventory, the spread being positive and approximately equal to carrying costs (storage, interest, insurance) when stocks are at or above their average level. As stocks fall below the average level, the spread becomes progressively more negative. When new information affects futures prices the spread is normally not affected so that the whole family of spot and futures prices fluc- tuate up and down together. Spot prices averaged over crop years with a normal level of in- ventory exhibit a regular seasonal cycle with prices rising from harvest time to the summer and then falling off again at the next harvest. Note that all these descriptive properties of prices can be translated into dual descriptive properties for stocks.

The futures prices of storable goods move up and down together even for contracts in ad- joining crop years. This follows from the presence of carry over from one crop year to the next. For non-storable goods there is no carry over and prices for two adjoining crop years are essentially independently determined. One consequence of this is the following.

t27

2.6 For harvested non-storable commodities the spring price of a futures contract with delivery in the next crop year is stable from one year to another and is approximately equal to the average of past spot prices at maturity ( Tomek - - Gray, 1970). An important conse- quence of this is that producers can more effectively stabilize their income by trading on fu- tures markets when the commodity is non-storable provided there is not excessive fluctua- tion in the producer's output.

3. Classical theory

Theories of futures markets are of recent origin. In 1923, as part of a broader study of com- modity markets Keynes (1923) laid out his risk sharing theory of futures markets - - we shall see in the section that follows that when appropriately interpreted it leads to a most natural theory of futures markets. Much needless confusion has arisen from taking it too literally. Keynes argued that most hedgers are long the underlying cash commodity (a cor- rect stylized fact for many commodity markets) and hence take short positions on the fu- tures market. If speculators have no commitments on other markets, then in order to carry risk for hedgers they must be rewarded with an expected return; this implies that the fu- tures price must lie below the expected spot, a difference which Keynes called normal backwardation. Armed with Markowitz's theory of portfolio selection we note at once that if speculators have commitments on other markets which generate a random income, then diversification may make it attractive to invest on this futures market without any expected return. Failure to recognize this property led to a long controversy among English econ- omists about futures markets.

Out of this controversy emerged the paper of Kaldor (1939), a singularly imaginative piece of work which simultaneously presented a theory of futures markets and an incisive critique of Keynes' "General Theory" based on the impact of speculation more generally on the lev- el of economic activity. Kaldor was concerned with the relation between futures prices and expected spot prices for storable commodities. He derived the basic pricing equations (on this see also Williams, 1936) and introduced the concept of marginal convenience yield (see the end of next section). His ideas were essentially the same as those introduced by Working (1933, 1948) on the basis of extensive empirical investigations.

I shall call these early formulations of Keynes, Kaldor, and Working the classical theory. Loosely speaking, these theories lack three properties which are basic ingredients of what I shall call the modern theory. First, there is no explicit formulation of expectations, nor con- cern with the idea that expectations should somehow be rational - - that the distributions held ex ante by agents should be confirmed in equilibrium. Second, there is no explicit con- sideration of the information structure under which agents make decisions. Third, there is no explicit concept of equilibrium - - a modelling of the mechanism by which individual max- imizing by agents and coordination of their decisions is possible. In an environment of un-

128

certainty this last property also involves rationality in the expectat ions of the agents. Finally and perhaps more importantly, by modern standards these authors do not present a ful ly articulated and well-defined mathematical model of their theory, a model, that is, whose as- sumptions can be made precise and whose qualitative propert ies can be explored to obtain richer and more precise insights into the funct ioning of these markets than is possible on the basis of the largely intuitive and verbal analysis of the classical theory.

4. Modern theory

The modern theory of resource allocation is based on two ideas: Individual maximization and coordinat ion of these individual decisions through a price system. The latter involves the concept of equil ibrium. The basic starting point for such an analysis is the Arrow-De- breu model. To be concrete let us recall the simplest model of pure exchange under uncer- tainty (Debreu, 1959, ch. 7). Consider an economy with a finite number (m) of agents. Sup- pose there are N states of nature, where state s occurs with probabil i ty ~ s > 0 , s =

N 1 . . . . , N, ~. Jrs = 1. The fact that each agent is uncertain what his endowment will be is ex-

s = l

pressed by saying that the endowment of the i th agent is a vector w i = (w~ . . . . . w~) is his endowment if state s occurs. For simplicity let us suppose that there is just where w s

one good so that w~ is a scalar. There are N state cont ingent markets on which a>vector of prices P = (P1 . . . . . PJv) is determined. Each agent has a preference ordering ~" defined on non-negative amounts of consumpt ion in each state (i. e., R+ N) and looks for a bundle x ~ E B i (P) which maximizes his preferences over his budget set

(1) x i >-" i x~ ' '

V x i" ~ B i ( P ) = {x i ' ~ RN+ I P x i ' < pwi},

i - ~ l , . . . , m

where x ; = (x{ . . . . . x~v) and w i = (w~ . . . . . w~). An equi l ibr ium is a pair (x ' . . . . . x " ; P) consist ing of a consumpt ion bundle for each agent and a price system P such that {1)

m m

i i holds and z~ x , = ~ ws, s = 1 . . . . . N (markets clear in each state of nature). We know i=1 i=1 >

that if the preference orderings i , i = 1 . . . . . m, are complete, transitive, cont inuous and monotone on R+ N and have convex preferred sets and if the endowments w i, i = 1 . . . . . m, are str ict ly positive, then an equi l ibr ium exists (Debreu, 1959, p. 83). We also know that such an equil ibrium is Pareto op t ima l (Debreu , 1959, p. 94). This means that there does not exist a feasible allocation

m m

129

such that y i >>, X i, i = 1, m, and yk :~ x k for some k. From a welfare point of view this is the best we can hope for from a system of markets.

Let me show how this framework can by a suitable transformation be used to throw light on the process of risk-sharing that occurs on a futures market. This is a simplification of the analysis in M a g i # - - N e r m u t h (1984B). Consider a collection of k producers each of whom owns a farm which produces a random output y i = (Yl . . . . . Y~v) of a single good. Suppose there is a spot market on which a demand function 9~s determines the spot price ps that

k

producers will receive in the fall, Ps = 9~ ( ~, Y:) . Since production is assumed to be cost- ~ i = 1 r

less each producer's spot market income is a random variable i w ~ = p s y s , s = 1 . . . . , N, i = 1 . . . . . k. There is another group of agents called speculators who have an exogenously

i given income w s, s = 1 . . . . . N, i = k + 1 . . . . . k + r = m. Note that each endowment vec- tor w i now represents an endowment of income across the states of nature so that agents will be exchanging income streams. Each agent's preference ordering is thus defined over such income streams. Producers and speculators can trade on a sequence of T futures markets between the spring and the fall. Information about the state of nature s is revealed gradually over time as follows. Each time period t > 1 one of two signals is revealed st = 1 or st =2. Let ot = (s l . . . . . st) denote the information available to each agent at time t and let us assume that each state of nature s can be identified with some sequence (sl . . . . . ST) SO that N = 2 r _ for brevity we write s = ( s l , . . . , s t ) . A futures contract at time t calls for the delivery of one unit of the commodity at date T. Let z~ (or) denote the number of contracts purchased by the i th agent at t ime t given the information o~. We assume that each agent

closes out his futures posit ion at the beginning of the next period and then takes a new po- sition for that period. If qt (or) denotes the futures price at time t given the information ut, then the profit made by the i th agent depends on his sequential futures trading strategy

" i i z i (z~ . . . . . Z~T_I) where z t = zt (05) and is given by

T - - 1 i 7, z, (o,) (q,+l (or) - - q, (o,+1)).

t=O

We assume that each agent chooses the most preferred trading strategy so that

(2) T--1 T--1

W i Jr ~, 2" I Z1 qt ~ Wi i + ~' Zlt'z~qt' t = 0 t = 0

V Z i ',

i = 1 , . . . , m

where zf q t = q , + l - - q t and where the preference orderings >~ i , i = 1 . . . . . m, satisfy the condit ions given above, so that in particular in view of the convexity of the preferred sets each agent is either risk averse or risk neutral. Let q = (qo . . . . . qT-1 ), then an e q u i l i b r i u m

130

on the sequence o f T futures markets is a pair (z 1 . . . . . zm; q) consisting of a trading strategy for each agent and a system of futures prices q such that (2) holds and each ru-

m i tures market clears ~, z t (or)=0 for all or, t = 0 . . . . . T- -1.

i=1

It can be shown that except in degenerate cases the vector of futures prices q can be chosen in such a way that the set of income bundles that can be achieved by trading on the

T--1

futures markets x i <_ w i + ~, z~ zl qt coincides with the budget set B i (P) in (1). Thus x i in t =0

(1) has associated with it a trading strategy z i which satisfies (2). The market clearing prop- m m

erty ~,, ( x i - - w i) = 0 can be shown to imply that the futures markets clear ~ z i=0 . Since i=1 i=1

(x 1 . . . . . x m) is Pareto optimal, the futures market equilibrium (z~,... , zm; q) is Pareto opti- mal. Thus, trading on a sequence o f futures markets has under the given information struc- ture led to an optimal sharing o f risk between producers and speculators. The importance of trading over time as a vehicle for increasing the spanning properties of a fixed set of se- curities was emphasized by Kreps (1982) and a related result was obtained by Nermuth (1982, ch. 10) and Duffle - - Huang (1983).

The information that becomes available at each point of time t between the spring and the fall is information about the random variables (~s, Y~, i = 1 . . . . . k). Thus, at each point of time the futures price changes in response to the new information about demand and sup- ply. Note that this information is assumed to be available to all of the agents simultaneously so that the problem of asymmetry of information and the associated problems with the revelation of information by price to the uninformed do not arise. Notice also that the effi- ciency of the risk sharing process between producers and speculators depends on the in- formation structure: Only when information is revealed a little bit at a time is the efficiency of the risk sharing process assured. Information and risk sharing are thus closely related.

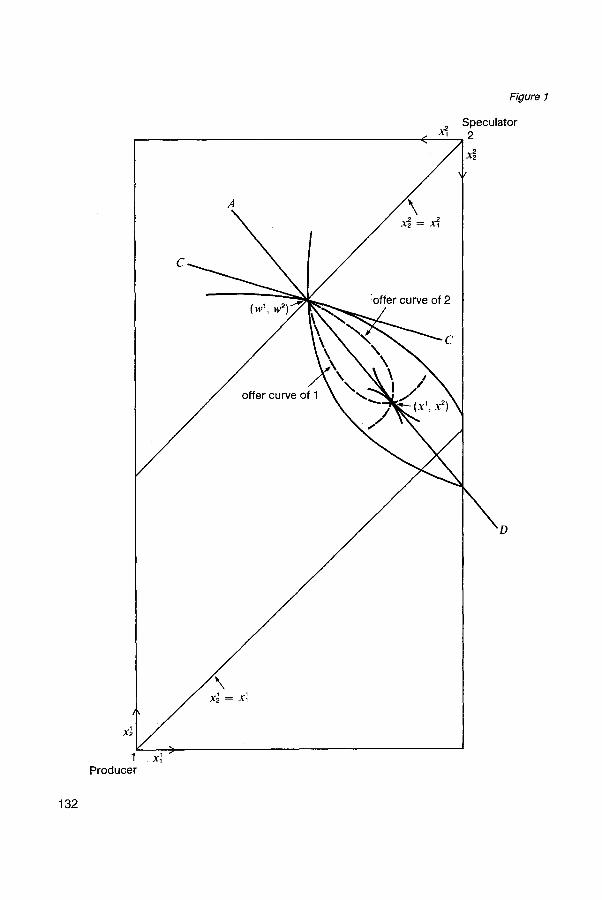

It is instructive to give a simple geometric proof of this result in the case where there is one producer ( k= 1), one speculator ( r= 1), and two states of nature (N=2 ) so that T= 1. The consumption set for each agent is R 2+. Consider the usual Edgeworth box in Figure 1 ; the lengths of the sides represent the aggregate endowments in states 1 and 2 respectively (w~ + w~, w~ + w~). The endowments have been taken to be non-random for the speculator (w~ = w~) but random for the producer (w~ < w~). Let A D be the price line for the Arrow-De-

breu equilibrium (with slope --P-~--~) and let (x', x 2) denote the associated equilibrium in-

come bundles. When the producer trades on the futures market he can attain any income bundle along the line

{x ~ I x ~ = w ~ + z ~ ( p ~ - - q , p 2 - - q ) , z ~ ~ R} .

If we vary q, then this defines a one-parameter family of lines through the producer's initial endowment point w !. Figure 2 shows how the slope of this line varies as we change q (note

131

C

~ = ~

(w 1, :offer curve of 2

offer curve of 1

\

Figure 1

Speculator 2

132

x~[

1 Producer

x~

x~ = x~

p2

F,,~,-- ~ (p,, p2)

z (P' -- q " P2--~q " ) ~ /

F " _ ~ T a [0, p2--P~)

Z ( p l " "

(pl--p2, 0i [ .--~-I ~ F" > Pl

/R- p2

I q

Figure 2

that the futures market cannot have an equil ibrium unless q c (p~, p2) assuming 0<p~ <pa).

Now since the slope of this line is P2- -q if we choose P~ + P2 = 1, q = p l P~ +p2 P2, then pl - -q the slope of the futures market trading line will coincide with the Arrow-Debreu line AD. If

1 1

the producer now chooses the futures trade z 1 x l - - w ~ then he moves from the initial p l q ,

endowment point w 1 to the income bundle x! . If we set z 2= - - z ~, then the futures market clears and the speculator moves from w 2' to x 2. Thus, the futures market equil ibrium (z ~, z2; q) achieves the same allocation as the Arrow-Debreu equil ibrium (x ~, x2; P). It fol- lows from the tangency of the indifference curves at (x ~, x 2) that both allocations are Pareto optimal.

If the preferences of the speculator are taken to be state independent and if w 2 is non-ran- dom (w~= w~), then the slope of the speculator 's indifference curve at w 2 is equal to the

slope ( ~ r ~ ) of the actuarily fair line C C through w 2. Since the speculator is risk averse,

the slope o f the line C C must be greater than the slope of the equil ibrium line A D so that

__ ~___! > __ P_.! = pa--q ~ q < ~ P~ + ~a p2. ,71;'2 P2 p ~ -- q

133

If the speculator enters the market with no risk, then being risk averse he must earn a posi- tive expected return if he is to share risk with the producer. This is precisely Keynes' argu- ment for normal backwardation (Keynes, 1923). Notice that more generally the speculator will enter the market with a random endowment and in such cases the relation between the futures price q and the expected spot price depends on the covariance between w 1 and W 2 ,

In the above model the information structure is decomposed in such a way that each reali- zation of the random variables (~s, Y~, i = 1 . . . . . k) is revealed slowly between the spring and the fall. This is a qualitative aspect of the way uncertainty is resolved. If we now add a precise quantitative description of how these random variables are resolved, then we can deduce some further properties of the equilibrium price process [q, rot)] f__-~. Uncertainty is resolved when the receipt of information reduces the variance of our estimate of the ran- dom variables (~,, Yis, i = 1 . . . . . k). Thus, intuitively in periods when important compo- nents of these variables are revealed we expect to find the greatest variability in futures prices. Thus, if demand is relatively stable and information becomes available in March which enables us to deduce with a fair degree of certainty whether the harvest will be large or small, then the March futures price will be low or high accordingly.

This problem has been studied in an interesting paper of Anderson - - Danthine (1983A). Their model is closely related to the one outlined above, but they do not insist that informa- tion about the random variables (~s, Y~, i = 1 . . . . . k) be revealed in a binary way over time. For simplicity they allow for three time periods (t = 1, 2, 3) which we can think of as spring, summer, and fall. They assume that each producer's output y i is a sum of two independent random variables

E1 ~ ) ~ x~

E, =0,

t = 1 , 2

where ~i is publicly revealed at time t. The harvest covariance structure for the producers is taken for simplicity to be symmetric

v r = 4 ,

ot =I= O,

~or>O.

134

These assumptions express the idea that the farms are all of the same size ( E y i = x ) and are subject to the same general weather pattern (Pt > 0) though there can be variations in individual regions (farms): This is a natural idealized case. There are futures markets in the spring and the summer and a trivial futures market in the fall on which the futures price is equated to the spot price by arbitrage (no basis risk). If at least one speculator is taken to be risk neutral and if producers' preferences are not state dependent, then the futures price at time t will equal the spot price conditional on information available at time t. Thus, if the demand function is taken to be linear

~o(x) = a - - b x + e,

E,(e) = 0 ,

V (e) = d ~ >_ O,

a > O ,

b > 0

then

q~ = a - - b k x ,

k

q 2 = a - - b x ( y , ~ i ~ } , ~ i=1

k

q3 = a - - b % (ff~+ff~) + s = p i=1

so that

V~ (q2) = k f l 2 x 2 o21 (1 + ~o~ ( k - - l ) ) ,

V2 (q3) = k f l 2 x 2 o2, (1 + #2 ( k - - l ) ) + d~.

Thus the volatility of a futures price depends on the amount o f information that is revealed at that date. Suppose that by early summer the weather pattern has in large measure deter- mined what the size of each farmer's crop will be in the fall (02 >> 03) and suppose that the idiosyncratic component influencing each farm's output is not too great (~ot is sufficiently close to 1) so that the correlation between outputs is high (for widely dispersed production this may not be true), then if demand fluctuations are not important (d 2 small) most of the futures price fluctuations will occur in the second period. Alternatively, if information about the harvest becomes available evenly through the crop year (02 = 03) and demand fluctua-

135

tions are important ((~2 large), then most of the futures price fluctuations occur at (or near) the harvest time. Thus, we can expect there to be a fairly well-defined seasonal pattern in the volatility of futures prices for most of the harvested commodities for which there is not substantial demand-side fluctuation and for which there are fairly well-defined times of the year when the nature of weather in large measure determines the subsequent harvest.

The above model of a futures market equilibrium (or more generally of equilibrium on a sys- tem of such markets) was based on two important assumptions: First that production deci- sions are given ex ante and hence by construction are uninfluenced by futures prices, and second that information which becomes available is public information. In practice, futures markets affect production decisions. Broadly speaking, they do so in two ways. First, they serve to reduce the risks associated with producing a given level of output and hence lead to an increase in equilibrium output. This is the official view of the importance of futures markets expressed by the exchanges --,namely that futures markets thr, ough the mecha- nism of hedging and the trading of speculators provide the hedging firms with price insur- ance which enables them to produce more output at less cost to the consumer. Second, producers and speculators in search of greater profit are induced to acquire information about their own output (this applies only t ~ producers), the output of others, and demand. Typically, they do not publicise this information - - quite the contrary, they try to keep it pri- vate. But in using it to make their trading decision,~since their demand affects price (unless they are truly infinitesimal traders) the price may end,up;reflecting their information, itt is ar- gued that the private information acquired in this way is aggregated and incorporated into the futures price - - to the extent that the information is correctly interpreted by the agents and incorporated into the futures price, production and inventory decisions can be made on the basis of improved information. The papers of Grossman (1977), Danthine (1978), and Bray (1981) have sought to characterize this important ~informational role of futures mar- kets.

Two remarks are in order. First, I am uncomfortable with the simultaneity of the process (in the cited papers) by which information affects demand and hence price and price in turn is used as information to revise demand - - in a nutshell, demand functions are only well-de- fined in equilibrium. Also full revelation has been shown in these models only under very special assumptions on preferences (mean-variance) and on the way uncertainty enters. With ~r~espect to the latter Bray~(t981~) ~has made clear that full revelation ~can .only be ~ex- pected if uncertainty lies only on the demand or the supply side, but not both. This, of course, is the standard identification problem familiar in econometrics. Second, it is some- times argued that on ,asset and commodity markets speculators are more concerned with predicting the market by predicting the predictions of others than by acquiring fundamental information regarding demand and supply. This point was made forcefully by Keynes (1936, pp. 154-161) with regard to the Stock Exchange - - he ,was concerned with the associated distortion of prices on which investment decisions are based ("the capital development of a ~country becomes a by-product of the activities of a casino"). This type of behaviour on commodity markets is probably o f much less importance since the contracts themselves

136

expire within a few months and the futures price must coincide with the spot price at the termination of the contract.

Our understanding of the way information, both public and private, enters into market equi- librium is still at a rudimentary stage. In this respect, the papers of Grossman (1977), Dan- thine (1978), and Bray (1981) make an important contribution for they show how under idealized conditions privately acquired information can end up being signalled through the futures market price. The contribution of Danthine is particularly instructive since it shows how production decisions are affected and, as Hirshleifer (1971) has argued, this is what is important about prior information.

I shall now show how the earlier model can be altered so as to give us a framework within which to discuss these production, information, and risk bearing issues. Since we are not considering information acquired between the spring and the fall, but only information acquired in the spring, let us consider a simple two-period partial equilibrium model for a perishable commodity (this means that there is no need to worry about carry overfrom the previous period or into the period that follows). Production decisions are made in the spring and are based on whatever information is available at that time and output appears in the fall. In the spring firms decide (say) how many acres (Yi) to plant: They are uncertain what their output (xi) will be and may even be uncertain what input costs (r) per acre will be. However, output is related to the acres planted by a function xi (s) = f (Yi, s) for each state of nature s e S. Since speculators own no land f -=0 , i = k + 1 , . . . , k + r. Each agent may also earn profits Ri (s), s ~ S, from trading on other markets. If p (s) denotes the spot price in state s e S and if zi denotes the number of futures contracts purchased in the spring, then the total profit earned by each agent is given by

~ (yi, zi ; s) = ? (s) Z (yi, s) - r (s) y i + ~ (p ( s ) - q ) + Ri (s),

s E S ,

i = 1 , . . . , m .

Each agent gathers information regarding demand and supply conditions which result in a signal ai : S--*Ai where Ai is the signal space of the ith agent. Each agent's signal in con- junction with the futures price induces a partition ~ of S so that when the signal-futures price pair takes on the value (~i, ~o) the agent knows the state of nature s E S that is to oc- cur must lie in a subset

I~ (~, .o) = {s c S I ai (s) = ~xi, q (a (s)) = o},

i = 1 . . . . . m

> where Ii ej~ and a = (al . . . . . am). We assume that each preference ordering ~" is repre- sentable by avon Neumann-Morgenstern utility function ui so that each agent's trading de- cision, given that he observes (~i, ,o), is the solution of the problem

137

(3) SUp E [hi i (1~ i (Yi, Zi; S)) I Ii (Odi, 0)]"

(Yi, zi) C R + x R

Let (y, z ) = ( y l . . . . . Ym, zl . . . . . Zm), A = ~] Ai. A fu tures m a r k e t equilibrium is a pair i= 1

( y , z ; p , q ) consisting of quantities ( y , z ) " A ~ R + x R ~ and prices p ' A • +, q �9 A ~ R + such that (yi, zi) solves (3) and spot and futures markets clear

m : / z i , ( , , sJ),

~i=1

s E S ,

m ~, Z i = O.

i = 1

Bray (1981) considers the special case of this model where producers cannot influence output by their input decision so that

(4) f (yi, s) = f (s),

u i (iV) = - - e--Yi w,

#/>0,

fo(x) = - - b x + ~,

b > O

and (a~ . . . . . am, f~ . . . . . fk, C) are joint normally distributed. The futures price q is said to aggregate the information a = ( a ~ . . . . . am) if

E ( p I q) = E ( p l a),

V ( p l q) = V ( p l a).

Bray shows that the futures price aggregates the information a i f and only i f either a is in- k ,k

of s (and hence depends only on ~, f l or a is independent of ~, f (and hence dependent i = 1 ~ i = 1

depends only on e). The first condition asserts that agents receive information only about demand, while the second asserts that agents receive information only about supply.

Danthine (1978) considers the special case of this model where there is only demand-side uncertainty so that f (Yi, S) = f i (Yi) and ui and 9? are as in (4) with /~i = ~ , i = 1 . . . . . k,

138

/~ =y , i = k + 1, . . . , k + r. He assumes that the random term e in the demand function can be decomposed into a sum of two independent normally distributed random variables ~= ~2 + 0 and that the information ai, i = k + 1 . . . . . k + r, of the speculators forms a se- quence of independent drawings on the random variable ~/. He shows first that each producer's output is an increasing function of the futures price, and second if on the basis of the information acquired by the speculators demand is expected to be higher (lower) than normal then the equilibrium futures price is higher (lower) than normal so that in view of the first property production is increased (decreased) relative to its normal level This formalizes the idea that futures prices guide production using information acquired by speculators.

In the models of Bray and Danthine agents earn no profits on other markets, Ri-=0, i = 1 . . . . . m. Magill - - Nermuth (1984A) are interested in studying the way risk bearing by speculators affects the futures price and hence production. Thus they allow speculators to earn profits Ri = R =1=0 (i = k + 1 . . . . . m) on other markets while retaining the assumption that Ri-= 0 for producers. They make the same assumption as Danthine on the production functions, but allow general utility functions and a random decreasing demand function. Let x* denote the equilibrium output when there is no uncertainty in demand. They show that as the number of speculator's becomes very large (r--, oo) the risk premium zl = E (p)--q depends only on the nature of the stochastic dependence between the pair (99, R). The idi- osyncratic risk associated with the variability of 9~ disappears as this risk is spread over a larger and larger pool of speculators. But the stochastic dependence (covariance induced) risk remains and determines the nature of the risk premium. Thus, i f (~, R ) are independ- ent, then z/=O and x = x * . In this case all the risk is pooled away. If (99, R) are positively (negatively) dependent, then zl > 0 (zl < O) and x < x* (x > x*), so that whether output is reduced or increased relative to the deterministic case depends on whether demand on this market covaries positively or negatively with activity on other markets. This covariance term can be viewed as a measure of the perceived risk of this market.

In all of the above models the commodity under consideration was assumed to be perish- able: This meant that stocks of the commodity could not be carried from one year to the next as carry over. When the commodity under consideration is storable, then the equilib- rium problem becomes much more complicated: This is because we now need to find a joint equilibrium not only within each crop year but also across a whole sequence of adjoin- ing crop years. A futures market equilibrium for a random sequence of harvests with ran- dom intra-crop-year demand and with explicit trading in futures contracts for adjoining years by producers and speculators has not to my knowledge been formally analysed - - the problem is likely to be quite complex. Instead a simpler first approximation has been studied (see Samuelson, 1957). The object is to explain the observed price relations out- lined in 2.5 above. The basic idea for this theory emerged from the investigations of Work- ing (1933, 1948) and from a paper of Kaldor(1939) on speculation. Production requires not just fixed stocks such as capital equipment, but also circulating stocks. Just as fixed capi- tal has a marginal product, so circulating capital has a marginal product. This marginal prod-

139

uct of the circulating capital, or the marginal convenience yield as it is normally referred to, has the property that it rises fast when stocks of producers are depleted below a certain level and conversely falls rapidly to zero when stocks lie at or above this level. The need to keep circulating stocks arises for a variety of reasons which we shall not attempt to explain here. In the analysis that follows we summarize the various costs (benefits) associated with holding the level of inventory x in a single function (P (x) which we call the stock-out cost function.

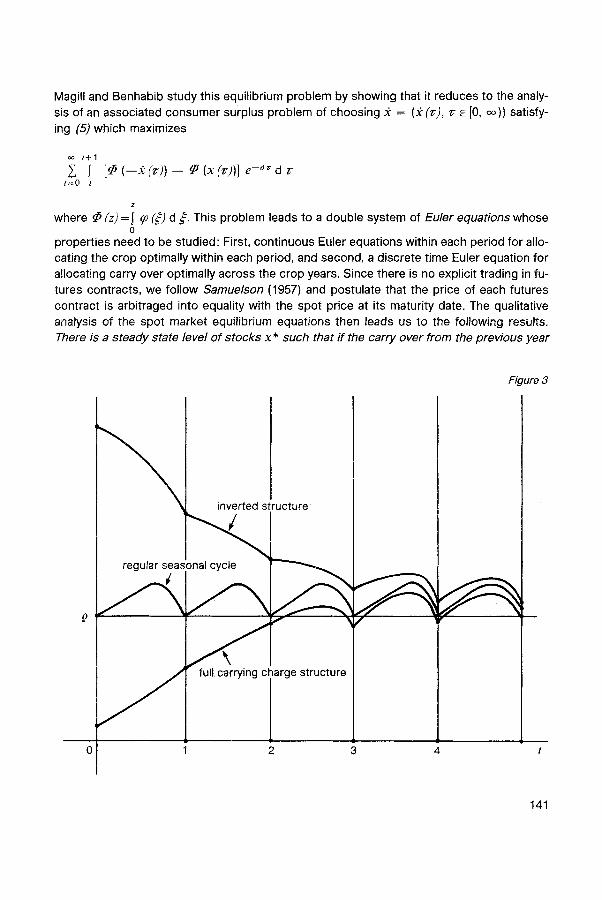

Magill - - Benhabib (1983) study the problem of finding an equilibrium using this idea. They assume that there is a known infinite sequence of future harvests {ht}~=0 and that demand by consumers for flow amounts of the commodity at each instant is unchanged over all fu- ture time. A single representative firm is involved in three simultaneous activities, the pro- duction of the commodity, the holding of working stocks, and the selling of inventory - - ac- tivities which in the case of a commodity like wheat would normally be undertaken by separate producers, namely farmers, millers, and elevator operators. The firm seeks to allo- cate its production, storage, and sales activities over time so as to maximize its discounted profits. If we let x (t § denote the initial inventory at the beginning of the crop year It, t + 1] and x ( t-) denote the carry over of stocks from the crop year I t - - l , t], then, assuming al- ways x (r ) >_ O,

(5) x (t +) = x ( t - ) + h,,

t = 0 , 1 . . . . .

x(r) = x( t +) +i20,)d~,, t

r E ( t , t + l ) .

If q (z-) denotes the price at date zero for one unit of the commodity deliverable at time E [0, oo) and if d > 0 is the constant instantaneous interest rate, then p (z-)= e ~ q (~) de-

notes the spot price at time ~- for the same good. Given a path of prices q = (q (~), ~" E [13, co)) the firm chooses its sale of inventory - -2 = - - (2 (~-), ~" E [0, co)) over all paths satisfying (5) so as to maximize its profit

oo t + l

~(2) = Z I t = 0 t

[q (~-) ( - - 2 (r)) - - f (x (~-))] e - ~ ~ d ~.

A spot market equilibrium (q, x) is a pair satisfying ~r (2) >_ sr (2') for all 2' satisfying (5), and p (~-) = 9~ ( - -2 (~')), ~r e [0, co), so that firms maximize profit and spot markets clear, 99 (.) being the inverse demand function of consumers. This is simply an Arrow-Debreu equilib- rium for this model.

140

Magill and Benhabib study this equilibrium problem by showing that it reduces to the analy- sis of an associated consumer surplus problem of choosing 2 = (2 (~), ~- ~ [0, oo)) satisfy- ing (5)which maximizes

oo t + l

2 I t ~ O t

[~ (---~ (r')) -- ~P (x (v))] e -~ ~ d r

2

where ~ (z) = I 99 (~') d ~'. This problem leads to a double system of Euler equations whose 0

properties need to be studied: First, continuous Euler equations within each period for allo- cating the crop optimally within each period, and second, a discrete time Euter equation for allocating carry over optimally across the crop years. Since there is no explicit trading in fu- tures contracts, we follow Samuelson (1957) and postulate that the price of each futures contract is arbitraged into equality with the spot price at its maturity date. The qualitative analysis of the spot market equilibrium equations then leads us to the following results. There is a steady state level of stocks x* such that if the carry over from the previous year

Figure 3

0

inverted structure

regular seasonal cycle

~ full, carrying c arge structure

2

----->,_

f f

3 4 t

141

is at the steady state level (x (0-) = x*), then the spot prices and inventory exhibit a regular seasonal cycle as described in 2.5 above, ff the carry over x (0-) lies sufficiently below x * then futures prices have an inverted structure (decrease as maturity date increases). Con- versely, i f x (0-) lies sufficiently above x* then futures prices have a carrying charge struc- ture (increase at the rate of interest as the maturity date increases). These three cases are exhibited in Figure 3. Futures markets are thus a mechanism for projecting future spot prices into the present. When there is a deficiency (surplus) of carry over the inverted (car- rying charge) market discourages (encourages) consumption by a high (low) spot price, while simultaneously discouraging (encouraging) inventory holding by revealing through the structure of the prices on the futures market a falling (rising) course of spot prices. Thus, by projecting the future into the present the futures market serves to guide the con- sumption and inventory accumulation behaviour of consumers and producers in the econ- omy.

5. References

Anderson, R. W., "The Determinants of the Volatility of Futures Prices', Center for the Study of Futures Markets, Columbia University, Working Paper, 1982, (33).

Anderson, R.W., Danthine, J.-P. (1983A), "The Time Pattern of Hedging and the Volatility of Futures Prices", Review of Economic Studies, 1983, 50(2), pp. 249-266.

Anderson, R. W., Danthine, J.-P. (1983B), "Hedger Diversity in Futures Markets", The Economic Jour- nal, 1983, 93, pp. 370-389.

Arrow, K. J., "Role of Securities in the Optimal Allocation of Risk-Bearing", Review of Economic Stud- ies, 1964, 31(2), pp. 91-96.

Bray, M., "Futures Trading, Rational Expectations, and the Efficient Markets Hypothesis ~, Econome- trice, 1981, 49(3), pp. 575-596.

Brennan, M. J., 'The Supply of Storage", American Economic Review, 1958, 48(1), pp. 50-72.

Danthine, J.-P., "Information, Futures Prices, and Stabilizing Speculation", Journal of Economic Theory, 1978, 17(1), pp. 79-98.

Debreu, G., Theory of Value, John Wiley & Sons, New York, 1959.

Duffie, D., Huang, C., "Implementing Arrow-Debreu Equilibria by Continuous Trading of Few Long- Lived Securities", Stanford University, Working Paper, 1983.

142

Gray, R. W., "The Characteristic Bias in Some Thin Futures Markets", Food Research Institute Studies, 1960, 1, pp. 296-312.

Grossman, S. J., "On the Efficiency of Competitive Stock Markets Where Traders Have Diverse Infor- mation", Journal of Finance, 1976, 31(2), pp. 573-585.

Grossman, S. J., "The Existence of Futures Markets, Noisy Rational Expectations and Informational Ex- ternalities", Review of Economic Studies, 1977, 44(3), pp. 431-449.

Grossman, S. J., Stiglitz, J. E., "On the Impossibility of Informationally Efficient Markets", American Economic Review, 1980, 70(3), pp. 393-408.

Guesnerie, R., Jaffray, J.-Y., "Optimality of Equilibrium of Plans, Prices and Price Expectations", in Dreze, J. H. (Ed.), Allocation under Uncertainty: Equilibrium and Optimality, John Wiley & Sons, New York, 1974, pp. 71-86.

i

Hirshleifer, J., "The Private and Social Value of Information and the Reward to Inventive Activity", Amer- ican Economic Review, 1971, 61 (4), pp. 561-574.

Hoffman, G.W., "Grain Prices and the Futures Market. A 15-Year Survey, 1923-1938", United States Department of Agriculture, Technical Bulletin No. 747, Washington, DC, 1941.

Kaldor, N., "Speculation and Economic Stability", Review of Economic Studies, 1939, 7(1), pp. 1-27.

}<eynes, J. M, "Some Aspects of Commodity Markets", Manchester Guardian Commercial, European Reconstruction Series, Section 13, 1923, March 29, pp. 784-786.

Keynes, J. M., The General Theory of Employment, Interest and Money, Macmillan Press Ltd., London, 1936.

Kreps, D., "Multiperiod Securities and the Efficient Allocation of Risk: A Comment on the Black- Scholes Option Pricing Model", in McCall, J. (Ed.), The Economics of Uncertainty and Information, Uni- versity of Chicago Press, Chicago, 1982.

Lintner, J., "The Valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets", Review of Economics and Statistics, 1965, 47(1), pp. 13-37_

Magill, M. J. P., Benhabib, J., "Price Relations on Futures Markets for Storable Commodities", Journal of Mathematical Analysis and Applications, 1983, 91, pp. 567-591.

Magill, M. J. P., Nermuth, M. (1984A), "Futures Markets: Speculation and Production", University of Southern California, MRG Working Paper, 1984.

Magill, M. J. P., Nermuth, M. (1984B), "On the Efficiency of Futures Markets", University of Southern California, Working Paper, 1984.

143

Malinvaud, E., "The Allocation of Individual Risks in Large Markets ~, Journal of Economic Theory, 1972, 4(2), pp. 312-328.

Markowitz, H., Portfolio Selection: Efficient Diversification of Investments, John Wiley & Sons, New York, 1959.

Nermuth, M., Information Structures in Economics, Springer, Wien-New York, 1982.

Radner, R., "Existence of Equilibrium Plans, Prices, and Price Expectations in a Sequence of Markets", Econometrica, 1972, 40(2), pp. 289-303.

Radner, R., "Rational Expectations Equilibrium: Generic Existence and the Information Revealed by Price", Econometdca, 1979, 47(3), pp. 655-678.

Rockwell, C.S., "Normal Backwardation, Forecasting, and the Returns to Commodity Futures Trad- ers", Food Research Institute Studies, 1967, 7, SuppL, pp. 107-130.

Ross, S. A., "The Current Status of the Capital Asset Pricing Model (CAPM)", Journal of Finance, 1978, 33(3), pp. 885-901.

Samuelson, P. A., "lntertemporal Price Equilibrium: A Prologue to the Theory of Speculation", Weltwirt- schafttiches Archiv, 1957, 79(2), pp. 181-219.

Samuelson, P. A., "Proof that Properly Anticipated Prices Fluctuate Randomly", Industrial Management Review, 1965, 6, pp. 41-49.

Samuelson, P. A., "Stochastic Speculative Price', Proceedings of the National Academy of Sciences, 1971, 68, pp. 335-337.

Sharpe, W., "Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk", Journal of Finance, 1964, 19(3), pp. 425-442.

Tobin, J., "Liquidity Preference as Behavior towards Risk", Review of Economic Studies, 1958, 25(2), pp. 65-85.

Tomek, W. G., Gray, R. W., "Temporal Relationships Among Prices on Commodity Markets: Their AIIo- cative and Stabilizing Roles", American Journal of Agricultural Economics, 1970, 52(3), pp. 372-380.

Williams, J.B., "Speculation and the Carryover", Quarterly Journal of Economics, 1936, 50(3), pp. 436-455.

Working, H., "Price Relations Between July and September Wheat Futures at Chicago Since 1885", Wheat Studies of the Food Research Institute, 1933, 9, pp. 187-238.

Working, H., "Theory of Inverse Carrying Charge in Futures Markets', Journal of Farm Economics, 1948, 30, pp. 1-28.

144

Working, H., "Speculation on Hedging Markets", Food Research Institute Studies, 1961, 2, pp. 185-220.

Correspondence:

Michael J. P. Magill

Department of Economics University of Southern California

University Park Los Angeles, CA 90089-0152

USA

145