01.Ppt Daniela Schreiber

21

Daniela Schreiber Slide 1 Europe PV Market and Public Policy Daniela Schreiber EuPD Research

-

Upload

hyo-seob-an -

Category

Documents

-

view

226 -

download

0

Transcript of 01.Ppt Daniela Schreiber

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 1/21

Daniela Schreiber Slide 1

Europe PV Mark et and Publ icPol icy

Daniela Schreiber

EuPD Research

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 2/21

Daniela Schreiber Slide 2

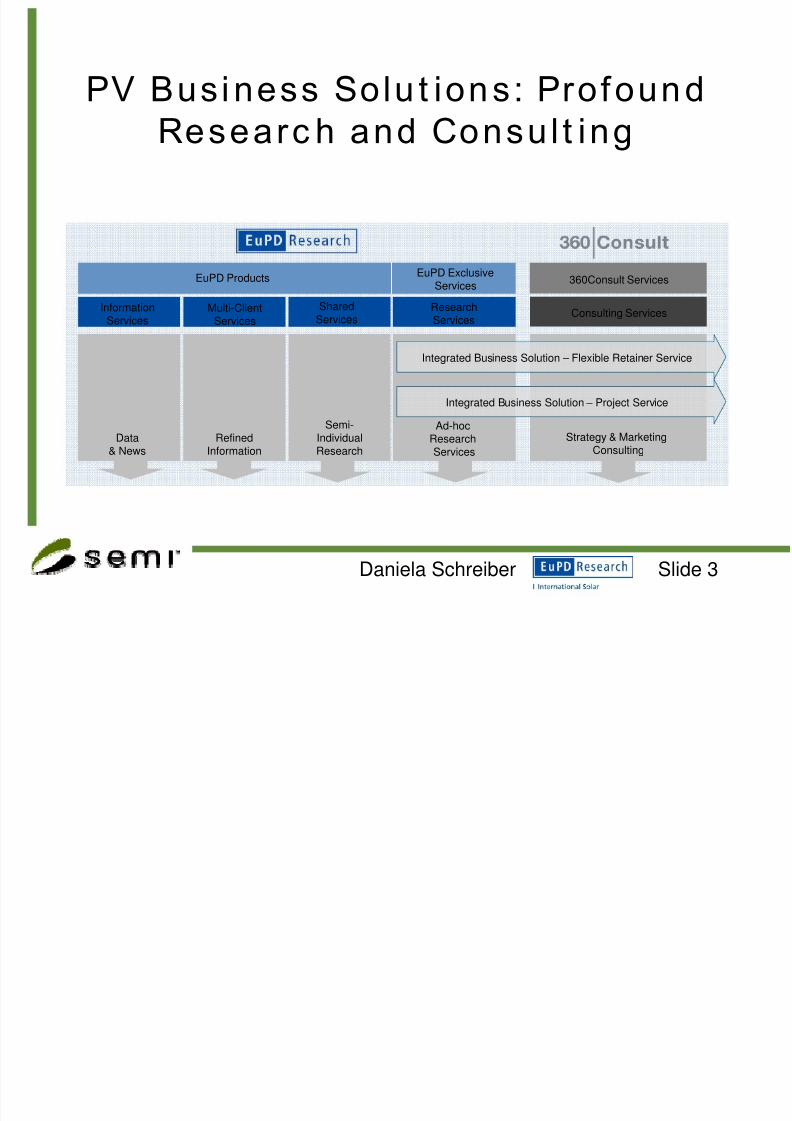

PV Business Solu t ions: Profound

Researc h and Consul t ing

About EuPD Research

• EuPD Research is an international B2B marketresearch company that provides sustainableresearch for sustainable companies.

About 360Consult

• 360Consult is a strategy & marketing consultancythat provides sustainable consulting forsustainable companies based on primary andsecondary data.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 3/21

Daniela Schreiber Slide 3

PV Business Solu t ions: ProfoundResearc h and Consul t ing

Information

Services

Multi-Client

Services

Shared

Services

EuPD Products

Research

Services

EuPD ExclusiveServices

Consulting Services

360Consult Services

Data& News

RefinedInformation

Semi-IndividualResearch

Ad-hocResearchServices

Strategy & MarketingConsulting

Integrated Business Solution – Flexible Retainer Service

Integrated Business Solution – Project Service

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 4/21

Daniela Schreiber Slide 4

Current s i t uat ion on t he g lobal PVmarke ts :

• Ramp-up of PV module supply• Collapse of the Spanish PV market

• Emerging markets (e.g. EasternEurope, Asia and the US) cannot beexpected to absorb Spanish capacities

• Panel price decrease• Global financial and economic crisis

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 5/21

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 6/21

Daniela Schreiber Slide 6

In t ernat iona l ModulePr ic eIndex

2009

This chartdisplays theprice indices for

each nationalmarket. Startingpoint isQ4/2008.

65.85%

91.63%

80.70%

67.79%

100%

92.01%

69.90%

94.10%

86.59%

72.02%

86.07%85.38%

69.49%

83.22% 82.27%

50%

60%

70%

80%

90%

100%

110%

4th quarter2008 1st quarter2009 2nd quarter2009 3rd quarter2009

Germany Spain Italy France USA

Source: EuPD Research 2009

startingpoint

78.62%D e c r e a s e o f ~ 3 0 %

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 7/21

Daniela Schreiber Slide 7

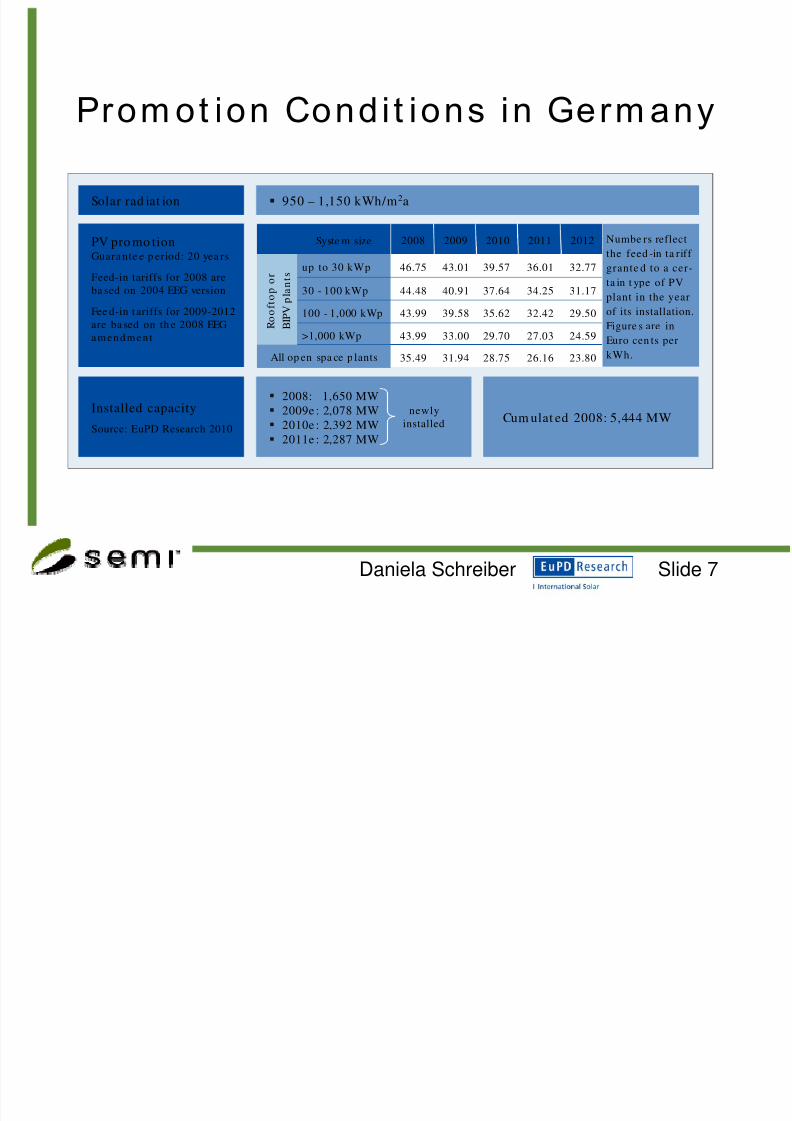

Prom ot ion Condi t ions in Germ any

950 – 1,150 kWh/m2aSolar rad iat ion

PV pro mo tionGuara nte e p eriod: 20 yea rs

Feed-in tariffs for 2008 are

ba sed on 2004 EEG version

Fee d-in t ariffs for 2009-2012

are ba sed on th e 2008 EEGamendment

Numbe rs reflect

the feed -in ta riff

grante d to a cer-

ta in t ype of PV

plant in the year

of its installation.

Figure s are in

Euro cen ts per

kWh.

2008: 1,650 MW

2009e : 2,078 MW

2010e : 2,392 MW 2011e : 2,287 MW

Installed capacity

Source: EuPD Research 2010

Cum ulat ed 2008: 5,444 MW

2008 2009 2010 2011 2012Syste m size

up to 30 kWp 46.75 43.01 39.57 36.01 32.77

30 - 100 kWp 44.48 40.91 37.64 34.25 31.17

100 - 1,000 kWp 43.99 39.58 35.62 32.42 29.50

>1,000 kWp 43.99 33.00 29.70 27.03 24.59

35.49 31.94 28.75 26.16 23.80

R o

o f t o p o r

B I P V p l a n t s

All op en spa ce p lants

newly

installed

950 – 1,150 kWh/m2aSolar rad iat ion

PV pro mo tionGuara nte e p eriod: 20 yea rs

Feed-in tariffs for 2008 are

ba sed on 2004 EEG version

Fee d-in t ariffs for 2009-2012

are ba sed on th e 2008 EEGamendment

Numbe rs reflect

the feed -in ta riff

grante d to a cer-

ta in t ype of PV

plant in the year

of its installation.

Figure s are in

Euro cen ts per

kWh.

2008: 1,650 MW

2009e : 2,078 MW

2010e : 2,392 MW 2011e : 2,287 MW

Installed capacity

Source: EuPD Research 2010

Cum ulat ed 2008: 5,444 MW

2008 2009 2010 2011 2012Syste m size

up to 30 kWp 46.75 43.01 39.57 36.01 32.77

30 - 100 kWp 44.48 40.91 37.64 34.25 31.17

100 - 1,000 kWp 43.99 39.58 35.62 32.42 29.50

>1,000 kWp 43.99 33.00 29.70 27.03 24.59

35.49 31.94 28.75 26.16 23.80

R o

o f t o p o r

B I P V p l a n t s

All op en spa ce p lants

newly

installed

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 8/21

Daniela Schreiber Slide 8

Main aspec t s o f t he 2008 EEG

am endm ent c onc ern ing t hephot ovo l t a ic indus t ry

• Increase in the annual degression rate (stronger than

originally stipulated in the initial draft amendment).• Establishment of a dynamic ‘growth corridor’; an

instrument that serves to limit the amount of newly installedPV plants by increasing the degression rate if a certaintarget value is exceeded while rewarding less excessive

capacity growth.• There is currently no existing promotion scheme for BIPV.

In the past, BIPV was advocated by the façade bonus of €0,05/kWh for new PV installations integrated in the façadeof a building. This special promotion was abolished in 2009.

• Since the change of government, remuneration for solarelectricity is reviewed. This could mean that in 2011, at thelatest, feed-in tariff rates could decline even further thanoriginally anticipated.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 9/21

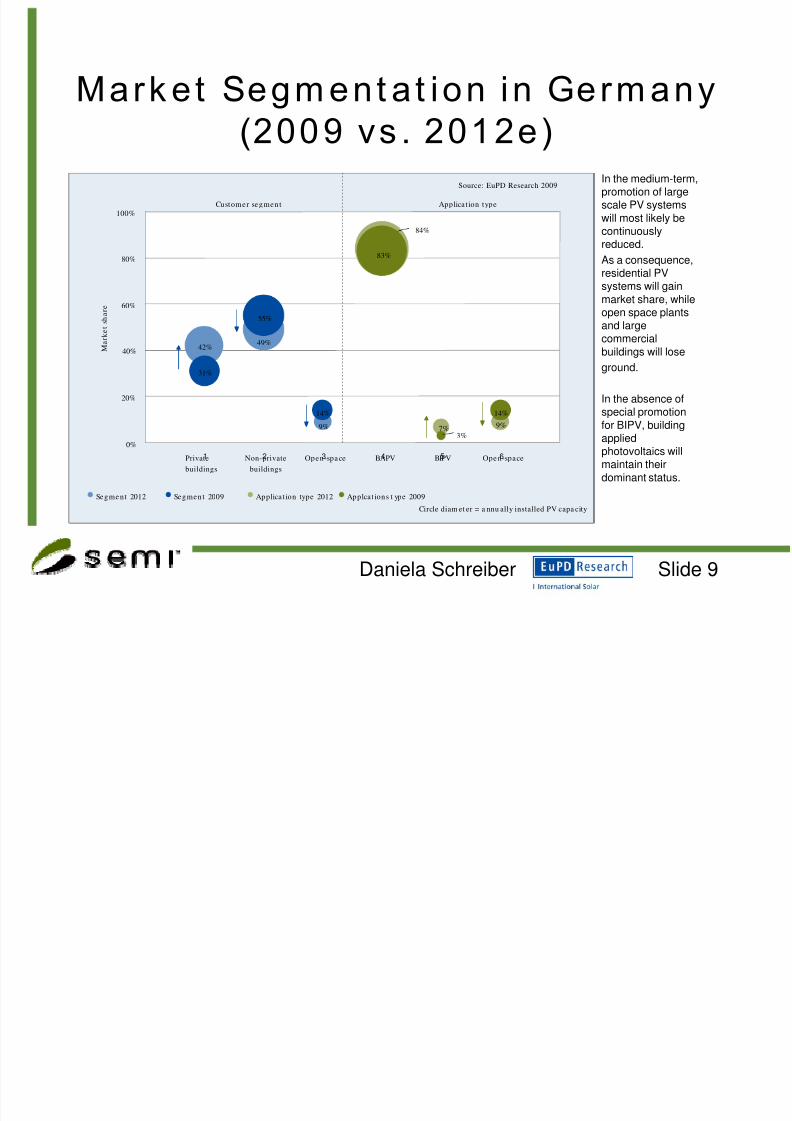

Daniela Schreiber Slide 9

Mark et Segm ent a t ion in Germ any(2009 vs . 2012e)

49%

9%

42%

31%

55%

14%

7% 9%

84%

3%

14%

83%

0%

20%

60%

80%

100%

1 2 3 4 5 6

M a r k e t s h a r e

Segme nt 2012 Segment 2009 Applica t ion type 2012 Applca t ions t ype 2009

Customer segment Applica t ion type

Private

buildings

Non-private

buildings

Open-spa ce BAPV BIPV Ope n-space

Source: EuPD Research 2009

Circle diam et er = a nnu ally installed PV capa city

40%49%

9%

42%

31%

55%

14%

7% 9%

84%

3%

14%

83%

0%

20%

60%

80%

100%

1 2 3 4 5 6

M a r k e t s h a r e

Segme nt 2012 Segment 2009 Applica t ion type 2012 Applca t ions t ype 2009

Customer segment Applica t ion type

Private

buildings

Non-private

buildings

Open-spa ce BAPV BIPV Ope n-space

Source: EuPD Research 2009

Circle diam et er = a nnu ally installed PV capa city

40%

In the medium-term,promotion of largescale PV systems

will most likely becontinuouslyreduced.

As a consequence,residential PVsystems will gain

market share, whileopen space plants

and largecommercial

buildings will lose

ground.

In the absence ofspecial promotion

for BIPV, buildingappliedphotovoltaics willmaintain their

dominant status.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 10/21

Daniela Schreiber Slide 10

Prom ot ion Condi t ions in Spain

1,000 – 1,900 kWh/m²aSolar radiation

Fee d-in t a riff

2007: 556 MW*

2008: 2,750 MW*

2009e: 500 MW**

2010e: 493 MW**

2011e: 466 MW**

Insta lled capa citySource: EuPD Research 2009

Cum ulat ed 2008*: 3,360 MWNewlyinstalled

Roo fto p: 0.32 – 0.34 €/kWh

Ope n-space: origina lly 0.32 €/kWh, in Q3/2009 cut ba ck to 0.30 €/kWh

The fee d-in ta riff varies in dep en de ncy on how much of t he cap‘s limit ha s

bee n re ached in t he preceding qu arte rs (critical limit: 75 percent of th e cap)

The cap increases by the p ercent ag e th e fe ed-in tariff de crea ses an d vice versa.

500 MW cap in 2009 (233 MW op en -spa ce an d 267 MW roo ftop ); prospe ctivecap: 460 MW in 2010, 400 MW in 2011

Current ly, a new a men dme nt is being draw n up for the t ime after 2011.

2008 am en dm en t of feed -in ta riffs by the Rea l Decreto 1578/2008

* As per October 2009.

**The given figures do not

represent the market

volume in the given year

but the upper limit of the

current promotion act RD

1578/2008. According to

information from the

Spanish Energy

Commission CNE in

October 2009, only 18

MW have been newly

installed between January

and August 2009. Hence,

it can not be expected that

the upper limit will be

reached in 2009. The

Spanish Solar Association

ASIF 150 MW at the most

in 2009. On slide A.6., the

main reasons for thisdevelopment are depicted.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 11/21

Daniela Schreiber Slide 11

Mark et Segm ent a t ion in Spa in

(2009 vs . 2012e)

14%

42%44%

63%

28%

9%

52%

42%

6%

34%

63%

3%

0%

20%

40%

60%

80%

100%

0 1 2 3 4 5 6 7

M a r k e t s h

a r e

Segment 2012 Segment 2009 Appliance 2012 Appliance 2009

Market Segment Application Type

Residential

buildings

Non-residential

buildings

Open

space

BAPV BIPV Ground-

mounted

Source: EuPD Research 2009

Diame trer o f bub ble = Installed PV capacity

Due to the dynamic

capping, the marketshare of BAPV

plants will increase.

Moreover, the extra

contingent for theopen-spacesegment (100 MWin 2009, 60 MW in

2010) will be

abolished in 2011.Regardingapplication types,

BAPV and BIPVplants will acquiremarket shares.

However, BIPVplants will remain a

niche market as thissegment is not

particularlypromoted.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 12/21

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 13/21

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 14/21

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 15/21

Daniela Schreiber Slide 15

Mark et Segm ent a t ion in Franc e

(2009 vs. 2012e)

34% 35%

31%

39%

31% 30%

52%

35%

13%

59%

30%

11%

0%

20%

40%

60%

80%

100%

0 1 2 3 4 5 6 7

M a r k e t s

h a r e

Se gm en t 2012 Se gm en t 2009 Ap plica tio n t yp e 2012 Application type 2009

Source: EuPD Research 2009

Circle size=yearly insta lled cap acity

Customer se gm en ts Applica t ion type

Private

buildings

Non-private

buildings

Open-space BAPV BIPV Open-space

34% 35%

31%

39%

31% 30%

52%

35%

13%

59%

30%

11%

0%

20%

40%

60%

80%

100%

0 1 2 3 4 5 6 7

M a r k e t s

h a r e

Se gm en t 2012 Se gm en t 2009 Ap plica tio n t yp e 2012 Application type 2009

Source: EuPD Research 2009

Circle size=yearly insta lled cap acity

Customer se gm en ts Applica t ion type

Private

buildings

Non-private

buildings

Open-space BAPV BIPV Open-space

EuPD Researchexpect an increasein market share

within all marketsegments,especially within theopen space

segment due to theBorloo plan.

The particularlyhigh feed-in tariff for

BIPV plantssecures stable

market shares forplants on residentialand non-residentialbuildings.

French PV pro-motion is currently

being revised. Inthe future, thenumber of plants

receiving BIPVpromotion will mostlikely be reduceddrastically.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 16/21

Daniela Schreiber Slide 16

Current Mark et Trends

High Low

c o m p

e t i t i v e

i n t e n s i t

y

C u s t o m e r v a l u e

High

Low

Selling price

Development/Introduction

Rapid market growth

Extension of production

capacities

The search for new markets

Price / cost reduction

The search for differentiation

2nd EEG amendment 2009

and Spanish market collapse

1st EEG amendment

2004

Currentsituation

Penetration of markets

“Tausend-Dächer-

Programm “ 2000

Production orientation

Product orientation

Sales

orientation

Marketorientation

Customer

orientation

Development of

reliable products

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 17/21

Daniela Schreiber Slide 17

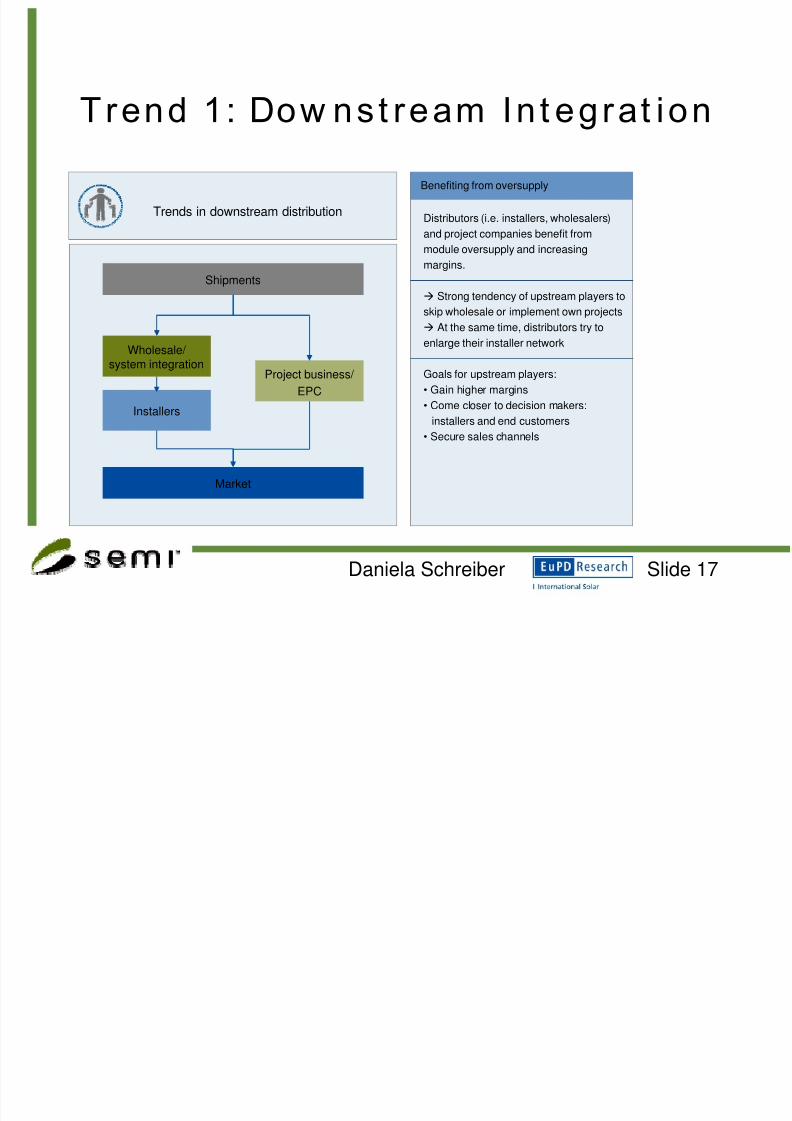

Trend 1: Dow nst ream In t egrat ion

Trends in downstream distribution Distributors (i.e. installers, wholesalers)and project companies benefit from

module oversupply and increasing

margins.

Strong tendency of upstream players to

skip wholesale or implement own projects

At the same time, distributors try to

enlarge their installer network

Goals for upstream players:

• Gain higher margins

• Come closer to decision makers:

installers and end customers

• Secure sales channels

Benefiting from oversupply

Shipments

Market

Project business/

EPC

Wholesale/

system integration

Installers

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 18/21

Daniela Schreiber Slide 18

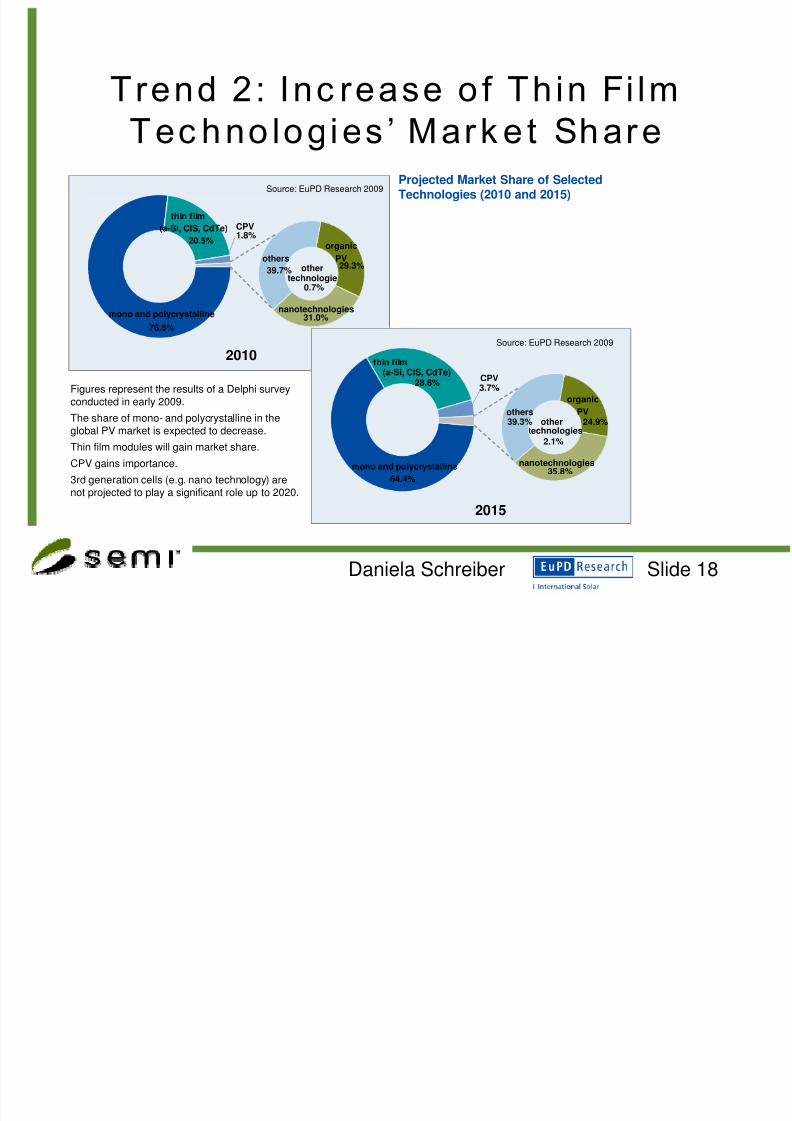

Trend 2: Inc rease o f Thin Fi lm

Tec hno logies ’ Mark e t Share

other39.7% 29.3%

Source: EuPD Research 2009

othertechnologies

0.7%

nanotechnologies31.0%

others

39.7%

organic

PV29.3%

1.8%

thin film(a-Si, CIS, CdTe)

20.5%

mono and polycrystalline

76.6%

Source: EuPD Research 2009

n = 35

CPV

2010

2015

other

39.7% 29.3%

Source:EuPD Research 2009

othertechnologies

0.7%

nanotechnologies31.0%

others*39.7%

organicPV29.3%

1.8%

thin-film

(a-Si, CIS, CdTe)20.5%

mono-and polycrystalline

PV76.6%

Source:EuPD Research 2009

n = 35

CPV

2010

other

39.7% 29.3%

Source:EuPD Research 2009

othertechnologies

0.7%

nanotechnologies31.0%

others*39.7%

organicPV29.3%

1.8%

thin-film

(a-Si, CIS, CdTe)20.5%

mono-and polycrystalline

PV76.6%

Source:EuPD Research 2009

n = 35

CPV

2010

64.4%

other

technologies2.1%

CPV3.7%

28.6%

nanotechnologies35.8%

24.9%others39.3%

Source: EuPD Research 2009

thin film(a-Si, CIS, CdTe)

mono and polycrystalline

organic

PV

2015

Projected Market Share of SelectedTechnologies (2010 and 2015)

Figures represent the results of a Delphi survey

conducted in early 2009.

The share of mono- and polycrystalline in the

global PV market is expected to decrease.Thin film modules will gain market share.

CPV gains importance.

3rd generation cells (e.g. nano technology) are

not projected to play a significant role up to 2020.

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 19/21

Daniela Schreiber Slide 19

Trend 2: PV Tec hnology Waves

time

Quelle:EuPDResea rch 2008

2007 2010 2015

0 %

100 %

Degre eof m arke tdiffusion

Time2009 2015 2020

0 %

100 %

R & D

CdTe

thin film

a-µ-Si, CIS/CIGS, CdTe

Degre e of ma rket diffusion

m a s s p r o d u c t i o n

Source: EuPD Research 2009

thin filma-µ -Si, CIS/CIGS, CdTe

crystallinec-Si, mc-Si

crystallinec-Si, mc-Si

crystallinec-Si, mc-Si

thin filma-µ-Si, CIS/CIGS, CdTe

nano

new

technologies

new

technologies

new

technologies

organic

nano organic

nano organic

time

Quelle:EuPDResea rch 2008

2007 2010 2015

0 %

100 %

Degre eof m arke tdiffusion

Time2009 2015 2020

0 %

100 %

R & D

CdTe

thin film

a-µ-Si, CIS/CIGS, CdTe

Degre e of ma rket diffusion

m a s s p r o d u c t i o n

Source: EuPD Research 2009

thin filma-µ -Si, CIS/CIGS, CdTe

crystallinec-Si, mc-Si

crystallinec-Si, mc-Si

crystallinec-Si, mc-Si

thin filma-µ-Si, CIS/CIGS, CdTe

nano

new

technologies

new

technologies

new

technologies

organic

nano organic

nano organic

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 20/21

Daniela Schreiber Slide 20

Trend 3: Produc t Di f ferent ia t ion –

Ex am ple BIPV

0% 10% 20% 30% 40% 50% 60%

France

Germany

Italy

USA

Spain

China

Japan

Switzerland

Emirates

Netherlands

Scandinavia

no answer

Source: EuPD Research 2010

multi response

n = 87

two mentions

- Greece

- UK

- Belgium

only mentioned once:

- Poland

- Canada

- Korea

- Mexico

- Brazil

- India

- Austria

- Turkey

- Luxemburg

- Marocco

0% 10% 20% 30% 40% 50% 60%

France

Germany

Italy

USA

Spain

China

Japan

Switzerland

Emirates

Netherlands

Scandinavia

no answer

Source: EuPD Research 2010

multi response

n = 87

two mentions

- Greece

- UK

- Belgium

only mentioned once:

- Poland

- Canada

- Korea

- Mexico

- Brazil

- India

- Austria

- Turkey

- Luxemburg

- Marocco

Most Important Future BIPV Markets

8/8/2019 01.Ppt Daniela Schreiber

http://slidepdf.com/reader/full/01ppt-daniela-schreiber 21/21

Daniela Schreiber Slide 21

Thank you very m uc h fo r your

a t ten t i on !

Disclaimer

NEITHER HOEHNER RESEARCH & CONSULTING GROUP GMBH NOR ANY OF ITS EMPLOYEES MAKES ANY WARRANTY, EXPRESS OR IMPLIED, ORASSUMES ANY LEGAL LIABILITY OR RESPONSIBILITY FOR THE ACCURACY, COMPLETENESS, OR USEFULNESS OF ANY INFORMATION, PRODUCT, ORPROCESS DISCLOSED. THIS PRODUCT WAS PREPARED USING PROFESSIONAL METHODS AND WITH GREAT CARE, TAKING ACCOUNT OF RELEVANT

LEGISLATION. THE DATA CONATINED IN THIS PRODUCT IS BASED ON SURVEYS OF SAMPLE POPULATIONS, CONDUCTED USING STANDARDSTATISTICAL METHODS. AS SUCH, THE STUDY IS SUBJECT TO A CERTAIN STATISTICAL ERROR RATE AND IS BASED EXCLUSIVELY ON THE FACTSWHICH WERE AVAILABLE AT THE TIME OF THE SURVEY.THE AUTHORS MAKE NO GUARANTEES THAT ANY DECISION BASED ON THE INFORMATIONPROVIDED WILL BENEFIT YOU IN SPECIFIC APPLICATIONS, OWING TO THE RISK THAT IS INVOLVED IN DECISION-MAKING OF ALMOST ANY KIND.

REFERENCE TO ANY SPECIFIC COMMERCIAL PRODUCT, PROCESS, OR SERVICE BY TRADE NAME, TRADEMARK, MANUFACTURER, OR OTHERWISEDOES NOT NECESSARILY CONSTITUTE OR IMPLY ITS ENDORSEMENT, RECOMMENDATION, OR FAVORING BY HOEHNER RESEARCH & CONSULTINGGROUP GMBH. OUR SALESPEOPLE, RESEARCH ANALYSTS, AND OTHER PROFESSIONALS MAY PROVIDE ORAL OR WRITTEN MARKET COMMENTARYTO OUR CLIENTS THAT REFLECT OPINIONS THAT ARE CONTRARY TO VIEWS AND OPINIONS EXPRESSED IN THIS PUBLICATION. THE VIEWS ANDOPINIONS OF AUTHORS EXPRESSED HEREIN DO NOT NECESSARILY STATE OR REFLECT THOSE OF HOEHNER RESEARCH & CONSULTING GROUPGMBH.

NO PART OF THIS PUBLICATION MAY BE COPIED OR DUPLICATED IN ANY FORM BY ANY MEANS OR REDISTRIBUTED OR PUBLISHED WITHOUT THEPRIOR WRITTEN CONSENT OF HOEHNER RESEARCH & CONSULTING GROUP GMBH. UNAUTHORIZED COPYING OF THIS PUBLICATION IS CONSIDERED

A BREACH OF COPYRIGHT.

EuPD ResearchAdenauerallee 134 | D-53113 Bonn | Telephone +49 (0) 228-971 43-0 | Fax +49 (0) 228-971 [email protected] | http://www.eupd-research.com | http://shop.eupd-research.com/

ContactDaniela Schreiber | Head Strategic Operations

EuPD Research® is a brand of HOEHNER RESEARCH & CONSULTING GROUP GmbH.

Member of ESOMAR World Research

![[Lukas Schreiber, Jörg Schönherr] Water and Solutions](https://static.fdokument.com/doc/165x107/577c7dbe1a28abe0549fba0a/lukas-schreiber-joerg-schoenherr-water-and-solutions.jpg)

![VisuellEntworfeneProzesseWerdenRealitaet Kufstein2.ppt ...€¦ · Title: Microsoft PowerPoint - VisuellEntworfeneProzesseWerdenRealitaet_Kufstein2.ppt [Kompatibilitätsmodus] Author:](https://static.fdokument.com/doc/165x107/60361314636c52237e13becb/visuellentworfeneprozessewerdenrealitaet-title-microsoft-powerpoint-visuellentworfeneprozessewerdenrealitaet.jpg)