Wachstumsmarkt Healthcare Industrie - Gewinner und Verlierer

21

Copyright © 2016 QuintilesIMS. All rights reserved. Wachstumsmarkt Healthcare Industrie Gewinner und Verlierer Dr. Frank Wartenberg President Central Europe QuintilesIMS

-

Upload

quintilesims-germany -

Category

Healthcare

-

view

146 -

download

0

Transcript of Wachstumsmarkt Healthcare Industrie - Gewinner und Verlierer

Copyright © 2016 QuintilesIMS. All rights reserved.

Wachstumsmarkt Healthcare Industrie

Gewinner und Verlierer

Dr. Frank Wartenberg

President Central Europe

QuintilesIMS

1

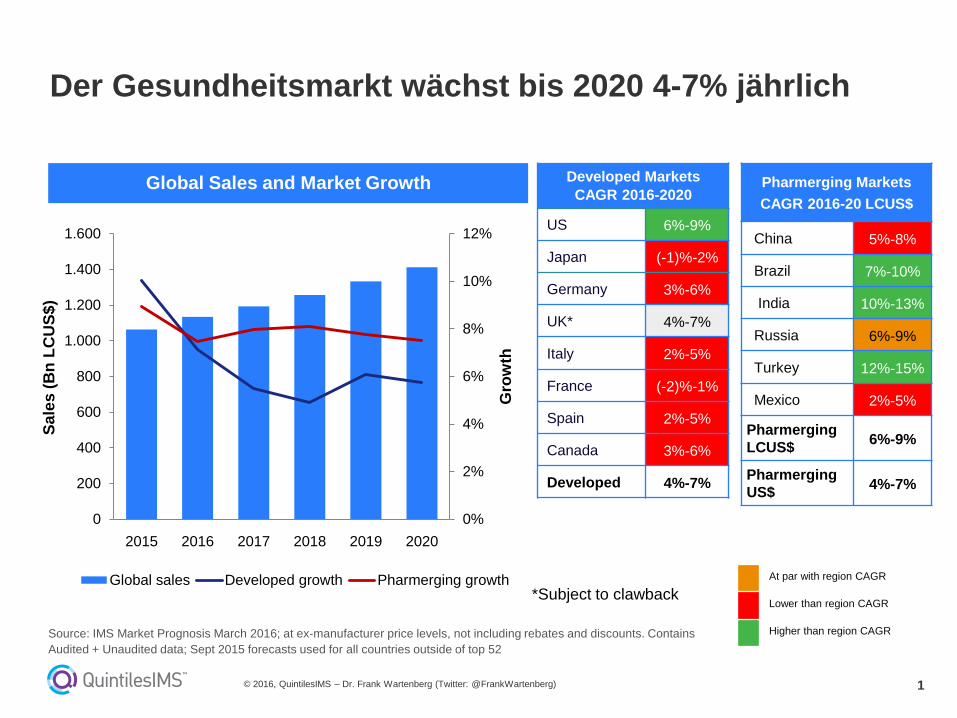

Source: IMS Market Prognosis March 2016; at ex-manufacturer price levels, not including rebates and discounts. Contains

Audited + Unaudited data; Sept 2015 forecasts used for all countries outside of top 52

Der Gesundheitsmarkt wächst bis 2020 4-7% jährlich

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Developed Markets

CAGR 2016-2020

US 6%-9%

Japan (-1)%-2%

Germany 3%-6%

UK* 4%-7%

Italy 2%-5%

France (-2)%-1%

Spain 2%-5%

Canada 3%-6%

Developed 4%-7%

Pharmerging Markets

CAGR 2016-20 LCUS$

China 5%-8%

Brazil 7%-10%

India 10%-13%

Russia 6%-9%

Turkey 12%-15%

Mexico 2%-5%

Pharmerging

LCUS$6%-9%

Pharmerging

US$4%-7%

Global Sales and Market Growth

At par with region CAGR

Lower than region CAGR

Higher than region CAGR

*Subject to clawback

0%

2%

4%

6%

8%

10%

12%

0

200

400

600

800

1.000

1.200

1.400

1.600

2015 2016 2017 2018 2019 2020

Gro

wth

Sa

les

(B

n L

CU

S$

)

Global sales Developed growth Pharmerging growth

2

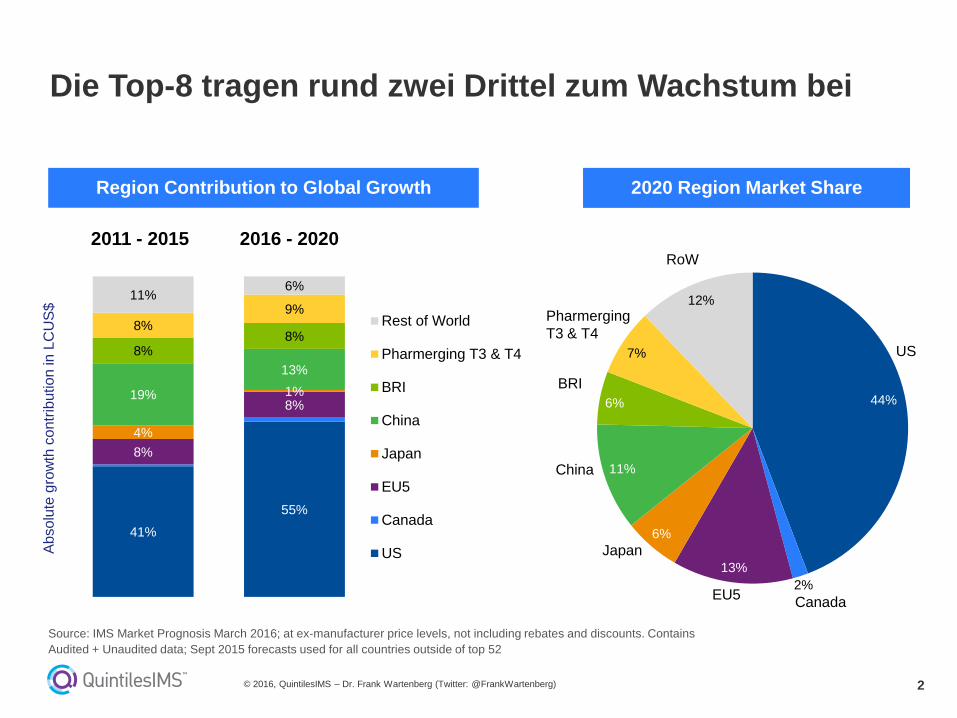

Die Top-8 tragen rund zwei Drittel zum Wachstum bei

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

41%

55%

8%

8%

4%

1%19%

13%

8%8%

8%

9%11%

6%

Rest of World

Pharmerging T3 & T4

BRI

China

Japan

EU5

Canada

US

44%

2%

13%

6%

11%

6%

7%

12%

Region Contribution to Global Growth 2020 Region Market Share

2011 - 2015 2016 - 2020

BRI

Pharmerging

T3 & T4

China

Japan

EU5Canada

US

RoW

Ab

solu

te g

row

th c

ontr

ibutio

n in

LC

US

$

Source: IMS Market Prognosis March 2016; at ex-manufacturer price levels, not including rebates and discounts. Contains

Audited + Unaudited data; Sept 2015 forecasts used for all countries outside of top 52

3

Deutschland wächst im Vergleich zu anderen

europäischen Ländern stark

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Top 25 Europe

Growth dynamic

EU RestEU5

2011-2015 Europe

CAGR 2.8%

2016-2020

Europe CAGR 2-

5%

Source: IMS Health Market Prognosis, May 2016, at ex-manufacturer price levels, excluding rebates and discounts.

Contains Audited + Unaudited data. Bubble Size indicates 2014 US$ Sales; Europe excludes Russia

1

0

-1

3

10

6

14

5

2

3210-1 98765-2-5-6

4

4

Sweden

Netherlands

Belgium

Switzerland

Poland

Finland

Denmark

RomaniaPortugal

Greece

Historical Growth % (CAGR 2011-15)

Turkey

Spain

Italy

England

Hungary

France

Germany

Austria

Pro

gn

os

ed

Gro

wth

% (

CA

GR

20

16

-20

)

Slovenia

Croatia

Bulgaria

Slovakia

Norway

IrelandCzech Republic

4

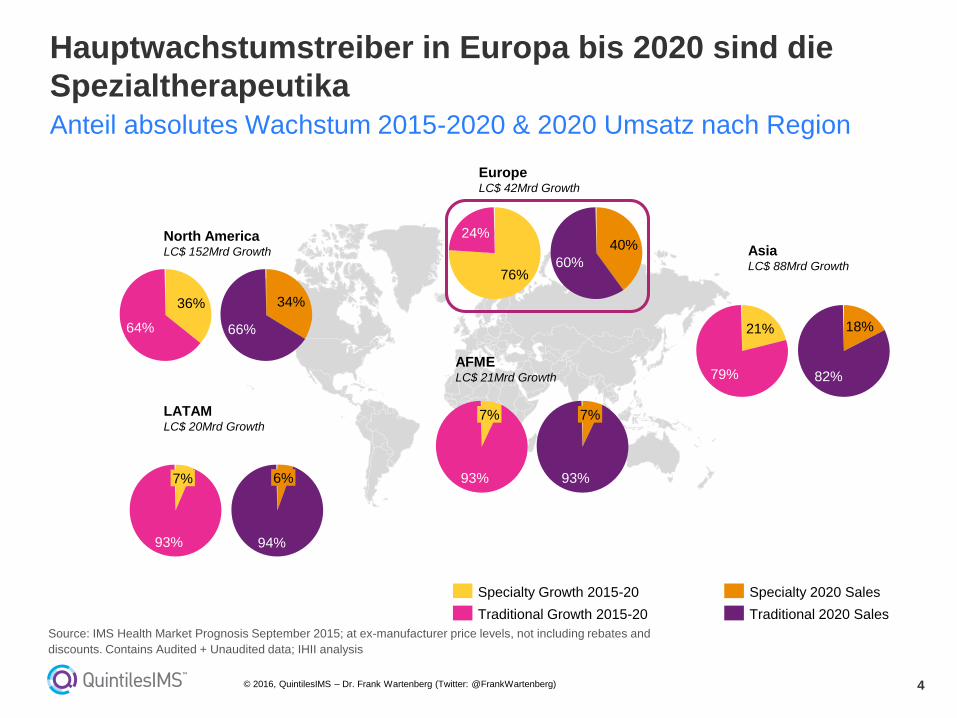

Hauptwachstumstreiber in Europa bis 2020 sind die

SpezialtherapeutikaAnteil absolutes Wachstum 2015-2020 & 2020 Umsatz nach Region

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

93%

7%

Traditional 2020 Sales

Specialty 2020 Sales

93%

7%

Traditional Growth 2015-20

Specialty Growth 2015-20

66%

34%

64%

36%

94%

6%

93%

7%

60%

40%24%

76%

82%

18%

79%

21%

LATAMLC$ 20Mrd Growth

North AmericaLC$ 152Mrd Growth

EuropeLC$ 42Mrd Growth

AFMELC$ 21Mrd Growth

AsiaLC$ 88Mrd Growth

Source: IMS Health Market Prognosis September 2015; at ex-manufacturer price levels, not including rebates and

discounts. Contains Audited + Unaudited data; IHII analysis

5

Onkologie und Autoimmun-Krankheiten werden die

führenden Therapiegebiete gemessen am Umsatz

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Oncology

Autoimmune

Viral Hepatitis

Immunosuppressants

HIV Antivirals

Immunostimulants

Interferons

Erythropoietins

Macular Degeneration

*Sales in

2020

CAGR

2016-2020

9-12%

11-14%

7-10%

11-14%

1-4%

2-5%

1-4%

0-3%

6-9%

$100-120Bn

$55-65Bn

$45-55Bn

$20-30Bn

$20-30Bn

$15-18Bn

$7-9Bn

$7-9Bn

$6-8Bn

*Sales represented in constant US dollars.

Leading Specialty Therapy Areas

Source: IMS Health, IMS Therapy Prognosis, September 2015; IMS Institute for Healthcare Informatics, October 2015

Note: Leading traditional therapy areas shown for 8 developed countries and 6 pharmerging countries.

6

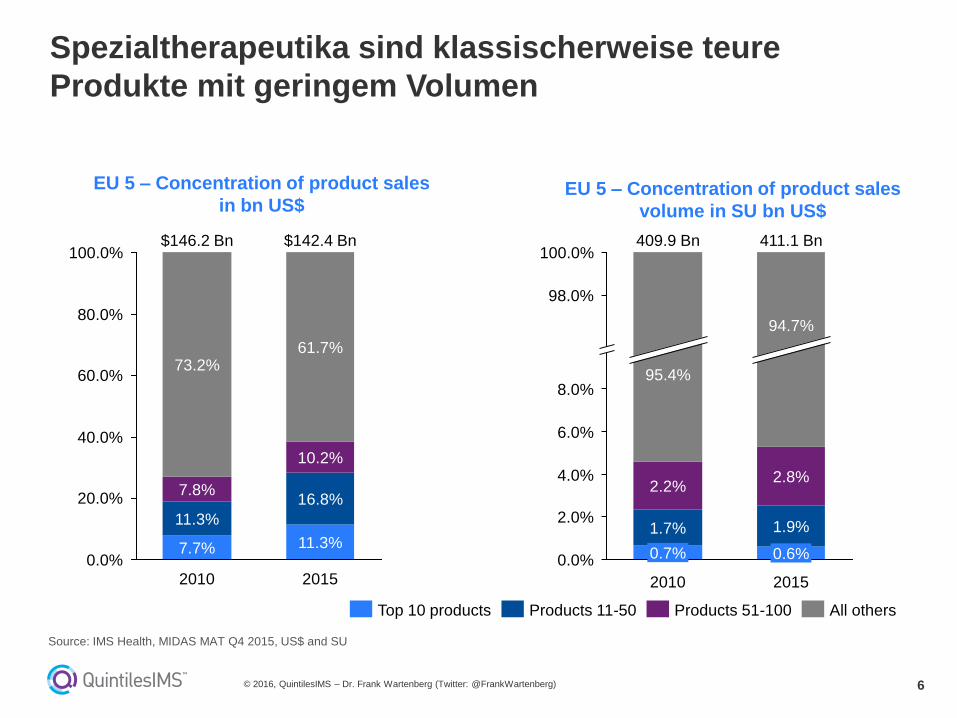

Spezialtherapeutika sind klassischerweise teure

Produkte mit geringem Volumen

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

100.0%

80.0%

60.0%

40.0%

20.0%

0.0%

2015

$142.4 Bn

61.7%

10.2%

16.8%

11.3%

2010

$146.2 Bn

73.2%

7.8%

11.3%

7.7%

EU 5 – Concentration of product sales

volume in SU bn US$

All othersProducts 51-100Products 11-50Top 10 products

4.0%

2.0%

0.0%

100.0%

8.0%

98.0%

6.0%

2015

411.1 Bn

94.7%

2.8%

1.9%1.7%

2.2%

95.4%

409.9 Bn

2010

0.6%0.7%

EU 5 – Concentration of product sales

in bn US$

Source: IMS Health, MIDAS MAT Q4 2015, US$ and SU

7

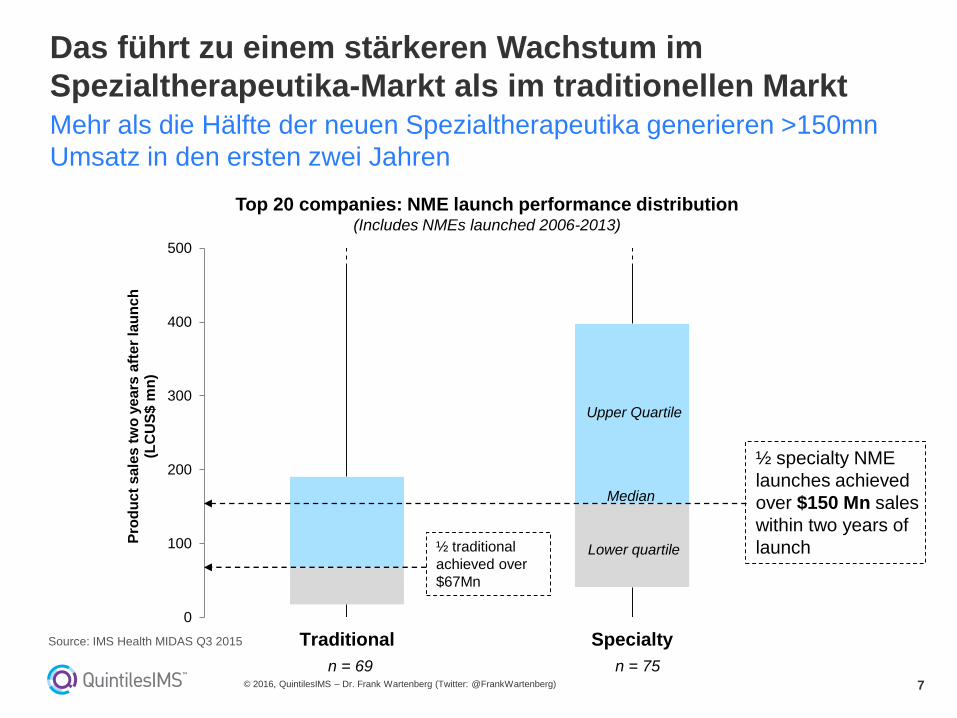

Das führt zu einem stärkeren Wachstum im

Spezialtherapeutika-Markt als im traditionellen MarktMehr als die Hälfte der neuen Spezialtherapeutika generieren >150mn

Umsatz in den ersten zwei Jahren

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

0

100

200

300

400

500

Traditional Specialty

Pro

du

ct

sale

s t

wo

ye

ars

aft

er

lau

nch

(LC

US

$ m

n)

Top 20 companies: NME launch performance distribution(Includes NMEs launched 2006-2013)

n = 69 n = 75

½ specialty NME

launches achieved

over $150 Mn sales

within two years of

launch½ traditional

achieved over

$67Mn

Median

Lower quartile

Upper Quartile

Source: IMS Health MIDAS Q3 2015

8

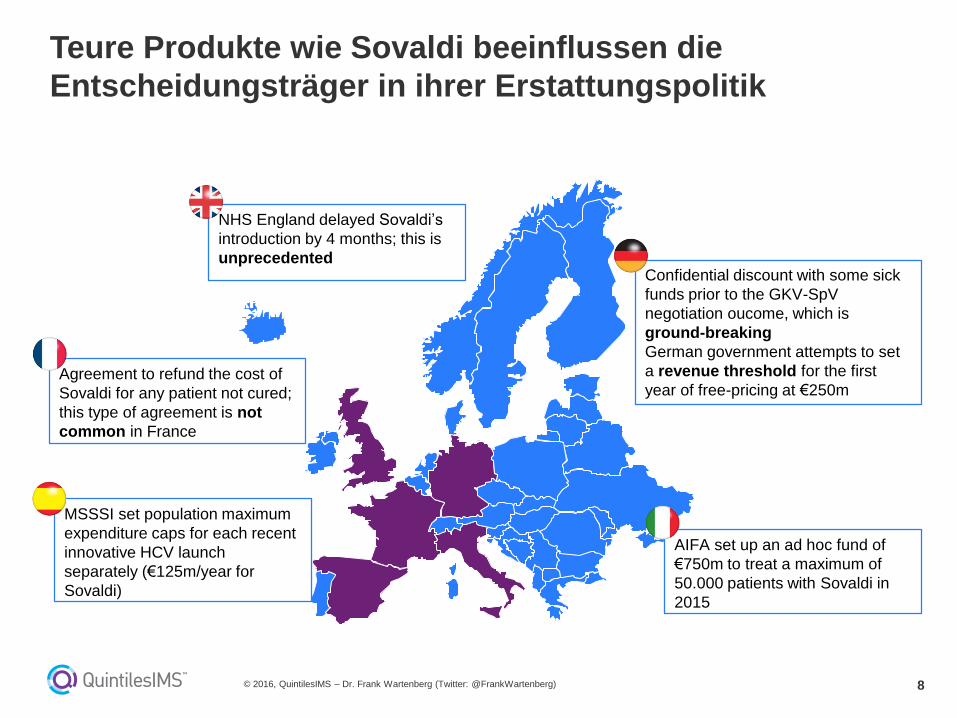

Teure Produkte wie Sovaldi beeinflussen die

Entscheidungsträger in ihrer Erstattungspolitik

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Confidential discount with some sick

funds prior to the GKV-SpV

negotiation oucome, which is

ground-breaking

German government attempts to set

a revenue threshold for the first

year of free-pricing at €250m

NHS England delayed Sovaldi’s

introduction by 4 months; this is

unprecedented

Agreement to refund the cost of

Sovaldi for any patient not cured;

this type of agreement is not

common in France

MSSSI set population maximum

expenditure caps for each recent

innovative HCV launch

separately (€125m/year for

Sovaldi)

AIFA set up an ad hoc fund of

€750m to treat a maximum of

50.000 patients with Sovaldi in

2015

9

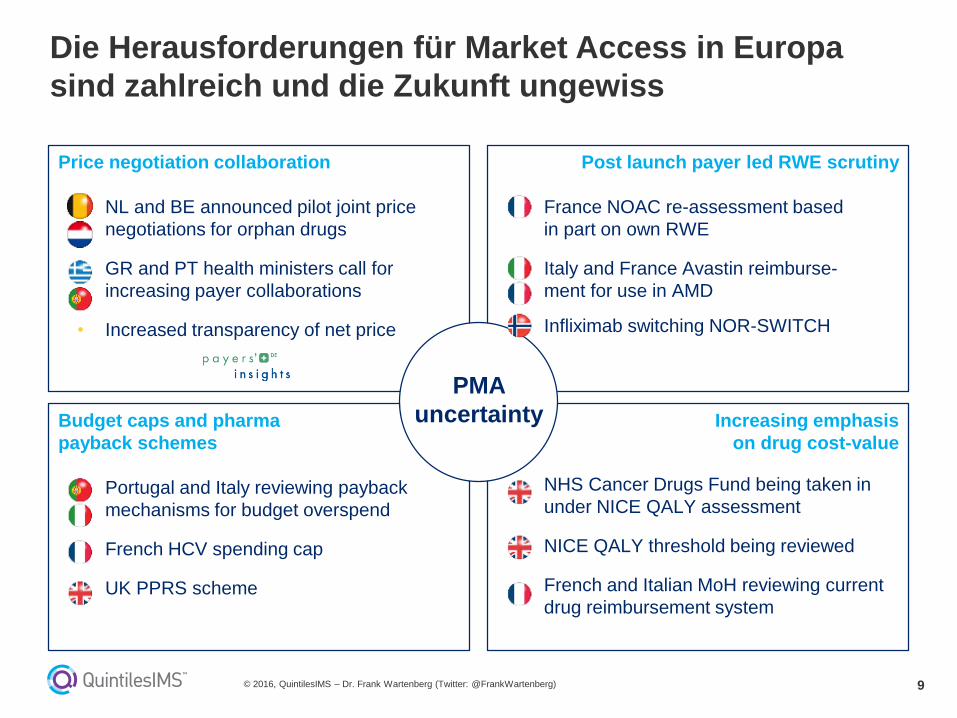

Die Herausforderungen für Market Access in Europa

sind zahlreich und die Zukunft ungewiss

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Price negotiation collaboration

• NL and BE announced pilot joint price

negotiations for orphan drugs

• GR and PT health ministers call for

increasing payer collaborations

• Increased transparency of net price

Post launch payer led RWE scrutiny

• France NOAC re-assessment based

in part on own RWE

• Italy and France Avastin reimburse-

ment for use in AMD

• Infliximab switching NOR-SWITCH

Budget caps and pharma

payback schemes

• Portugal and Italy reviewing payback

mechanisms for budget overspend

• French HCV spending cap

• UK PPRS scheme

Increasing emphasis

on drug cost-value

• NHS Cancer Drugs Fund being taken in

under NICE QALY assessment

• NICE QALY threshold being reviewed

• French and Italian MoH reviewing current

drug reimbursement system

PMA

uncertainty

10

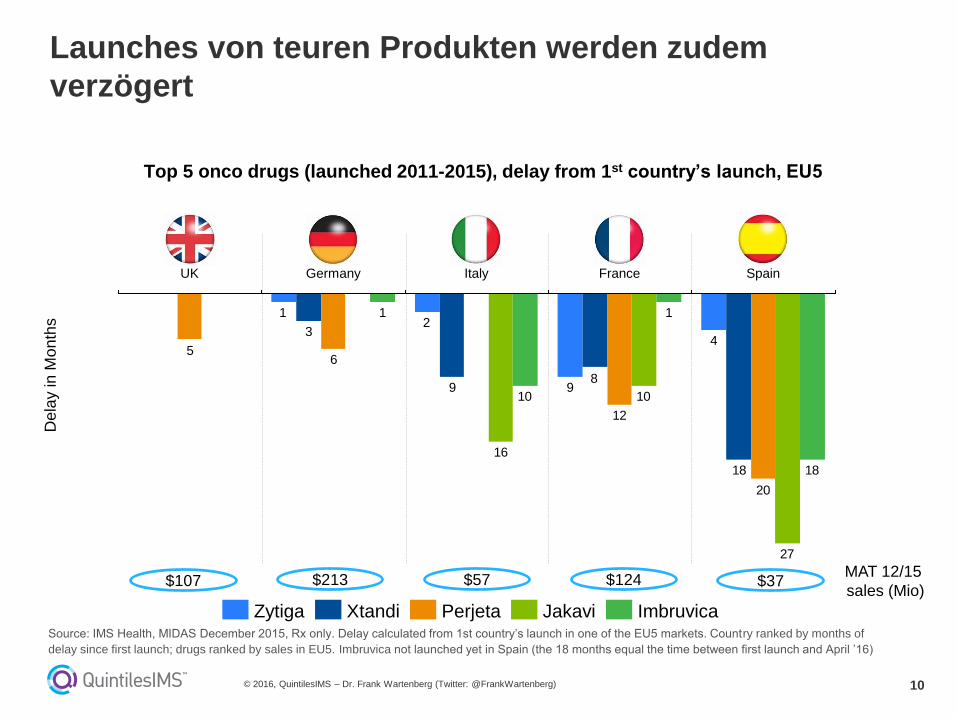

Launches von teuren Produkten werden zudem

verzögert

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Dela

y in

Mo

nth

s

Top 5 onco drugs (launched 2011-2015), delay from 1st country’s launch, EU5

$107 $213 $57 $124 $37

4

9

21

18

89

3

20

12

65

27

10

16

18

1

10

1

SpainFranceItalyGermanyUK

JakaviPerjeta ImbruvicaXtandiZytiga

MAT 12/15

sales (Mio)

Source: IMS Health, MIDAS December 2015, Rx only. Delay calculated from 1st country’s launch in one of the EU5 markets. Country ranked by months of

delay since first launch; drugs ranked by sales in EU5. Imbruvica not launched yet in Spain (the 18 months equal the time between first launch and April ’16)

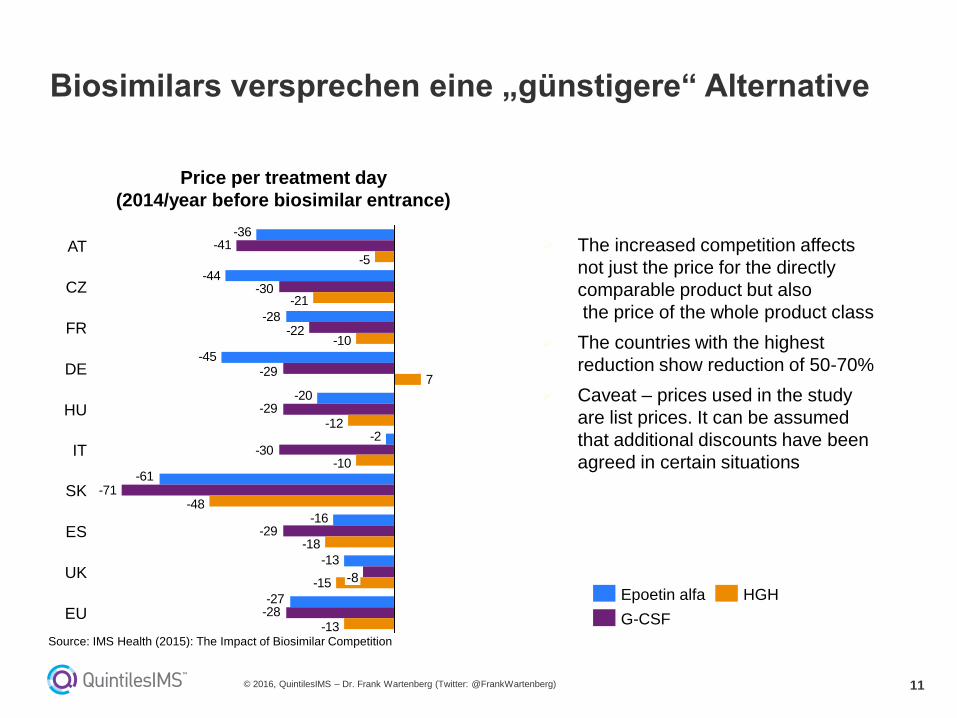

11

The increased competition affects

not just the price for the directly

comparable product but also

the price of the whole product class

The countries with the highest

reduction show reduction of 50-70%

Caveat – prices used in the study

are list prices. It can be assumed

that additional discounts have been

agreed in certain situations

Biosimilars versprechen eine „günstigere“ Alternative

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Price per treatment day

(2014/year before biosimilar entrance)

-27

-13

-16

-61

-2

-20

-45

-28

-44

-36

-28

-29

-71

-30

-29

-29

-22

-30

-41

-13

-15

-18

-48

-10

-12

7

-10

-21

-5

UK -8

ES

SK

IT

HU

DE

EU

FR

CZ

AT

Epoetin alfa HGH

G-CSF

Source: IMS Health (2015): The Impact of Biosimilar Competition

12

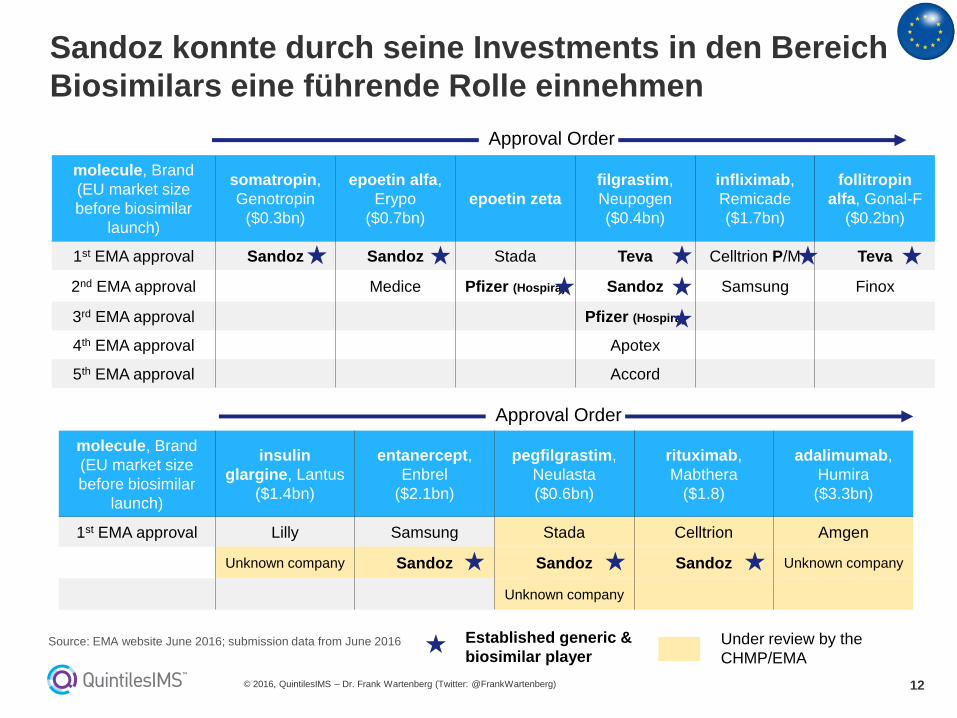

Sandoz konnte durch seine Investments in den Bereich

Biosimilars eine führende Rolle einnehmen

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

molecule, Brand

(EU market size

before biosimilar

launch)

somatropin,

Genotropin

($0.3bn)

epoetin alfa,

Erypo

($0.7bn)

epoetin zeta

filgrastim,

Neupogen

($0.4bn)

infliximab,

Remicade

($1.7bn)

follitropin

alfa, Gonal-F

($0.2bn)

1st EMA approval Sandoz Sandoz Stada Teva Celltrion P/M Teva

2nd EMA approval Medice Pfizer (Hospira) Sandoz Samsung Finox

3rd EMA approval Pfizer (Hospira)

4th EMA approval Apotex

5th EMA approval Accord

molecule, Brand

(EU market size

before biosimilar

launch)

insulin

glargine, Lantus

($1.4bn)

entanercept,

Enbrel

($2.1bn)

pegfilgrastim,

Neulasta

($0.6bn)

rituximab,

Mabthera

($1.8)

adalimumab,

Humira

($3.3bn)

1st EMA approval Lilly Samsung Stada Celltrion Amgen

Unknown company Sandoz Sandoz Sandoz Unknown company

Unknown company

Approval Order

Approval Order

Under review by the

CHMP/EMA

Established generic &

biosimilar playerSource: EMA website June 2016; submission data from June 2016

13

In den kommenden Jahren werden Biosimilars primär

für onkologische und autoimmun Krankheiten erwartet

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

12

23

1

23

32

0

5

10

15

20

25

30

35

No. o

f b

iosim

ilars

in d

eve

lop

men

t

Ph

ase

III

Pre

-Reg/R

eg

Ph

ase

II

Ph

ase

I

Pre

clin

ica

l

Biosimilar pipeline by phase 2015

Pre-clinical to registration

5

2

2

3

3

3

3

7

10

25

28

0 5 10 15 20 25 30

Erythropoietins

Antidiabetics

Sex Hormones

Dermatologics

Number of biosimilars in development *

Multiple Sclerosis

Others

Growth Hormones

Oncologics

HGFs

Immunosuppr.

Autoimmune

Biosimilar pipeline by therapy area 2015

Pre-clinical to registration

35 biosimilars in late

stage development

Source: IMS Health R&D focus Dec 2015; Not exhaustive

14

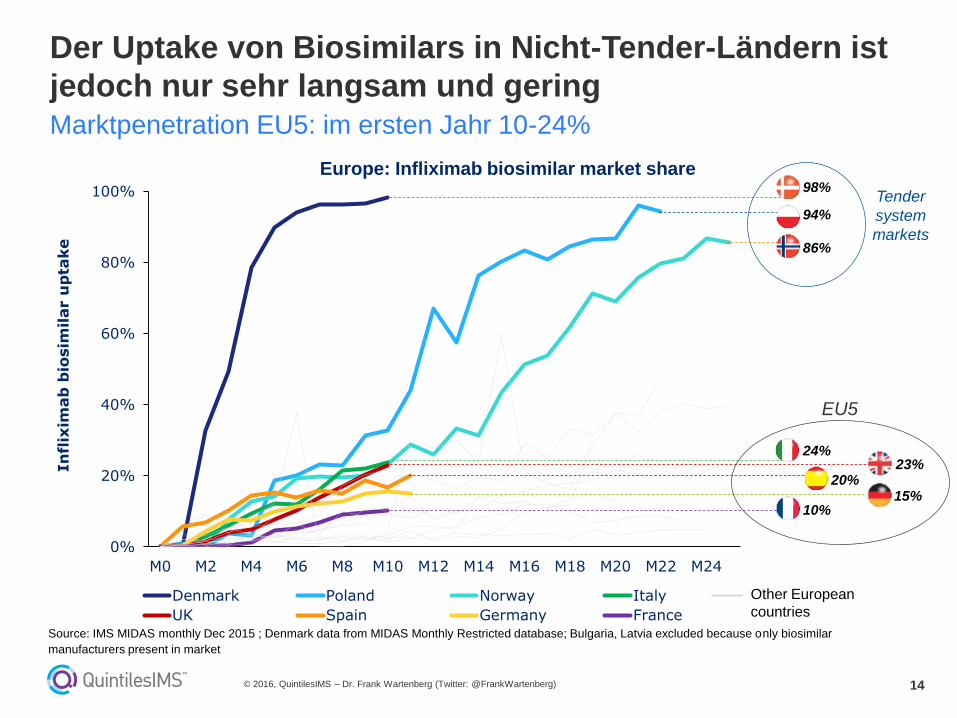

Der Uptake von Biosimilars in Nicht-Tender-Ländern ist

jedoch nur sehr langsam und geringMarktpenetration EU5: im ersten Jahr 10-24%

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Europe: Infliximab biosimilar market share

0%

20%

40%

60%

80%

100%

M0 M2 M4 M6 M8 M10 M12 M14 M16 M18 M20 M22 M24

In

flix

imab

bio

sim

ilar u

pta

ke

Denmark Poland Norway Italy

UK Spain Germany France

98%

94%

86%

24%23%

20%

10%15%

EU5

Tender

system

markets

Other European

countries

Source: IMS MIDAS monthly Dec 2015 ; Denmark data from MIDAS Monthly Restricted database; Bulgaria, Latvia excluded because only biosimilar

manufacturers present in market

15

Die Regularien für den Market Access von Biosimilars

ändern sich jedoch – zu Gunsten der Biosimilars

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Source: QuintilesIMS

Proposed new concrete

biosimilar approval

guidelines in 2016

Behind in terms of

regulation, particularly on

clinical requirements and

length of regulatory process

Established biosimilar

legislation and

guidance (PMDA)

Established biosimilar

legislation and guidance

aligned to EMA

framework.

Fully established framework and solid

draft guidance for biosimilar Mab.

Substitution not allowed

Guidance published.

Global reference

product accepted

Regulatory maturity framework

Fully established

framework

Lack of a clear

framework

Legal pathway

established, FDA

guidelines published.

Pathway now being

tested

Pathway under development.

Access through national and

regional tenders

Global Biosimilar Landscape

Guidance finalized in 2010. Dual

pathway with abbreviated non-

clinical and clinical data

Guidance finalized. No clear

clinical criteria for biosimilar

approval (case-by-case

approach)

• Regulatory framework of biosimilars in EMs varies and likely to evolve differently from country to

country

• Competition of biosimilars vs. NOBs in EMs to be influenced by local policies (e.g. PDPs in Brazil)

Approval of a “biosimilar product”

requires submission of an “abridged”

application to the MOH. Biosimilars have

interchangeable status

16

Auf lange Sicht werden drei Faktoren, den Uptake von

Biosimilars beeinflussen

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Market

opportunity for

biosimilar

players

Huge financial incentive in pursuing

this growing market

Payer

willCost Savings (~20-30% vs. Originator)

and better patient healthcare management

Patients seeking

access

Affordable Access to breakthrough therapies

leading to better health outcomes

Source: IMS Health

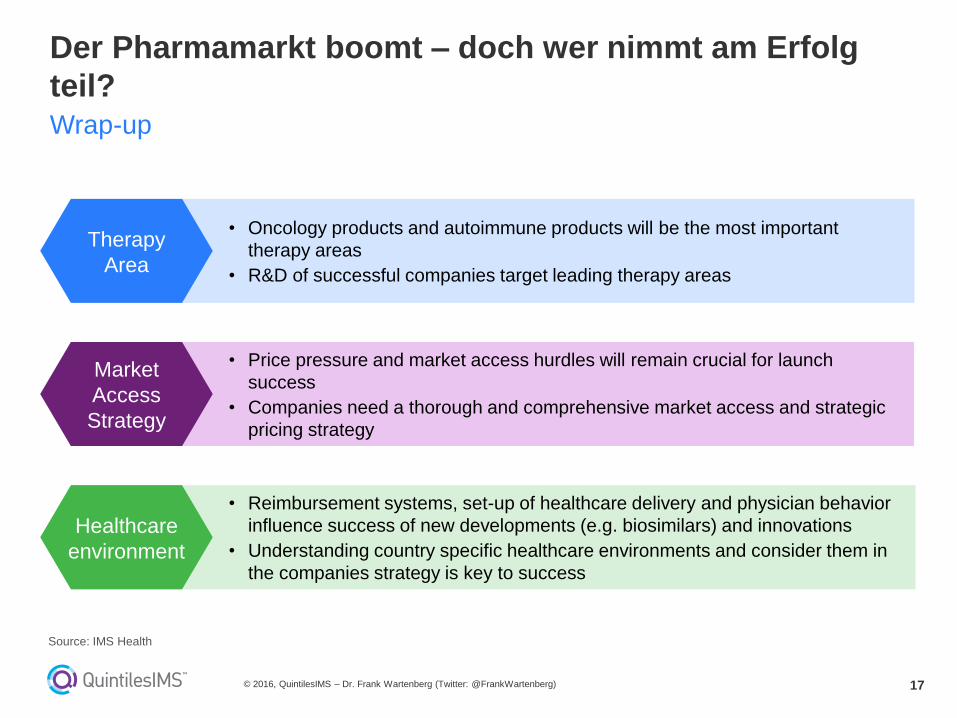

17

• Reimbursement systems, set-up of healthcare delivery and physician behavior

influence success of new developments (e.g. biosimilars) and innovations

• Understanding country specific healthcare environments and consider them in

the companies strategy is key to success

• Price pressure and market access hurdles will remain crucial for launch

success

• Companies need a thorough and comprehensive market access and strategic

pricing strategy

• Oncology products and autoimmune products will be the most important

therapy areas

• R&D of successful companies target leading therapy areas

Der Pharmamarkt boomt – doch wer nimmt am Erfolg

teil? Wrap-up

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Therapy

Area

Market

Access

Strategy

Healthcare

environment

Source: IMS Health

18

Please contact me for further information

© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

Dr. Frank Wartenberg

President Central Europe

+49 (0) 69 6604-4315

Follow me on Twitter: @FrankWartenberg

19© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

© 2016, IMS HEALTH GmbH & Co. OHG

Alle Rechte vorbehalten. Die Informationen dürfen weder ganz noch teilweise ohne vorherige ausdrückliche Erlaubnis von

IMS HEALTH GmbH & Co. OHG vervielfältigt, gespeichert, weiterverarbeitet und in keiner Weise zugänglich gemacht werden.

Die gegebenenfalls im Zusammenhang mit Daten verwendeten Begriffe „Patient, Arzt, Arztpraxis, Verordner oder Apotheke“ bezeichnen keine

personenbezogenen, sondern ausschließlich (nach § 3 Abs. 6 Bundesdatenschutzgesetz) anonyme Informationen.

IMS stellt durch den Einsatz modernster Technologien und Verfahren sicher, dass seine Dienstleistungen, unabhängig davon wie die Daten

untereinander verknüpft werden, den Datenschutzbestimmungen entsprechen.

20© 2016, QuintilesIMS – Dr. Frank Wartenberg (Twitter: @FrankWartenberg)

© 2016, IMS HEALTH GmbH & Co. OHG

All rights reserved. The information may not be duplicated, stored, further processed, nor be made accessible in whole or in part to any third party

without the prior express written consent of IMS HEALTH.

In connection with data/figures used terms, such as „patient, doctor, medical practice, prescriber or pharmacy”, do not designate any personal data

but exclusively anonymous information (in accordance with § 3 Abs. 6 “Bundesdatenschutzgesetz” – German Federal Data Protection Act)

IMS employs high sophisticated technologies and methods which ensure all its Information Services to meet the applicable data-protection

requirements, regardless the way data are combined with one another.