Acquisition of new Spanish customers through German ...

90

Acquisition of new Spanish customers through German Commercial Banks Master Thesis Jordi Basco Carrera | 2520106 Rechts- und Wirtschaftswissenschaften

Transcript of Acquisition of new Spanish customers through German ...

Acquisition of new Spanish customers through German Commercial Banks

Master Thesis

Jordi Basco Carrera | 2520106

Rechts- und Wirtschaftswissenschaften

ii

Universalbanken

Jordi Basco Carrera

Matrikelnummer: 2520106

Studiengang: Diplom Rechts- und Wirtschaftswissenschaften

Master Thesis

Thema: “Kundengewinnung in Spanien durch Deutsche Universalbanken“

Eingereicht: 21. Juli 2013

Betreuer: Dipl.-Wirtsch.-Ing. Daniel Maul

Prof. Dr. Dirk Schiereck

Fachgebiet Unternehmensfinanzierung

Fachbereich Rechts- und Wirtschaftswissenschaften

Technische Universität Darmstadt

Hochschulstraße 1

64289 Darmstadt

iii

Ehrenwörtliche Erklärung

Ich erkläre hiermit ehrenwörtlich, dass ich die vorliegende Arbeit selbstständig angefertigt

habe. Sämtliche aus fremden Quellen direkt oder indirekt übernommenen Gedanken sind als

solche kenntlich gemacht.

Die Arbeit wurde bisher keiner anderen Prüfungsbehörde vorgelegt und noch nicht

veröffentlicht.

Darmstadt, den 21. Juli 2013

i

Abstract

The global economic crisis has led Spain into a dramatic spot. This macroeconomic scene

has had negative consequences in terms of the increase in unemployment, loss of

confidence in the Spanish banking system, capital flight and the increasing number of

evictions, amongst others. This MSc thesis aims to analyse the effects that this economic

crisis has had on people’s attitudes and feelings with regard to the Spanish banking sector

and the identification of potential clients that German banks could gain by entering the

Spanish banking market.

The research was carried out using data collected through a written survey given to over 120

people living in Spain. A review of literature on the topic was made to analyse people’s

perceptions and impressions regarding the current banking sectors both in Spain and

Germany. Literature research shows a variety of parameters that play an important role when

analysing peoples’ attitudes, including age, amount of capital invested, type of client, and

trust in the banking system, amongst others. The results of the research show that people

within the working age group from 18 to 65 years would be more likely to invest their money

in a German bank. Therefore, the German banks’ target group could be clients in this age

range. They could also target particular clients with a small amount of savings. The main

challenges that German banks need to face, if they intend to enter the Spanish market, are

that Spaniards are unlikely to travel to Germany to invest their savings and the issue of

language. Both of these variables have been identified from the statistical analysis as the two

main reasons that deter Spaniards from investing in German banks.

Key words: banking system industry, economic crisis, client perceptions

ii

Table of Contents

Ehrenwörtliche Erklärung .............................................. iii

Abstract ............................................................. i

Table of Contents ..................................................... ii

Acknowledgments .................................................... iv

1. Introduction ........................................................ 1

2. Goal and Research questions ........................................... 5

2.1. Goal .......................................................... 5

2.2. Research questions ............................................... 5

3. Problem analysis and the banking industry .................................. 6

3.1. Loss of confidence in the Spanish banking industry ........................ 6

3.1.1. Evictions .................................................... 9

3.1.2. Preferential shares ............................................ 12

3.2. Client attitude ................................................... 13

3.3. Banks in Spain .................................................. 14

3.4. Capital flight .................................................... 19

4. Main Activities and the methodological approach to research ................... 22

4.1. Analysis of people’s feelings and perceptions ............................ 22

4.2. Main activities................................................... 24

4.3. Data collection methods ........................................... 26

4.4. Limitations of the study ............................................ 29

5. Assessment methodology - Survey ...................................... 30

5.1. Filter questions .................................................. 31

5.1.1. Age range .................................................. 31

5.1.2. Type of client ................................................ 31

5.1.3. Capital invested .............................................. 33

5.1.4. Assets ..................................................... 34

5.2. Specific questions – Spain ......................................... 35

5.2.1. Level of trust ................................................ 35

5.2.2. Relationship between Spanish banks and their clients. .................. 35

5.2.3. Social questions .............................................. 36

5.2.4. Financial questions ............................................ 36

5.2.5. Fear about the safety of savings .................................. 37

iii

5.3. Specific questions – Germany ....................................... 38

5.3.1. Trust in German banks ......................................... 38

5.3.2. Investment in German banks. .................................. 39

5.3.3. Transferring capital out of Spain ................................ 40

5.4. Specific questions – Spain & Germany ................................. 41

6. Results and Statistical Analysis........................................ 42

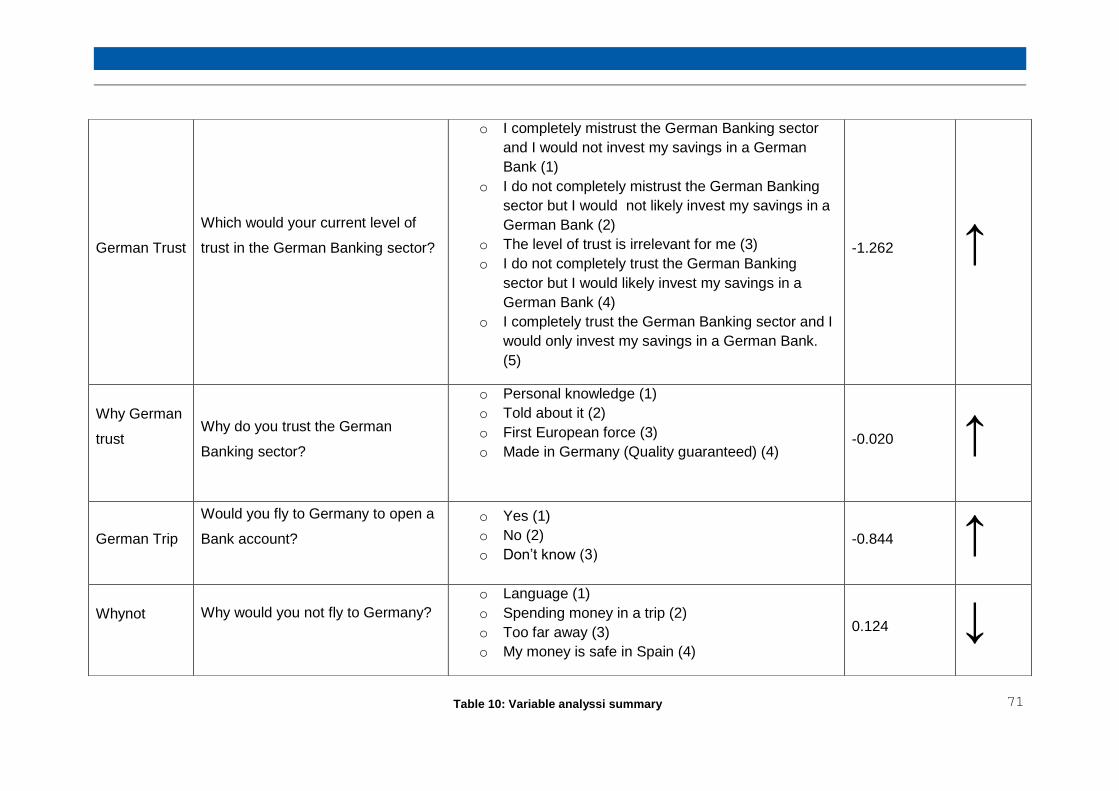

6.1. Analytical variables ............................................... 42

6.2. Survey results .................................................. 48

6.3. Multinomial regression ............................................ 62

6.3.1. The multinomial regression ...................................... 62

6.3.2. Variables and assumptions ..................................... 62

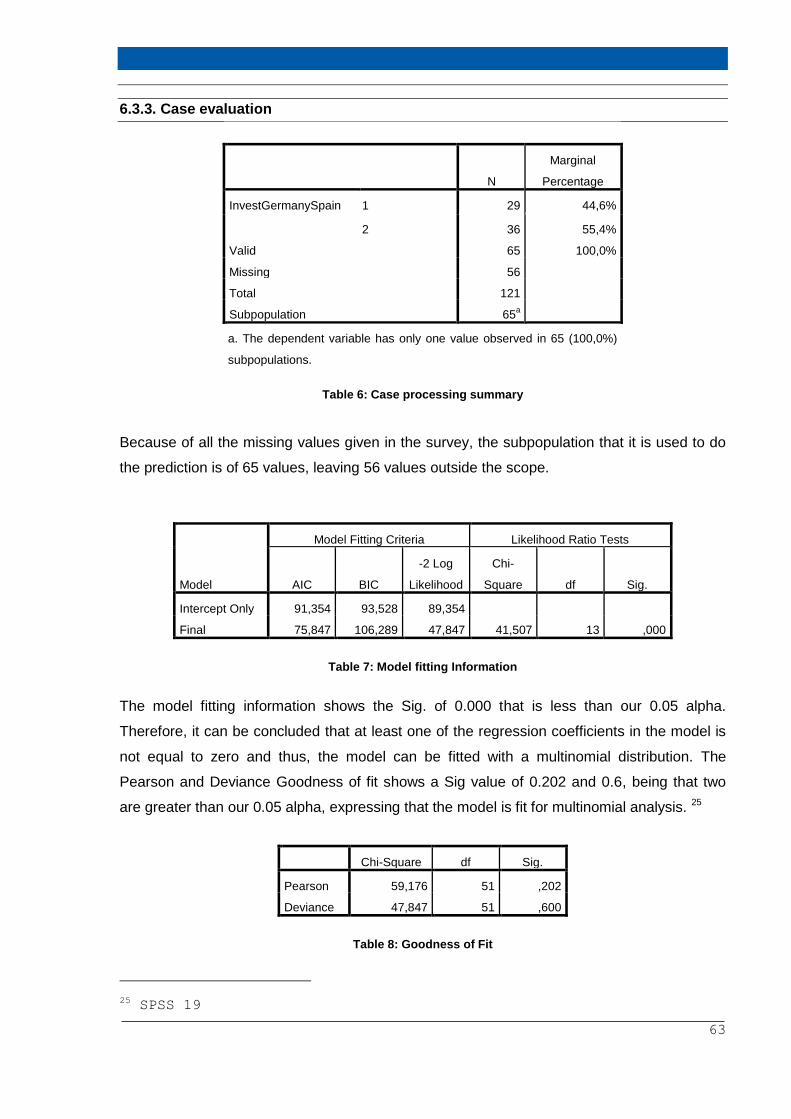

6.3.3. Case evaluation .............................................. 63

6.3.4. Evaluation of Results .......................................... 65

6.3.5. Variable Analysis summary ...................................... 67

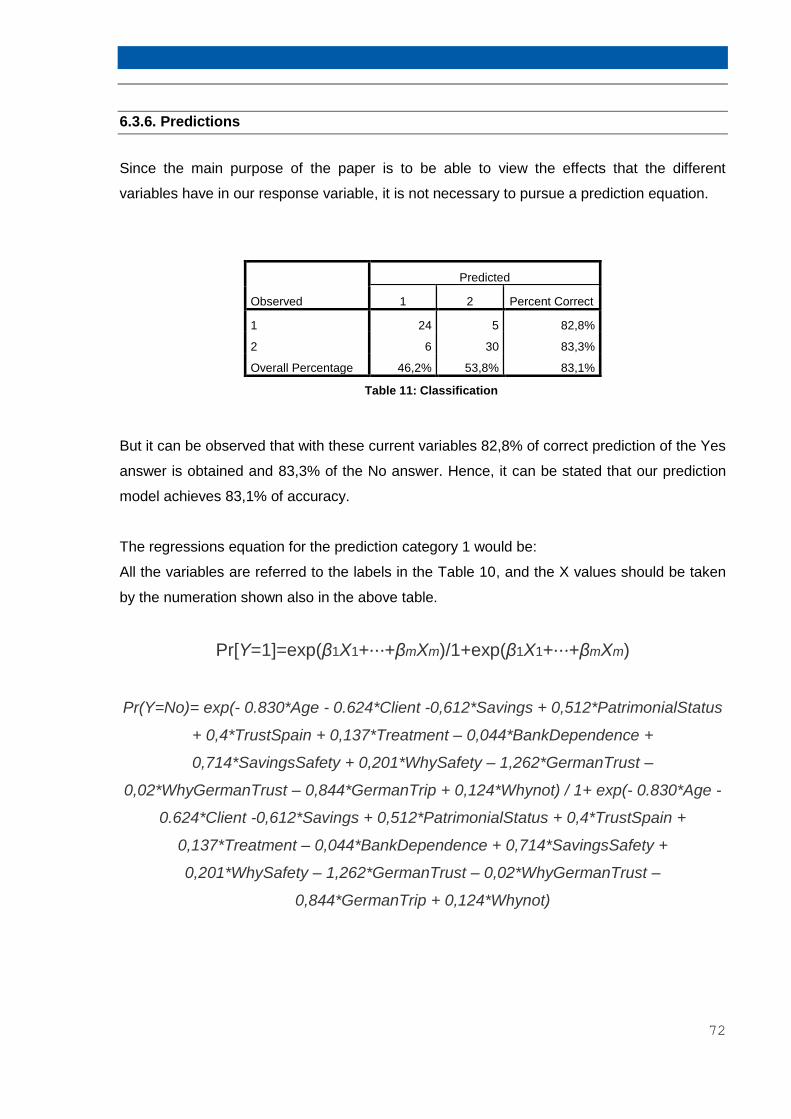

6.3.6. Predictions .................................................. 72

7. Conclusions and recommendations ...................................... 73

List of figures ........................................................ 75

List of tables ......................................................... 76

References ......................................................... 77

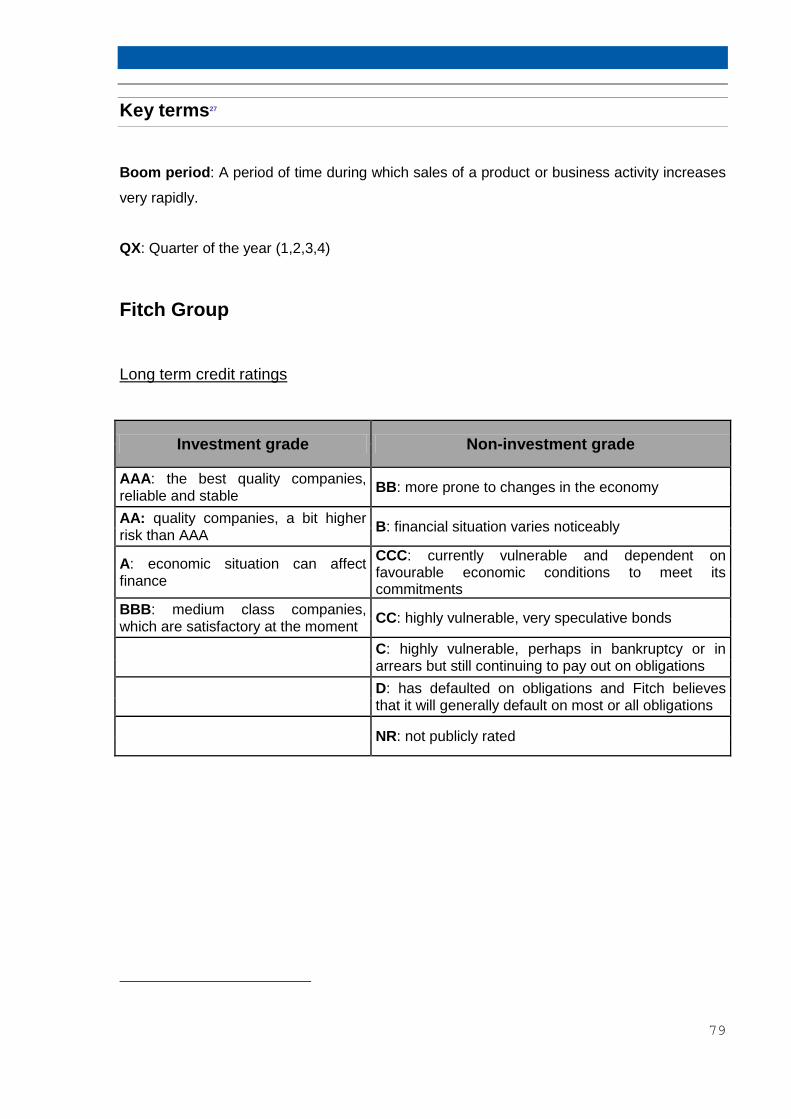

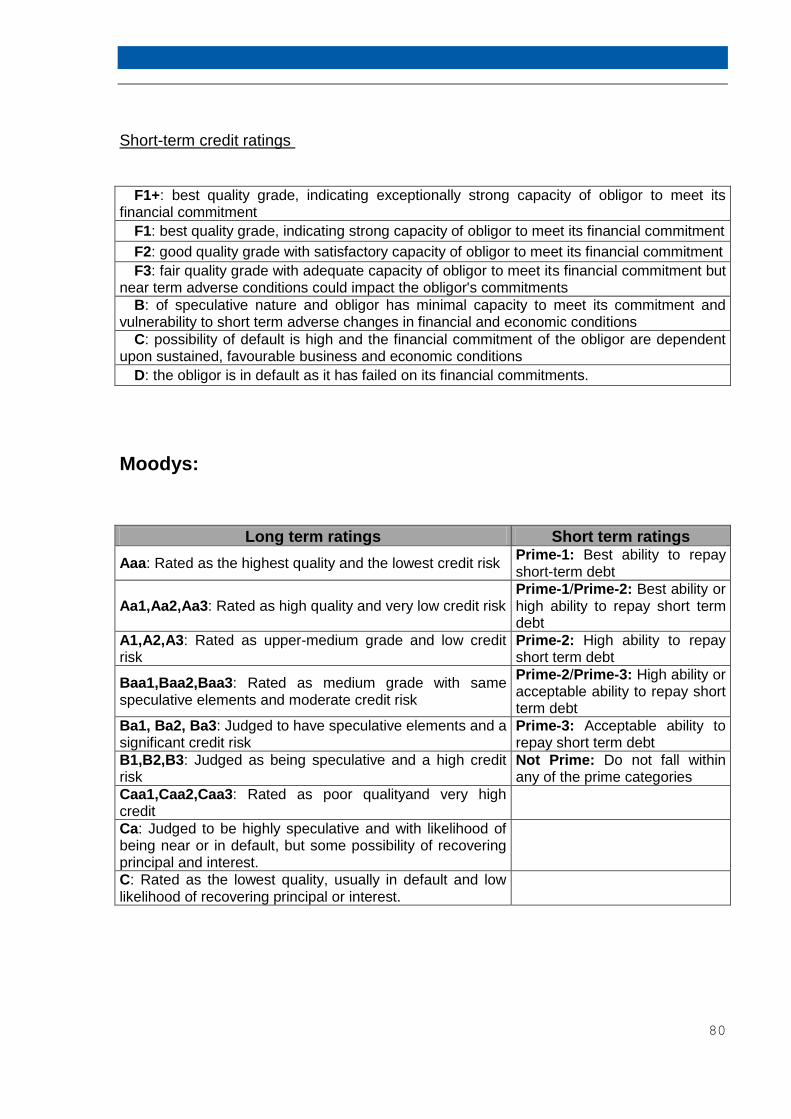

Key terms .......................................................... 79

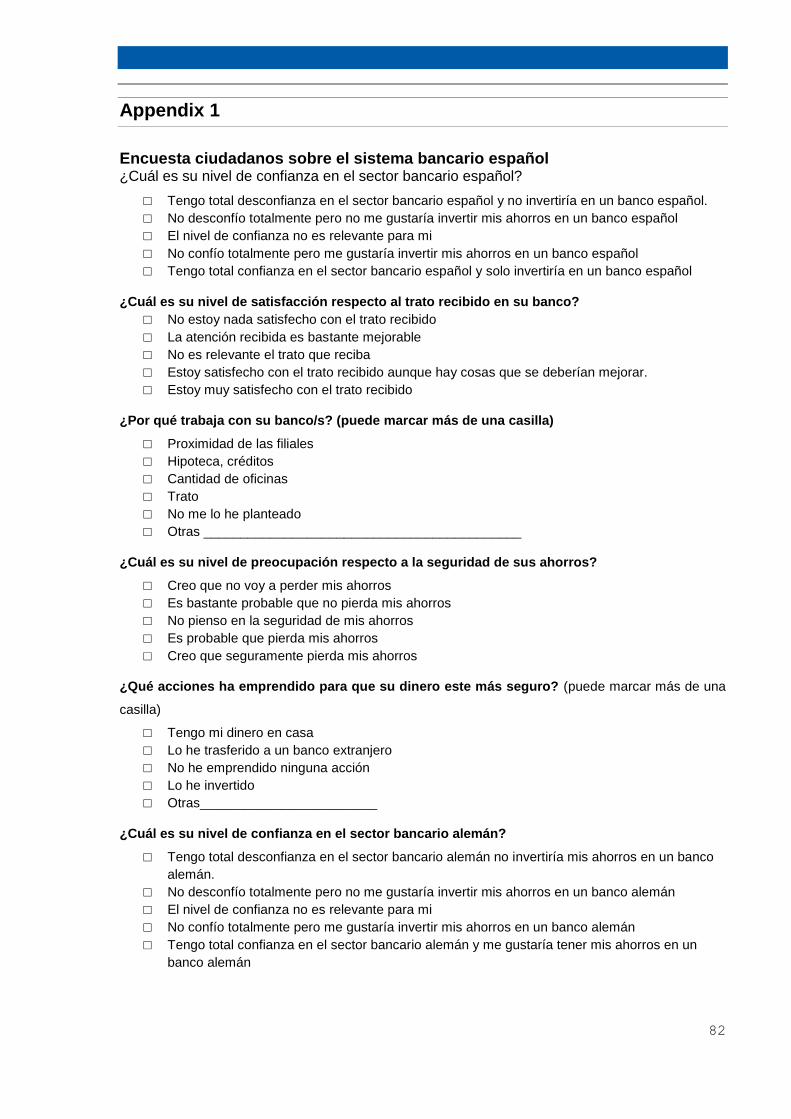

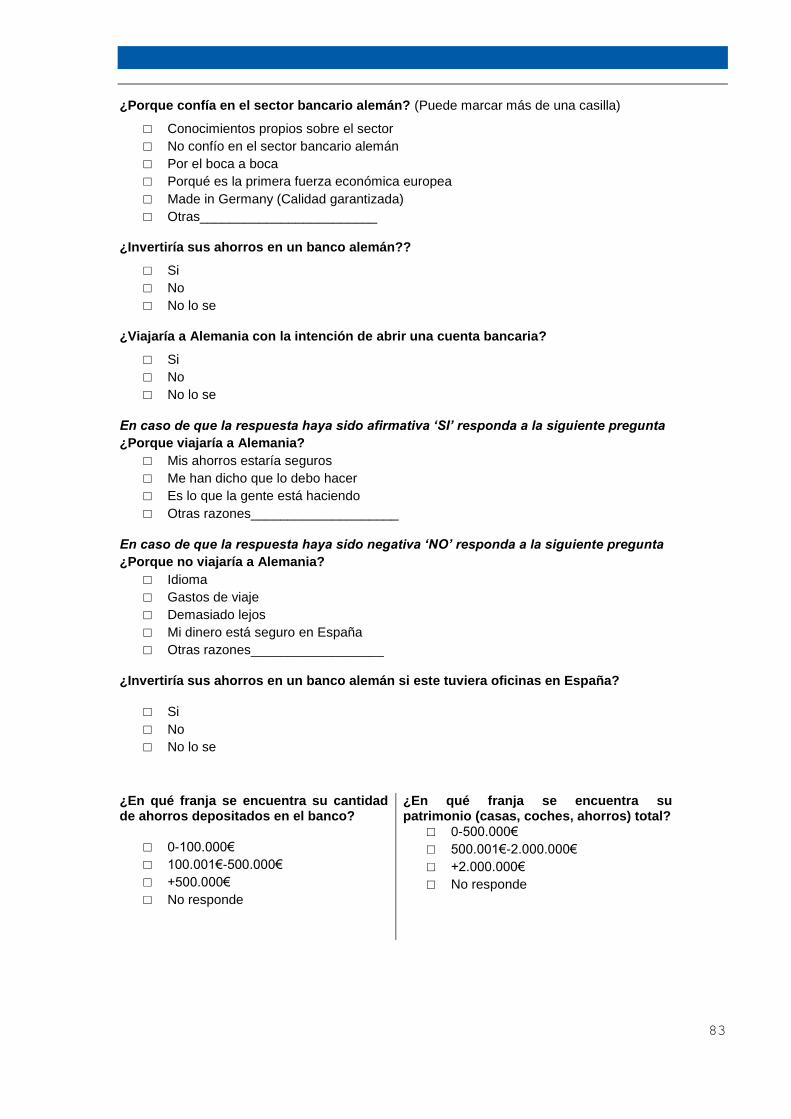

Annex 1 ............................................................ 82

iv

Acknowledgments

I would like to thank my supervisor Daniel Maul for his valuable support and advice during the

period of the development of this MSc Thesis and throughout my time at the university. I

would also like to thank Dr. Schiereck for giving me the opportunity of working on this Msc

Thesis with him and for the valuable discussions and support during the preparation of this

thesis. Thank you to my other supervisor Julian Trillig for allowing me the opportunity to carry

out the work for my MSc Thesis at Technische Universität Darmstadt and for his support.

I would like to thank my family, specially my sister Laura, for their permanent support and for

encouraging me in moments of despair. I am very pleased and proud to belong to such a

family.

1

1. Introduction

Since 2007 the world economy is considered to be in a phase of marked instability1. The

Spanish economy has been affected by this instability mainly because of vulnerability to

changes in macroeconomic factors and the financial conditions of the imbalances amassed

during the ‘Boom period’ which were also vulnerable. The international financial crisis

precipitated the need to correct the real estate debt excess in both state and the private-

sector debt; which marked the growing phase which preceded the recession. The

deterioration of the macroeconomic scene and increasing unemployment has directly

damaged the public finances and the position of financial institutions, whose balance sheets

showed exposure to real state risk.

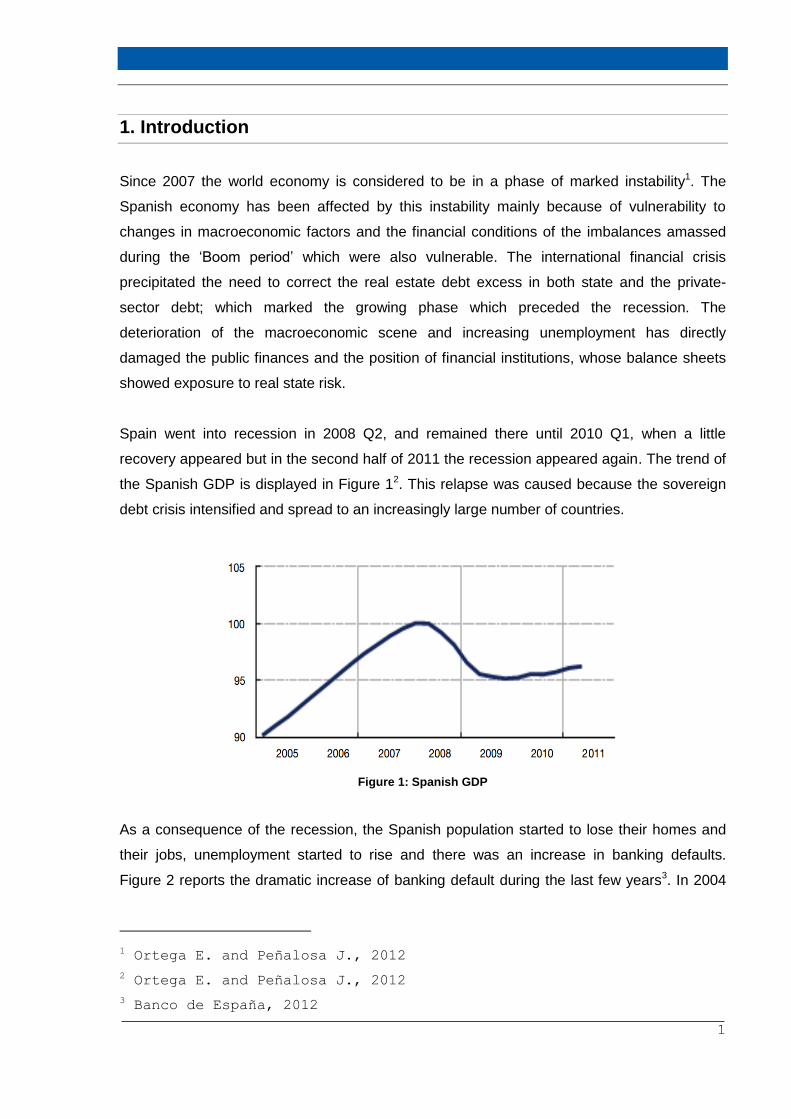

Spain went into recession in 2008 Q2, and remained there until 2010 Q1, when a little

recovery appeared but in the second half of 2011 the recession appeared again. The trend of

the Spanish GDP is displayed in Figure 12. This relapse was caused because the sovereign

debt crisis intensified and spread to an increasingly large number of countries.

Figure 1: Spanish GDP

As a consequence of the recession, the Spanish population started to lose their homes and

their jobs, unemployment started to rise and there was an increase in banking defaults.

Figure 2 reports the dramatic increase of banking default during the last few years3. In 2004

1 Ortega E. and Peñalosa J., 2012

2 Ortega E. and Peñalosa J., 2012

3 Banco de España, 2012

2

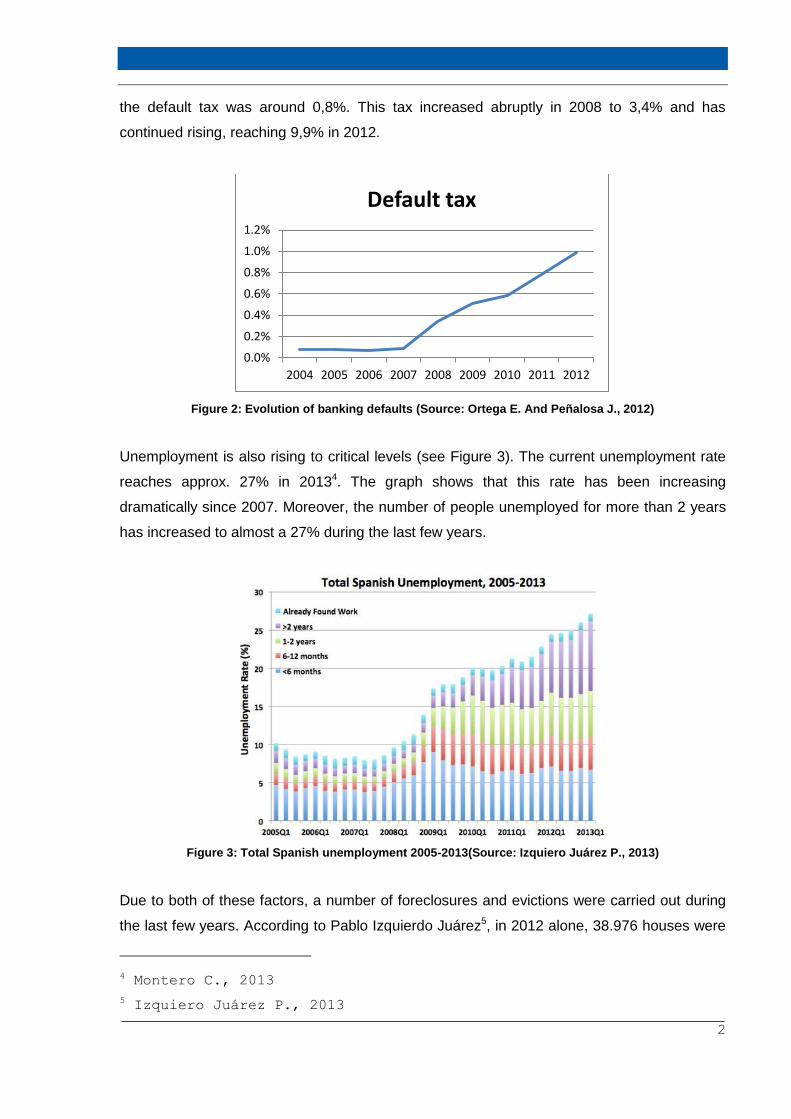

the default tax was around 0,8%. This tax increased abruptly in 2008 to 3,4% and has

continued rising, reaching 9,9% in 2012.

Figure 2: Evolution of banking defaults (Source: Ortega E. And Peñalosa J., 2012)

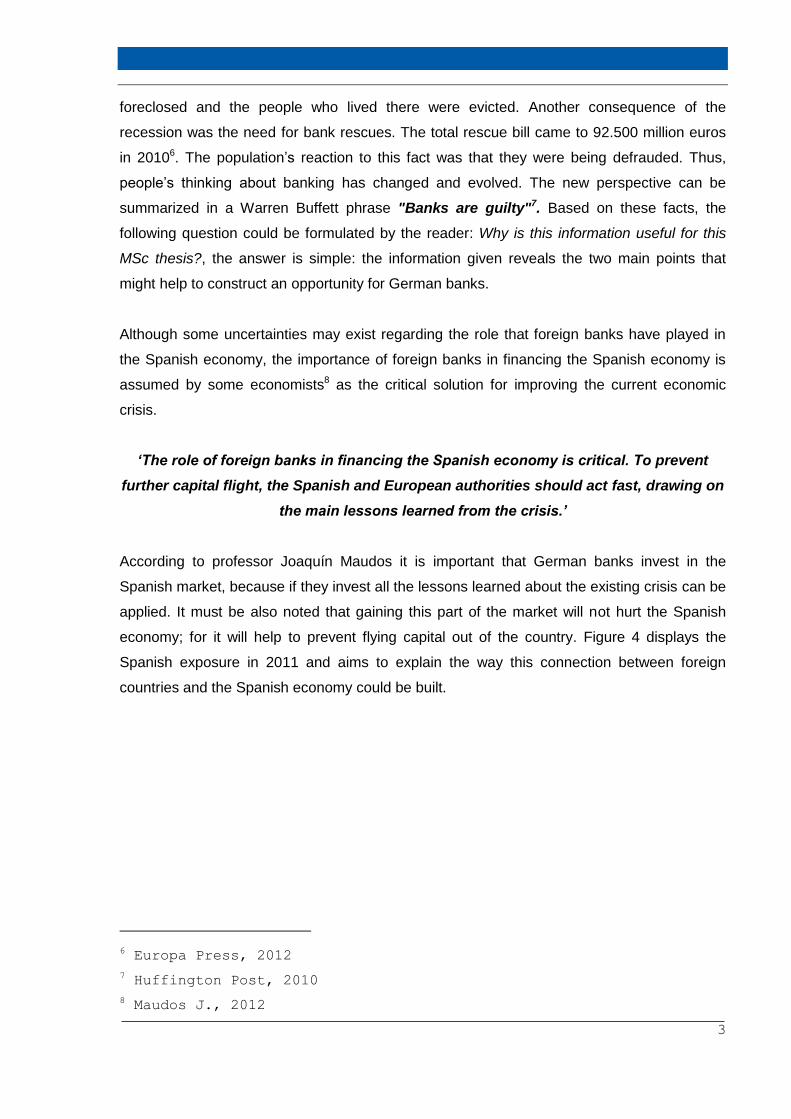

Unemployment is also rising to critical levels (see Figure 3). The current unemployment rate

reaches approx. 27% in 20134. The graph shows that this rate has been increasing

dramatically since 2007. Moreover, the number of people unemployed for more than 2 years

has increased to almost a 27% during the last few years.

Figure 3: Total Spanish unemployment 2005-2013(Source: Izquiero Juárez P., 2013)

Due to both of these factors, a number of foreclosures and evictions were carried out during

the last few years. According to Pablo Izquierdo Juárez5, in 2012 alone, 38.976 houses were

4 Montero C., 2013

5 Izquiero Juárez P., 2013

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2004 2005 2006 2007 2008 2009 2010 2011 2012

Default tax

3

foreclosed and the people who lived there were evicted. Another consequence of the

recession was the need for bank rescues. The total rescue bill came to 92.500 million euros

in 20106. The population’s reaction to this fact was that they were being defrauded. Thus,

people’s thinking about banking has changed and evolved. The new perspective can be

summarized in a Warren Buffett phrase "Banks are guilty"7. Based on these facts, the

following question could be formulated by the reader: Why is this information useful for this

MSc thesis?, the answer is simple: the information given reveals the two main points that

might help to construct an opportunity for German banks.

Although some uncertainties may exist regarding the role that foreign banks have played in

the Spanish economy, the importance of foreign banks in financing the Spanish economy is

assumed by some economists8 as the critical solution for improving the current economic

crisis.

‘The role of foreign banks in financing the Spanish economy is critical. To prevent

further capital flight, the Spanish and European authorities should act fast, drawing on

the main lessons learned from the crisis.’

According to professor Joaquín Maudos it is important that German banks invest in the

Spanish market, because if they invest all the lessons learned about the existing crisis can be

applied. It must be also noted that gaining this part of the market will not hurt the Spanish

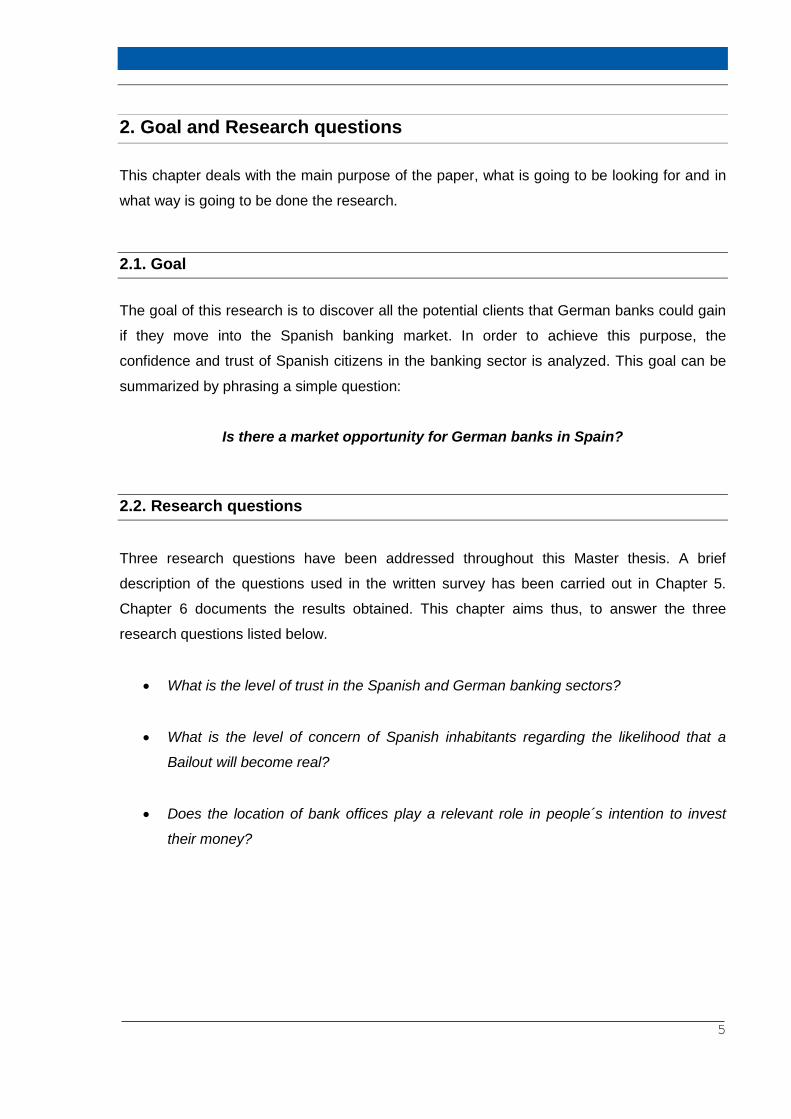

economy; for it will help to prevent flying capital out of the country. Figure 4 displays the

Spanish exposure in 2011 and aims to explain the way this connection between foreign

countries and the Spanish economy could be built.

6 Europa Press, 2012

7 Huffington Post, 2010

8 Maudos J., 2012

4

Figure 4: Foreign countries - Spanish exposure in percentage terms 2011

(Source: Maudos J., 2012)

Figure 4 reports that the exposure from German banks to the Spanish economy reaches

25.2%, being the foreign country with the highest exposure. Although this rate has been

reduced since 2011, the percentage is still around 20%, indicating the existing close

relationship between both countries in their financial environment. Thus, this research study

assumes that instead of eliminating this exposure, one of the best ways of rescuing the

Spanish economy is that German banks become a part of the Spanish market.

5

2. Goal and Research questions

This chapter deals with the main purpose of the paper, what is going to be looking for and in

what way is going to be done the research.

2.1. Goal

The goal of this research is to discover all the potential clients that German banks could gain

if they move into the Spanish banking market. In order to achieve this purpose, the

confidence and trust of Spanish citizens in the banking sector is analyzed. This goal can be

summarized by phrasing a simple question:

Is there a market opportunity for German banks in Spain?

2.2. Research questions

Three research questions have been addressed throughout this Master thesis. A brief

description of the questions used in the written survey has been carried out in Chapter 5.

Chapter 6 documents the results obtained. This chapter aims thus, to answer the three

research questions listed below.

What is the level of trust in the Spanish and German banking sectors?

What is the level of concern of Spanish inhabitants regarding the likelihood that a

Bailout will become real?

Does the location of bank offices play a relevant role in people´s intention to invest

their money?

6

3. Problem analysis and the banking industry

This chapter focuses on problem analysis, which includes loss of confidence in the Spanish

banking industry by inhabitants, the analysis of the banks in this country and capital flight.

Moreover, a brief description of the banking sector is presented.

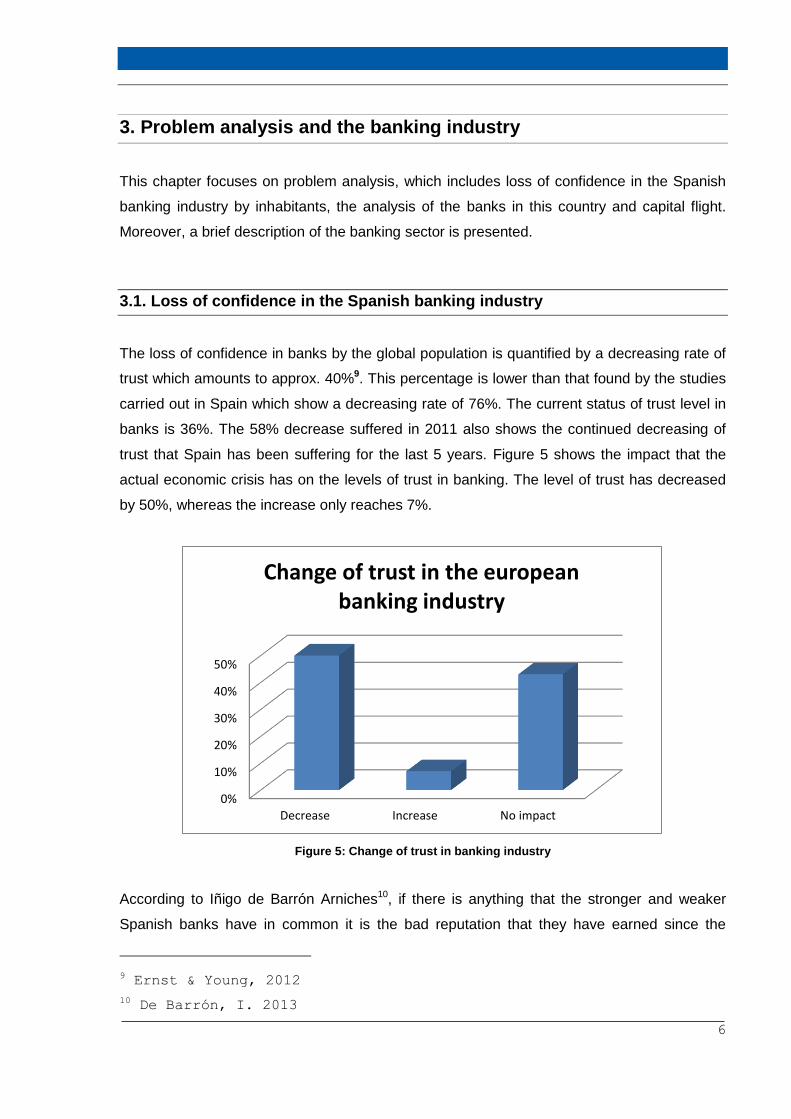

3.1. Loss of confidence in the Spanish banking industry

The loss of confidence in banks by the global population is quantified by a decreasing rate of

trust which amounts to approx. 40%9. This percentage is lower than that found by the studies

carried out in Spain which show a decreasing rate of 76%. The current status of trust level in

banks is 36%. The 58% decrease suffered in 2011 also shows the continued decreasing of

trust that Spain has been suffering for the last 5 years. Figure 5 shows the impact that the

actual economic crisis has on the levels of trust in banking. The level of trust has decreased

by 50%, whereas the increase only reaches 7%.

Figure 5: Change of trust in banking industry

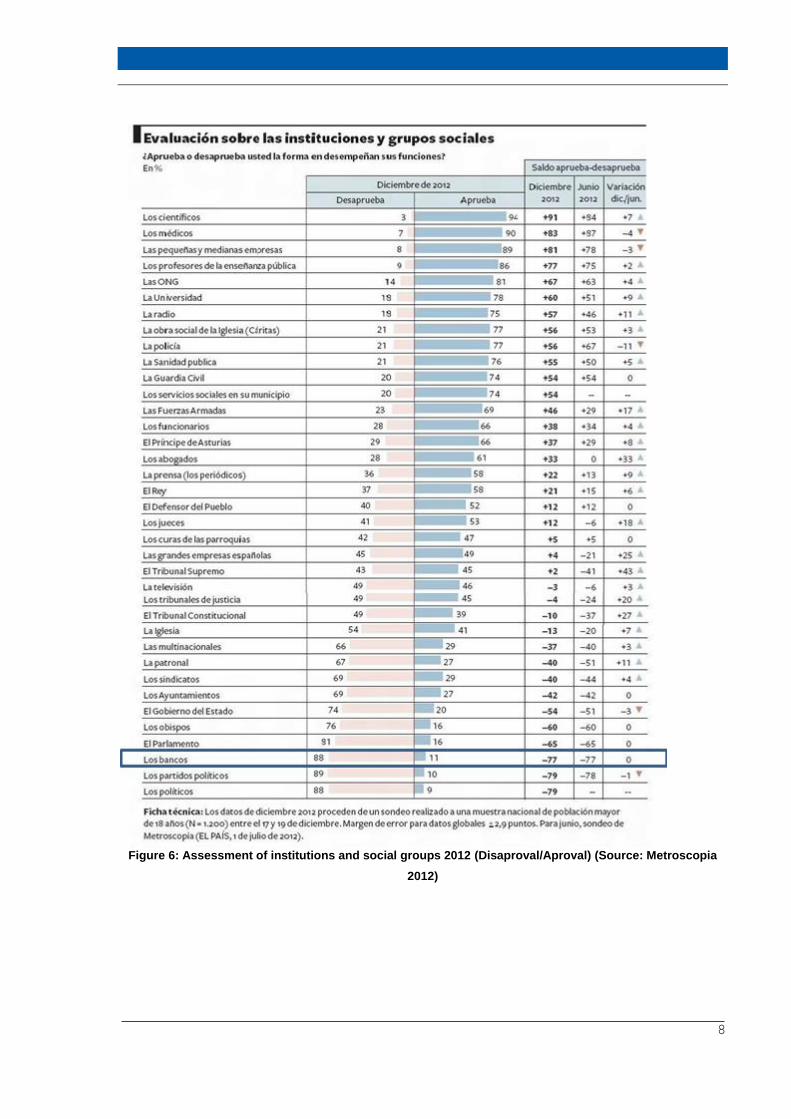

According to Iñigo de Barrón Arniches10, if there is anything that the stronger and weaker

Spanish banks have in common it is the bad reputation that they have earned since the

9 Ernst & Young, 2012

10 De Barrón, I. 2013

0%

10%

20%

30%

40%

50%

Decrease Increase No impact

Change of trust in the european banking industry

7

economic crisis started. The evidence that shows that their reputation is at its lowest level, is

the report that they appear as the second worse social valued institution for the first time in

history as reveled in the last Metroscopia survey of March 2013. It can be appreciated by

looking at Figure 6 that banks were disapproved of by 88% of people, which means a

decrease of approval of 11 percentage points during the year. This might open up an

opportunity for German banks to enter the Spanish banking market. Two main events have

damaged the image and reputation of the Spanish banking system bringing customers

perception to its lowest in history: the increasing number of evictions and investments in

preferential shares. Both events are described in the following sub-chapters.

8

Figure 6: Assessment of institutions and social groups 2012 (Disaproval/Aproval) (Source: Metroscopia

2012)

9

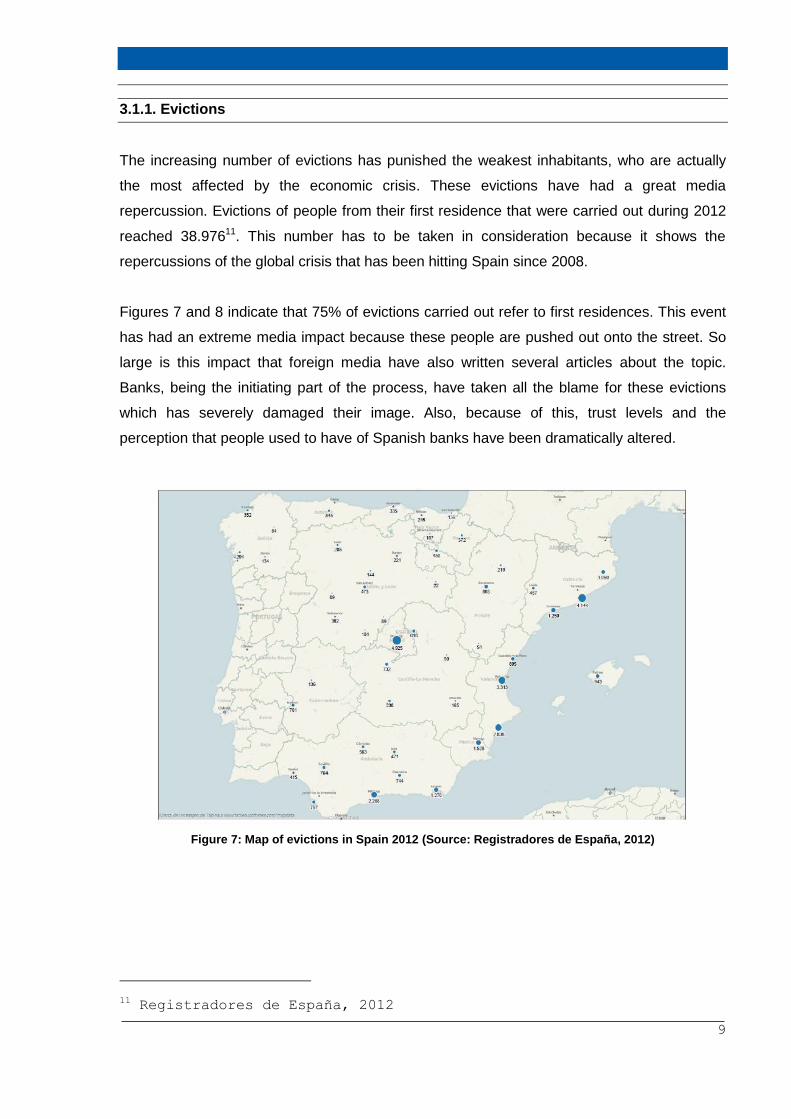

3.1.1. Evictions

The increasing number of evictions has punished the weakest inhabitants, who are actually

the most affected by the economic crisis. These evictions have had a great media

repercussion. Evictions of people from their first residence that were carried out during 2012

reached 38.97611. This number has to be taken in consideration because it shows the

repercussions of the global crisis that has been hitting Spain since 2008.

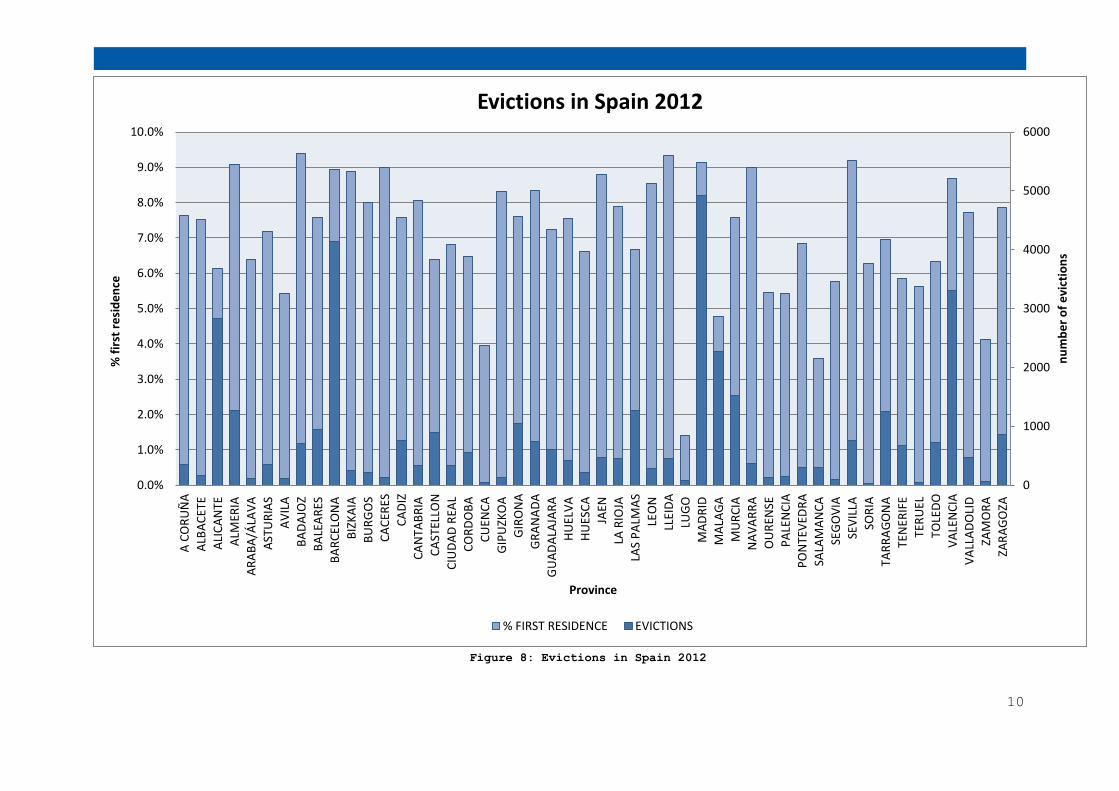

Figures 7 and 8 indicate that 75% of evictions carried out refer to first residences. This event

has had an extreme media impact because these people are pushed out onto the street. So

large is this impact that foreign media have also written several articles about the topic.

Banks, being the initiating part of the process, have taken all the blame for these evictions

which has severely damaged their image. Also, because of this, trust levels and the

perception that people used to have of Spanish banks have been dramatically altered.

Figure 7: Map of evictions in Spain 2012 (Source: Registradores de España, 2012)

11 Registradores de España, 2012

10

0

1000

2000

3000

4000

5000

6000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

A C

OR

UÑ

A

ALB

AC

ETE

ALI

CA

NTE

ALM

ERIA

AR

AB

A/Á

LAV

A

AST

UR

IAS

AV

ILA

BA

DA

JOZ

BA

LEA

RES

BA

RC

ELO

NA

BIZ

KA

IA

BU

RG

OS

CA

CER

ES

CA

DIZ

CA

NTA

BR

IA

CA

STEL

LON

CIU

DA

D R

EAL

CO

RD

OB

A

CU

ENC

A

GIP

UZK

OA

GIR

ON

A

GR

AN

AD

A

GU

AD

ALA

JAR

A

HU

ELV

A

HU

ESC

A

JAEN

LA R

IOJA

LAS

PA

LMA

S

LEO

N

LLEI

DA

LUG

O

MA

DR

ID

MA

LAG

A

MU

RC

IA

NA

VA

RR

A

OU

REN

SE

PA

LEN

CIA

PO

NTE

VED

RA

SALA

MA

NC

A

SEG

OV

IA

SEV

ILLA

SOR

IA

TAR

RA

GO

NA

TEN

ERIF

E

TER

UEL

TOLE

DO

VA

LEN

CIA

VA

LLA

DO

LID

ZAM

OR

A

ZAR

AG

OZA

nu

mb

er

of

evi

ctio

ns

% f

irst

re

sid

en

ce

Province

Evictions in Spain 2012

% FIRST RESIDENCE EVICTIONS

Figure 8: Evictions in Spain 2012

11

Both Figures show that the greatest number of evictions is carried out in the major cities,

Madrid and Barcelona. The main reason for this was the huge growth of real estate during the

pre-crisis period. Hence, when the crisis hit the Spanish economy, these cities were the most

at risk. Moreover, Valencia’s community has become the most damaged province because

this province was the main focus of real estate investments.12

Figure 9: Article informing about evictions in Spain (Source: Daley S., 2012)

12 Daley S., 2012

12

3.1.2. Preferential shares

The investments in preferential shares has also damaged de image of the Spanish banking

system. This has mainly been caused by the great losses incurred associated with the

reduction of share value, leading to a huge loss of money by smaller savers. It must be noted

that the problem is not the amount of money that the savers have lost, the problem resides in

the way those shares were sold. The shares were sold as a safe place to deposits money

without explaining the risk that these kinds of shares have. This event has had a large media

impact in Spain but not outside the country. This means that the bad banking behavior

surrounding this issue has damaged only the image of Spanish banks within the country and

is not an extended perception.

Figure 10: Preferential shares demonstration in Spain13

(Source: Ruiz J., 2013)

Customer’s perception about the purpose of banking has changed leading it towards a

distrustful attitude. In conclusion, this can be confirmed as, regarding the selling of

preferential shares that banks generally sell what is interesting for the bank and not

necessarily what is best for the customer14.

13 Ruiz J., 2013

14 De Barrón, I. 2013

13

3.2. Client attitude

Customer attitude towards their relationship with banks has changed since the economic

crisis started. Literature highlights15 that their attitude has evolved into a renewed one:

“The client is cautious, smart, less trusting and loyal, and now demanding better

service and clearer value”

Cautious, less trusting and less loyal are the three key points to be considered as important

when analysing the study results. These attitudes should be the key for opening the Spanish

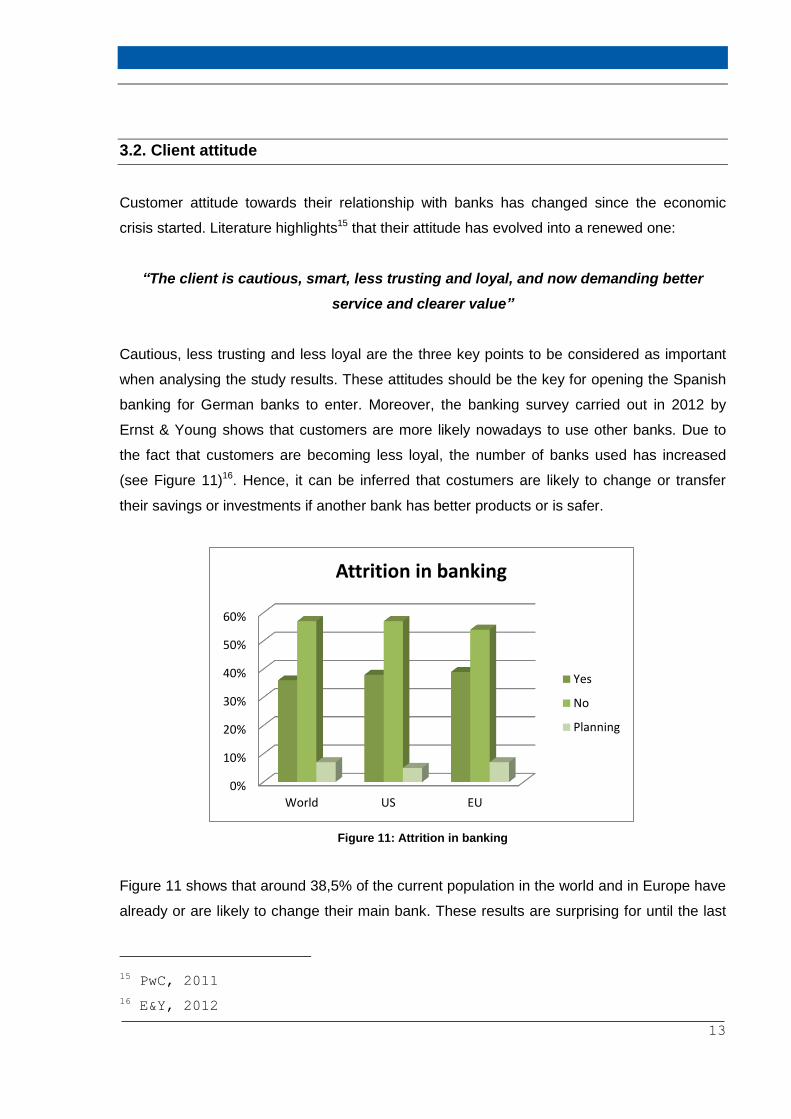

banking for German banks to enter. Moreover, the banking survey carried out in 2012 by

Ernst & Young shows that customers are more likely nowadays to use other banks. Due to

the fact that customers are becoming less loyal, the number of banks used has increased

(see Figure 11)16. Hence, it can be inferred that costumers are likely to change or transfer

their savings or investments if another bank has better products or is safer.

Figure 11: Attrition in banking

Figure 11 shows that around 38,5% of the current population in the world and in Europe have

already or are likely to change their main bank. These results are surprising for until the last

15 PwC, 2011

16 E&Y, 2012

0%

10%

20%

30%

40%

50%

60%

World US EU

Attrition in banking

Yes

No

Planning

14

few years the rate of changing banks was really low. However, due to the fact that this

willingness to change banks exists, a question should be formulated:

Why are people changing banks?

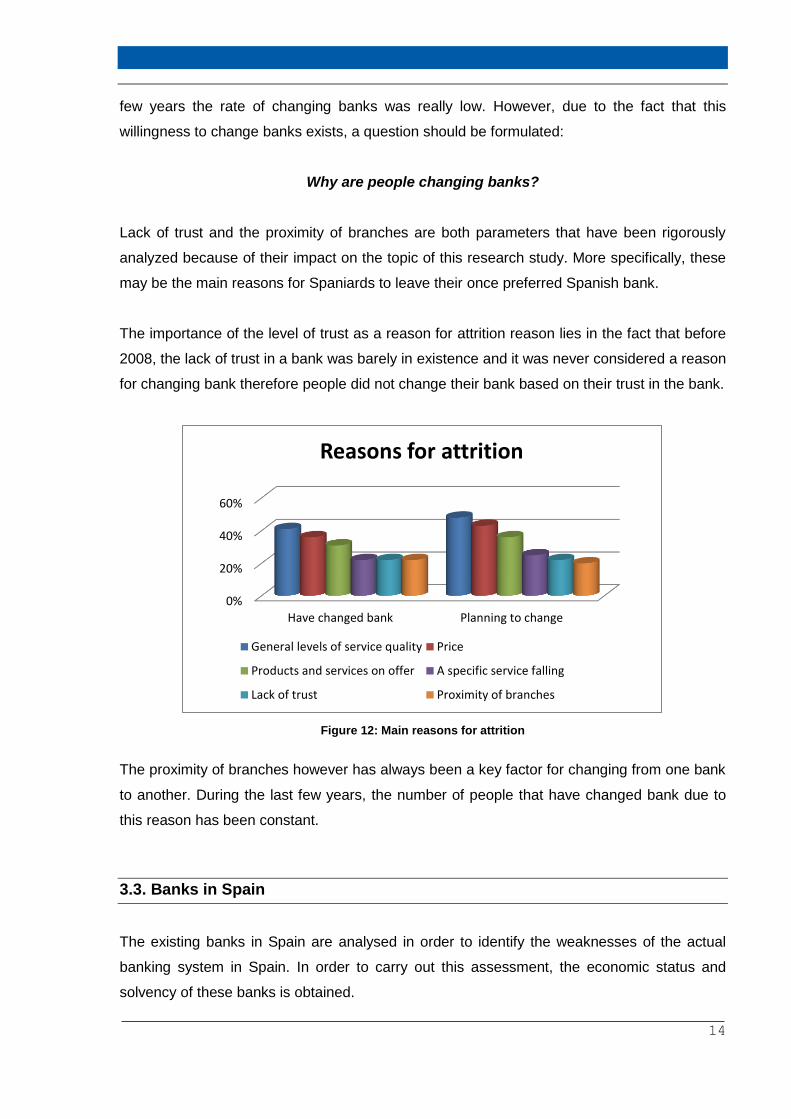

Lack of trust and the proximity of branches are both parameters that have been rigorously

analyzed because of their impact on the topic of this research study. More specifically, these

may be the main reasons for Spaniards to leave their once preferred Spanish bank.

The importance of the level of trust as a reason for attrition reason lies in the fact that before

2008, the lack of trust in a bank was barely in existence and it was never considered a reason

for changing bank therefore people did not change their bank based on their trust in the bank.

Figure 12: Main reasons for attrition

The proximity of branches however has always been a key factor for changing from one bank

to another. During the last few years, the number of people that have changed bank due to

this reason has been constant.

3.3. Banks in Spain

The existing banks in Spain are analysed in order to identify the weaknesses of the actual

banking system in Spain. In order to carry out this assessment, the economic status and

solvency of these banks is obtained.

0%

20%

40%

60%

Have changed bank Planning to change

Reasons for attrition

General levels of service quality Price

Products and services on offer A specific service falling

Lack of trust Proximity of branches

15

Figure 13 displays the current market share of the Spanish banks in terms of Spanish assets.

This chart states that Santander, BBVA, Caixabank and Bankia are the four main banks in

Spain controlling more than 60% of total Spanish assets. Alternatively, the rest of the banks

have relatively small market share.

Figure 13: Market share in Spain in 2012 (Source: Horwood C., 2012)

Although these four banks have the major assets of the Spanish banking market, these main

banks have a BBB+ or BBB rating according to Fitch’s long term rating. This rating means

that they are a medium class company, which is satisfactory at the moment. These rates

should not be shocking or surprising; however, since Santander has been awarded the title of

best bank of the world in 2012 by Euromoneys17 It is kind of surprising that the best bank in

the world has a BBB+ rating instead of a AAA rating. Moreover, CaixaBank has been given

the award for being as the best bank in Spain in 2012 by Euromoneys but the bank has a

17 Horwood C., 2012

1.9%

1.5%

1.2% 1.2%

0.6%

0.6%

0.4%

0.3% 0.3%

0.3% 0.3% 0.2% 0.2% 0.1%

Market share (% of Spanish assets)

Santander (incl. Banesto) BBVA (incl. UNNIM)

Caixabank (incl. Banca Cívica) BFA-Bankia

Banc Sabadell (incl. CAM) Popular (incl. Pastor)

Libercaja (Ibercaja - Caja 3 – Liberbank) Unicaja – CEISS

Kutxabank Catalunyabanc

NCG Banco BMN

Bankinter Banco de Valencia

16

BBB rating. It is surprising that the best banks in the world even though they are in Spain

have low ratings. This study assumes that a specific reason exists for such a low rating. In

order to get an explanation a question is formulated:

Which problems do Spanish banks have?

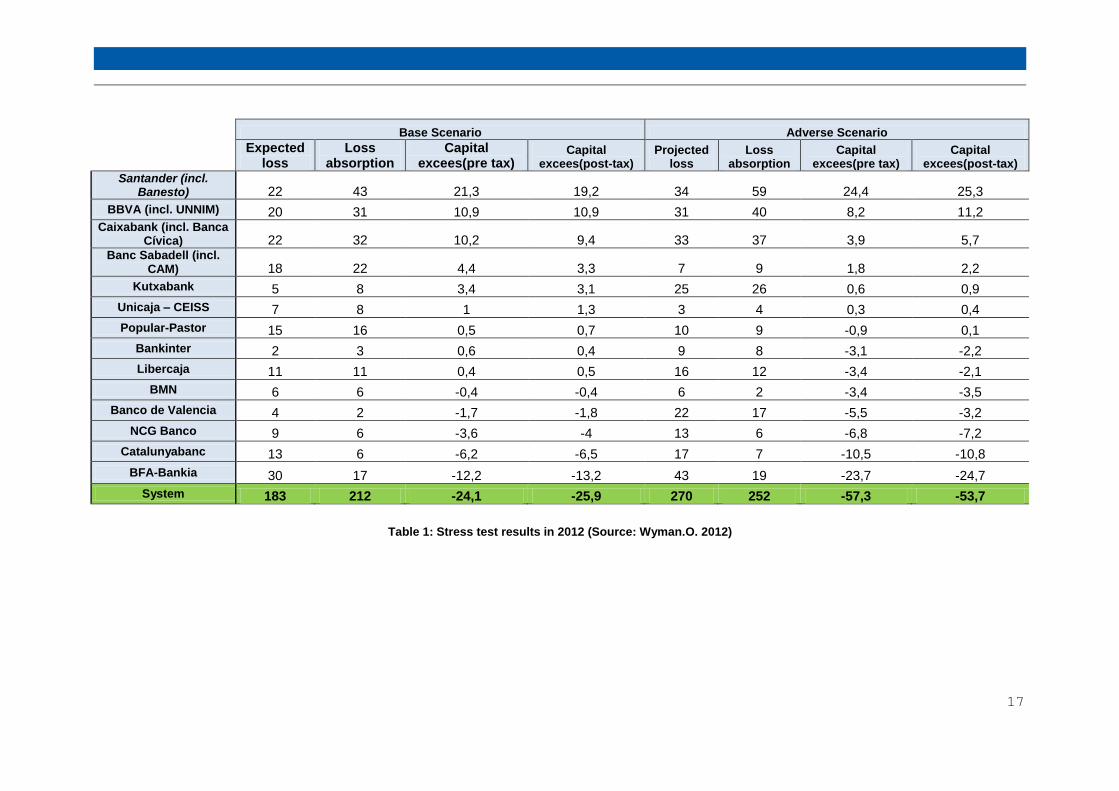

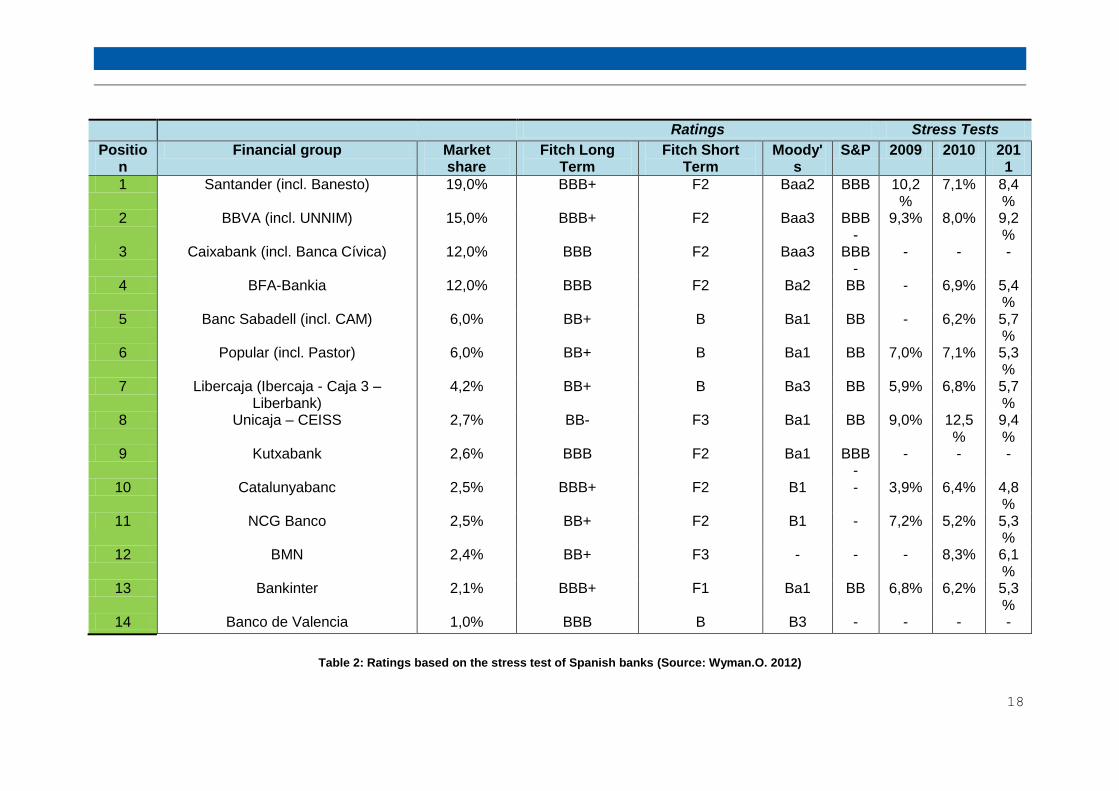

Figures 14 and 15 report the findings of the stress test done by Oliver Wyman18 in 2012 about

the Spanish banking sector and their capital needs. Crossing both figures is the problematic

picture that Bankia brings to the Spanish banking market: a bank with a 12% share of the

total Spanish Market but with a capital need of 13.200 million euros in a Base scenario or

24.700 million euros in an adverse scenario. Moreover, Bankia is the bank with the largest

number of preferential shares that have been sold to clients, thus, it can be assumed that

Bankia is the black sheep of the Spanish Bank system. Only three banks have no need for

additional capital, Santander, Caixabank and BBVA. The direct consequence of this image

problem leading to the expectation, for instance, of the need of rescue, that faces a high

number of banks is that Spaniards have lost their trust in the Spanish banking system.

18 Wyman O., 2012

17

Base Scenario Adverse Scenario

Expected loss

Loss absorption

Capital excees(pre tax)

Capital excees(post-tax)

Projected loss

Loss absorption

Capital excees(pre tax)

Capital excees(post-tax)

Santander (incl. Banesto) 22 43 21,3 19,2 34 59 24,4 25,3

BBVA (incl. UNNIM) 20 31 10,9 10,9 31 40 8,2 11,2 Caixabank (incl. Banca

Cívica) 22 32 10,2 9,4 33 37 3,9 5,7 Banc Sabadell (incl.

CAM) 18 22 4,4 3,3 7 9 1,8 2,2

Kutxabank 5 8 3,4 3,1 25 26 0,6 0,9

Unicaja – CEISS 7 8 1 1,3 3 4 0,3 0,4

Popular-Pastor 15 16 0,5 0,7 10 9 -0,9 0,1

Bankinter 2 3 0,6 0,4 9 8 -3,1 -2,2

Libercaja 11 11 0,4 0,5 16 12 -3,4 -2,1

BMN 6 6 -0,4 -0,4 6 2 -3,4 -3,5

Banco de Valencia 4 2 -1,7 -1,8 22 17 -5,5 -3,2

NCG Banco 9 6 -3,6 -4 13 6 -6,8 -7,2

Catalunyabanc 13 6 -6,2 -6,5 17 7 -10,5 -10,8

BFA-Bankia 30 17 -12,2 -13,2 43 19 -23,7 -24,7

System 183 212 -24,1 -25,9 270 252 -57,3 -53,7

Table 1: Stress test results in 2012 (Source: Wyman.O. 2012)

18

Ratings Stress Tests

Position

Financial group Market share

Fitch Long Term

Fitch Short Term

Moody's

S&P 2009 2010 2011

1 Santander (incl. Banesto) 19,0% BBB+ F2 Baa2 BBB 10,2%

7,1% 8,4%

2 BBVA (incl. UNNIM) 15,0% BBB+ F2 Baa3 BBB-

9,3% 8,0% 9,2%

3 Caixabank (incl. Banca Cívica) 12,0% BBB F2 Baa3 BBB-

- - -

4 BFA-Bankia 12,0% BBB F2 Ba2 BB - 6,9% 5,4%

5 Banc Sabadell (incl. CAM) 6,0% BB+ B Ba1 BB - 6,2% 5,7%

6 Popular (incl. Pastor) 6,0% BB+ B Ba1 BB 7,0% 7,1% 5,3%

7 Libercaja (Ibercaja - Caja 3 – Liberbank)

4,2% BB+ B Ba3 BB 5,9% 6,8% 5,7%

8 Unicaja – CEISS 2,7% BB- F3 Ba1 BB 9,0% 12,5%

9,4%

9 Kutxabank 2,6% BBB F2 Ba1 BBB-

- - -

10 Catalunyabanc 2,5% BBB+ F2 B1 - 3,9% 6,4% 4,8%

11 NCG Banco 2,5% BB+ F2 B1 - 7,2% 5,2% 5,3%

12 BMN 2,4% BB+ F3 - - - 8,3% 6,1%

13 Bankinter 2,1% BBB+ F1 Ba1 BB 6,8% 6,2% 5,3%

14 Banco de Valencia 1,0% BBB B B3 - - - -

Table 2: Ratings based on the stress test of Spanish banks (Source: Wyman.O. 2012)

19

3.4. Capital flight

Flight of capital19 out of the country has become an issue for the Spanish economy. Since

2004, the increasing number of capital transfers has damaged the national economy.

However, this exodus has not hit bottom yet. One alternative option could be that instead of

fighting for the money or capital that is currently leaving Spain, foreign banks should be

encouraged to enter in Spanish market. It could be prove to be a great opportunity for all

players in the market.

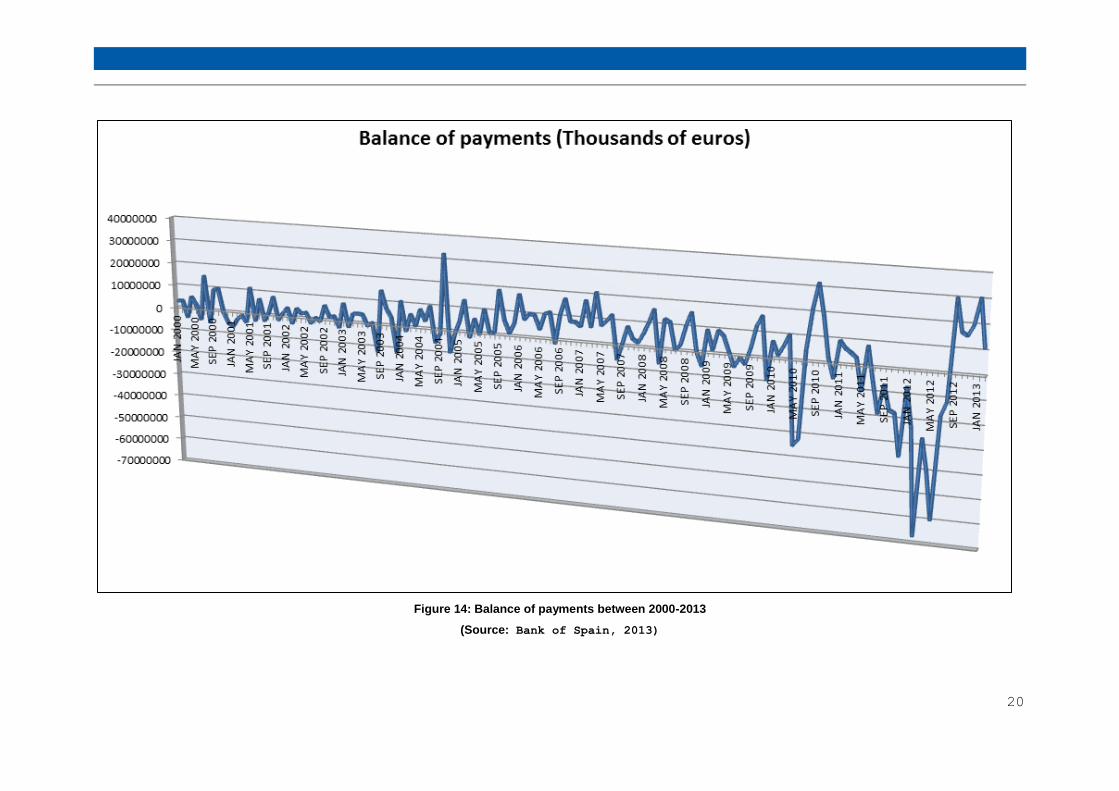

Figure 16 shows that between 2000 and 2005 there was regulation between capital both

incoming and outgoing and thus, the balance between them was approximately 0.

Subsequently, from September 2004 till September 2007 incoming capital was higher than

outgoing, which means that foreigners were transferring to and investing in the Spanish

market system. However, from September 2007 till May 2010 the negative fluctuations have

appeared more frequently and with a higher impact so that private capital was starting to

move away from Spain. This considerable deterioration in the situation was stopped by the

little money injections put by the European Union. However, from May 2010 until today capital

flight has become a great matter of importance. As Figure 16 shows, it has continued to be a

negative trend which means that capital flight has become a reality, and no monetary help

from Europe has been able to stop it.

The worst year in terms of capital flight was 2012, reaching a total amount of 223.400 million

euros from April 2011 till the end of 2012. This huge amount of money has been transferred

to foreign countries where the solvency of those countries and their banking system was not

in question.

19 Bank of Spain, 2013

20

Figure 14: Balance of payments between 2000-2013

(Source: Bank of Spain, 2013)

21

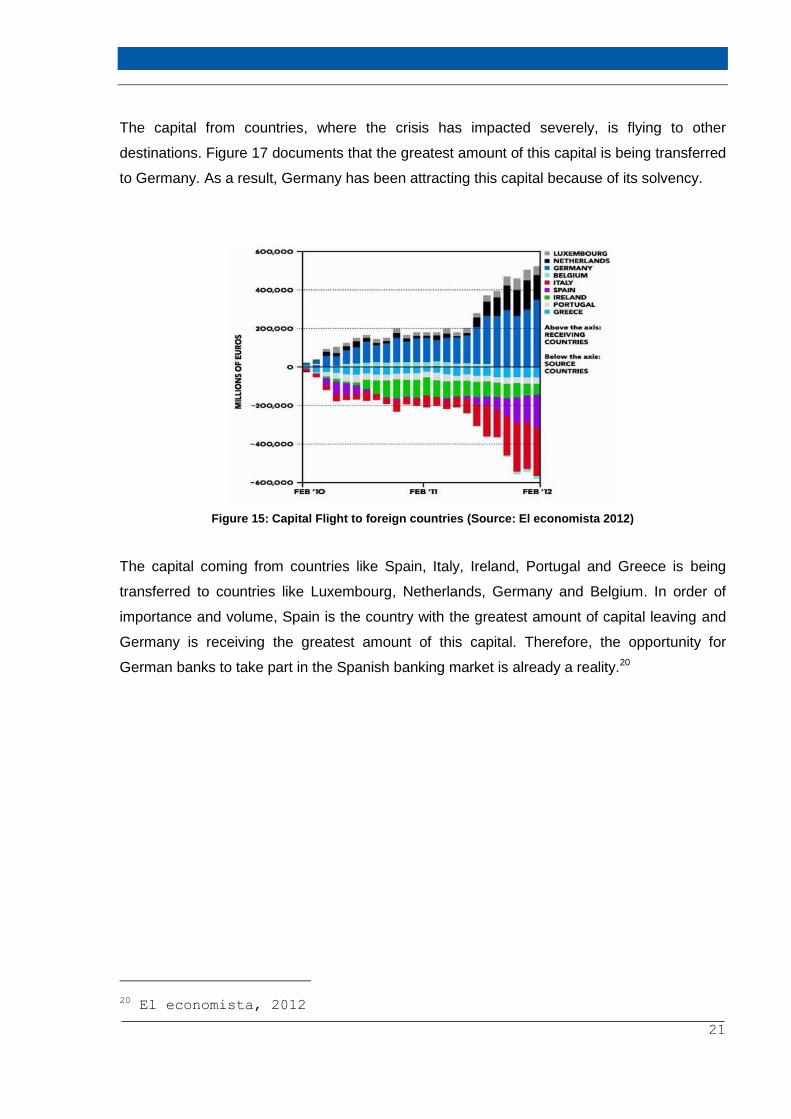

The capital from countries, where the crisis has impacted severely, is flying to other

destinations. Figure 17 documents that the greatest amount of this capital is being transferred

to Germany. As a result, Germany has been attracting this capital because of its solvency.

Figure 15: Capital Flight to foreign countries (Source: El economista 2012)

The capital coming from countries like Spain, Italy, Ireland, Portugal and Greece is being

transferred to countries like Luxembourg, Netherlands, Germany and Belgium. In order of

importance and volume, Spain is the country with the greatest amount of capital leaving and

Germany is receiving the greatest amount of this capital. Therefore, the opportunity for

German banks to take part in the Spanish banking market is already a reality.20

20 El economista, 2012

22

4. Main Activities and the methodological approach to research

Chapter 4 aims to make a brief analysis of people’s perceptions and feelings. Moreover, data

gathering methods are specified according to the specific goal of each research question.

Finally, any limitations encountered during the preparation of this MSc Thesis are presented

in this chapter.

4.1. Analysis of people’s feelings and perceptions

People’s perceptions, including thoughts, feelings and intentions, as well as social

characteristics have a considerable influence on their savings and investments. Thus, the

successful entry of a German bank to Spain, is subject to people’s perceptions. Levels of

trust depend largely on the quantity and quality of available information that people have and

on the difference in people’s perceptions of risk.21

In order to identify this range of perceptions and awareness, multiple social questions are

addressed in the survey. First there is a question regarding Spain and Germany, followed by

the identification of current perceptions about both banking systems. From the answers, the

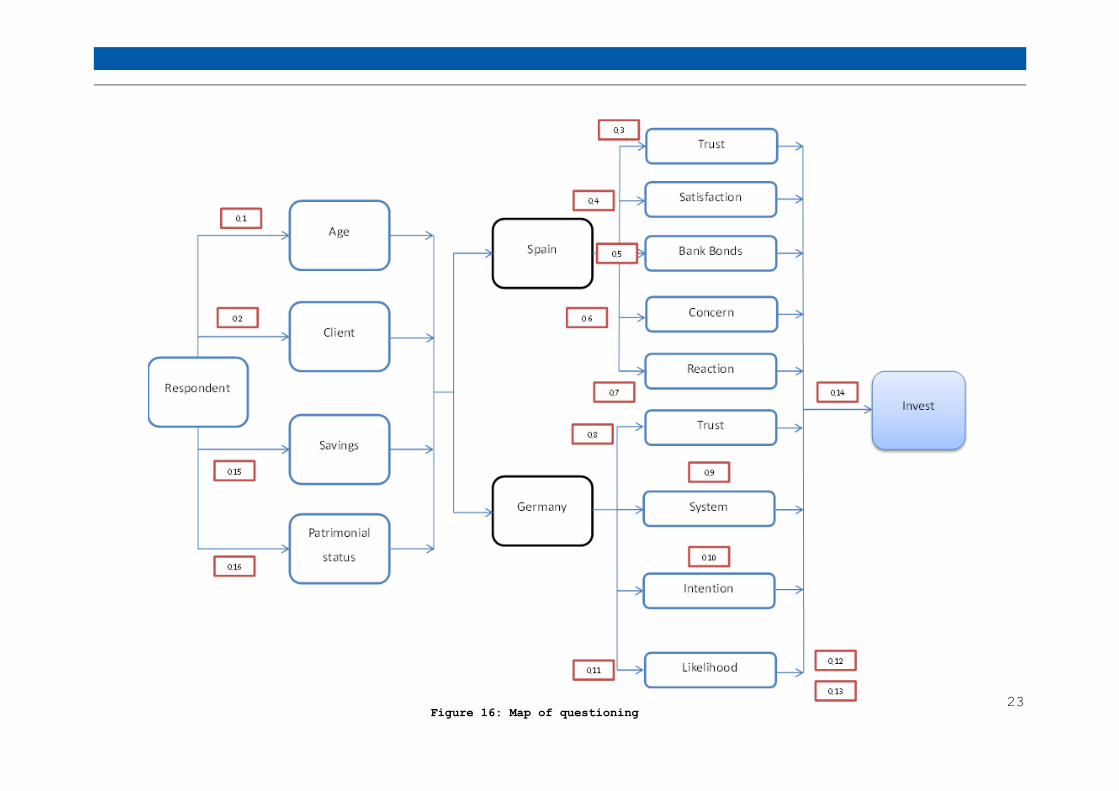

result of an irruption of a German bank into Spain can be predicted. Therefore, the map of

questioning is displayed in Figure 16, and is extensively addressed in Chapter 5, in order to

get a brighter view of the line of questions that are included in the survey. Note that the QX

questions are referred to by their position in the survey.

21 KpmG, 2012

23

Figure 16: Map of questioning

24

4.2. Main activities

This subchapter aims to list the specific activities that are carried out in order to answer the

research questions.

Research question 1: What is the level of trust in the Spanish and German banking sectors?

Activities carried out:

Literature review of banking surveys

Identification of the main reasons for the loss of trust in the Spanish banking sector.

Specific questions in the survey referring to the actual perceptions of Spanish

banking.

Analysis of the results obtained from the survey.

The literature review regarding banking surveys has been obtained by searching publications

from the big four consulting enterprises: Ernst & Young, PwC, KPMG and Deloitte. It has

taken into account the last three years of surveys. The reasons for loss of trust have been

identified through extensive research including publications from economic agencies and

newspapers. Specific questions in the survey have been obtained from reading the

mentioned information and assessing it against goals of the project.

Research question 2: What is the level of concern of Spanish inhabitants regarding the

likelihood that a Bailout will become real?

Activities carried out:

Literature review about strikes, preferential shares, flying capital and all the different

variables that have shown individual and societal fear about the loss of money.

Analysis of people’s perceptions and experiences

Identification of the facts that make the Spanish banking system weak.

Quantification of the different variables within the survey

Analysis of different people’s attitudes towards confidence in the Spanish banking

system

The activities carried out are mainly focused in people’s perceptions and knowledge. In order

to get clear information, four filter questions have been introduced into the survey defining the

responder’s economic status and therefore allowing the researcher to recognize the different

behaviors depending on the amount of money invested. Literature research has been carried

25

out using newspapers and private consultants’ publications. Newspapers have shown the

impact that media have had on fear and on the impact of the economic crisis in people’s

confidence. Additionally, private consultants have shown the measurable reactions of this

fear by using several quantification methods.

Research question 3: Does the location of bank offices play a relevant role in people´s

intention to invest their money?

Activities carried out:

Literature review about the banking system and all the customers’ surveys done by

the consulting enterprises.

Analysis of people’s wants about their relationship with banking.

Direct questioning through survey about the main reasons for working with a bank

Analyzing the variables that have come out of the survey

The literature review has shown a lot of different points that the new client or evolved client

has earned and has identified the way to get to those clients. The proximity of branches has

come to be identified as an importance decision making factor when it comes to working with

a bank and other variables have come to light to show that people’s wants have to be met

before getting new clients can be a reality.

26

4.3. Data collection methods

A number of methods have been employed for data collection for this MSc thesis. The

general approach is qualitative and involves the methods listed below:

Literature reviews

Searches of the internet

Direct contact with Spaniards through written surveys

This research assumes that the best way to identify people’s intentions regarding their

investment approaching is achieved by carrying out a closed survey and by analyzing out

coming results. A large number of media are used for delivering surveys; however this MSc

Thesis focuses on face-to-face written questioners. Moreover, literature review and searches

of the internet have been also considered as assessment tools as they can provide valuable

background information.

Although it could be easily assumed that written surveys are just questionnaires, developing a

survey includes instructions for the procurement of standardized information from a targeted

sample, for the formulation of questions, for assessing the answers in order to identify the

most relevant points, amongst all the others.

According to Kraemer (1991)22, the three main characteristics that should be addressed in

surveys are the following:

1. The survey research is being used to quantitatively describe specific aspects of a

given population, this needs to be identified

2. Data are gathered from people therefore, they are subjective.

3. A selected portion of the population is used from which the findings can later be

generalized back to the whole population.

The construction of a written survey consists of two steps. The first step should be the

development of a sampling plan followed by the definition of the expected population

estimation and its reliability. The sampling plan makes a description of the approach that is

used to select the sample that would be used to determine the size of the sample and the

communication media for delivering the surveys.

22 Glasow P., 2005

27

Since surveys are carried out to collect information, it is essential to identify the information

that is required for the study and thus, this must be considered when designing the questions

to be used in the survey. In order to collect information, two different types of questions can

be used: open-ended questions and closed-ended questions. The difference between open

and closed questions lies in the formulation of the answer. In closed questions, the recipient

receives a list of possible responses. In open questions the possible response list disappears

and the responder answers with whatever seems desirable. In order to get a more in-depth

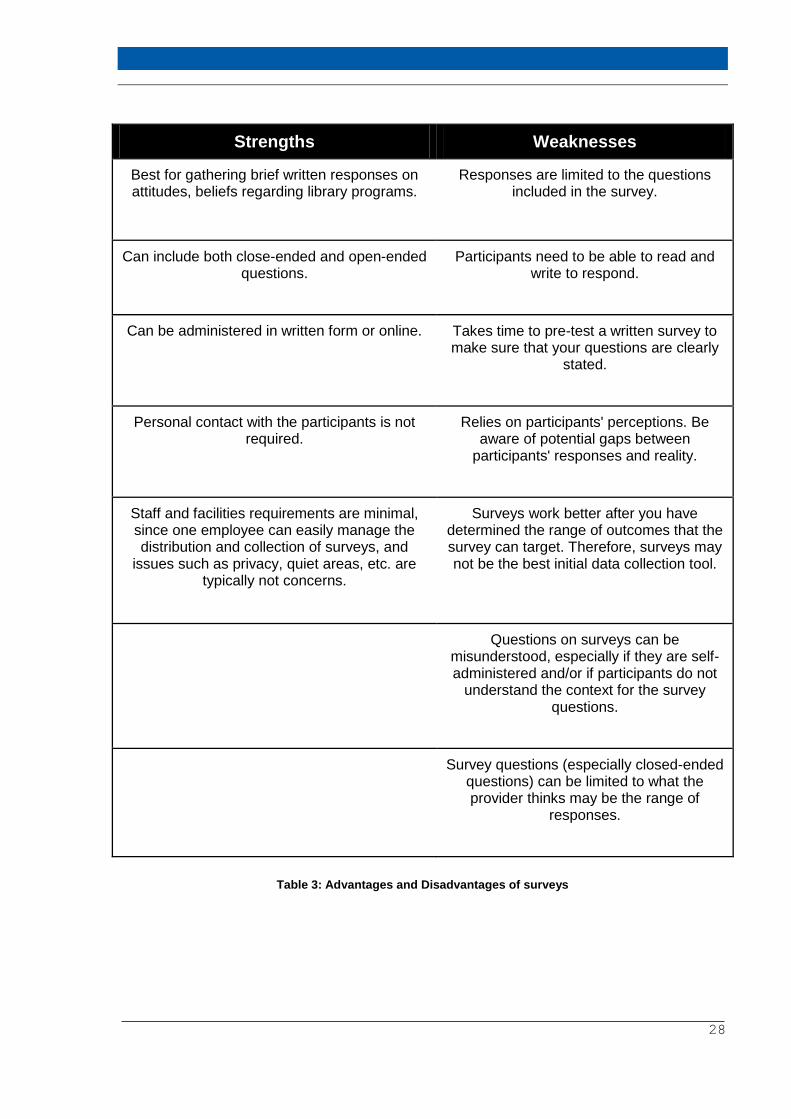

view of the field of research surveys, an evaluation23 of the weaknesses and strengths of a

written survey is displayed in Table 3.

23 Joan C. and Fisher K., 2005

28

Strengths Weaknesses

Best for gathering brief written responses on attitudes, beliefs regarding library programs.

Responses are limited to the questions included in the survey.

Can include both close-ended and open-ended questions.

Participants need to be able to read and write to respond.

Can be administered in written form or online.

Takes time to pre-test a written survey to make sure that your questions are clearly

stated.

Personal contact with the participants is not required.

Relies on participants' perceptions. Be aware of potential gaps between

participants' responses and reality.

Staff and facilities requirements are minimal, since one employee can easily manage the distribution and collection of surveys, and

issues such as privacy, quiet areas, etc. are typically not concerns.

Surveys work better after you have determined the range of outcomes that the survey can target. Therefore, surveys may not be the best initial data collection tool.

Questions on surveys can be misunderstood, especially if they are self-administered and/or if participants do not

understand the context for the survey questions.

Survey questions (especially closed-ended questions) can be limited to what the provider thinks may be the range of

responses.

Table 3: Advantages and Disadvantages of surveys

29

4.4. Limitations of the study

The main constraint of this MSc Thesis is the lack of research studies about people´s

perceptions and attitudes regarding the current banking system. The small number of existing

studies focuses on the relation between client and banks and do they not consider as

relevant the trust and confidence in the banking system. A further important gap in this MSc

thesis is the reduced number of people who have answered the written survey, reaching

approx. 120 responders. An acceptable representative sample in the city of Tarragona

according to a 5% of margin error and with a 95% of confidence level should be around 400

inhabitants. However, due to the lack of time, the results of this MSc thesis should be only

considered as a trending analysis.

30

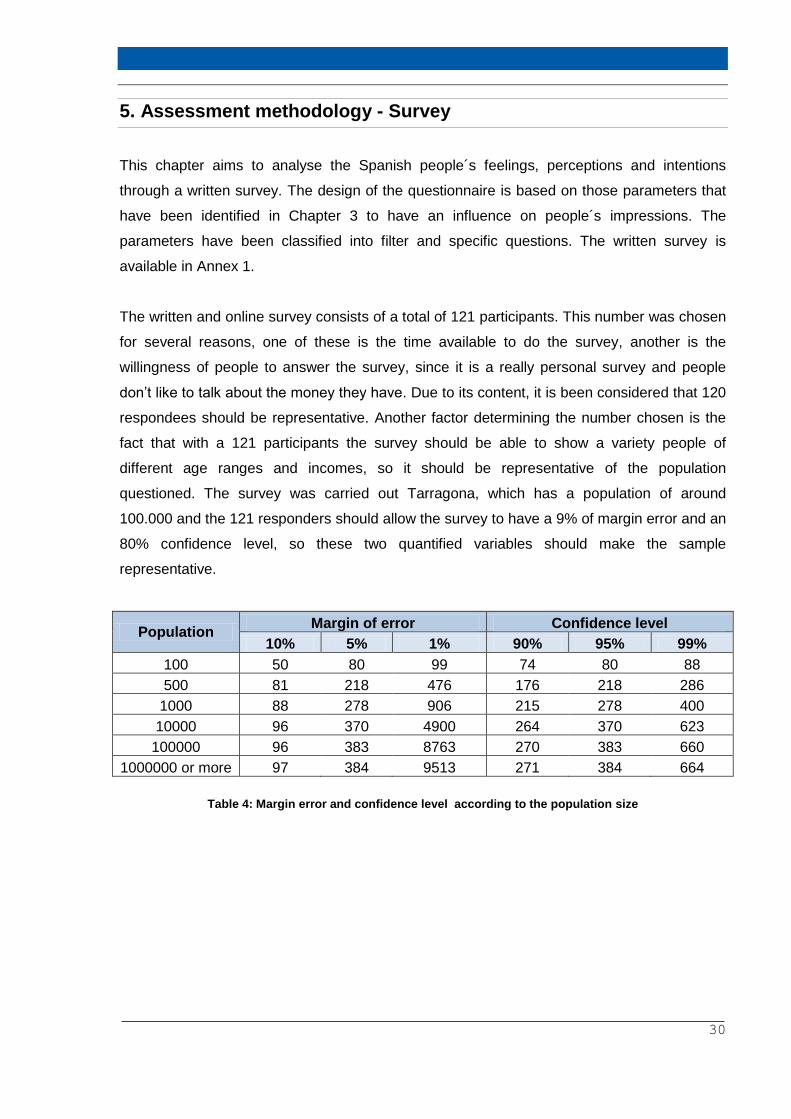

5. Assessment methodology - Survey

This chapter aims to analyse the Spanish people´s feelings, perceptions and intentions

through a written survey. The design of the questionnaire is based on those parameters that

have been identified in Chapter 3 to have an influence on people´s impressions. The

parameters have been classified into filter and specific questions. The written survey is

available in Annex 1.

The written and online survey consists of a total of 121 participants. This number was chosen

for several reasons, one of these is the time available to do the survey, another is the

willingness of people to answer the survey, since it is a really personal survey and people

don’t like to talk about the money they have. Due to its content, it is been considered that 120

respondees should be representative. Another factor determining the number chosen is the

fact that with a 121 participants the survey should be able to show a variety people of

different age ranges and incomes, so it should be representative of the population

questioned. The survey was carried out Tarragona, which has a population of around

100.000 and the 121 responders should allow the survey to have a 9% of margin error and an

80% confidence level, so these two quantified variables should make the sample

representative.

Population Margin of error Confidence level

10% 5% 1% 90% 95% 99%

100 50 80 99 74 80 88

500 81 218 476 176 218 286

1000 88 278 906 215 278 400

10000 96 370 4900 264 370 623

100000 96 383 8763 270 383 660

1000000 or more 97 384 9513 271 384 664

Table 4: Margin error and confidence level according to the population size

31

5.1. Filter questions

5.1.1. Age range

The first question is a filter question that allowed 3 groups of people to be categorized, and

thus the results were disaggregated into these three groups. The main reason for making this

filter is because banks sort their customers into these three big groups: young people, adults

and old people.

Young People (18-26)

This category includes all types of young people from workers to students; the expected

results are low income per year, and few capital investments.

Adults (26-65)

Adults are the group that involves all type of workers and the unemployed. Their range of

income will be very varied with the expectation of a mortgage or credit, and these might be

capital investments.

Old people (65+)

Old people will be expected to have capital investments in banks.

The following filter question in the written questionnaire identifies age range:

What is your age range?

o 18-26

o 26-65

o 65+

5.1.2. Type of client

The second question is another filter question needed to be addressed in this survey because

different types of clients tend to have a different behaviour.

32

Personal

The personal group gathers all the people that have a bank account and are not receptive of

any type of bank bonus offers like young and old people are. Although this does not mean

that these people could not be expected to have a certain credited range of income or be

attracted by some other offers that the bank gives to their clients. However, in order to make

it clear let’s say that this group of people are not getting recognised as a group.

Business

The business group is formed by the people who are part of a firm and operate in the bank as

a legal customer, so their relationship between the bank and its business is a bit different

than the one that operates between bank and individuals. This is the reason for having this

particular group as a filter.

Young people

This group of people of between 18-26 years old is treated as a separate group as they do

not get a bonus, commission or other types of bonuses only because of being young. They

are treated specially in the bank as well.

Old people

Old people are kind of a young people group but they are going to get all types of bonuses

only because of their age. This is the main reason for why one is going to treat them as a

separate group.

This factor regarding people´s characteristics has been addressed in this written survey as

the following question:

In which group of clients do you belong?

o Personal

o Business

o Young people

o Old people

33

5.1.3. Capital invested

The amount of capital invested is both a filter and an absorption question. The main reason

for including this question in the written survey was to show and filter the preferences of the

different types of savers. By separating them into three groups according to the Spanish bank

classifications, the results showed the type of clients that might be more interested in

investing in the German Banks. It must be also noted that this kind of question is also an

absorption question, because with the wide ranges to choose from the intention is not to

offend anyone’s personal honour.

Particular Bank (0 – 100.000€)

Particular Bank is a group of small savers that probably don’t think they have enough money

to be afraid of a bailout process as they would not be investing a lot. The study put forward

the hypothesis that the bulk of the population belongs to this group.

Personal Bank (100.000 – 500.000€)

This group of people have more money to invest and they have invested in the Spanish

Banks so this group should be one of the targets that the German Banks should focus on

first, because this group of people may think they do not have enough money to transfer to

another country, and secondly that their belief in German stability is going to be a main factor

in their investment decision making process.

Private Bank (+500.000€)

The private bank group is composed of those people that have more than a half million euros

to invest. This group of people are normally very active in investing their capital, and if their

capital has not already flown out of the country should offer a great opportunity for the

German Banks to gain market entry.

This factor regarding people´s characteristics in terms of their socio-economic status has

been addressed in the survey as follows:

In which money range do your personal savings belong to (invested and not

invested)?

o 0-100.000€

o 100.000€-500.000€

o +500.000€

34

5.1.4. Assets

The next filter question was used to make a distinction based on the total personal assets

belonging to a person like houses, cars, amongst others. This filter showed another

perspective about clients’ behavior by sorting them through their financial status. The

question is also an absorption question due to the fact that although it is a personal question,

the intention is not to attempt to invade personal privacy and allow them to answer it with

generalities.

0 - 500.000€

In this group the main population is covered. These persons frequently own or rent only a

single house. Moreover, this group is also expected to have a low personal income per year

giving them only small amounts of money to save. Thus it is assumed that these are not the

principal target for the German banks.

500.000€ - 2.000.000€

This group is composed of people who own a high value house or even two. They might also

be involved in all types of business with a local market. Moreover, it can be assumed that this

group tends to have more saving than the other group as described previously. These are

more likely to invest their saving. As a result, This MSc thesis assumes that this group would

be the main target of German banks.

+2.000.000€

This group is composed of wealthy people with a considerable amount of money to invest.

Hence, the population that establishes this group are considered as another important target

group that the German banks should be aiming to.

This filter and absorption question has been addressed in the written survey as the following

question:

In which money range does the value of your personal assets belong to?

o 0-500.000€

o 500.000€-2.000.000€

o +2.000.000€

35

5.2. Specific questions – Spain

5.2.1. Level of trust

The general question that tends to be answered is: What is your level of trust in the

Spanish Banking sector?. However, in order to get a more precise answer from the

respondent, this had to be formulated differently. More specifically, this was given a choice of

answers from 1 to 5 in order to be more precise when analyzing the results. As a direct

consequence of that question, the existing connections between banks and population could

be constructed. The question was phrased in a way that is not ambiguous. Ambiguity in such

a survey should be avoided because the results could be affected, defining the different

levels turn this question into a clear question. This factor has been addressed in this written

survey by posing as the following question:

What is your current level of trust in the Spanish Banking sector?

o I completely mistrust the Spanish banking sector and I would not invest my

savings in a Spanish bank

o I do not completely mistrust the Spanish banking sector but I would not likely

invest my savings in a Spanish bank

o The level of trust is irrelevant for me

o I do not completely trust the Spanish banking sector but I would be likely to

invest my savings in a Spanish bank

o I completely trust the Spanish banking sector and I would only invest my

savings in a Spanish bank.

5.2.2. Relationship between Spanish banks and their clients.

An informative question is used to identify the connection between Spanish banks and their

clients “Why do you have your money invested in a Spanish bank?”. This question was

separated into two further questions. As a result, information about the existing connection

between Banks and customers was obtained allowing the discovery of whether it is an

obligated connection or a willing connection. In order to discover about this type of

connection, a social question and a financial question are used.

36

5.2.3. Social questions

With the purpose of identifying the current social relationship between banks and clients, the

level of satisfaction of the Spanish clients regarding their banks was explored in the written

survey. Therefore, the existing customer relationship between clients and banks was

identified based on how well or poorly the Spanish banks treat their own clients. Including this

question in the survey, the possible lack of customer service from banks was analyzed. It was

also an opportunity to create a pattern for customer service excellence allowing the German

banks offer better customer service.

Which would be the value of your current satisfaction regarding your bank’s

treat?

o I am completely disappointed with my bank´s customer service procedures

o I am quite disappointed with my bank’s customer service procedures

o Customer service is irrelevant to my investment choice.

o I am quite satisfied with my bank’s customer service procedure but there are

several things that could be done in a better way.

o I am completely satisfied with my bank´s customer service procedure

5.2.4. Financial questions

This closed question established the main reason for the direct connection between a bank

and its current customers allowing the identification of whether the connection established is

mandatory or voluntary.

The question is a multiple choice question in which the responders is only able to tilt one

answer. This measure allowed to identify the strengths and weaknesses from Spanish Banks

regarding their clients. On the one hand, the ‘Don’t know’ answer was only used in the case

that the responder had not considered the reason of being a costumer from a bank. On the

other hand, an open question however was used in order to let the polled express any other

fact that could be important to his personal connection. The financial question been

addressed in this written survey as the following question:

37

Why do you choose to have your capital in a specific bank? (You can choose

more than one answer)

o Proximity

o Availability of mortgages, Credits

o Number of offices

o Customer Service

o Don’t know

o Other reasons______________________________________________

5.2.5. Fear about the safety of savings

In order to provide the following information, the question indirectly addressed in the research

asks “Are you afraid of losing your money if the bailout becomes real?” Two sub-

questions are asked in the written survey. The questions have been split into two further

questions since an in depth look into the fear of losing money is essential. Thus, one question

asks about has been directed to the level of fear that the population have and the other refers

to the kind of reaction that people experience when encountering this fear.

a) Level of fear question

Since the purpose of this sub-question is to get a quantifiable level of fear that people have in

relation to losing their money due to a bailout, a 1 to 5 scale of fear is formulated and

therefore, the capital leaving the country can be linked with the fear at bailout.

Which would most closely describe your current level of fear about the safety

of your money?

I think...

1. I will not lose my money

2. It is not probable that I will lose my money

3. I do not think about it

4. It is probable that I will lose my money

5. I will certainly lose my money

38

b) Reaction to the Bailout fear

People reactions (potentially or real) regarding the current economic situation is analyzed in

this informative question. More specifically, this multiple-choice question aims to assess the

way in which people are resolving/will resolve that fear in terms of the actions that people are

carrying out or are going to carry out with the specific purpose of making their money safe

before the hypothetic bailout happens. This parameter has been addressed in this written

survey as the following question:

What have you done to ensure the safety of your money? (You can tick more

than one)

o I keep it at home

o I have transferred it to a foreign bank

o I have done nothing

o I have invested it

o Other________________________

5.3. Specific questions – Germany

5.3.1. Trust in German banks

This sub-chapter proposes to answer the following question: “What is your level of trust in

the German Banking sector?” Instead to asking this question directly, two sub-questions

have been used in the written survey. The main reason for splitting this question up was to

quantify the level of trust and to understand the reason behind their trust in German banking.

From the answers, the strengths that German banks should exploit if they decide to invest in

the Spanish market.

39

a) Level of trust in German Banks

With the main purpose of quantifying the level of trust that the current Spanish population

have in the German banking sector, a 1 to 5 level question is used.

What would your current level of trust be in the German Banking sector?

o I completely mistrust the German banking sector and I would not invest my

savings in a German bank

o I mistrust the German banking sector and I would be not likely to invest my

savings in a German bank

o The level of trust is irrelevant for me

o I do not completely trust the German banking sector but I would be likely to

invest my savings in a German bank

o I completely trust the German banking sector and I would only invest my

savings in a German bank.

b) Trust in the German Banking sector

This information question is addressed in the written survey in order to discover the main

grounds for why the Spanish people currently trust the German banking sector. This in

connection with the level question gives a representative overview of the Spanish perceptions

of German banking.

Why do you trust the German Banking sector? (You can tick more than one)

o Personal knowledge

o I’ve been told about it

o Germany is the leading first European force

o Their reputation Made in Germany (Quality guaranteed)

o Other________________________

5.3.2. Investment in German banks.

The Yes/No question “Would you be least worried if your money was invested in a

German Bank?” is used in the written survey to analyze investment in German banks. The

main reason for choosing this as a Yes/No question, is because in such issues people tend to

give the ‘but answer’ (Yes,but……. No,but…..). Hence, the intention is to avoid this kind of

ambiguity by summarizing the whole question in a Yes/No question.

40

Would you invest your capital in a German Bank?

o Yes

o No

o Don’t know

5.3.3. Transferring capital out of Spain

The question that is answered in this part of the survey refers to the principal reasons people

have for not transferring their money to a foreign country, specifically Germany. The main

question is: “Would you fly to Germany in order to open a bank account and transfer

your money?”. However, since the intention is to get as much information as possible, the

main question is divided into a Yes/No question with two possible further questions based on

the answer to the first question. People’s reactions to the idea of going to Germany to open a

bank account are addressed in these sub-questions.

Would you fly to Germany to open a Bank account?

o Yes

o No

o Don’t know

If the answer to the above question is a Yes then:

Why would you fly to Germany?

o My money will be safe

o I am told to do it

o That is what people are doing

o Other reasons____________________

o

If the answer to the above question is a No then:

Why would you not fly to Germany?

o Language issue

o Spending money on a trip

o Too far away

o My money is safe in Spain

o Other reasons__________________

41

5.4. Specific questions – Spain & Germany

The above questions led to the final question that summed up the variables addressed

before. The last question also gave a response to the question that reflected the MSc thesis

main goal: “Would you open a bank account and transfer your capital to a German Bank

if there were German banks offices operating in Spain?”. The goal question was a

Yes/No question in order to get a clear answer and thus making, results more accurate.

Would you invest in a German bank if it has offices in Spain?

o Yes

o No

o Don’t know

42

6. Results and Statistical Analysis

The identification of the main variables that play a role in this topic, the survey results and

finally the statistical analysis are carried out in this chapter. The research questions

concerning this M.Sc. Thesis addressed are:

What is the level of trust in the Spanish and German banking sectors?

What is the level of concern of Spanish inhabitants regarding the likelihood that a

bailout will become real?

Does the location of the bank offices play a relevant role in people´s decision-making

with regard to investing their money?

6.1. Analytical variables

The analysis of people’s feelings and perceptions both German and Spanish banking has

been carried out initially by identifying 16 critical analytical variables. These have been

classified according to the type of question in which they are addressed and the

transformation used during the statistical analysis. In the case of closed questions, possible

responses have been listed.

43

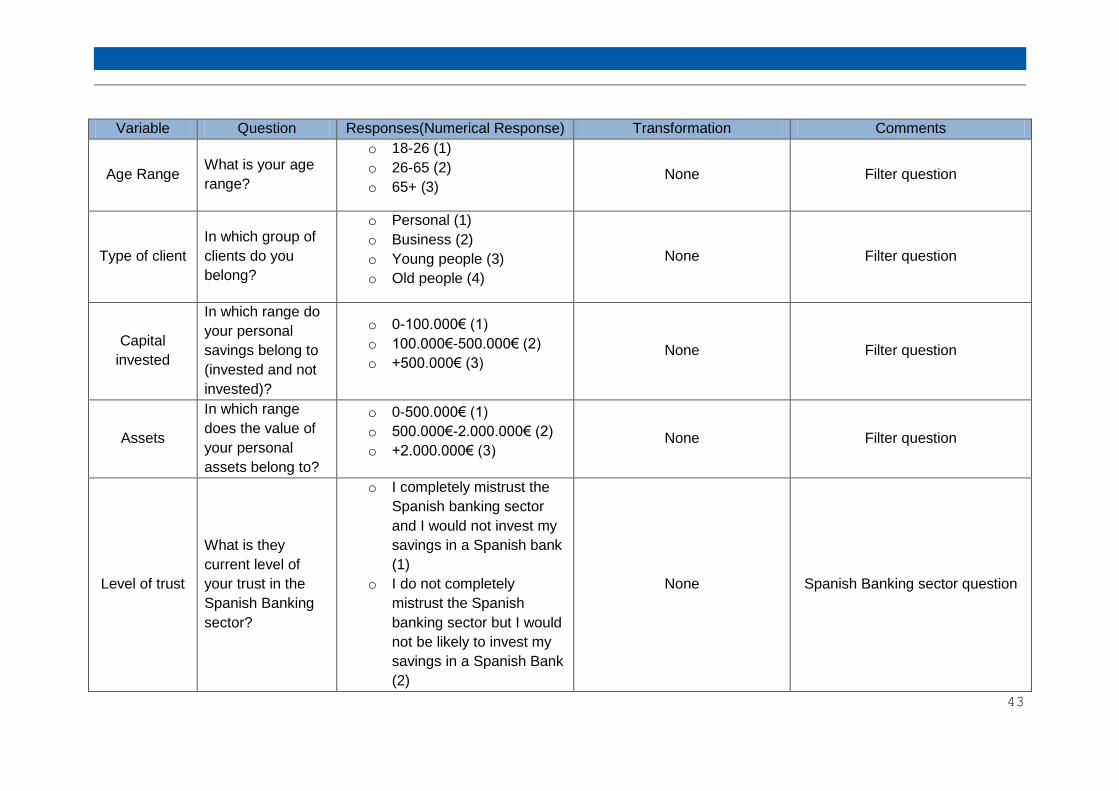

Variable Question Responses(Numerical Response) Transformation Comments

Age Range What is your age

range?

o 18-26 (1)

o 26-65 (2)

o 65+ (3) None Filter question

Type of client

In which group of

clients do you

belong?

o Personal (1)

o Business (2)

o Young people (3)

o Old people (4)

None Filter question

Capital

invested

In which range do

your personal

savings belong to

(invested and not

invested)?

o 0-100.000€ (1)

o 100.000€-500.000€ (2)

o +500.000€ (3) None Filter question

Assets

In which range

does the value of

your personal

assets belong to?

o 0-500.000€ (1)

o 500.000€-2.000.000€ (2)

o +2.000.000€ (3) None Filter question

Level of trust

What is they

current level of

your trust in the

Spanish Banking

sector?

o I completely mistrust the

Spanish banking sector

and I would not invest my

savings in a Spanish bank

(1)

o I do not completely

mistrust the Spanish

banking sector but I would

not be likely to invest my

savings in a Spanish Bank

(2)

None Spanish Banking sector question

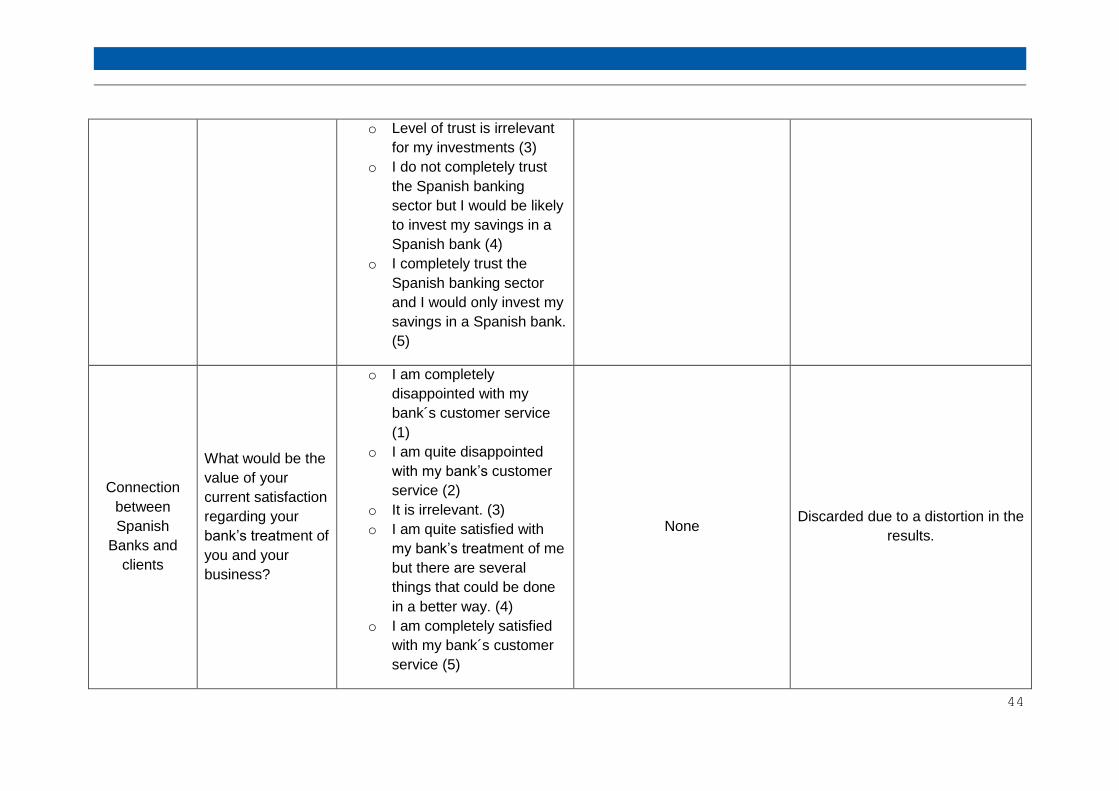

44

o Level of trust is irrelevant

for my investments (3)

o I do not completely trust

the Spanish banking

sector but I would be likely

to invest my savings in a

Spanish bank (4)

o I completely trust the

Spanish banking sector

and I would only invest my

savings in a Spanish bank.

(5)

Connection

between

Spanish

Banks and

clients

What would be the

value of your

current satisfaction

regarding your

bank’s treatment of

you and your

business?

o I am completely

disappointed with my

bank´s customer service

(1)

o I am quite disappointed

with my bank’s customer

service (2)

o It is irrelevant. (3)

o I am quite satisfied with

my bank’s treatment of me

but there are several

things that could be done

in a better way. (4)

o I am completely satisfied

with my bank´s customer

service (5)

None Discarded due to a distortion in the

results.

45

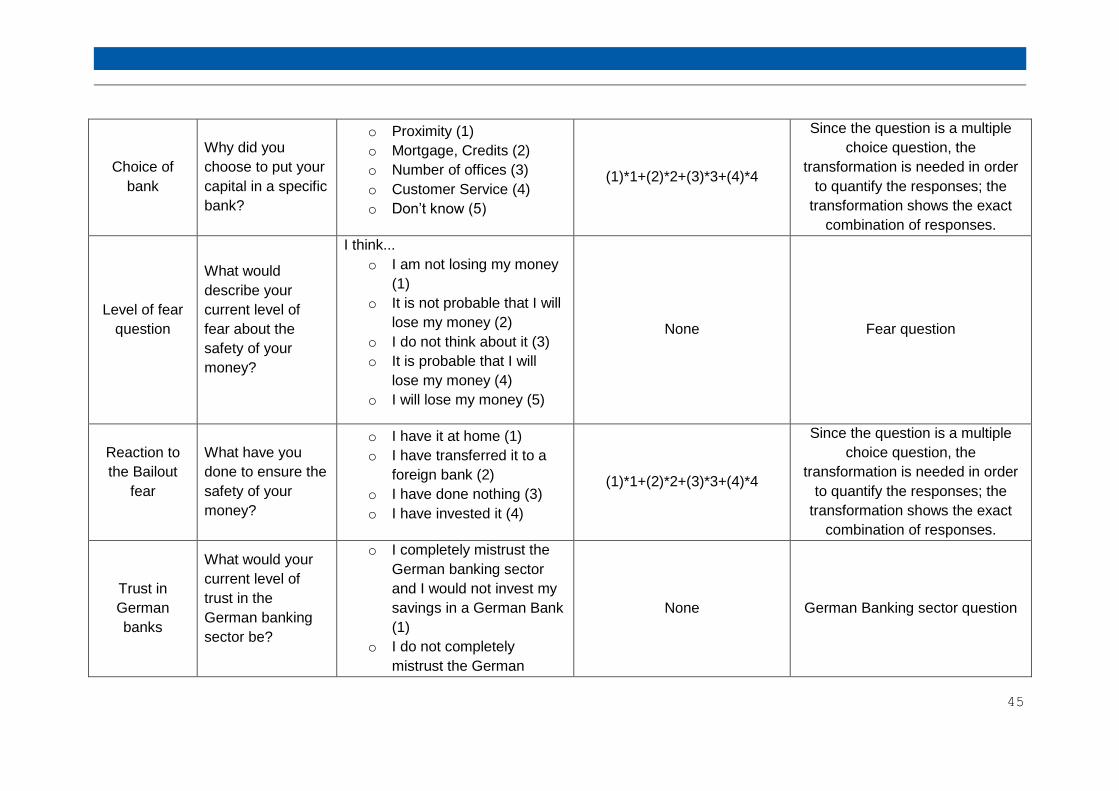

Choice of

bank

Why did you

choose to put your

capital in a specific

bank?

o Proximity (1)

o Mortgage, Credits (2)

o Number of offices (3)

o Customer Service (4)

o Don’t know (5)

(1)*1+(2)*2+(3)*3+(4)*4

Since the question is a multiple

choice question, the

transformation is needed in order

to quantify the responses; the

transformation shows the exact

combination of responses.

Level of fear

question

What would

describe your

current level of

fear about the

safety of your

money?

I think...

o I am not losing my money

(1)

o It is not probable that I will

lose my money (2)

o I do not think about it (3)

o It is probable that I will

lose my money (4)

o I will lose my money (5)

None Fear question

Reaction to

the Bailout

fear

What have you

done to ensure the

safety of your

money?

o I have it at home (1)

o I have transferred it to a

foreign bank (2)

o I have done nothing (3)

o I have invested it (4)

(1)*1+(2)*2+(3)*3+(4)*4

Since the question is a multiple

choice question, the

transformation is needed in order

to quantify the responses; the

transformation shows the exact

combination of responses.

Trust in

German

banks

What would your

current level of

trust in the

German banking

sector be?

o I completely mistrust the

German banking sector

and I would not invest my

savings in a German Bank

(1)

o I do not completely

mistrust the German

None German Banking sector question

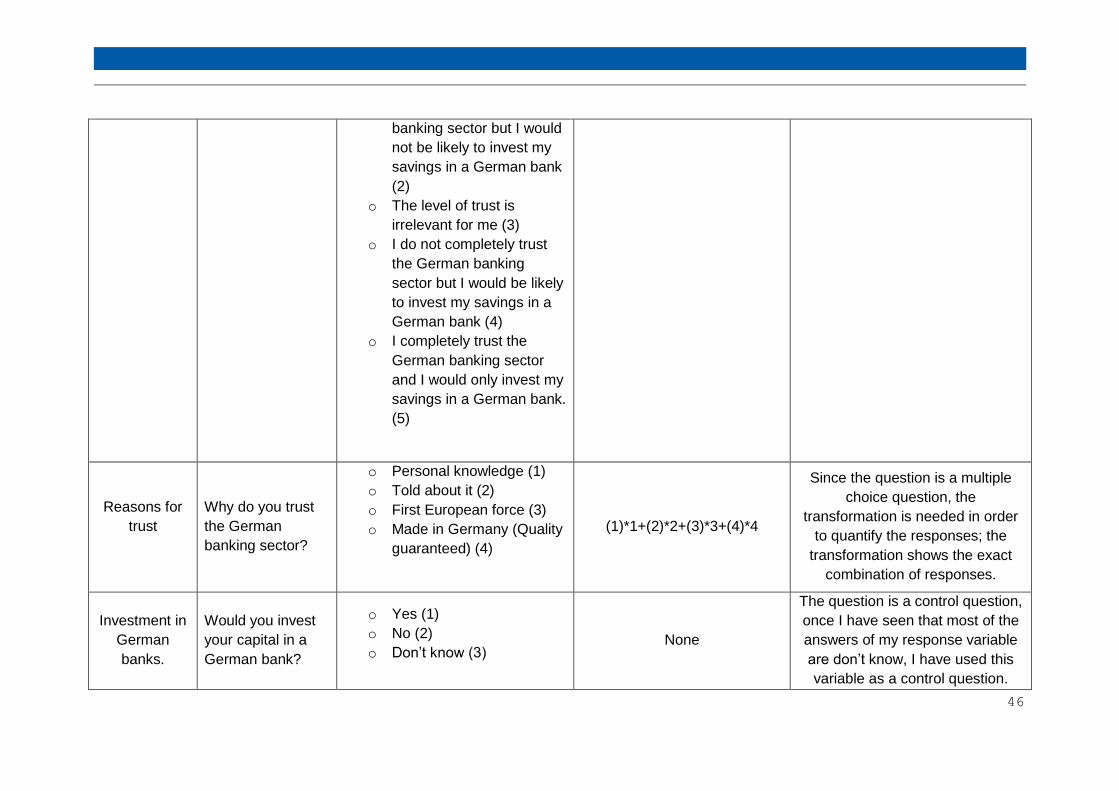

46

banking sector but I would

not be likely to invest my

savings in a German bank

(2)

o The level of trust is

irrelevant for me (3)

o I do not completely trust

the German banking

sector but I would be likely

to invest my savings in a

German bank (4)

o I completely trust the

German banking sector

and I would only invest my

savings in a German bank.

(5)

Reasons for

trust

Why do you trust

the German

banking sector?

o Personal knowledge (1)

o Told about it (2)

o First European force (3)

o Made in Germany (Quality

guaranteed) (4)

(1)*1+(2)*2+(3)*3+(4)*4

Since the question is a multiple

choice question, the

transformation is needed in order

to quantify the responses; the

transformation shows the exact

combination of responses.

Investment in

German

banks.

Would you invest

your capital in a

German bank?

o Yes (1)

o No (2)

o Don’t know (3) None

The question is a control question,

once I have seen that most of the

answers of my response variable

are don’t know, I have used this

variable as a control question.

47

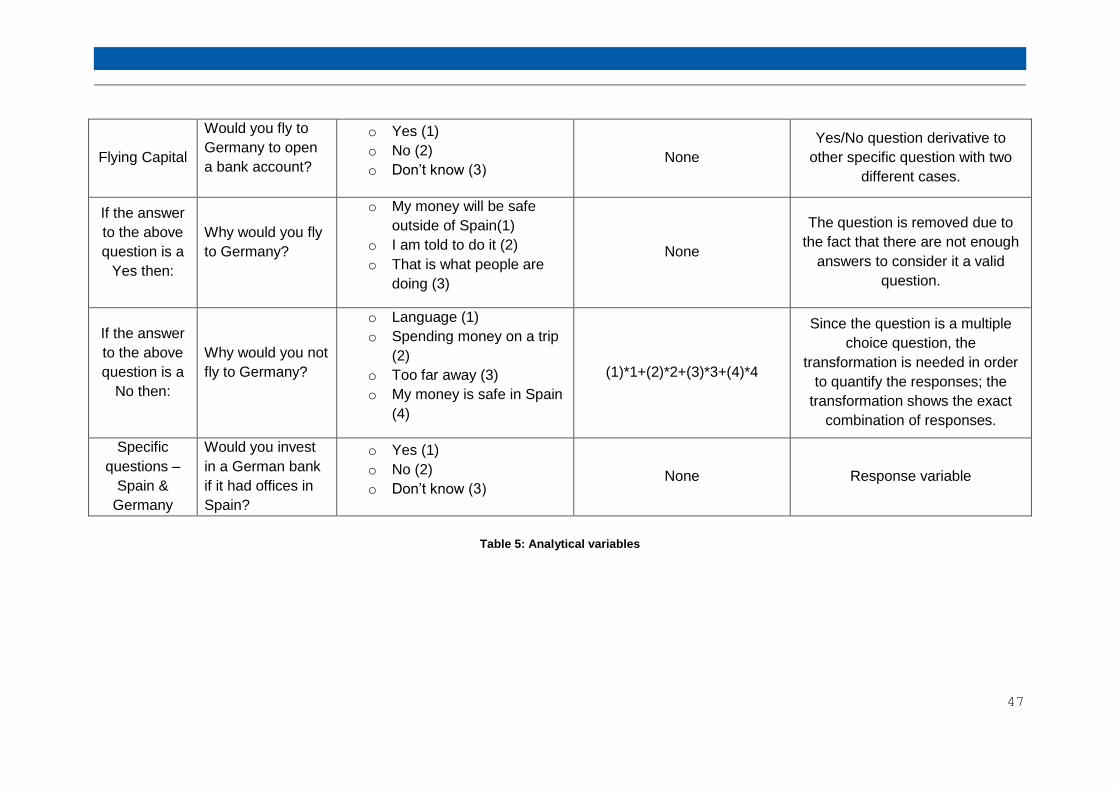

Flying Capital

Would you fly to

Germany to open

a bank account?

o Yes (1)

o No (2)

o Don’t know (3) None

Yes/No question derivative to

other specific question with two

different cases.

If the answer

to the above

question is a

Yes then:

Why would you fly

to Germany?

o My money will be safe

outside of Spain(1)

o I am told to do it (2)

o That is what people are

doing (3)

None

The question is removed due to

the fact that there are not enough

answers to consider it a valid

question.

If the answer

to the above

question is a

No then:

Why would you not

fly to Germany?

o Language (1)

o Spending money on a trip

(2)

o Too far away (3)

o My money is safe in Spain

(4)

(1)*1+(2)*2+(3)*3+(4)*4

Since the question is a multiple

choice question, the

transformation is needed in order

to quantify the responses; the

transformation shows the exact

combination of responses.

Specific

questions –

Spain &

Germany

Would you invest

in a German bank

if it had offices in

Spain?

o Yes (1)

o No (2)

o Don’t know (3) None Response variable

Table 5: Analytical variables

48

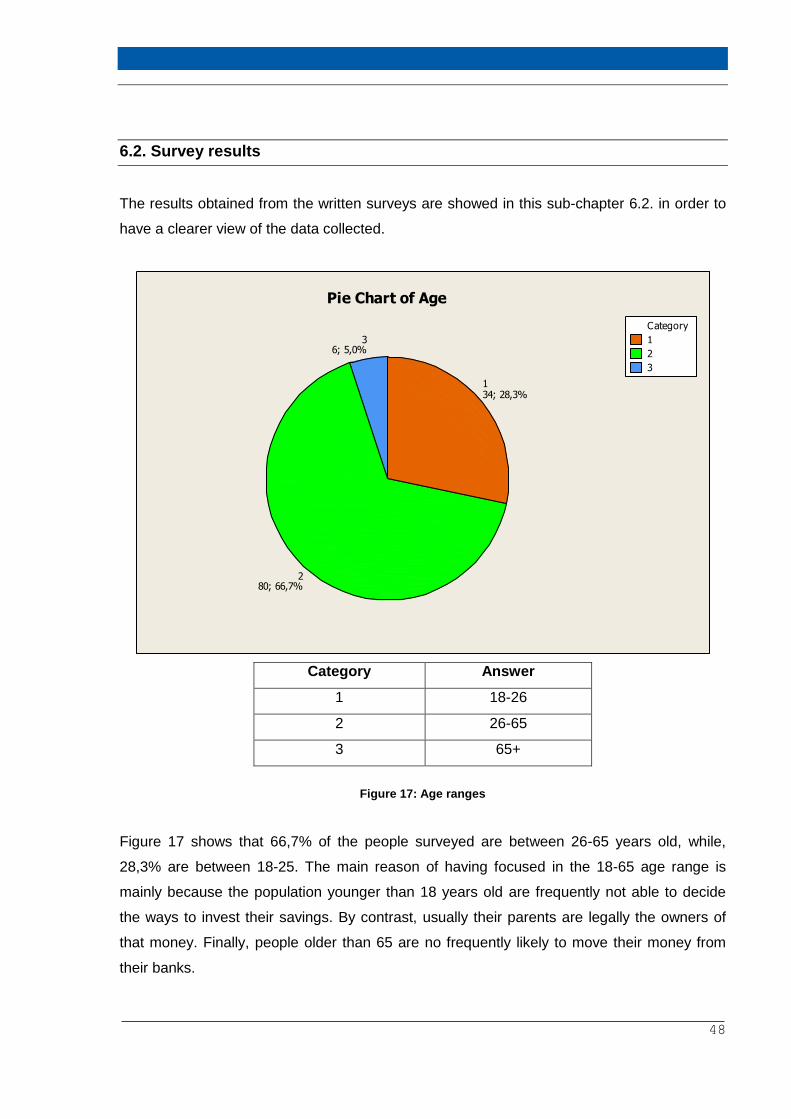

6.2. Survey results

The results obtained from the written surveys are showed in this sub-chapter 6.2. in order to

have a clearer view of the data collected.

1

2

3

Category

36; 5,0%

280; 66,7%

134; 28,3%

Pie Chart of Age

Category Answer

1 18-26

2 26-65

3 65+

Figure 17: Age ranges

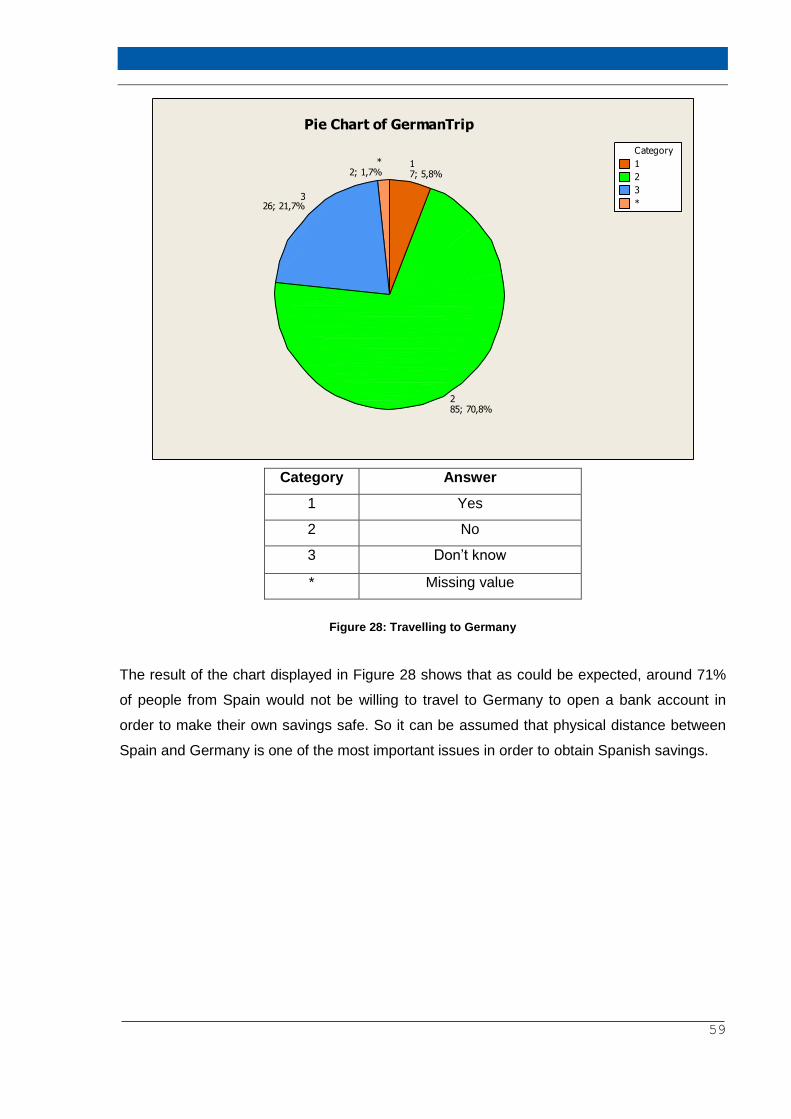

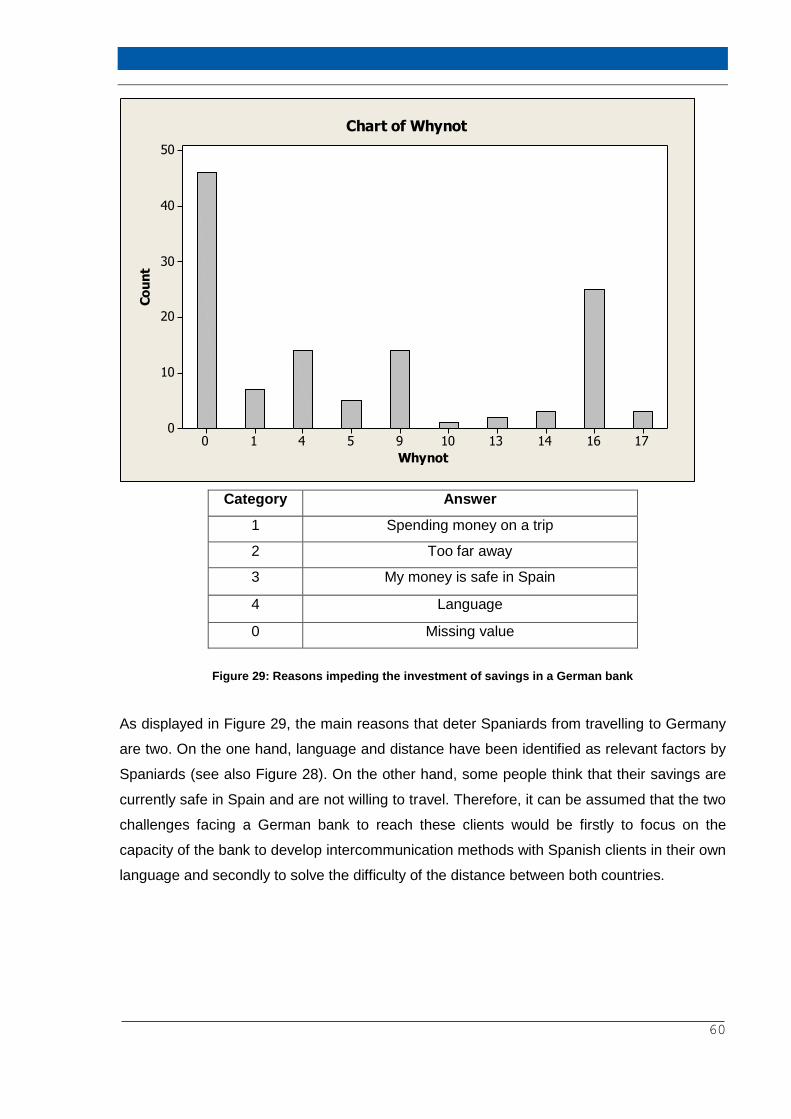

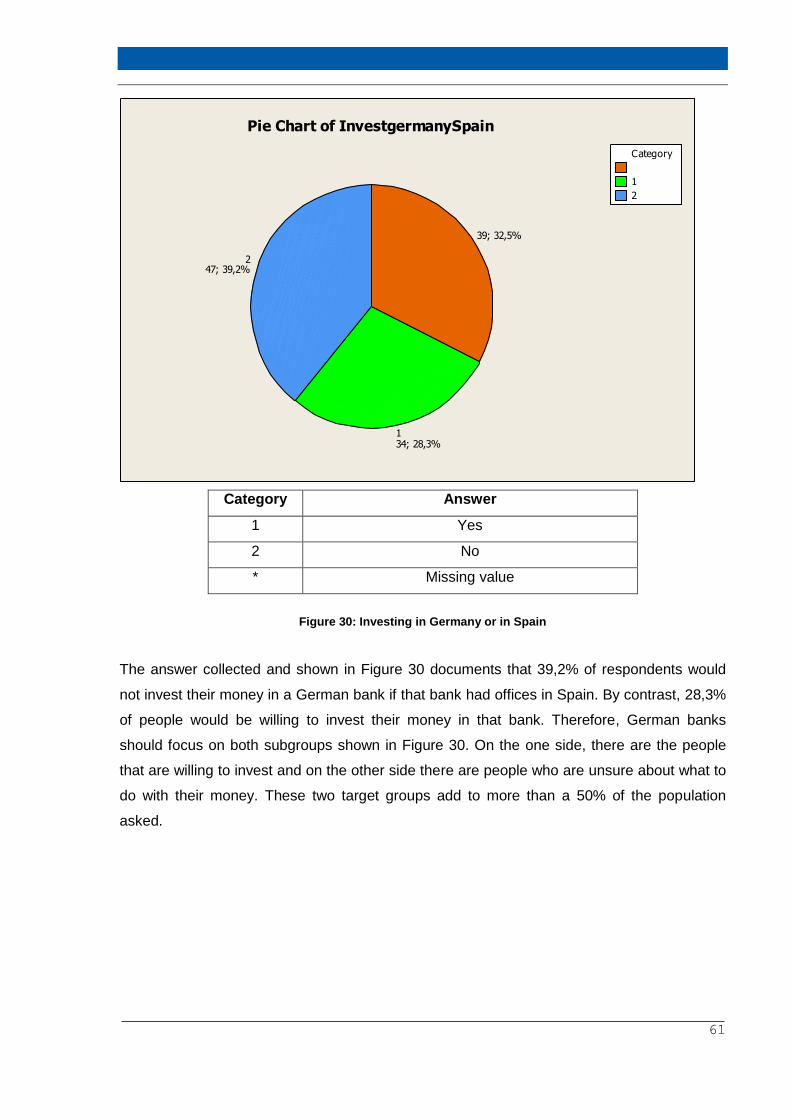

Figure 17 shows that 66,7% of the people surveyed are between 26-65 years old, while,

28,3% are between 18-25. The main reason of having focused in the 18-65 age range is

mainly because the population younger than 18 years old are frequently not able to decide

the ways to invest their savings. By contrast, usually their parents are legally the owners of

that money. Finally, people older than 65 are no frequently likely to move their money from

their banks.

49

1

2

3

4

*

Category*

5; 4,2%43; 2,5%

332; 26,7%

25; 4,2%

175; 62,5%

Pie Chart of Client

Category Answer

1 Personal

2 Young People

3 Business

4 Old People

* Missing value

Figure 18: Client type

Two types of client have been identified as predominant in the survey, personal customers

and young people. There are 62,5% of personal clients which accounts for a total of 75

surveyed, within which group young people account for 26,7% (32 respondents). Referring to

the data analysed in Figure 17 the conclusion obtained from both Figures 17 and 18 would be

similar: our target customer would be a man or woman between 18-65 years old and

therefore eligible for personal or young people customer privileges.

The main reason of removing business clients from the survey is based on their need to work

in a day-to-day bank-business relationship and have different requirements. Hence, since the

survey is looking for investors and not for a typical client, business people are not likely to be

representative in the survey.

50

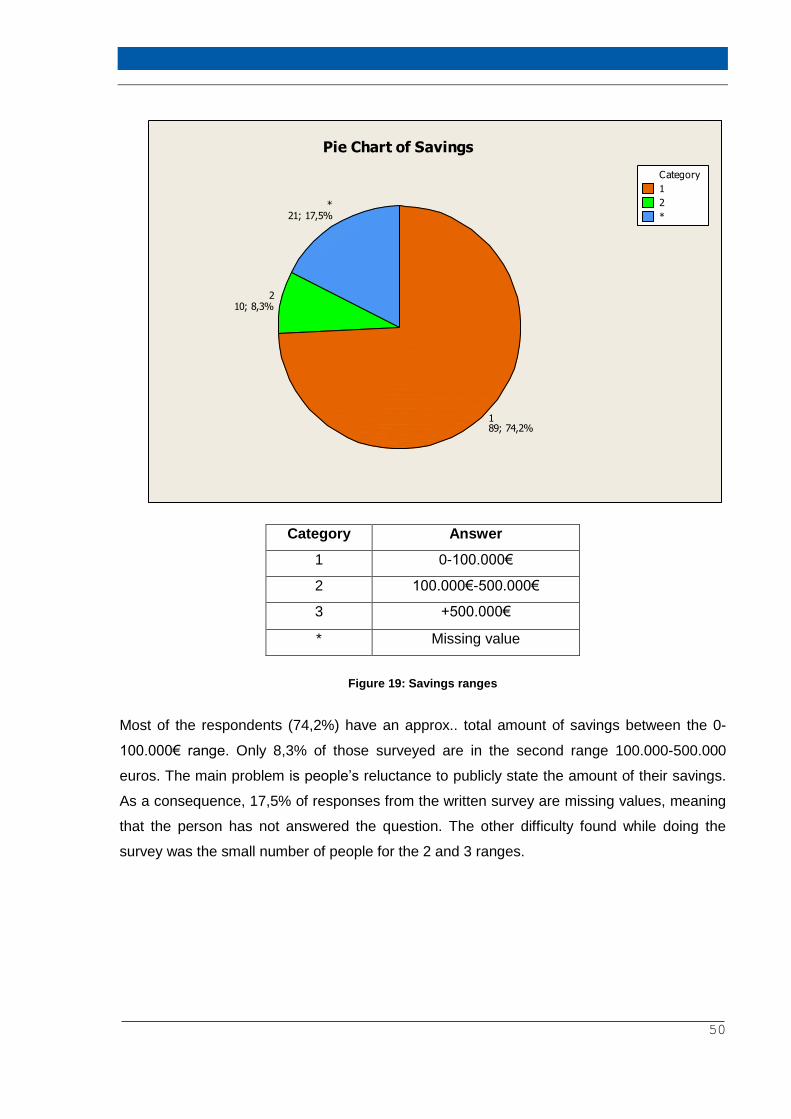

1

2

*

Category

*21; 17,5%

210; 8,3%

189; 74,2%

Pie Chart of Savings

Category Answer

1 0-100.000€

2 100.000€-500.000€

3 +500.000€

* Missing value

Figure 19: Savings ranges

Most of the respondents (74,2%) have an approx.. total amount of savings between the 0-

100.000€ range. Only 8,3% of those surveyed are in the second range 100.000-500.000

euros. The main problem is people’s reluctance to publicly state the amount of their savings.

As a consequence, 17,5% of responses from the written survey are missing values, meaning

that the person has not answered the question. The other difficulty found while doing the

survey was the small number of people for the 2 and 3 ranges.

51

1

2

3

*

Category

*23; 19,2%

31; 0,8%

211; 9,2%

185; 70,8%

Pie Chart of Patrimonial

Category Answer

1 0-500.000€

2 500.000€-2.000.000€

3 +2.000.000€

* Missing value

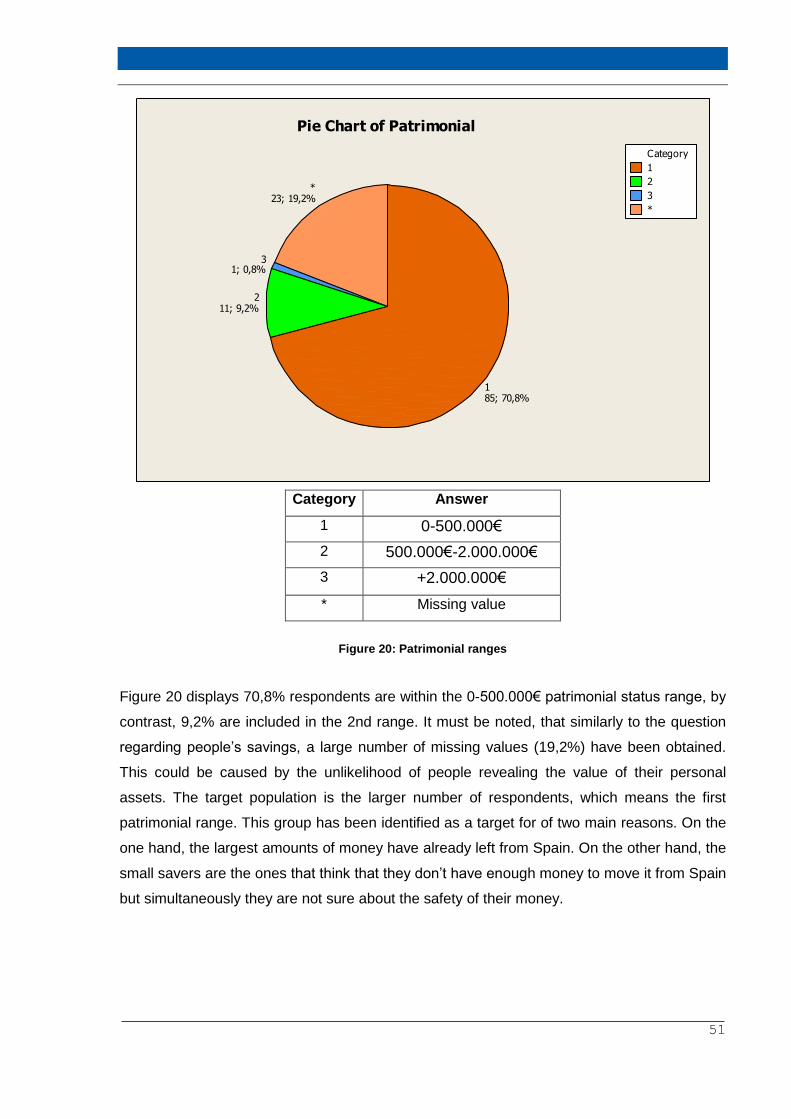

Figure 20: Patrimonial ranges

Figure 20 displays 70,8% respondents are within the 0-500.000€ patrimonial status range, by

contrast, 9,2% are included in the 2nd range. It must be noted, that similarly to the question

regarding people’s savings, a large number of missing values (19,2%) have been obtained.

This could be caused by the unlikelihood of people revealing the value of their personal

assets. The target population is the larger number of respondents, which means the first

patrimonial range. This group has been identified as a target for of two main reasons. On the

one hand, the largest amounts of money have already left from Spain. On the other hand, the

small savers are the ones that think that they don’t have enough money to move it from Spain

but simultaneously they are not sure about the safety of their money.

52

1

2

3

4

5

*

Category*

3; 2,5%53; 2,5%

429; 24,2%

326; 21,7%

243; 35,8%

116; 13,3%

Pie Chart of TrustSpain

Category Answer

1 I completely mistrust the Spanish banking sector and I would not

invest my savings in a Spanish bank

2 I do not completely mistrust the Spanish banking sector but I

would not likely invest my savings in a Spanish bank

3 The level of trust is irrelevant for me

4 I do not completely trust the Spanish banking sector but I would

likely invest my savings in a Spanish bank

5 I completely trust the Spanish banking sector and I would only

invest my savings in a Spanish bank.

* Missing value

Figure 21: Trust in the Spanish Banking system

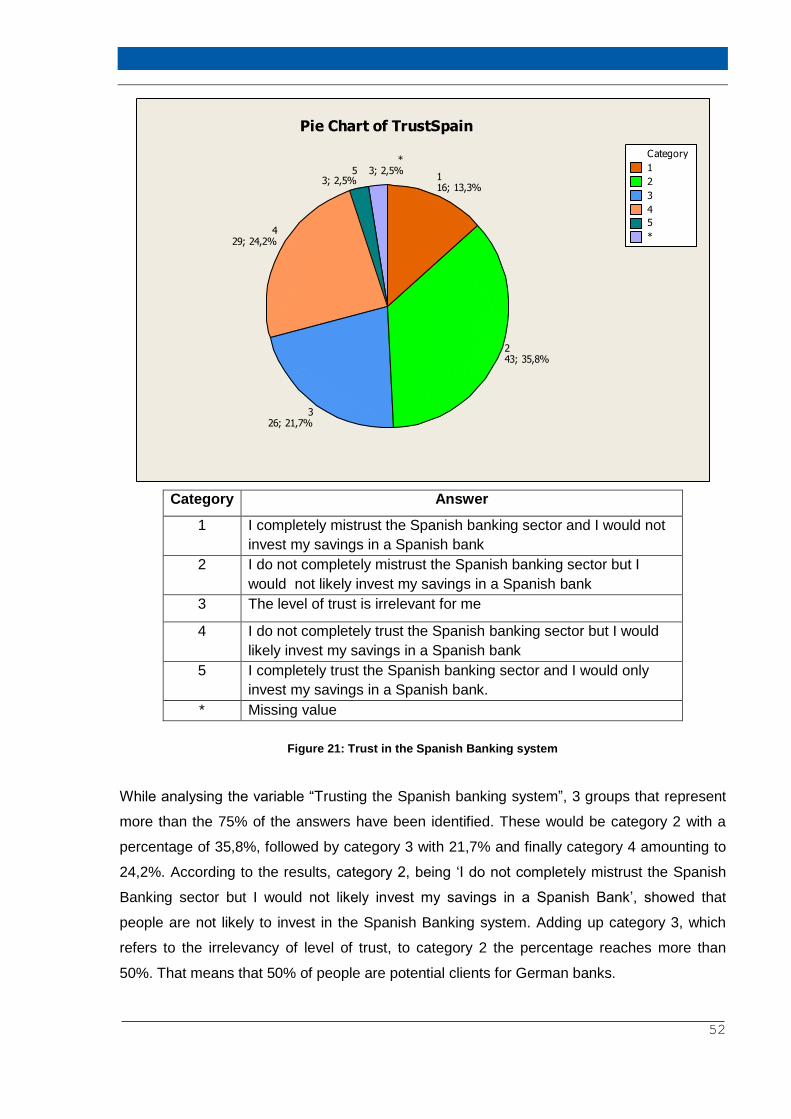

While analysing the variable “Trusting the Spanish banking system”, 3 groups that represent

more than the 75% of the answers have been identified. These would be category 2 with a

percentage of 35,8%, followed by category 3 with 21,7% and finally category 4 amounting to

24,2%. According to the results, category 2, being ‘I do not completely mistrust the Spanish

Banking sector but I would not likely invest my savings in a Spanish Bank’, showed that

people are not likely to invest in the Spanish Banking system. Adding up category 3, which

refers to the irrelevancy of level of trust, to category 2 the percentage reaches more than

50%. That means that 50% of people are potential clients for German banks.

53

1

2

3

4

5

Category

520; 16,7%

455; 45,8%

37; 5,8%

235; 29,2%

13; 2,5%

Pie Chart of Treatment

Category Answer

1 I am completely disappointed with my bank´s treatment of my

business

2 I am quite disappointed with my bank’s treatment of me and my

business

3 It is irrelevant.

4 I am quite satisfied with my bank’s level of service but there are

several things that could be done in a better way.

5 I am completely satisfied with my bank´s customer service

* Missing value

Figure 22: Bank’s treatment of me and my business

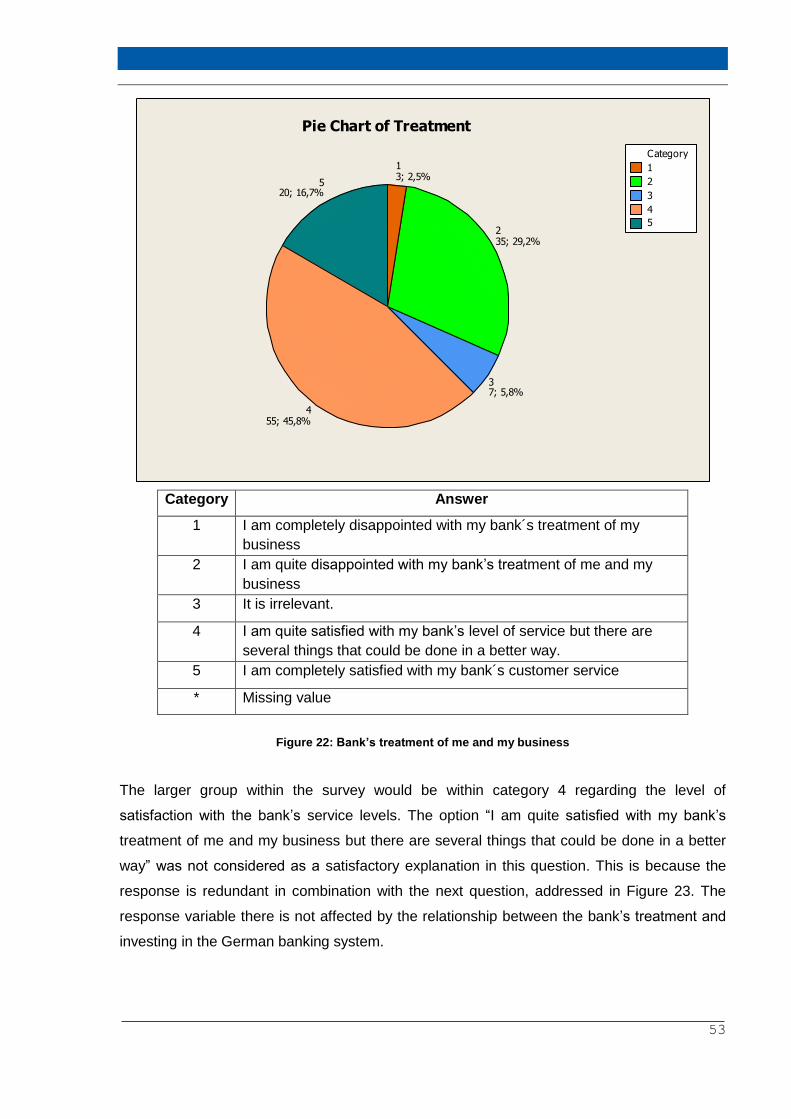

The larger group within the survey would be within category 4 regarding the level of

satisfaction with the bank’s service levels. The option “I am quite satisfied with my bank’s

treatment of me and my business but there are several things that could be done in a better

way” was not considered as a satisfactory explanation in this question. This is because the

response is redundant in combination with the next question, addressed in Figure 23. The

response variable there is not affected by the relationship between the bank’s treatment and

investing in the German banking system.

54

35302926252120171614131095410

20

15

10

5

0

BankDependence

Co

un

t

Chart of BankDependence

Category Answer

1 Proximity

2 Mortgage, Credits

3 Number of offices

4 Service Levels

5 Don’t know

* Missing value

Figure 23: Bank dependence

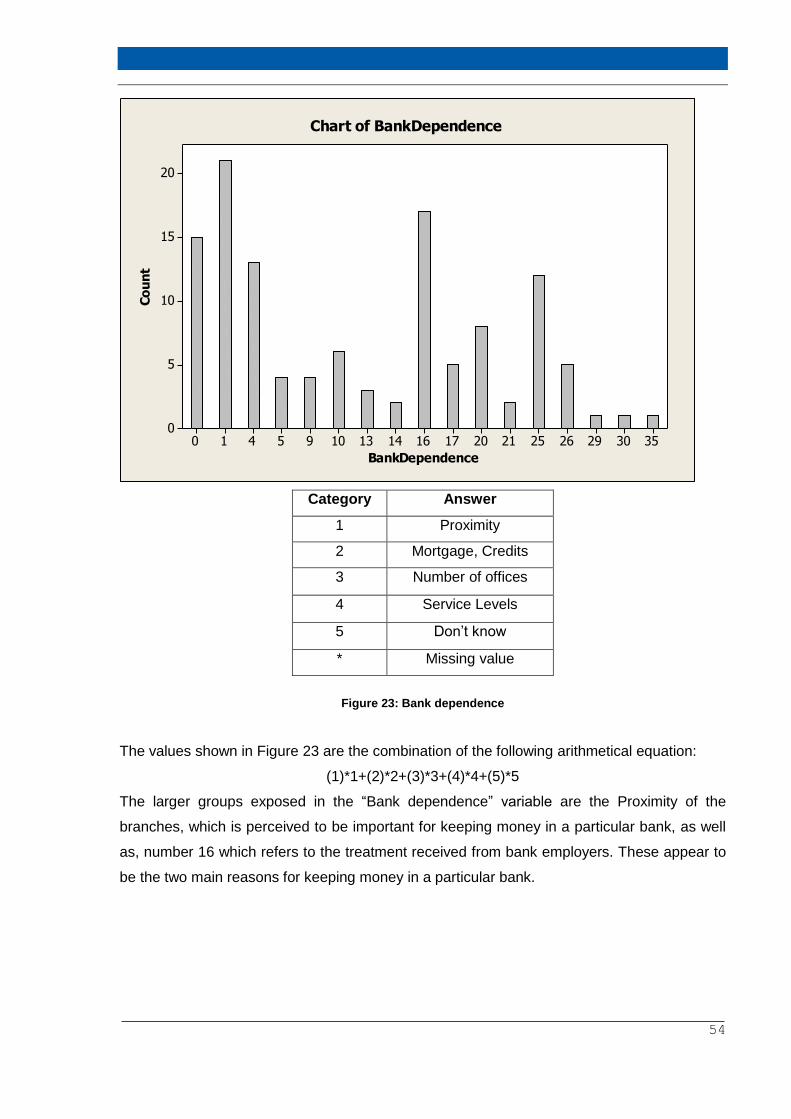

The values shown in Figure 23 are the combination of the following arithmetical equation:

(1)*1+(2)*2+(3)*3+(4)*4+(5)*5

The larger groups exposed in the “Bank dependence” variable are the Proximity of the

branches, which is perceived to be important for keeping money in a particular bank, as well

as, number 16 which refers to the treatment received from bank employers. These appear to

be the two main reasons for keeping money in a particular bank.

55

1

2

3

4

5

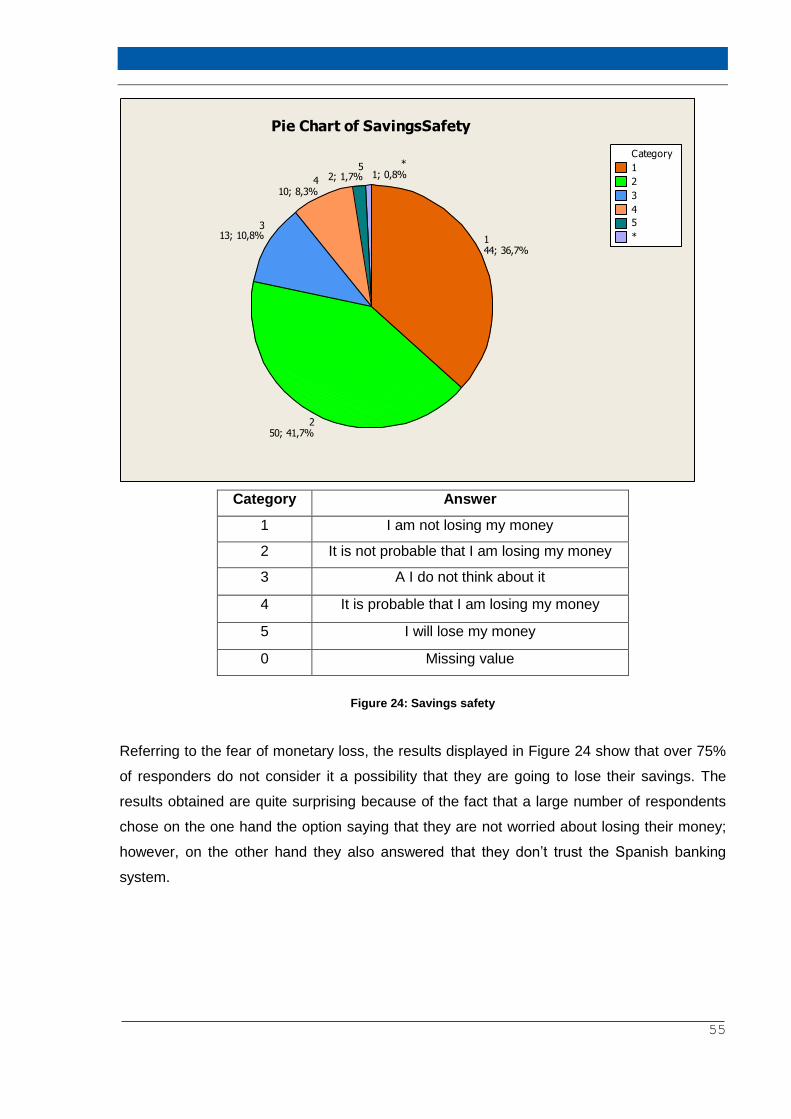

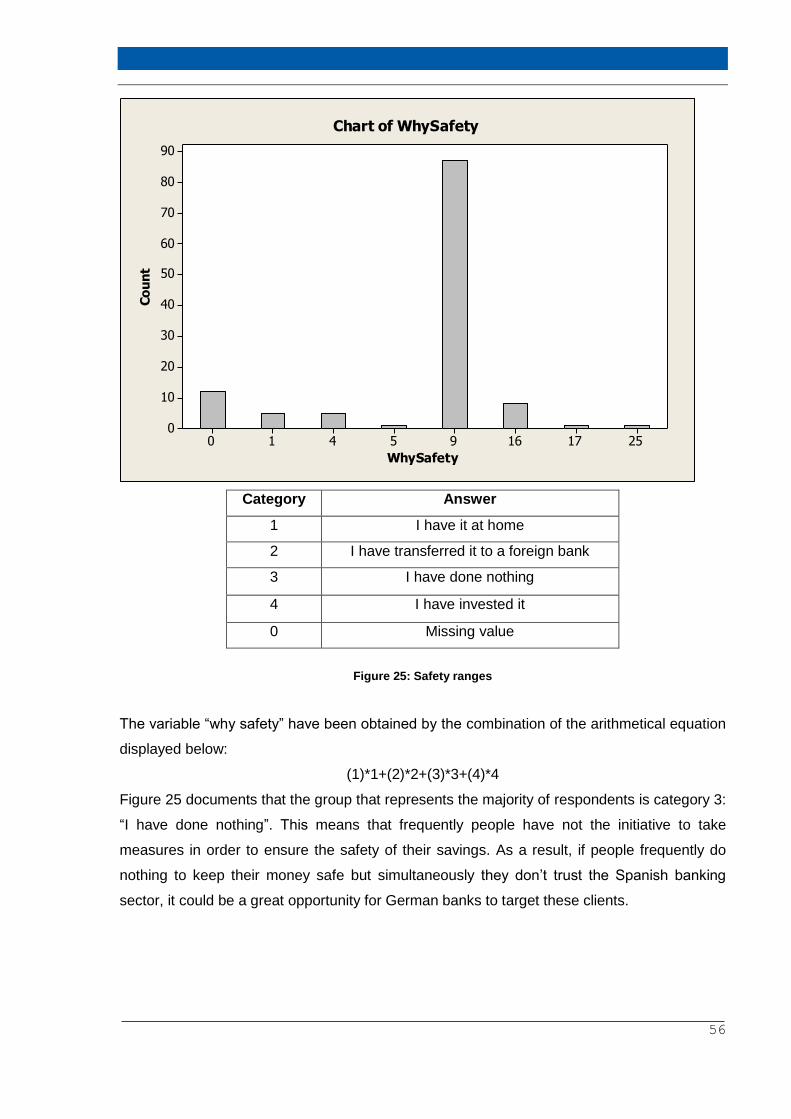

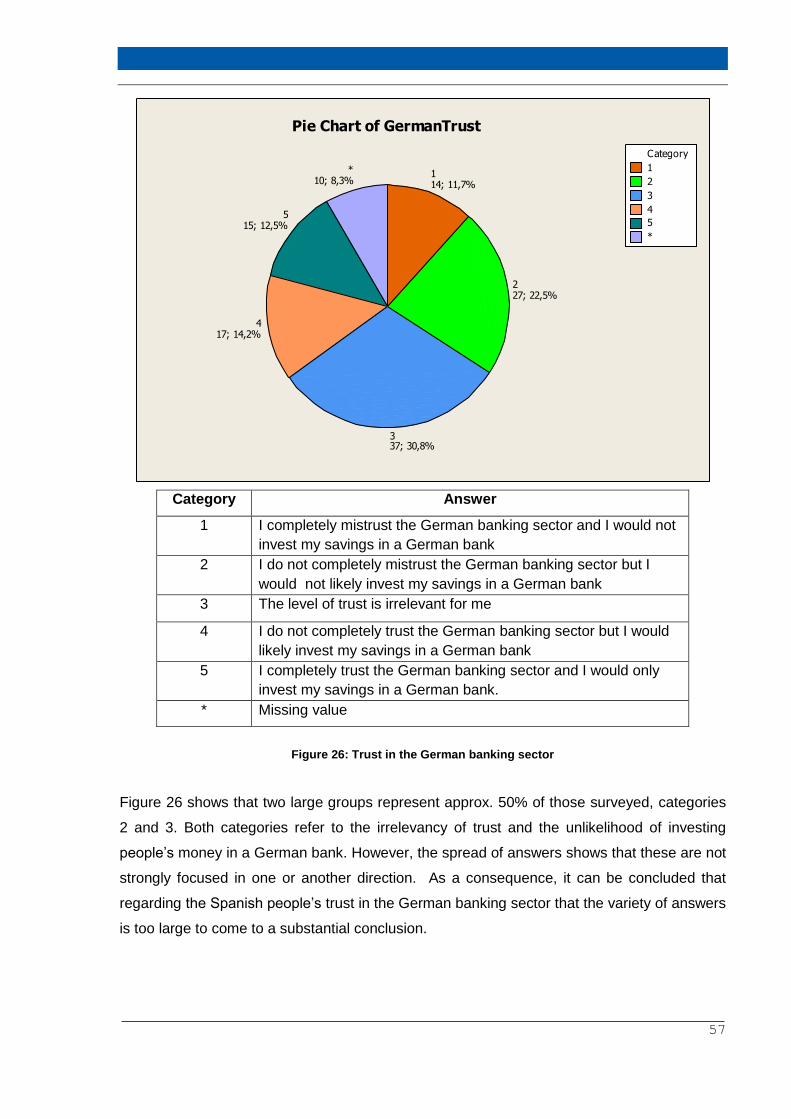

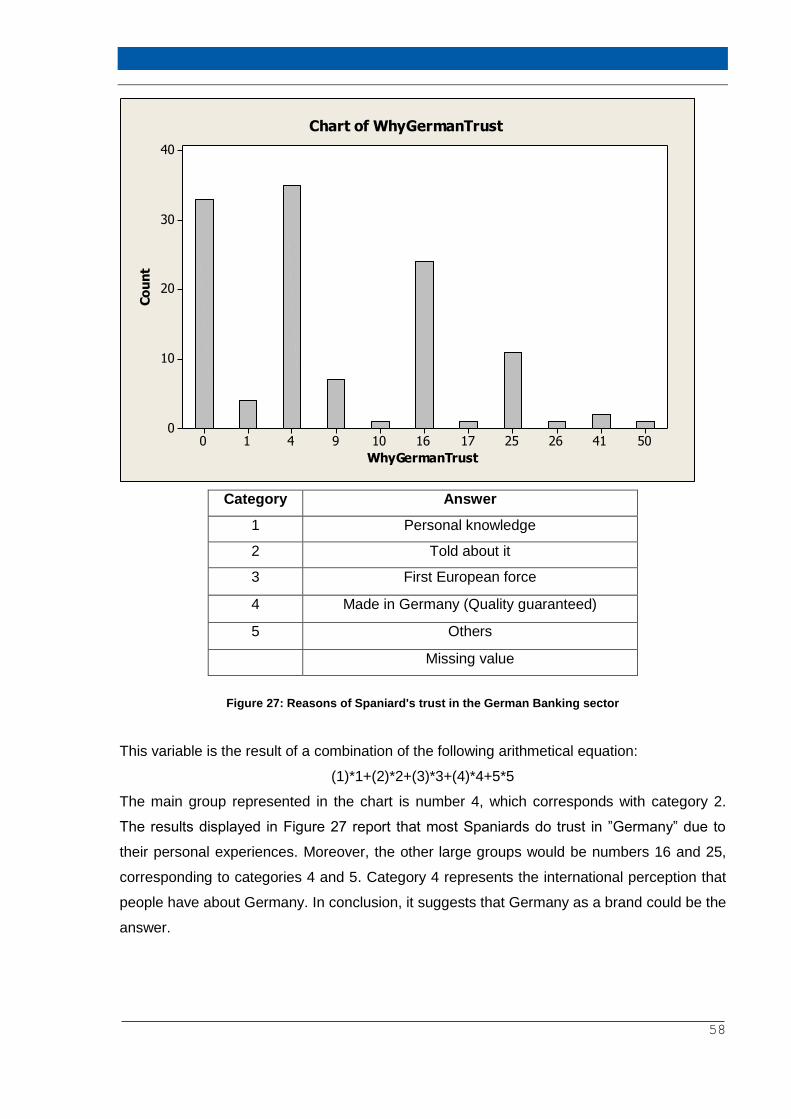

*