Aus: Thommen/Grösser: Economy · Company · Management ...

43

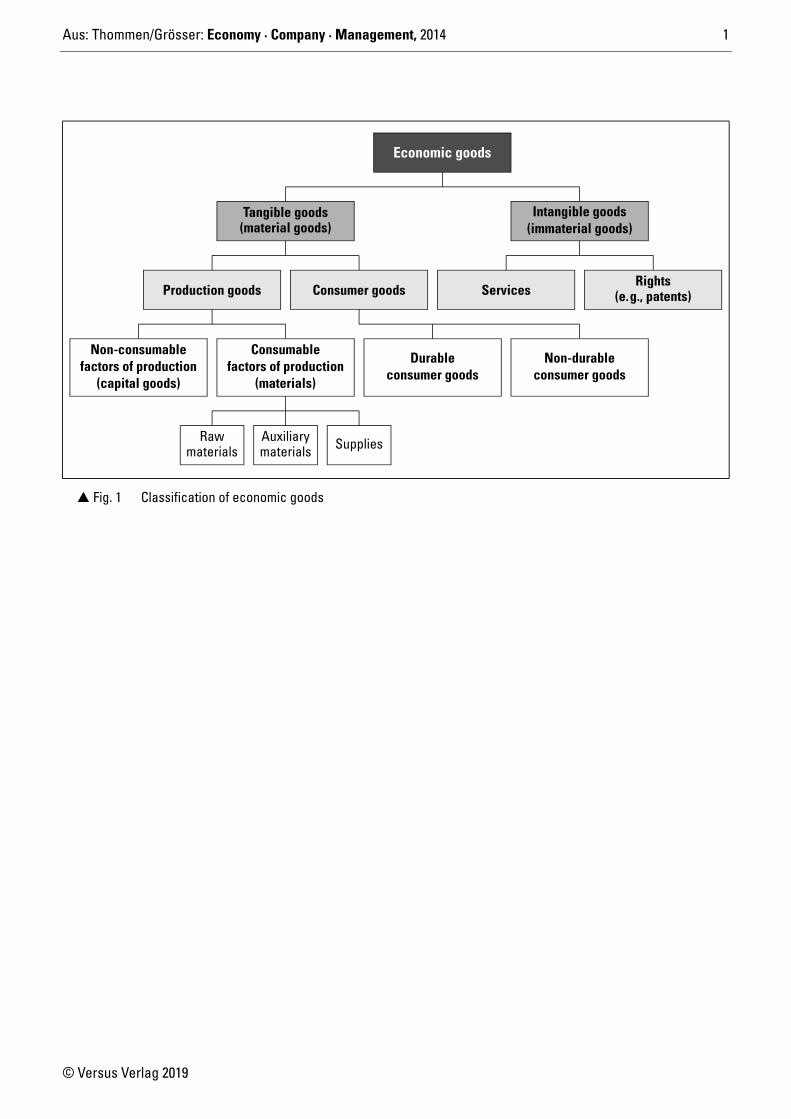

Aus: Thommen/Grösser: Economy · Company · Management, 2014 1 © Versus Verlag 2019 Fig. 1 Classification of economic goods Economic goods Intangible goods Tangible goods (material goods) Consumer goods Production goods Services Rights (e. g., patents) Durable Non-durable Non-consumable factors of production Consumable factors of production Auxiliary Supplies Raw materials materials (immaterial goods) consumer goods consumer goods (capital goods) (materials)

Transcript of Aus: Thommen/Grösser: Economy · Company · Management ...

Aus: Thommen/Grösser: Economy · Company · Management, 2014 1

© Versus Verlag 2019

� Fig. 1 Classification of economic goods

Economic goods

Intangible goodsTangible goods(material goods)

Consumer goodsProduction goods ServicesRights

(e.g., patents)

Durable Non-durableNon-consumable

factors of productionConsumable

factors of production

Auxiliary SuppliesRawmaterials materials

(immaterial goods)

consumer goodsconsumer goods(capital goods) (materials)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 2

© Versus Verlag 2019

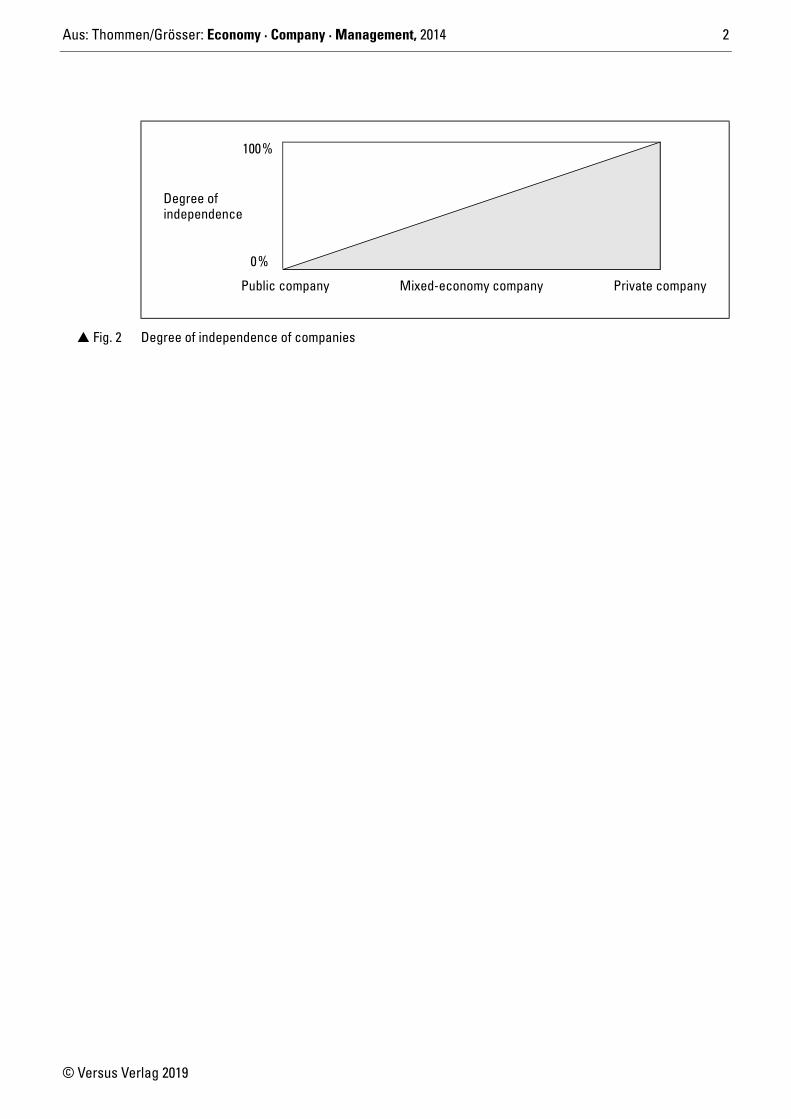

� Fig. 2 Degree of independence of companies

Degree of

100%

0%

Public company Mixed-economy company Private company

independence

Aus: Thommen/Grösser: Economy · Company · Management, 2014 3

© Versus Verlag 2019

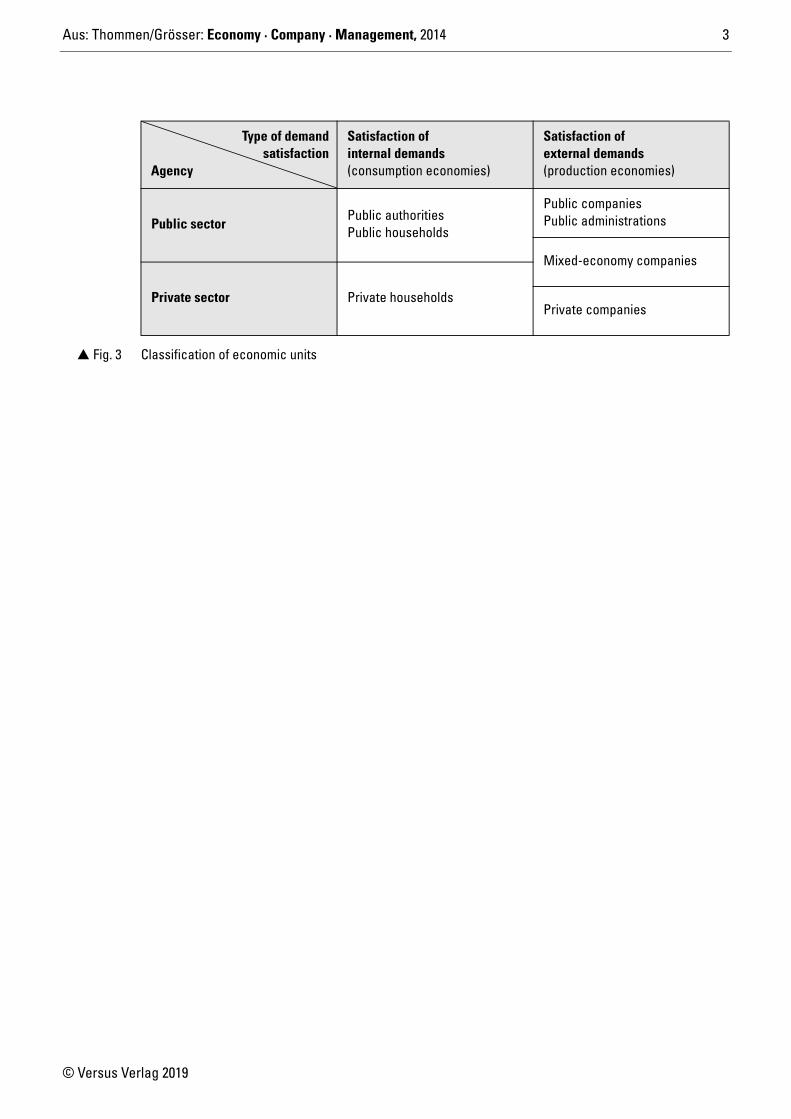

Satisfaction of internal demands(consumption economies)

Satisfaction of external demands(production economies)

Public sectorPublic authorities Public households

Public companiesPublic administrations

Mixed-economy companies

Private sector Private householdsPrivate companies

� Fig. 3 Classification of economic units

Type of demandsatisfaction

Agency

Aus: Thommen/Grösser: Economy · Company · Management, 2014 4

© Versus Verlag 2019

� Fig. 4 A new thinking paradigm (Backhausen/Thommen 2006, pp. 50; Groesser/Schaffernicht 2012)

We normally consider our daily experiences as if theywere shaped by the law of proportional effects: A gentletap with a hammer (or just a suggestion) drives the nail (orthought) a little bit deeper into the wood (or mind), whilea hard stroke has a correspondingly stronger effect.

Such proportionality can be mathematically repre-sented as a linear function, which is graphically repre-sented as a straight line. All processes that can be repre-sented in this way are described as linear processes.Their biggest advantage is that they are easy to compre-hend and calculate and therefore ensure an ability to act.

The example of the hammer strike (suggestion) showsthat the application of this kind of thinking to human com-munication seems convincing at first glance. This modelis used in education and training to teach us how theworld “works”. This concept does indeed apply to a largepart of our life experience, in particular when we are in a“stable situation”: the more you practise, the better itgets, the harder you try, the higher the effect, the strongerthe blow, the deeper the nail or thought will penetrate. Allother events around us can be disregarded. This is theway to develop world views and action models and theway to deal with colleagues or to guide employees; thispattern is used to make decisions. Deviating experiencesare rejected as exceptions or special cases – or providereasons to adapt and improve the models.

Proportionality is the consistent and binding patternused to explain dynamic processes and linear thinkingis still the common measure for professional behaviour.

Things started to change at the beginning of the 20th cen-tury. The revolution started in physics, where the verysmall deviations from the classical theories at first gaveonly a vague indication of a need for change, but latercauses a completely unexpected paradigm shift. Almostall of the physical view of the world was destroyed andquantum mechanics created a new, non-linear way ofthinking as the basis for modern physics. Scientists arestill cleaning up the fallout and system-based, construc-

tive thinking is to some extent a long-term effect of theseevents.

Small deviations have disproportionally large effects,consequences can no longer be foreseen in a linearway.

There is no doubt that the old models led to impressivesuccess in terms of understanding technology. However,we can see today that their usefulness was restricted toonly a small part of the world.

The physics example might suggest that it only dealswith an exceptional situation and that in everyday life,where people do not deal with atoms but with otherpeople, linear models are still good enough to cope.However, the transformations in the areas we are inter-ested in are likely to be even more severe than those inthe sciences.

This is not yet obvious, as many sociologists, econo-mists and cultural experts still rely on the concept ofproportionality of cause and effect and hope that theycan avoid restructuring their fields in the way thatbecame necessary in the science field. The linear modelis defended and the more complex non-linear thinking isregarded as too theory-based and impractical. Newattempts have been hesitant to date.

The reason for this persistence is obvious: linearitypromises to make it possible to plan and manage thedifficult field of human interaction and thus promisessecurity. However, it is becoming increasingly obviousthat linear thinking is becoming too restrictive, particu-larly in the social and economic field. The phenomenon ofincreasing complexity is decisive in this regard. It refersto processes that are highly dependent on interactionwith other equally complex processes and often have aninfluence on these processes as well. This creates feed-back loops that are difficult to comprehend. This is oftenaggravated by time delays that tend to obfuscate thedirect influences.

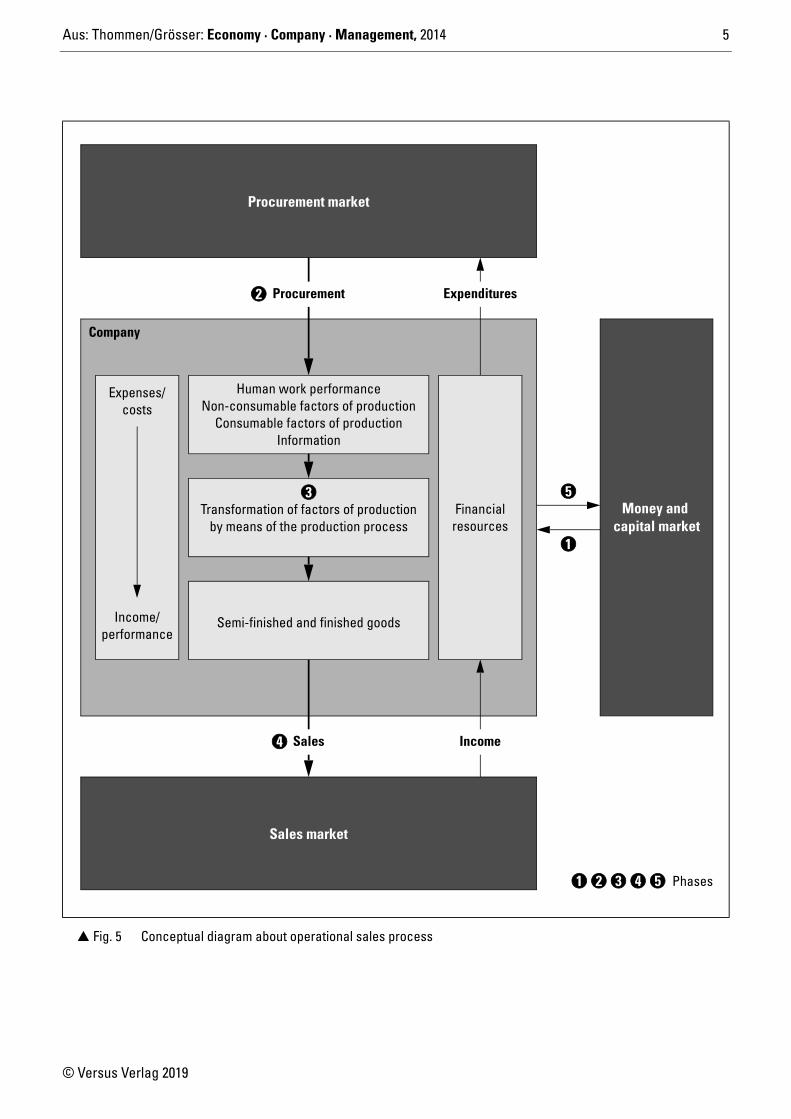

Aus: Thommen/Grösser: Economy · Company · Management, 2014 5

© Versus Verlag 2019

� Fig. 5 Conceptual diagram about operational sales process

Procurement market

Expenses/costs

Income/performance

Human work performanceNon-consumable factors of production

Consumable factors of productionInformation

Transformation of factors of productionby means of the production process

Semi-finished and finished goods

Financialresources

Money and

Sales Income

Sales market

Procurement Expenditures

capital market

Company

Phases1 2 3 4 5

1

2

4

53

Aus: Thommen/Grösser: Economy · Company · Management, 2014 6

© Versus Verlag 2019

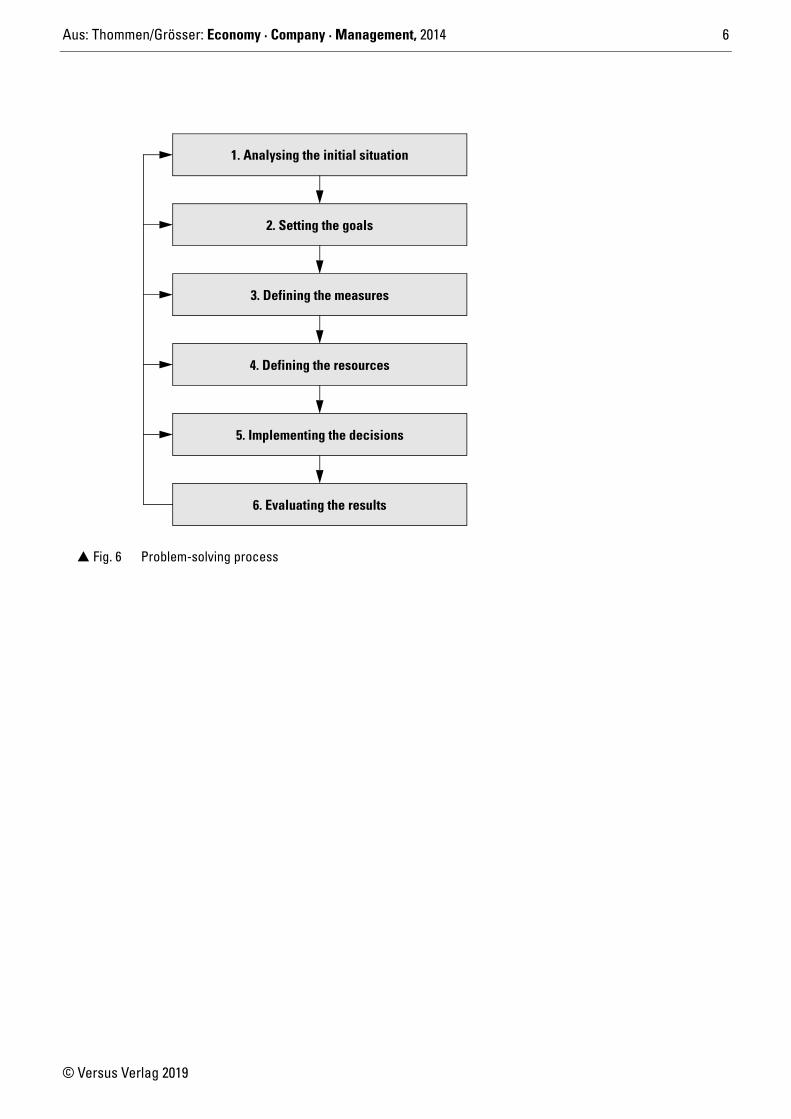

� Fig. 6 Problem-solving process

2. Setting the goals

6. Evaluating the results

5. Implementing the decisions

4. Defining the resources

3. Defining the measures

1. Analysing the initial situation

Aus: Thommen/Grösser: Economy · Company · Management, 2014 7

© Versus Verlag 2019

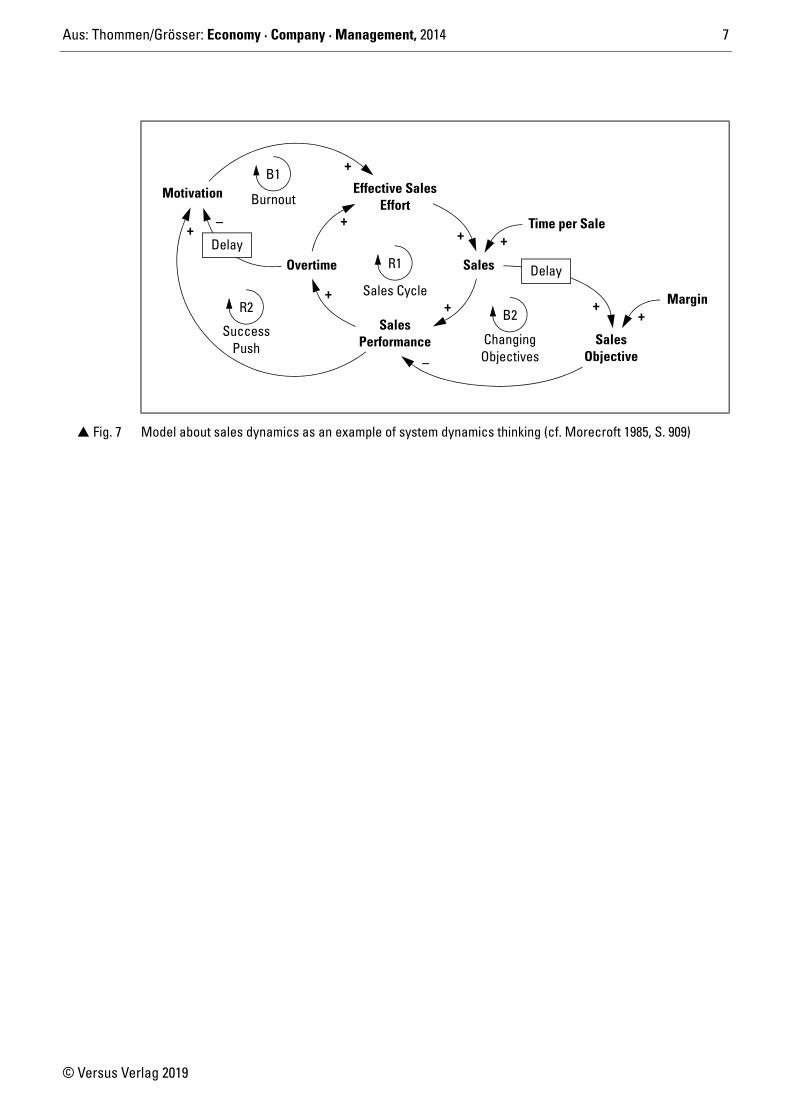

� Fig. 7 Model about sales dynamics as an example of system dynamics thinking (cf. Morecroft 1985, S. 909)

Effective SalesMotivation Burnout

Success

Overtime

SalesChangingObjectives

Sales

Sales

Margin

Time per Sale

Sales Cycle

Push

B1

R1

B2R2

Effort

Performance

++

++

Delay

+

+–

Objective

Delay

+

–

+

+

Aus: Thommen/Grösser: Economy · Company · Management, 2014 8

© Versus Verlag 2019

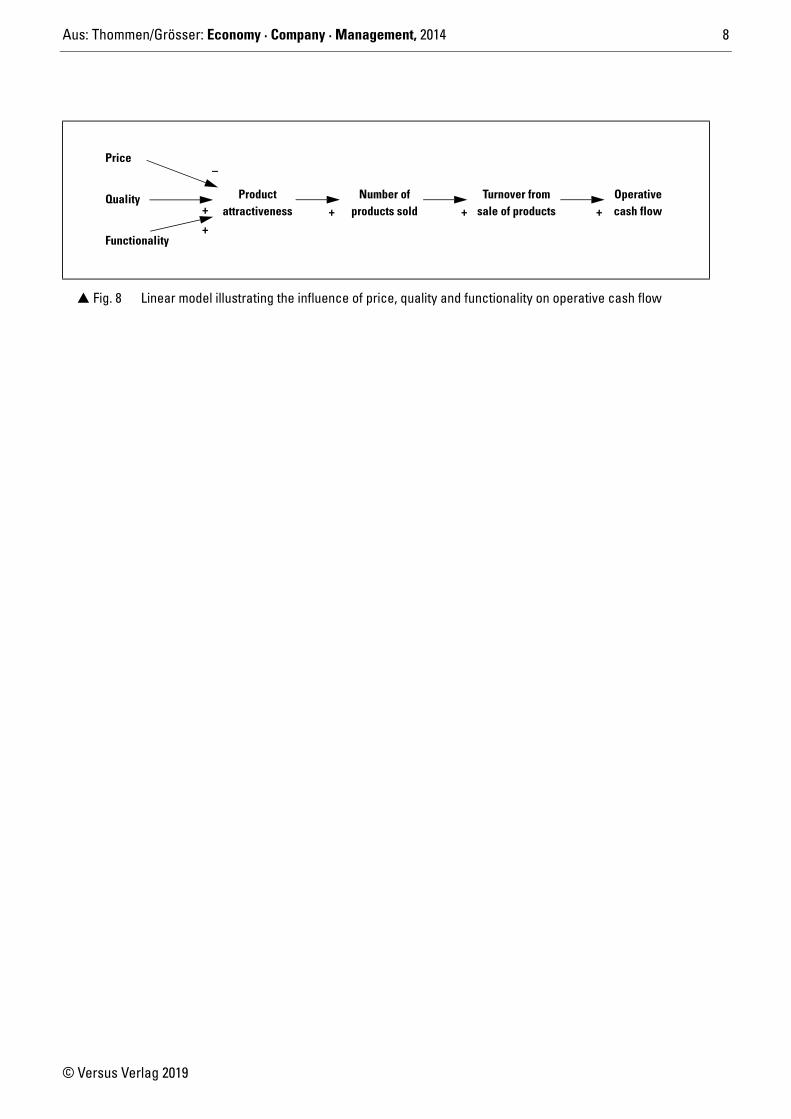

� Fig. 8 Linear model illustrating the influence of price, quality and functionality on operative cash flow

Product

Price

attractiveness +Quality

Functionality

Number ofproducts sold

Turnover fromsale of products

Operativecash flow+ +

+

+

–

Aus: Thommen/Grösser: Economy · Company · Management, 2014 9

© Versus Verlag 2019

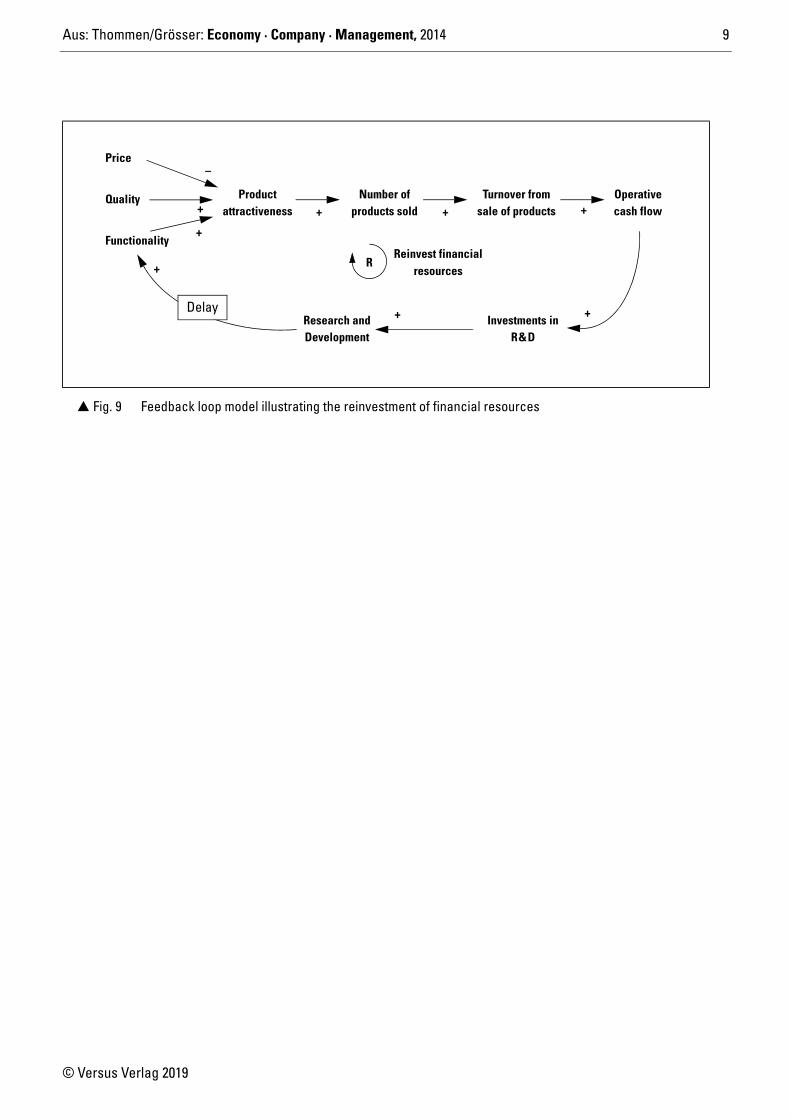

� Fig. 9 Feedback loop model illustrating the reinvestment of financial resources

Product

Price

attractiveness +Quality

Functionality

Number ofproducts sold

Turnover fromsale of products

Operativecash flow+ +

+

+

–

Reinvest financialresources

R

Investments inR&D

Research andDevelopment

+

+Delay +

Aus: Thommen/Grösser: Economy · Company · Management, 2014 10

© Versus Verlag 2019

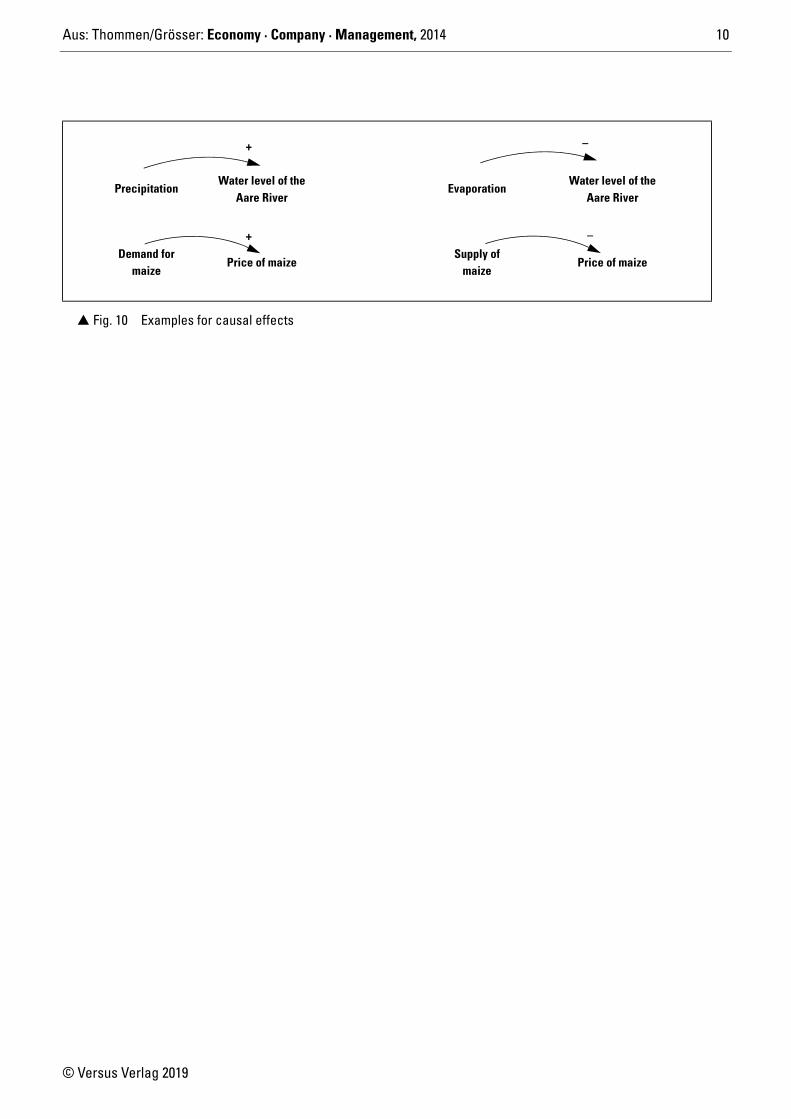

� Fig. 10 Examples for causal effects

Precipitation

Price of maizeDemand for

maize

Water level of theAare River

Evaporation

Supply ofmaize

Price of maize

Water level of theAare River

+

+ –

–

Aus: Thommen/Grösser: Economy · Company · Management, 2014 11

© Versus Verlag 2019

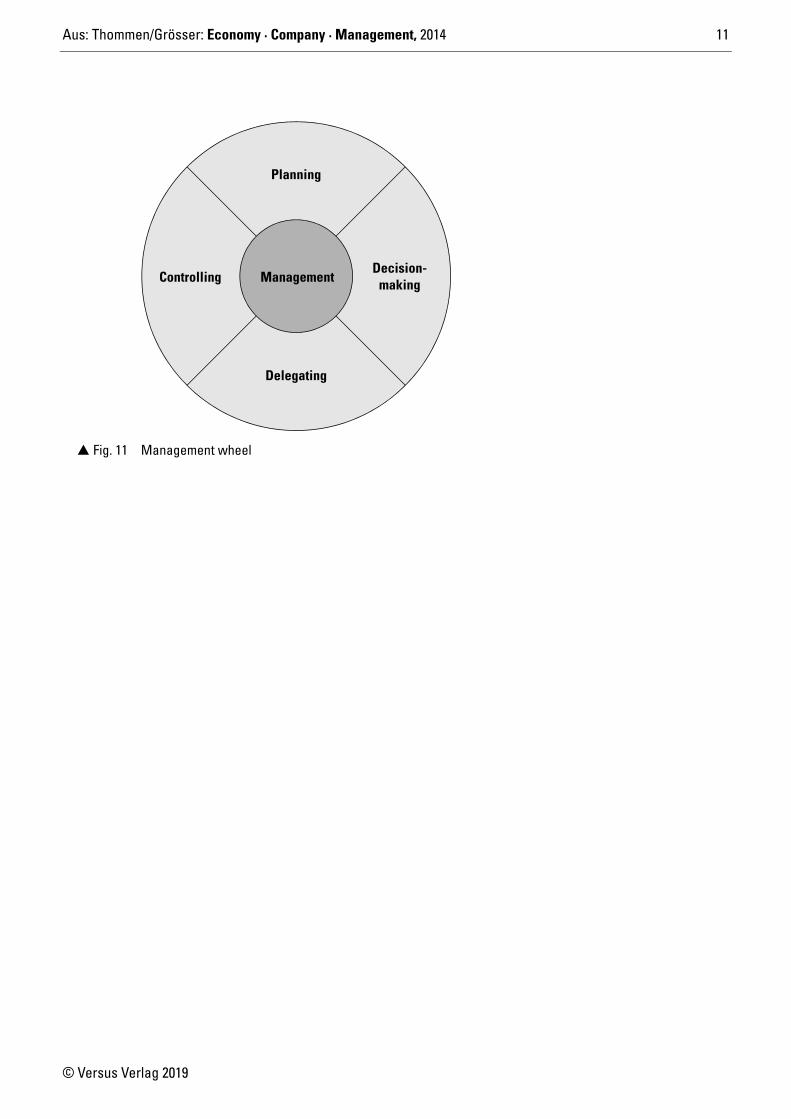

� Fig. 11 Management wheel

Management

Planning

Delegating

ControllingDecision-

making

Aus: Thommen/Grösser: Economy · Company · Management, 2014 12

© Versus Verlag 2019

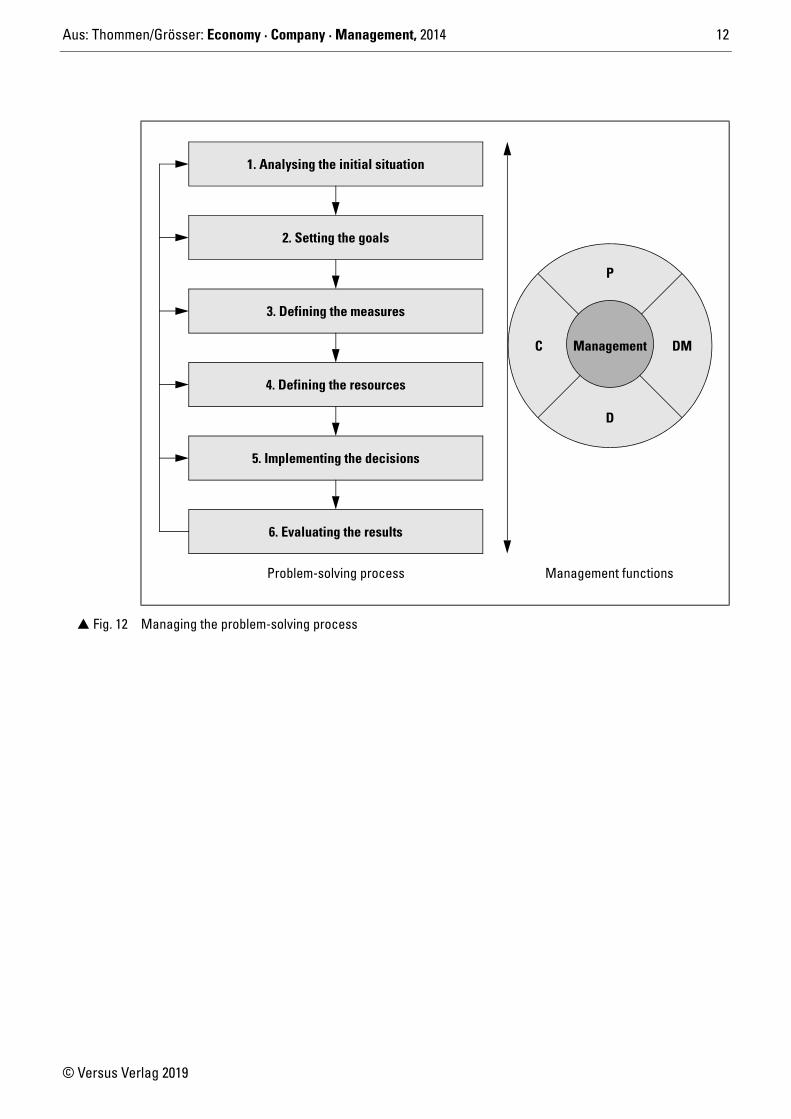

� Fig. 12 Managing the problem-solving process

Management

P

D

C DM

2. Setting the goals

6. Evaluating the results

5. Implementing the decisions

4. Defining the resources

3. Defining the measures

1. Analysing the initial situation

Problem-solving process Management functions

Aus: Thommen/Grösser: Economy · Company · Management, 2014 13

© Versus Verlag 2019

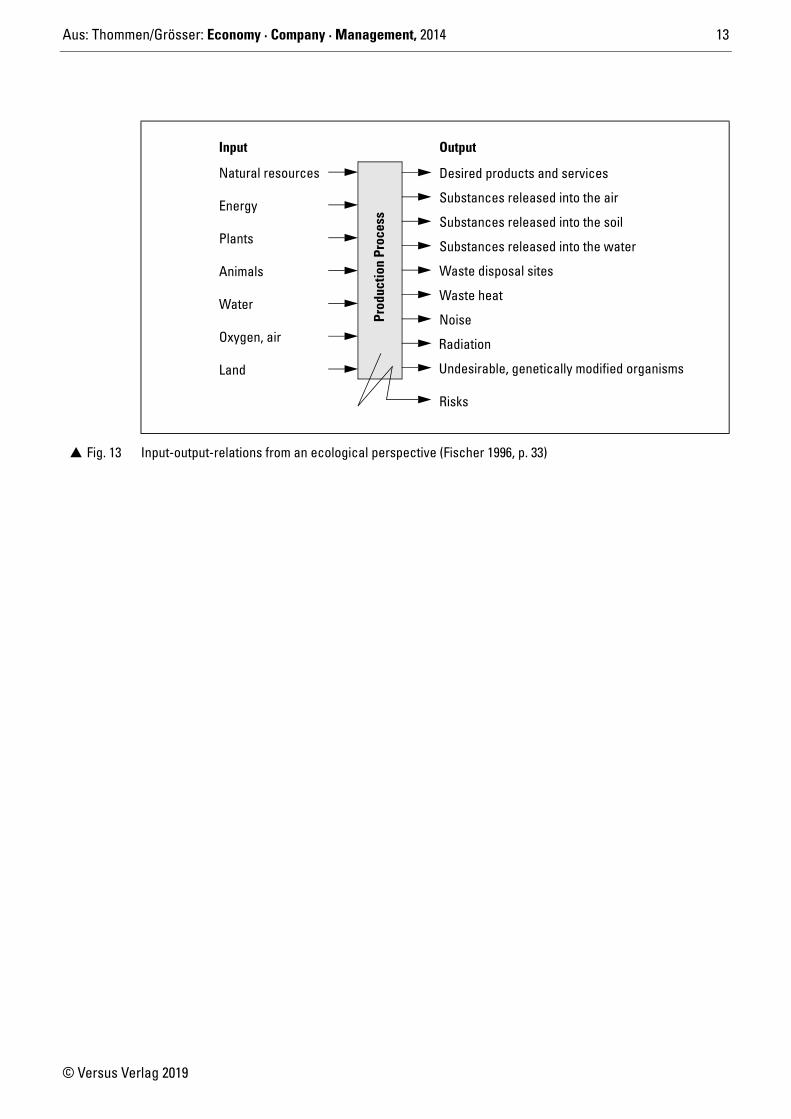

� Fig. 13 Input-output-relations from an ecological perspective (Fischer 1996, p. 33)

Input

Natural resources

Energy

Plants

Animals

Water

Oxygen, air

LandPr

oduc

tion

Proc

ess

Output

Desired products and services

Substances released into the air

Substances released into the soil

Substances released into the water

Waste disposal sites

Waste heat

Noise

Radiation

Undesirable, genetically modified organisms

Risks

Aus: Thommen/Grösser: Economy · Company · Management, 2014 14

© Versus Verlag 2019

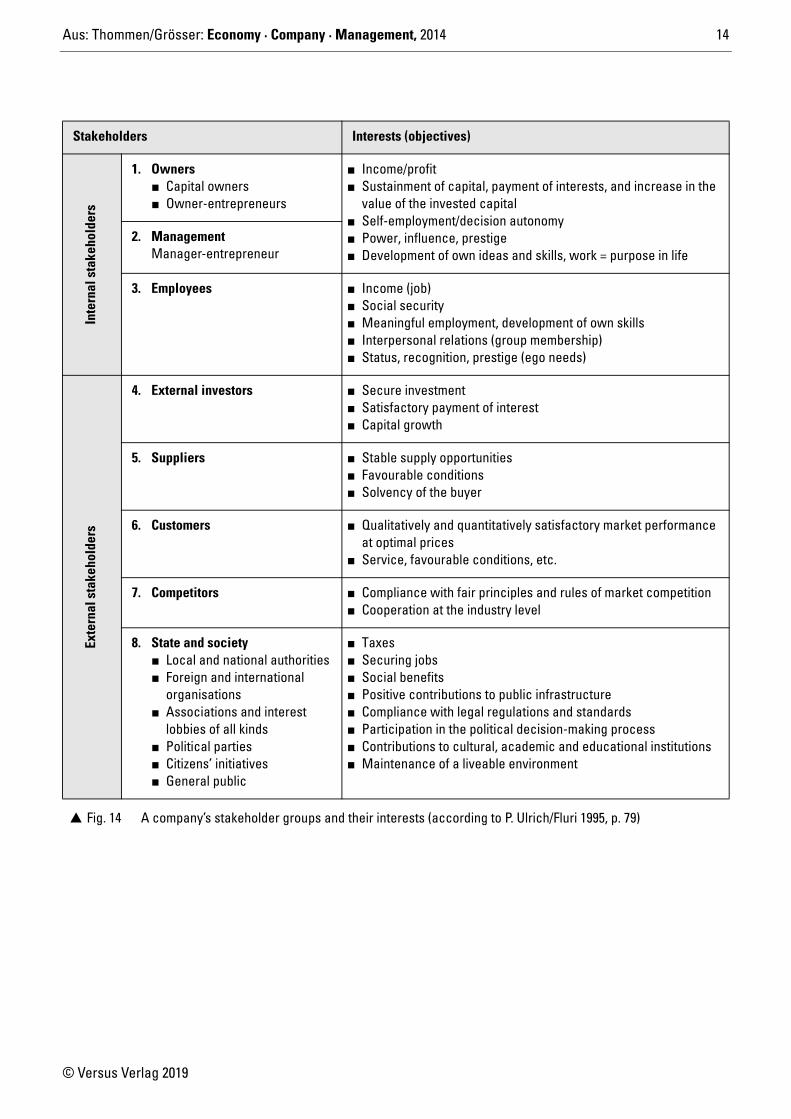

Stakeholders Interests (objectives)

Inte

rnal

sta

keho

lder

s

1. Owners� Capital owners� Owner-entrepreneurs

� Income/profit� Sustainment of capital, payment of interests, and increase in the

value of the invested capital� Self-employment/decision autonomy� Power, influence, prestige� Development of own ideas and skills, work = purpose in life

2. Management Manager-entrepreneur

3. Employees � Income (job)� Social security� Meaningful employment, development of own skills� Interpersonal relations (group membership)� Status, recognition, prestige (ego needs)

Exte

rnal

sta

keho

lder

s

4. External investors � Secure investment� Satisfactory payment of interest� Capital growth

5. Suppliers � Stable supply opportunities� Favourable conditions� Solvency of the buyer

6. Customers � Qualitatively and quantitatively satisfactory market performance at optimal prices

� Service, favourable conditions, etc.

7. Competitors � Compliance with fair principles and rules of market competition� Cooperation at the industry level

8. State and society� Local and national authorities� Foreign and international

organisations� Associations and interest

lobbies of all kinds� Political parties� Citizens’ initiatives� General public

� Taxes � Securing jobs� Social benefits� Positive contributions to public infrastructure� Compliance with legal regulations and standards� Participation in the political decision-making process� Contributions to cultural, academic and educational institutions� Maintenance of a liveable environment

� Fig. 14 A company’s stakeholder groups and their interests (according to P. Ulrich/Fluri 1995, p. 79)

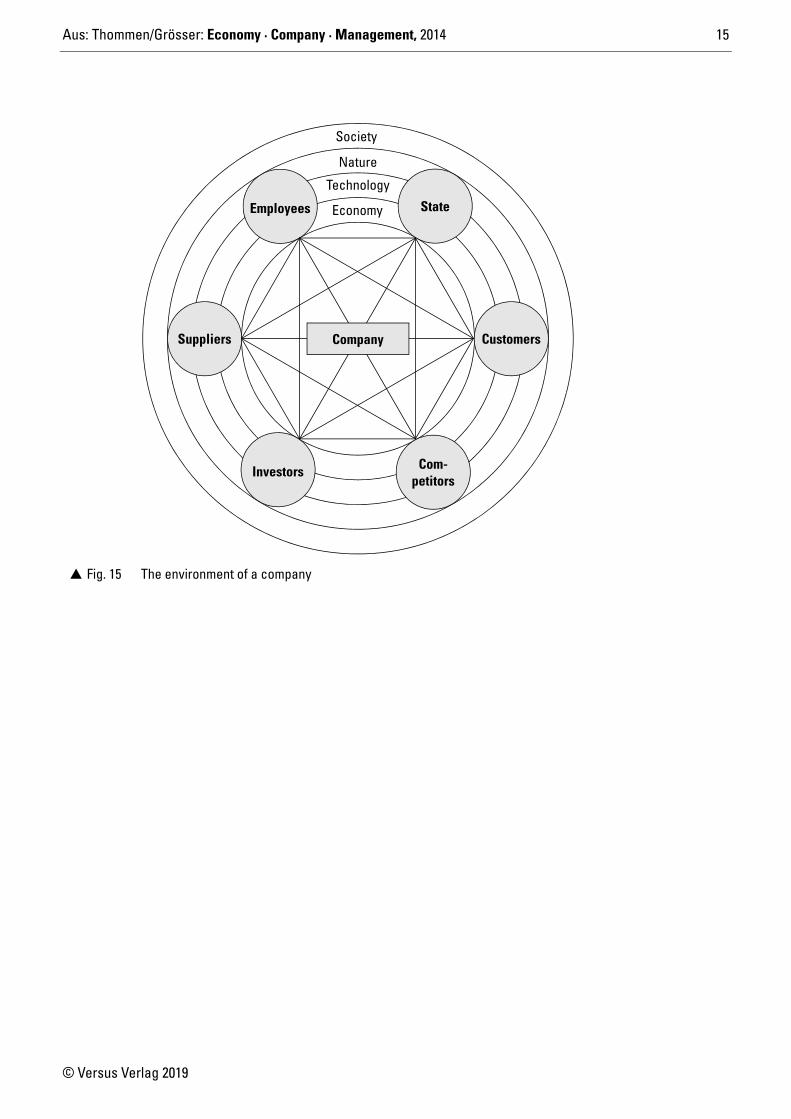

Aus: Thommen/Grösser: Economy · Company · Management, 2014 15

© Versus Verlag 2019

� Fig. 15 The environment of a company

Society

Nature

Technology

Economy State

Customers

Com-

Employees

Suppliers

Investors

Company

petitors

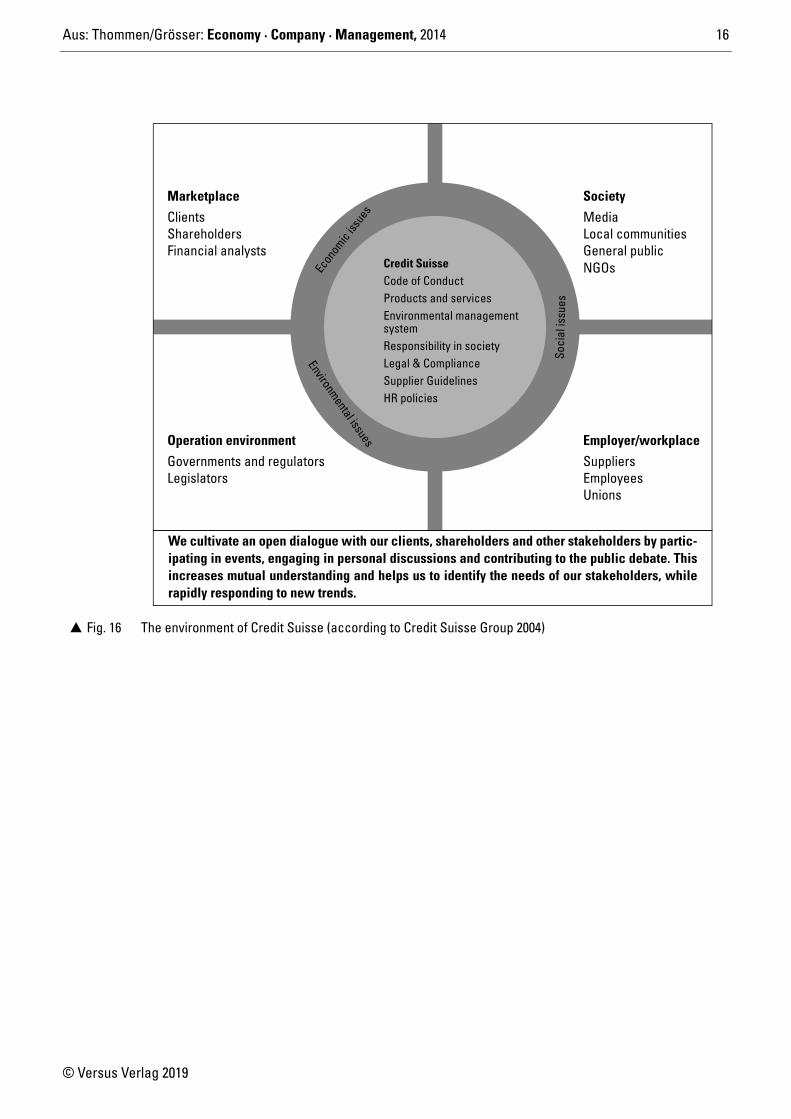

Aus: Thommen/Grösser: Economy · Company · Management, 2014 16

© Versus Verlag 2019

� Fig. 16 The environment of Credit Suisse (according to Credit Suisse Group 2004)

Credit Suisse

S oci

al is

sues

Environmental issues

Environmental managementsystem

Code of ConductProducts and services

Responsibility in societyLegal & ComplianceSupplier GuidelinesHR policies

Econ

omic

issue

s

SocietyMarketplace

Operation environment Employer/workplace

ShareholdersFinancial analysts

ClientsLocal communitiesGeneral public

Media

NGOs

LegislatorsGovernments and regulators

EmployeesUnions

Suppliers

We cultivate an open dialogue with our clients, shareholders and other stakeholders by partic-ipating in events, engaging in personal discussions and contributing to the public debate. Thisincreases mutual understanding and helps us to identify the needs of our stakeholders, whilerapidly responding to new trends.

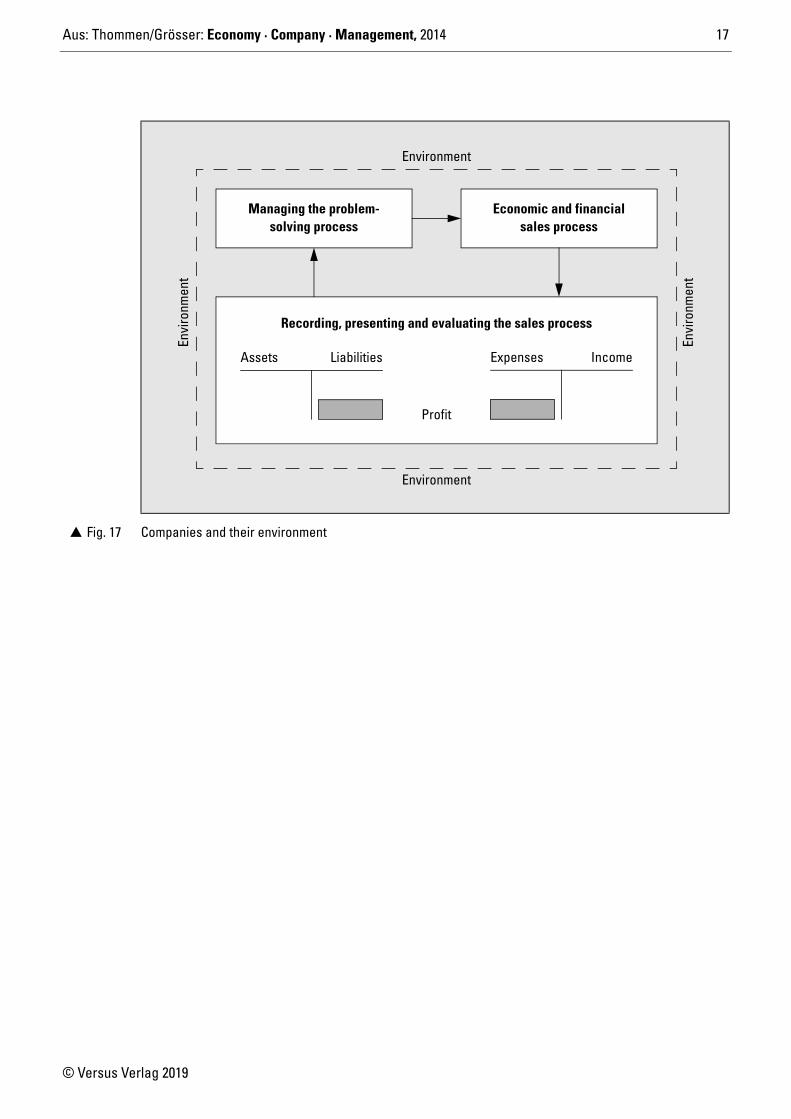

Aus: Thommen/Grösser: Economy · Company · Management, 2014 17

© Versus Verlag 2019

� Fig. 17 Companies and their environment

Environment

Envi

ronm

ent

Managing the problem-solving process

Economic and financialsales process

Recording, presenting and evaluating the sales process

Assets Liabilities

Profit

Expenses Income

Environment

Envi

ronm

ent

Aus: Thommen/Grösser: Economy · Company · Management, 2014 18

© Versus Verlag 2019

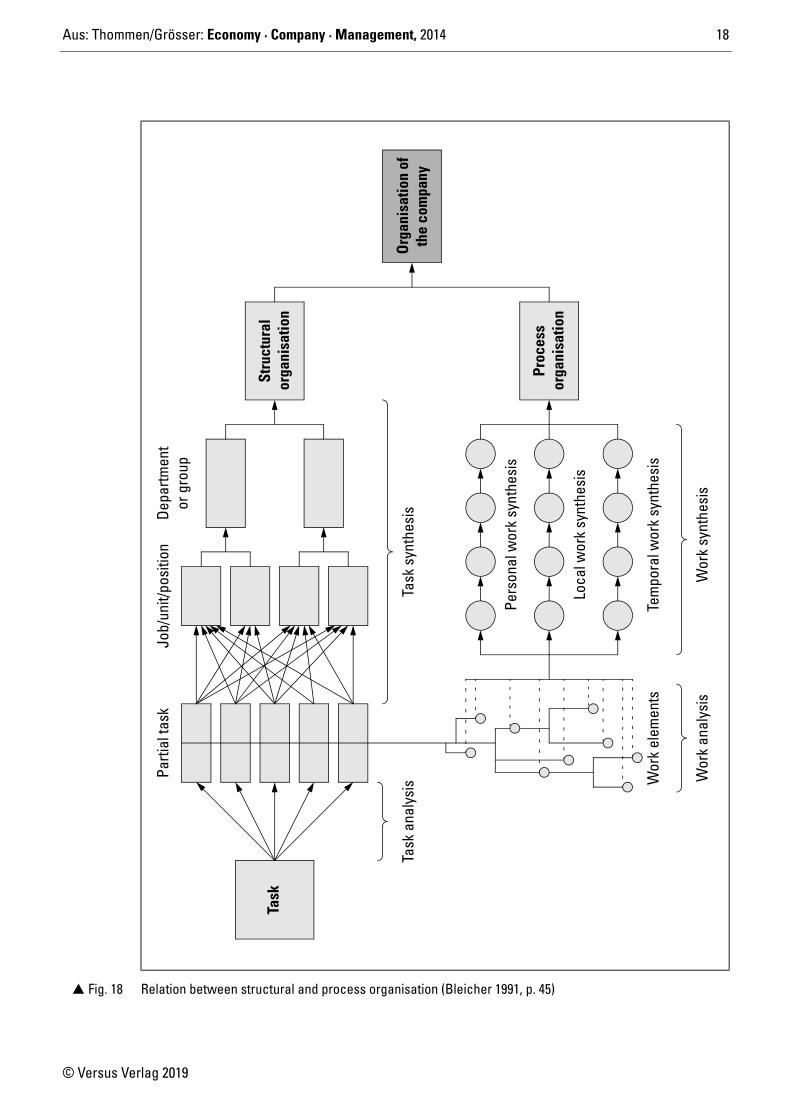

� Fig. 18 Relation between structural and process organisation (Bleicher 1991, p. 45)

Task

Org

anis

atio

n of

Stru

ctur

al

Depa

rtmen

tor

gro

upJo

b/un

it/po

sitio

nPa

rtial

task

Task

ana

lysi

sTa

sk s

ynth

esis

Pers

onal

wor

k sy

nthe

sis

Loca

l wor

k sy

nthe

sis

Tem

pora

l wor

k sy

nthe

sis

Wor

k el

emen

ts

Wor

k an

alys

isW

ork

synt

hesi

s

orga

nisa

tion

the

com

pany

Proc

ess

orga

nisa

tion

Aus: Thommen/Grösser: Economy · Company · Management, 2014 19

© Versus Verlag 2019

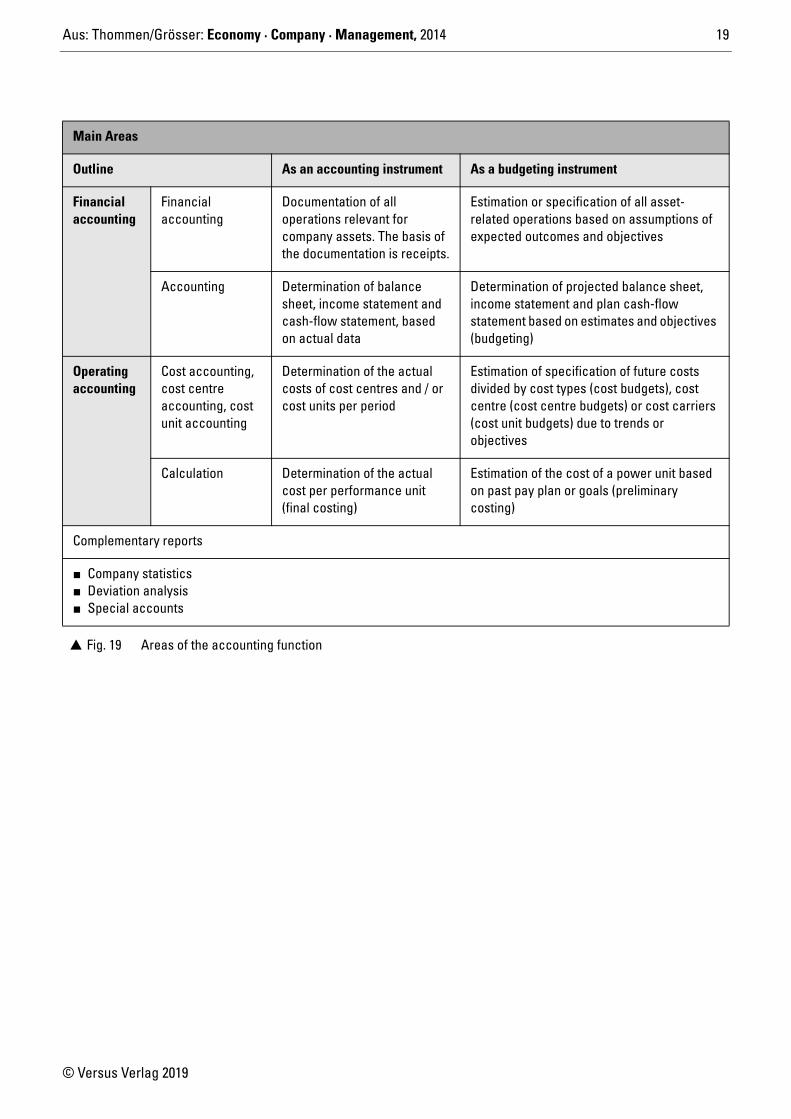

Main Areas

Outline As an accounting instrument As a budgeting instrument

Financial accounting

Financial accounting

Documentation of all operations relevant for company assets. The basis of the documentation is receipts.

Estimation or specification of all asset-related operations based on assumptions of expected outcomes and objectives

Accounting Determination of balance sheet, income statement and cash-flow statement, based on actual data

Determination of projected balance sheet, income statement and plan cash-flow statement based on estimates and objectives (budgeting)

Operating accounting

Cost accounting, cost centre accounting, cost unit accounting

Determination of the actual costs of cost centres and / or cost units per period

Estimation of specification of future costs divided by cost types (cost budgets), cost centre (cost centre budgets) or cost carriers (cost unit budgets) due to trends or objectives

Calculation Determination of the actual cost per performance unit (final costing)

Estimation of the cost of a power unit based on past pay plan or goals (preliminary costing)

Complementary reports

� Company statistics � Deviation analysis� Special accounts

� Fig. 19 Areas of the accounting function

Aus: Thommen/Grösser: Economy · Company · Management, 2014 20

© Versus Verlag 2019

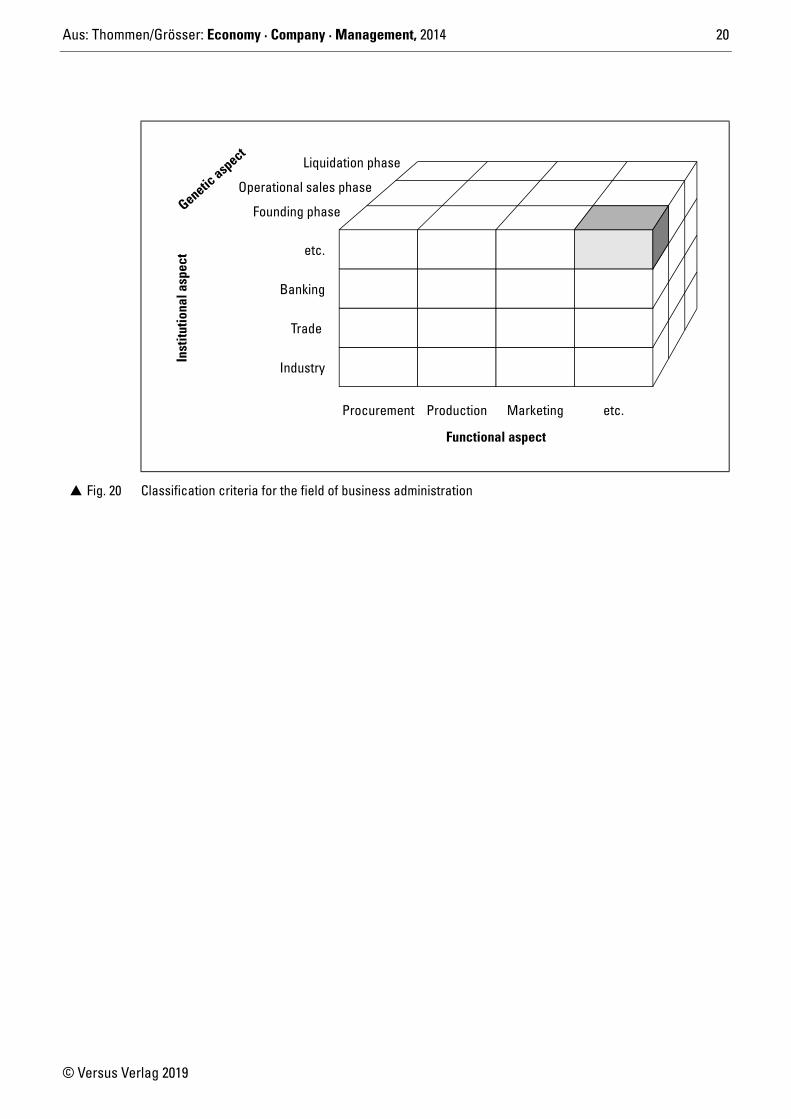

� Fig. 20 Classification criteria for the field of business administration

Procurement Production Marketing etc.

Inst

itutio

nal a

spec

t etc.

Banking

Trade

Industry

Liquidation phase

Operational sales phase

Founding phaseGenetic asp

ect

Functional aspect

Aus: Thommen/Grösser: Economy · Company · Management, 2014 21

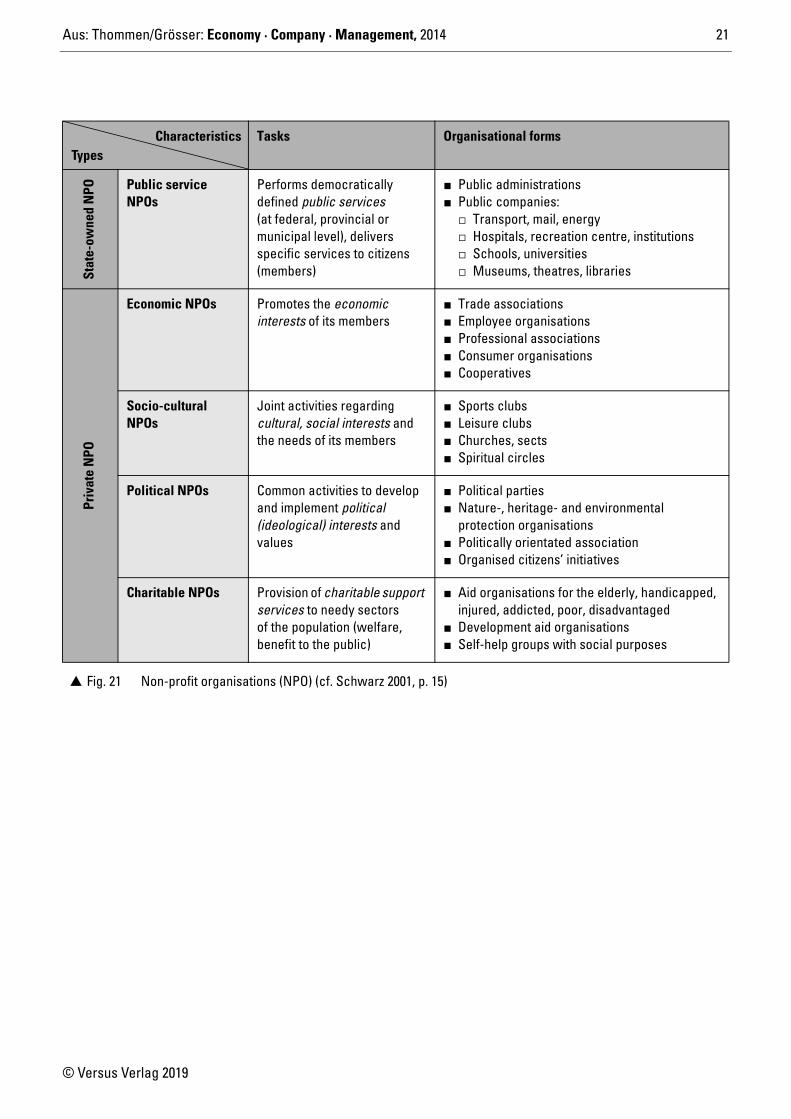

© Versus Verlag 2019

Tasks Organisational forms

Stat

e-ow

ned

NPO Public service

NPOsPerforms democratically defined public services (at federal, provincial or municipal level), delivers specific services to citizens (members)

� Public administrations� Public companies:

� Transport, mail, energy� Hospitals, recreation centre, institutions� Schools, universities� Museums, theatres, libraries

Priv

ate

NPO

Economic NPOs Promotes the economic interests of its members

� Trade associations� Employee organisations� Professional associations� Consumer organisations� Cooperatives

Socio-culturalNPOs

Joint activities regarding cultural, social interests and the needs of its members

� Sports clubs� Leisure clubs� Churches, sects� Spiritual circles

Political NPOs Common activities to develop and implement political (ideological) interests and values

� Political parties� Nature-, heritage- and environmental

protection organisations� Politically orientated association� Organised citizens’ initiatives

Charitable NPOs Provision of charitable support services to needy sectors of the population (welfare, benefit to the public)

� Aid organisations for the elderly, handicapped, injured, addicted, poor, disadvantaged

� Development aid organisations� Self-help groups with social purposes

� Fig. 21 Non-profit organisations (NPO) (cf. Schwarz 2001, p. 15)

CharacteristicsTypes

Aus: Thommen/Grösser: Economy · Company · Management, 2014 22

© Versus Verlag 2019

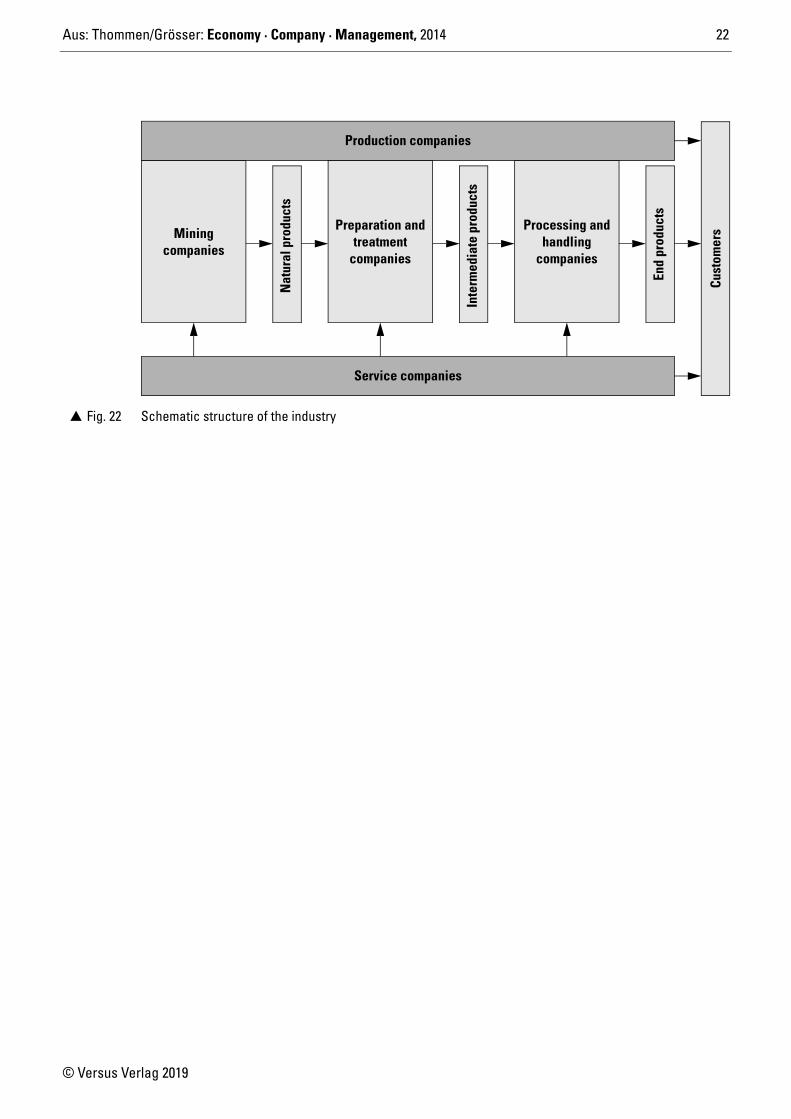

� Fig. 22 Schematic structure of the industry

Production companies

Miningcompanies

Nat

ural

pro

duct

s

Preparation andtreatment

Inte

rmed

iate

pro

duct

s

Processing andhandling

End

prod

ucts

Service companies

Cust

omer

s

companiescompanies

Aus: Thommen/Grösser: Economy · Company · Management, 2014 23

© Versus Verlag 2019

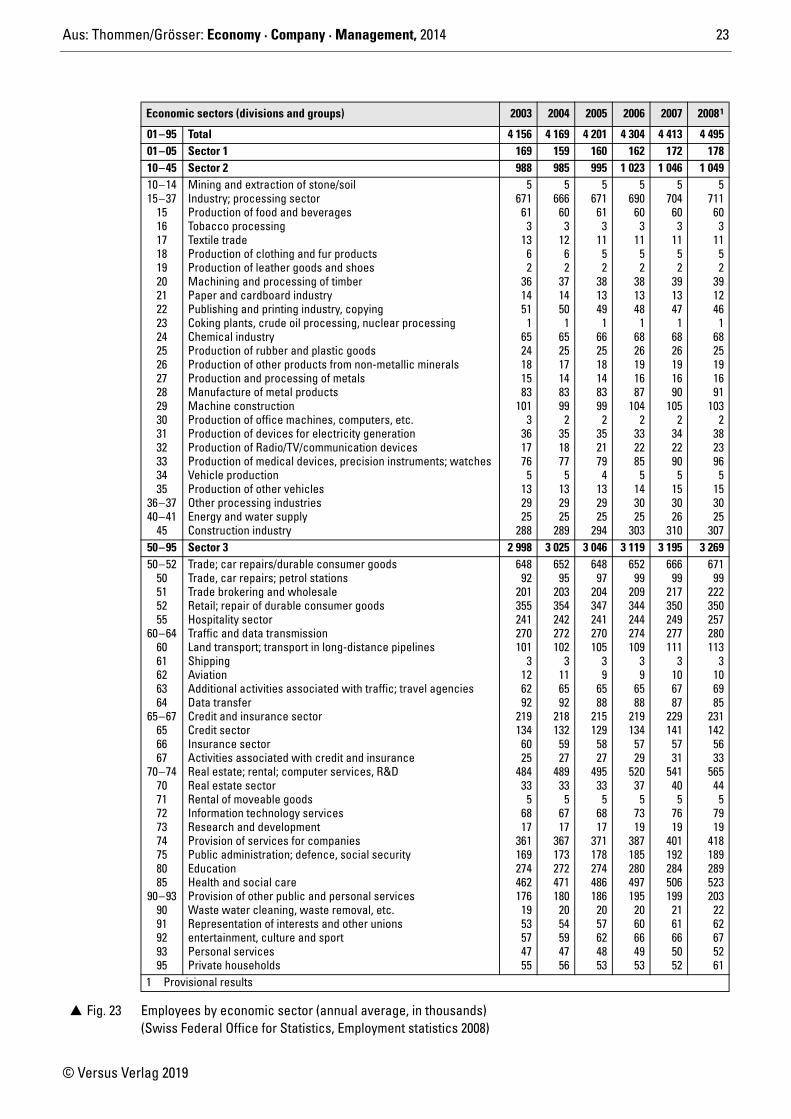

Economic sectors (divisions and groups) 2003 2004 2005 2006 2007 20081

01–95 Total 4 156 4 169 4 201 4 304 4 413 4 49501–05 Sector 1 169 159 160 162 172 17810–45 Sector 2 988 985 995 1 023 1 046 1 04910–1415–37

151617181920212223242526272829303132333435

36–3740–41

45

Mining and extraction of stone/soilIndustry; processing sectorProduction of food and beveragesTobacco processingTextile tradeProduction of clothing and fur productsProduction of leather goods and shoesMachining and processing of timberPaper and cardboard industryPublishing and printing industry, copyingCoking plants, crude oil processing, nuclear processingChemical industryProduction of rubber and plastic goodsProduction of other products from non-metallic mineralsProduction and processing of metalsManufacture of metal productsMachine constructionProduction of office machines, computers, etc.Production of devices for electricity generationProduction of Radio/TV/communication devicesProduction of medical devices, precision instruments; watchesVehicle productionProduction of other vehiclesOther processing industriesEnergy and water supplyConstruction industry

567161

313

62

361451

16524181583

1013

361776

5132925

288

5666603

1262

3714501

6525171483992

3518775

132925

289

5671

613

1152

3813491

6625181483992

3521794

132925

294

569060

311

52

381348

16826191687

1042

332285

5143025

303

5704603

1152

3913471

6826191690

1052

3422905

153026

310

5711603

1152

3912461

6825191691

1032

3823965

153025

30750–95 Sector 3 2 998 3 025 3 046 3 119 3 195 3 26950–52

50515255

60–646061626364

65–67656667

70–747071727374758085

90–939091929395

Trade; car repairs/durable consumer goodsTrade, car repairs; petrol stationsTrade brokering and wholesaleRetail; repair of durable consumer goodsHospitality sectorTraffic and data transmissionLand transport; transport in long-distance pipelinesShippingAviationAdditional activities associated with traffic; travel agenciesData transferCredit and insurance sectorCredit sectorInsurance sectorActivities associated with credit and insuranceReal estate; rental; computer services, R&DReal estate sectorRental of moveable goodsInformation technology servicesResearch and developmentProvision of services for companiesPublic administration; defence, social securityEducationHealth and social careProvision of other public and personal servicesWaste water cleaning, waste removal, etc.Representation of interests and other unionsentertainment, culture and sportPersonal servicesPrivate households

64892

201355241270101

3126292

2191346025

48433

56817

3611692744621761953574755

65295

203354242272102

3116592

2181325927

489335

6717

3671732724711802054594756

64897

204347241270105

39

6588

215129

5827

495335

6817

371178274486186

2057624853

65299

209344244274109

39

6588

2191345729

52037

57319

3871852804971952060664953

66699

217350249277111

3106787

2291415731

541405

7619

4011922845061992161665052

67199

222350257280113

3106985

2311425633

565445

7919

4181892895232032262675261

1 Provisional results

� Fig. 23 Employees by economic sector (annual average, in thousands) (Swiss Federal Office for Statistics, Employment statistics 2008)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 24

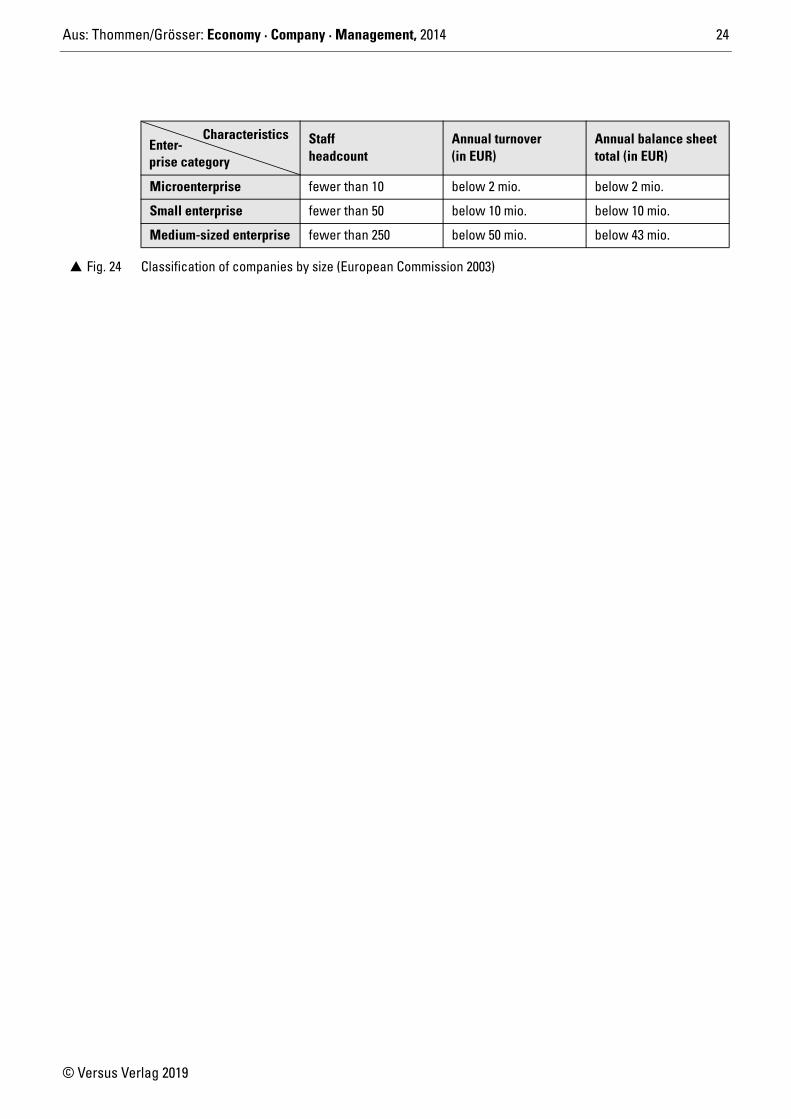

© Versus Verlag 2019

Staff headcount

Annual turnover(in EUR)

Annual balance sheet total (in EUR)

Microenterprise fewer than 10 below 2 mio. below 2 mio.

Small enterprise fewer than 50 below 10 mio. below 10 mio.

Medium-sized enterprise fewer than 250 below 50 mio. below 43 mio.

� Fig. 24 Classification of companies by size (European Commission 2003)

CharacteristicsEnter-prise category

Aus: Thommen/Grösser: Economy · Company · Management, 2014 25

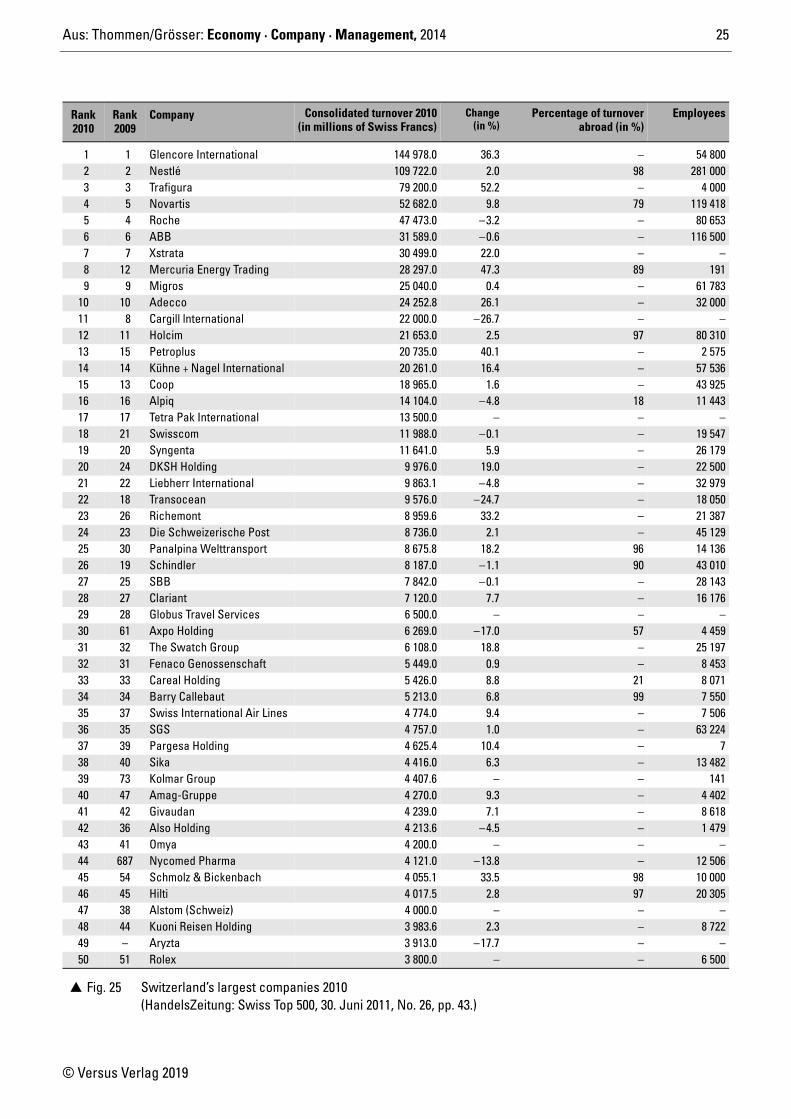

© Versus Verlag 2019

Rank2010

Rank2009

Company Consolidated turnover 2010(in millions of Swiss Francs)

Change(in %)

Percentage of turnoverabroad (in %)

Employees

1 1 Glencore International 144 978.0 36.3 – 54 8002 2 Nestlé 109 722.0 2.0 98 281 0003 3 Trafigura 79 200.0 52.2 – 4 0004 5 Novartis 52 682.0 9.8 79 119 4185 4 Roche 47 473.0 –3.2 – 80 6536 6 ABB 31 589.0 –0.6 – 116 5007 7 Xstrata 30 499.0 22.0 – –8 12 Mercuria Energy Trading 28 297.0 47.3 89 1919 9 Migros 25 040.0 0.4 – 61 783

10 10 Adecco 24 252.8 26.1 – 32 00011 8 Cargill lnternational 22 000.0 –26.7 – –12 11 Holcim 21 653.0 2.5 97 80 31013 15 Petroplus 20 735.0 40.1 – 2 57514 14 Kühne + Nagel International 20 261.0 16.4 – 57 53615 13 Coop 18 965.0 1.6 – 43 92516 16 Alpiq 14 104.0 –4.8 18 11 44317 17 Tetra Pak International 13 500.0 – – –18 21 Swisscom 11 988.0 –0.1 – 19 54719 20 Syngenta 11 641.0 5.9 – 26 17920 24 DKSH Holding 9 976.0 19.0 – 22 50021 22 Liebherr International 9 863.1 –4.8 – 32 97922 18 Transocean 9 576.0 –24.7 – 18 05023 26 Richemont 8 959.6 33.2 – 21 38724 23 Die Schweizerische Post 8 736.0 2.1 – 45 12925 30 Panalpina Welttransport 8 675.8 18.2 96 14 13626 19 Schindler 8 187.0 –1.1 90 43 01027 25 SBB 7 842.0 –0.1 – 28 14328 27 Clariant 7 120.0 7.7 – 16 17629 28 Globus Travel Services 6 500.0 – – –30 61 Axpo Holding 6 269.0 –17.0 57 4 45931 32 The Swatch Group 6 108.0 18.8 – 25 19732 31 Fenaco Genossenschaft 5 449.0 0.9 – 8 45333 33 Careal Holding 5 426.0 8.8 21 8 07134 34 Barry Callebaut 5 213.0 6.8 99 7 55035 37 Swiss International Air Lines 4 774.0 9.4 – 7 50636 35 SGS 4 757.0 1.0 – 63 22437 39 Pargesa Holding 4 625.4 10.4 – 738 40 Sika 4 416.0 6.3 – 13 48239 73 Kolmar Group 4 407.6 – – 14140 47 Amag-Gruppe 4 270.0 9.3 – 4 40241 42 Givaudan 4 239.0 7.1 – 8 61842 36 Also Holding 4 213.6 –4.5 – 1 47943 41 Omya 4 200.0 – – –44 687 Nycomed Pharma 4 121.0 –13.8 – 12 50645 54 Schmolz & Bickenbach 4 055.1 33.5 98 10 00046 45 Hilti 4 017.5 2.8 97 20 30547 38 Alstom (Schweiz) 4 000.0 – – –48 44 Kuoni Reisen Holding 3 983.6 2.3 – 8 72249 – Aryzta 3 913.0 –17.7 – –50 51 Rolex 3 800.0 – – 6 500

� Fig. 25 Switzerland’s largest companies 2010 (HandelsZeitung: Swiss Top 500, 30. Juni 2011, No. 26, pp. 43.)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 26

© Versus Verlag 2019

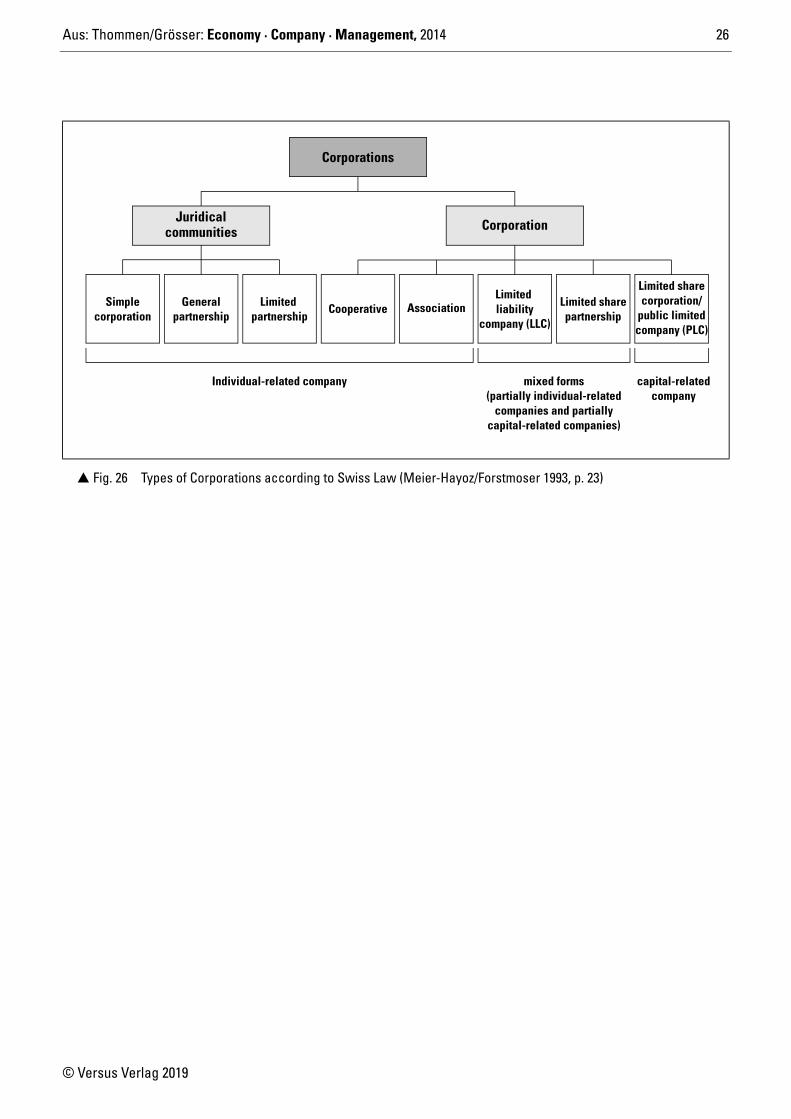

� Fig. 26 Types of Corporations according to Swiss Law (Meier-Hayoz/Forstmoser 1993, p. 23)

Corporations

CorporationJuridicalcommunities

Cooperative AssociationLimited liability

company (LLC)

Limited sharepartnership

Limited sharecorporation/

public limitedcompany (PLC)

Limited partnership

Generalpartnership

Simplecorporation

Individual-related company mixed forms(partially individual-related

companies and partiallycapital-related companies)

capital-relatedcompany

Aus: Thommen/Grösser: Economy · Company · Management, 2014 27

© Versus Verlag 2019

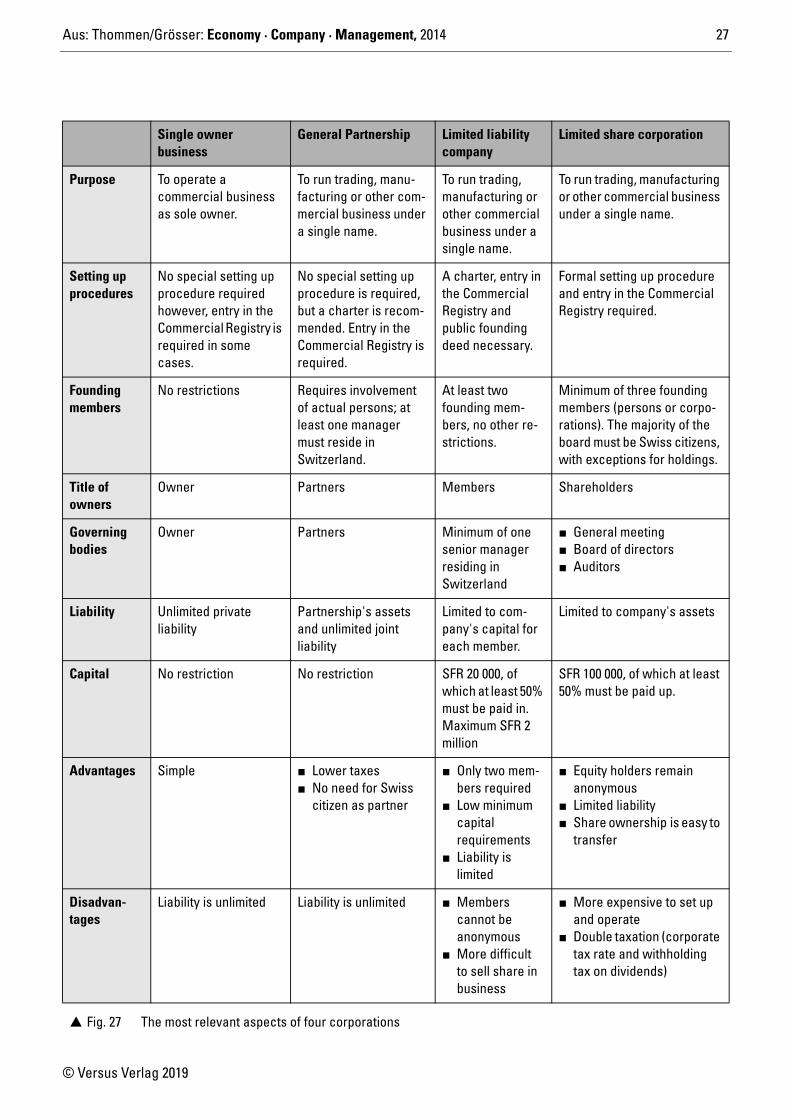

Single owner business

General Partnership Limited liability company

Limited share corporation

Purpose To operate a commercial business as sole owner.

To run trading, manu-facturing or other com-mercial business under a single name.

To run trading, manufacturing or other commercial business under a single name.

To run trading, manufacturing or other commercial business under a single name.

Setting up procedures

No special setting up procedure required however, entry in the Commercial Registry is required in some cases.

No special setting up procedure is required, but a charter is recom-mended. Entry in the Commercial Registry is required.

A charter, entry in the Commercial Registry and public founding deed necessary.

Formal setting up procedure and entry in the Commercial Registry required.

Founding members

No restrictions Requires involvement of actual persons; at least one manager must reside in Switzerland.

At least two founding mem-bers, no other re-strictions.

Minimum of three founding members (persons or corpo-rations). The majority of the board must be Swiss citizens, with exceptions for holdings.

Title of owners

Owner Partners Members Shareholders

Governing bodies

Owner Partners Minimum of one senior manager residing in Switzerland

� General meeting� Board of directors� Auditors

Liability Unlimited private liability

Partnership's assets and unlimited joint liability

Limited to com-pany's capital for each member.

Limited to company's assets

Capital No restriction No restriction SFR 20 000, of which at least 50% must be paid in. Maximum SFR 2 million

SFR 100 000, of which at least 50% must be paid up.

Advantages Simple � Lower taxes� No need for Swiss

citizen as partner

� Only two mem-bers required

� Low minimum capital requirements

� Liability is limited

� Equity holders remain anonymous

� Limited liability� Share ownership is easy to

transfer

Disadvan-tages

Liability is unlimited Liability is unlimited � Members cannot be anonymous

� More difficult to sell share in business

� More expensive to set up and operate

� Double taxation (corporate tax rate and withholding tax on dividends)

� Fig. 27 The most relevant aspects of four corporations

Aus: Thommen/Grösser: Economy · Company · Management, 2014 28

© Versus Verlag 2019

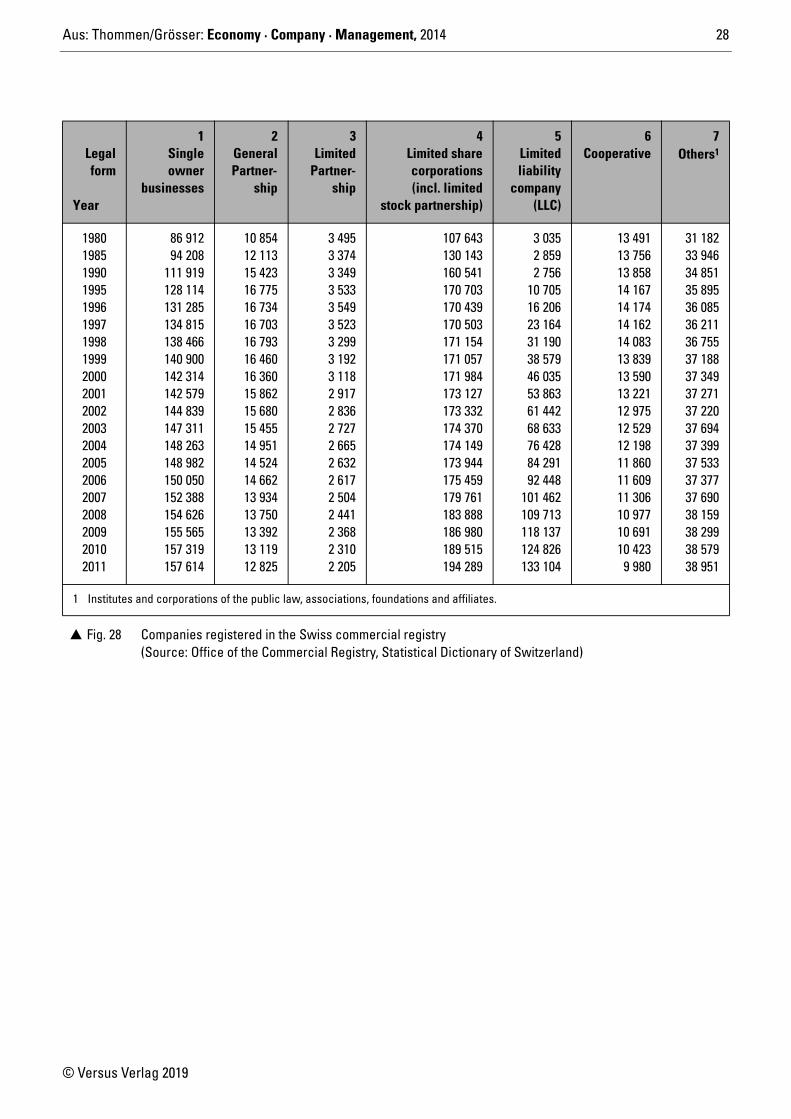

Legalform

Year

1Singleowner

businesses

2GeneralPartner-

ship

3Limited

Partner-ship

4Limited sharecorporations(incl. limited

stock partnership)

5Limitedliability

company(LLC)

6Cooperative

7Others1

19801985199019951996199719981999200020012002200320042005200620072008200920102011

86 91294 208

111 919128 114131 285134 815138 466140 900142 314142 579144 839147 311148 263148 982150 050152 388154 626155 565157 319157 614

10 85412 11315 42316 77516 73416 70316 79316 46016 36015 86215 68015 45514 95114 52414 66213 93413 75013 39213 11912 825

3 4953 3743 3493 5333 5493 5233 2993 1923 1182 9172 8362 7272 6652 6322 6172 5042 4412 3682 3102 205

107 643130 143160 541170 703170 439170 503171 154171 057171 984173 127173 332174 370174 149173 944175 459179 761183 888186 980189 515194 289

3 0352 8592 756

10 70516 20623 16431 19038 57946 03553 86361 44268 63376 42884 29192 448

101 462109 713118 137124 826133 104

13 49113 75613 85814 16714 17414 16214 08313 83913 59013 22112 97512 52912 19811 86011 60911 30610 97710 69110 423

9 980

31 18233 94634 85135 89536 08536 21136 75537 18837 34937 27137 22037 69437 39937 53337 37737 69038 15938 29938 57938 951

1 Institutes and corporations of the public law, associations, foundations and affiliates.

� Fig. 28 Companies registered in the Swiss commercial registry (Source: Office of the Commercial Registry, Statistical Dictionary of Switzerland)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 29

© Versus Verlag 2019

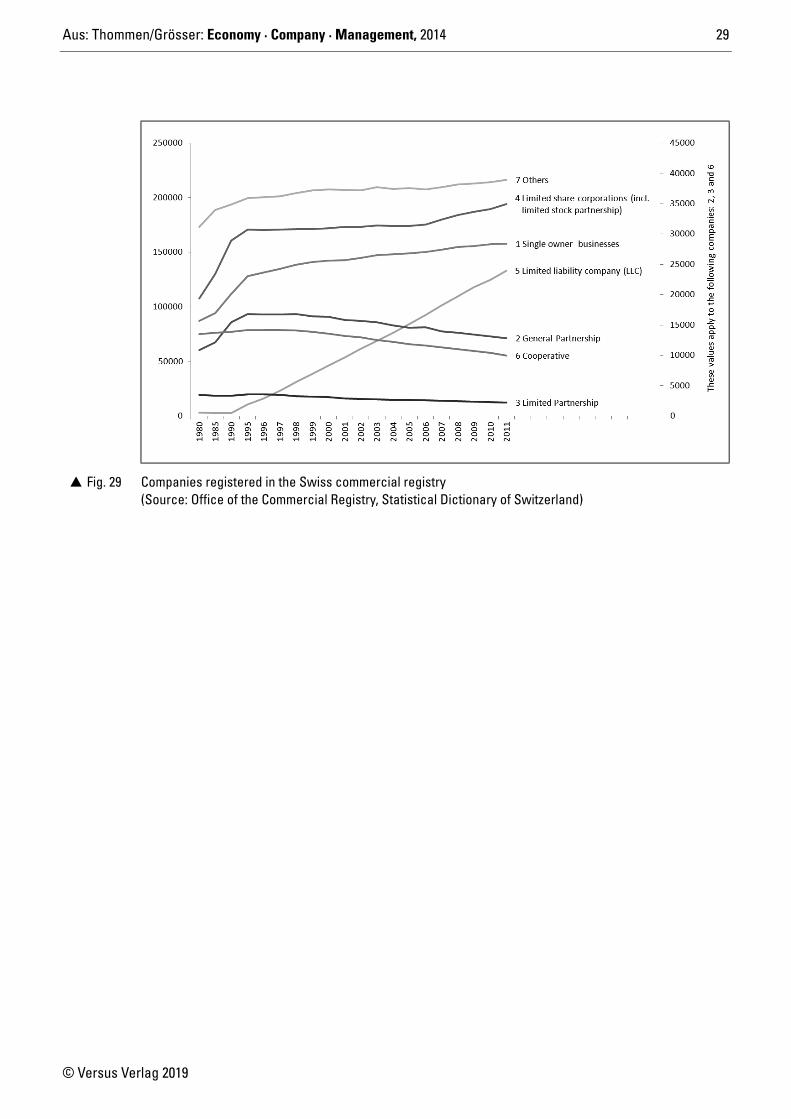

� Fig. 29 Companies registered in the Swiss commercial registry (Source: Office of the Commercial Registry, Statistical Dictionary of Switzerland)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 30

© Versus Verlag 2019

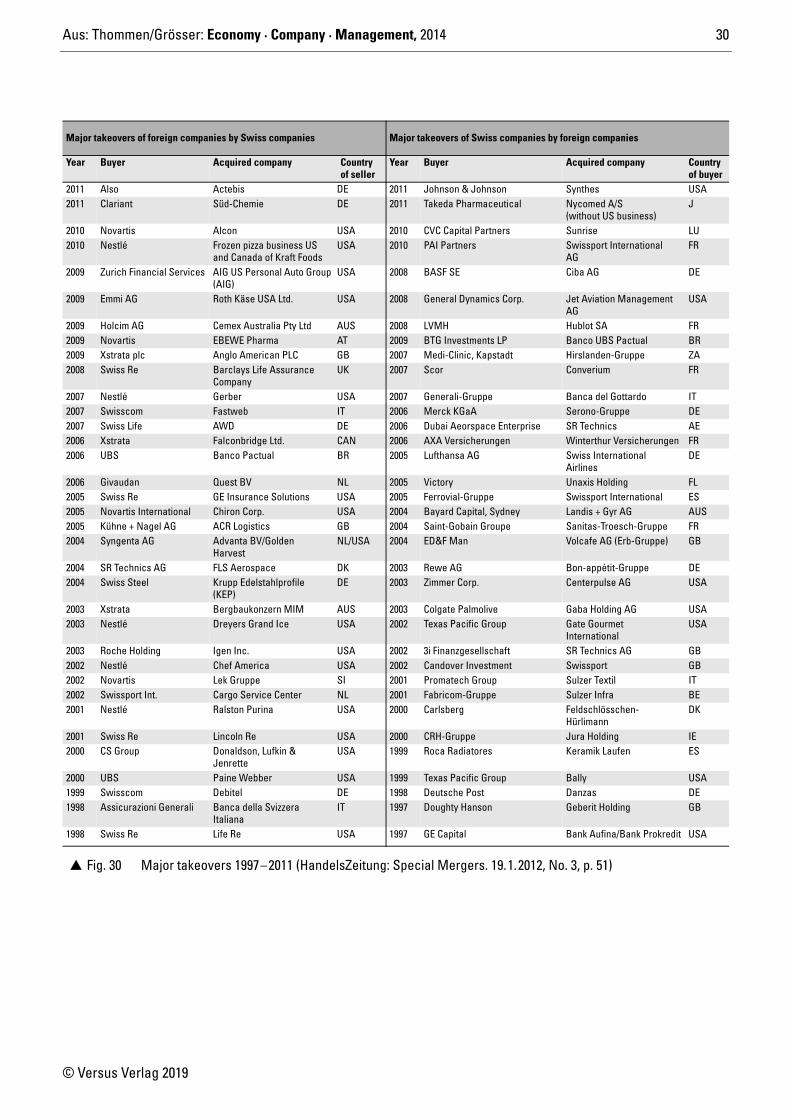

Major takeovers of foreign companies by Swiss companies Major takeovers of Swiss companies by foreign companies

Year Buyer Acquired company Country of seller

Year Buyer Acquired company Country of buyer

2011 Also Actebis DE 2011 Johnson & Johnson Synthes USA2011 Clariant Süd-Chemie DE 2011 Takeda Pharmaceutical Nycomed A/S

(without US business)J

2010 Novartis Alcon USA 2010 CVC Capital Partners Sunrise LU2010 Nestlé Frozen pizza business US

and Canada of Kraft FoodsUSA 2010 PAI Partners Swissport International

AGFR

2009 Zurich Financial Services AIG US Personal Auto Group (AIG)

USA 2008 BASF SE Ciba AG DE

2009 Emmi AG Roth Käse USA Ltd. USA 2008 General Dynamics Corp. Jet Aviation ManagementAG

USA

2009 Holcim AG Cemex Australia Pty Ltd AUS 2008 LVMH Hublot SA FR2009 Novartis EBEWE Pharma AT 2009 BTG Investments LP Banco UBS Pactual BR2009 Xstrata plc Anglo American PLC GB 2007 Medi-Clinic, Kapstadt Hirslanden-Gruppe ZA2008 Swiss Re Barclays Life Assurance

CompanyUK 2007 Scor Converium FR

2007 Nestlé Gerber USA 2007 Generali-Gruppe Banca del Gottardo IT2007 Swisscom Fastweb IT 2006 Merck KGaA Serono-Gruppe DE2007 Swiss Life AWD DE 2006 Dubai Aeorspace Enterprise SR Technics AE2006 Xstrata Falconbridge Ltd. CAN 2006 AXA Versicherungen Winterthur Versicherungen FR2006 UBS Banco Pactual BR 2005 Lufthansa AG Swiss International

AirlinesDE

2006 Givaudan Quest BV NL 2005 Victory Unaxis Holding FL2005 Swiss Re GE Insurance Solutions USA 2005 Ferrovial-Gruppe Swissport International ES2005 Novartis International Chiron Corp. USA 2004 Bayard Capital, Sydney Landis + Gyr AG AUS2005 Kühne + Nagel AG ACR Logistics GB 2004 Saint-Gobain Groupe Sanitas-Troesch-Gruppe FR2004 Syngenta AG Advanta BV/Golden

HarvestNL/USA 2004 ED&F Man Volcafe AG (Erb-Gruppe) GB

2004 SR Technics AG FLS Aerospace DK 2003 Rewe AG Bon-appétit-Gruppe DE2004 Swiss Steel Krupp Edelstahlprofile

(KEP)DE 2003 Zimmer Corp. Centerpulse AG USA

2003 Xstrata Bergbaukonzern MIM AUS 2003 Colgate Palmolive Gaba Holding AG USA2003 Nestlé Dreyers Grand Ice USA 2002 Texas Pacific Group Gate Gourmet

InternationalUSA

2003 Roche Holding Igen Inc. USA 2002 3i Finanzgesellschaft SR Technics AG GB2002 Nestlé Chef America USA 2002 Candover Investment Swissport GB2002 Novartis Lek Gruppe SI 2001 Promatech Group Sulzer Textil IT2002 Swissport Int. Cargo Service Center NL 2001 Fabricom-Gruppe Sulzer Infra BE2001 Nestlé Ralston Purina USA 2000 Carlsberg Feldschlösschen-

HürlimannDK

2001 Swiss Re Lincoln Re USA 2000 CRH-Gruppe Jura Holding IE2000 CS Group Donaldson, Lufkin &

JenretteUSA 1999 Roca Radiatores Keramik Laufen ES

2000 UBS Paine Webber USA 1999 Texas Pacific Group Bally USA1999 Swisscom Debitel DE 1998 Deutsche Post Danzas DE1998 Assicurazioni Generali Banca della Svizzera

ItalianaIT 1997 Doughty Hanson Geberit Holding GB

1998 Swiss Re Life Re USA 1997 GE Capital Bank Aufina/Bank Prokredit USA

� Fig. 30 Major takeovers 1997–2011 (HandelsZeitung: Special Mergers. 19.1.2012, No. 3, p. 51)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 31

© Versus Verlag 2019

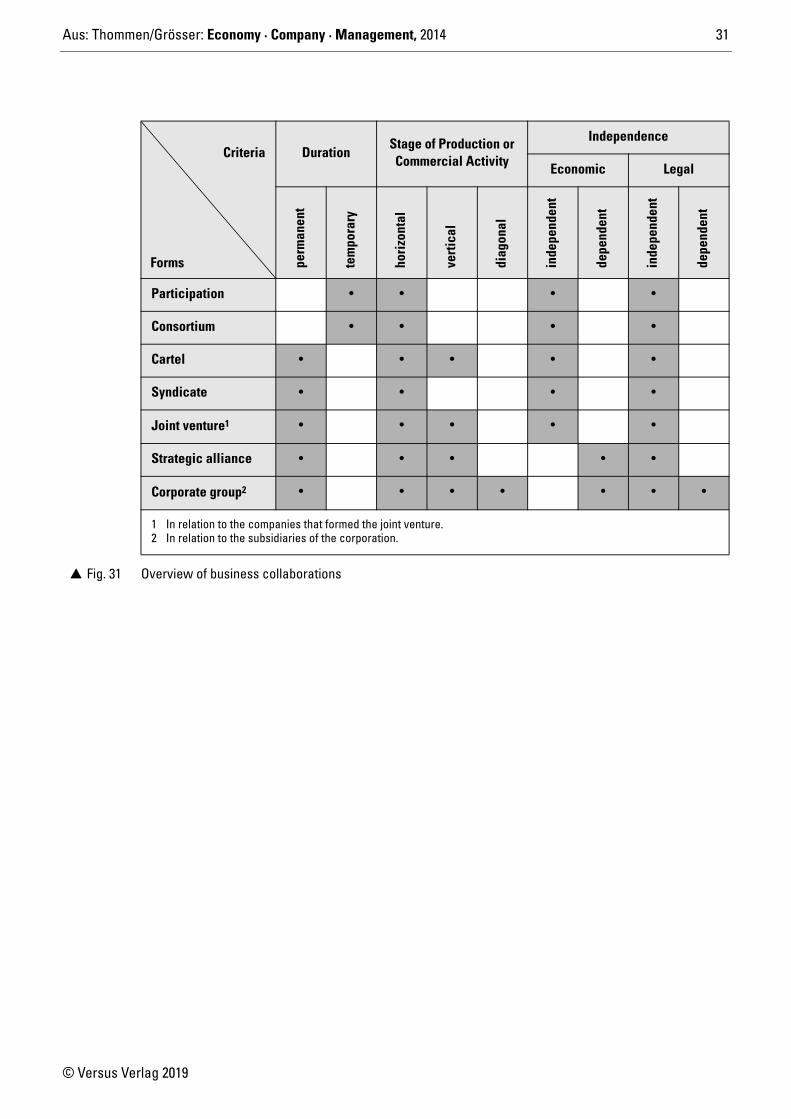

DurationStage of Production or Commercial Activity

Independence

Economic Legal

perm

anen

t

tem

pora

ry

hori

zont

al

vert

ical

diag

onal

inde

pend

ent

depe

nden

t

inde

pend

ent

depe

nden

t

Participation • • • •

Consortium • • • •

Cartel • • • • •

Syndicate • • • •

Joint venture1 • • • • •

Strategic alliance • • • • •

Corporate group2 • • • • • • •

1 In relation to the companies that formed the joint venture.2 In relation to the subsidiaries of the corporation.

� Fig. 31 Overview of business collaborations

Criteria

Forms

Aus: Thommen/Grösser: Economy · Company · Management, 2014 32

© Versus Verlag 2019

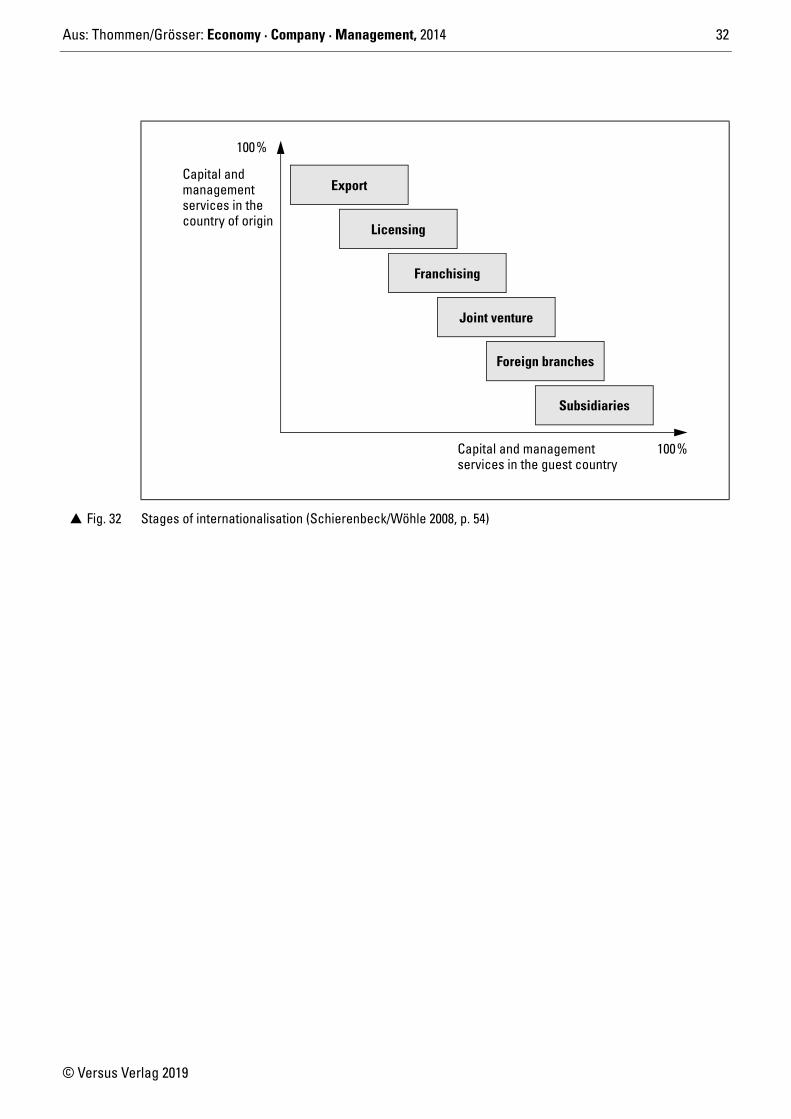

� Fig. 32 Stages of internationalisation (Schierenbeck/Wöhle 2008, p. 54)

100%

Capital andmanagementservices in thecountry of origin

Capital and managementservices in the guest country

Export

Licensing

Franchising

Joint venture

Foreign branches

Subsidiaries

100%

Aus: Thommen/Grösser: Economy · Company · Management, 2014 33

© Versus Verlag 2019

� Fig. 33 Labour as a location factor

Labour as a location factor

Number of Cost of Qualification ofemployeesemployees employees

Aus: Thommen/Grösser: Economy · Company · Management, 2014 34

© Versus Verlag 2019

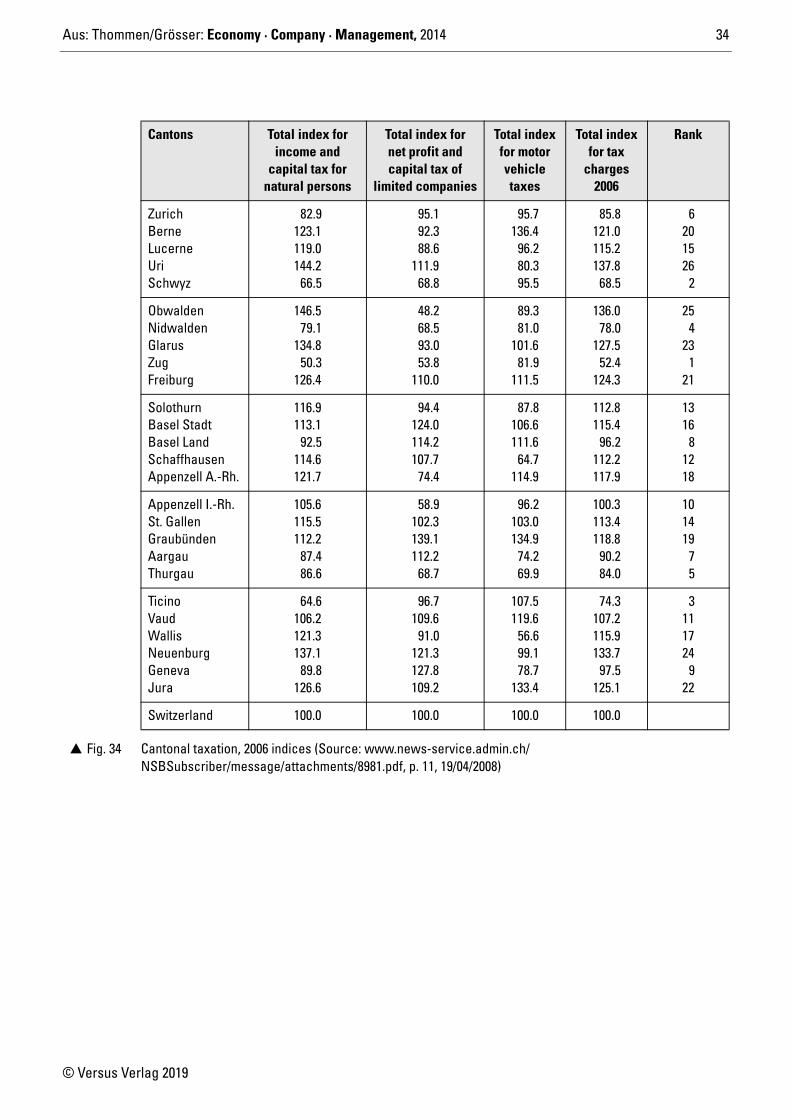

Cantons Total index for income and

capital tax fornatural persons

Total index for net profit and capital tax of

limited companies

Total index for motor vehicle taxes

Total index for tax

charges 2006

Rank

ZurichBerneLucerneUriSchwyz

82.9123.1119.0144.2

66.5

95.192.388.6

111.968.8

95.7136.4

96.280.395.5

85.8121.0115.2137.8

68.5

6201526

2

ObwaldenNidwaldenGlarusZugFreiburg

146.579.1

134.850.3

126.4

48.268.593.053.8

110.0

89.381.0

101.681.9

111.5

136.078.0

127.552.4

124.3

254

231

21

SolothurnBasel StadtBasel LandSchaffhausenAppenzell A.-Rh.

116.9113.1

92.5114.6121.7

94.4124.0114.2107.7

74.4

87.8106.6111.6

64.7114.9

112.8115.4

96.2112.2117.9

1316

81218

Appenzell I.-Rh.St. GallenGraubündenAargauThurgau

105.6115.5112.2

87.486.6

58.9102.3139.1112.2

68.7

96.2103.0134.9

74.269.9

100.3113.4118.8

90.284.0

101419

75

TicinoVaudWallisNeuenburgGenevaJura

64.6106.2121.3137.1

89.8126.6

96.7109.6

91.0121.3127.8109.2

107.5119.6

56.699.178.7

133.4

74.3107.2115.9133.7

97.5125.1

3111724

922

Switzerland 100.0 100.0 100.0 100.0

� Fig. 34 Cantonal taxation, 2006 indices (Source: www.news-service.admin.ch/NSBSubscriber/message/attachments/8981.pdf, p. 11, 19/04/2008)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 35

© Versus Verlag 2019

Loca

tion

D R 24 45 80 30 10 75 24 40 328

Rank

3

X=

Eval

uatio

n (g

ood

= 5,

sat

isfa

ctor

y =

3, b

ad =

1)

R =

Bene

fit p

er lo

catio

n fa

ctor

Not

e: E

ssen

tial r

equi

rem

ents

, i.e

., m

anda

tory

crit

eria

(e.g

., m

inim

um a

rea)

wer

e no

t con

side

red.

X 3 3 5 3 1 3 3 5

Loca

tion

C R 24 15 80 10 30 25 40 24 248

Rank

4

X 3 1 5 1 3 1 5 3

Loca

tion

B R 8 75 48 30 50 125 8 8

352

Rank

1

X 1 5 3 3 5 5 1 1

Loca

tion

A R 40 75 48 10 50 75 24 24 346

Rank

2

X 5 5 3 1 5 3 3 3

Wei

ghtin

g

8 15 16 10 10 25 8 8

100

Defin

ing

the

pref

eren

ce ra

nkin

g of

the

alte

rnat

ives

Loca

tion

requ

irem

ent

Good

tran

spor

t acc

essi

bilit

y(e

.g.,

clos

e to

mot

orw

ay a

nd a

irpor

t)

Favo

urab

le la

bour

mar

ket

(e.g

., qu

alifi

ed s

peci

alis

t wor

kers

, lab

our r

eser

ve)

Avai

labl

e in

dust

rial s

ite(e

.g.,

min

imum

are

a, o

ppor

tuni

ties

for f

utur

e ex

pans

ion)

Effic

ient

sup

ply

and

disp

osal

(e.g

., su

pply

with

ele

ctric

ity, g

as, w

ater

)

Acce

ptab

le le

gal r

equi

rem

ents

(e.g

., bu

ildin

g re

gula

tions

)

Low

tax

char

ges

(e.g

., lo

w ta

x ra

tes,

tax

ince

ntiv

es)

Good

pro

mot

iona

l mea

sure

s(e

.g.,

stat

e su

bsid

ies,

com

mun

al s

uppo

rt fo

r the

eco

nom

y)

Good

qua

lity

of li

fe(e

.g.,

soci

al, e

duca

tion,

leis

ure

faci

litie

s)

Tota

l ben

efit

of th

e al

tern

ativ

es

1 2 3 4 5 6 7 8

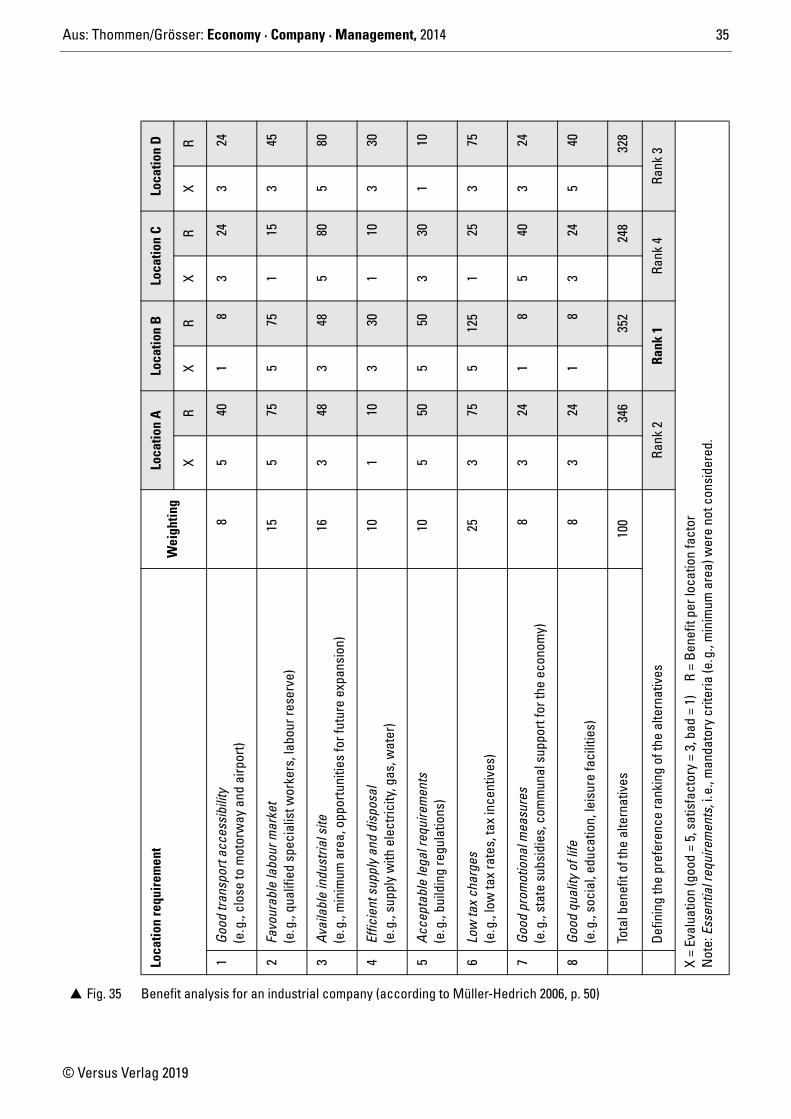

� Fig. 35 Benefit analysis for an industrial company (according to Müller-Hedrich 2006, p. 50)

Aus: Thommen/Grösser: Economy · Company · Management, 2014 36

© Versus Verlag 2019

Environmental Management

� Fig. 36 Credit Suisse Statement on Sustainability (Credit Suisse Group AG 2011)

� With respect to environmental aspects withinour operations, we strive to be among the mostprogressive companies. To that end we main-tain an environmental management system incompliance with the ISO 14001 standard. Westrive to continuously improve our sustainabil-ity performance and to use the most environ-mentally sound technology wherever possibleand in line with sound business practices.

� With respect to greenhouse gas emissions, weare committed to being greenhouse gas neutraland are actively engaging our employees inorder to further these endeavours.

� We involve our contractors, procurement,facilities management and logistics partners inour efforts to improve our performance in theprotection of environment and society, and toencourage them to meet high sustainabilitystandards. We request information on poten-tially harmful building materials and othersubstances and on the environmental or socialaspects of products supplied to us.

� All relevant environmental and social data ondesign, materials, operational matters, energyefficiency and ergonomics are taken intoaccount in the planning and construction ofnew premises and facilities.

� As laid down in our Supplier Code of Conduct,we expect our suppliers to go beyond theminimum required and strive to apply bestpractices, living up to their environmental andsocial responsibilities and carefully mitigatingrisk.

� By systematically measuring, recording andevaluating energy and resource consumption,emissions, waste and environmental risks, weset the foundation for continuous improve-ments in our environmental performance. Wetake precautions to prevent pollution as well asaccidents and to limit their impact on healthand the environment.

Aus: Thommen/Grösser: Economy · Company · Management, 2014 37

© Versus Verlag 2019

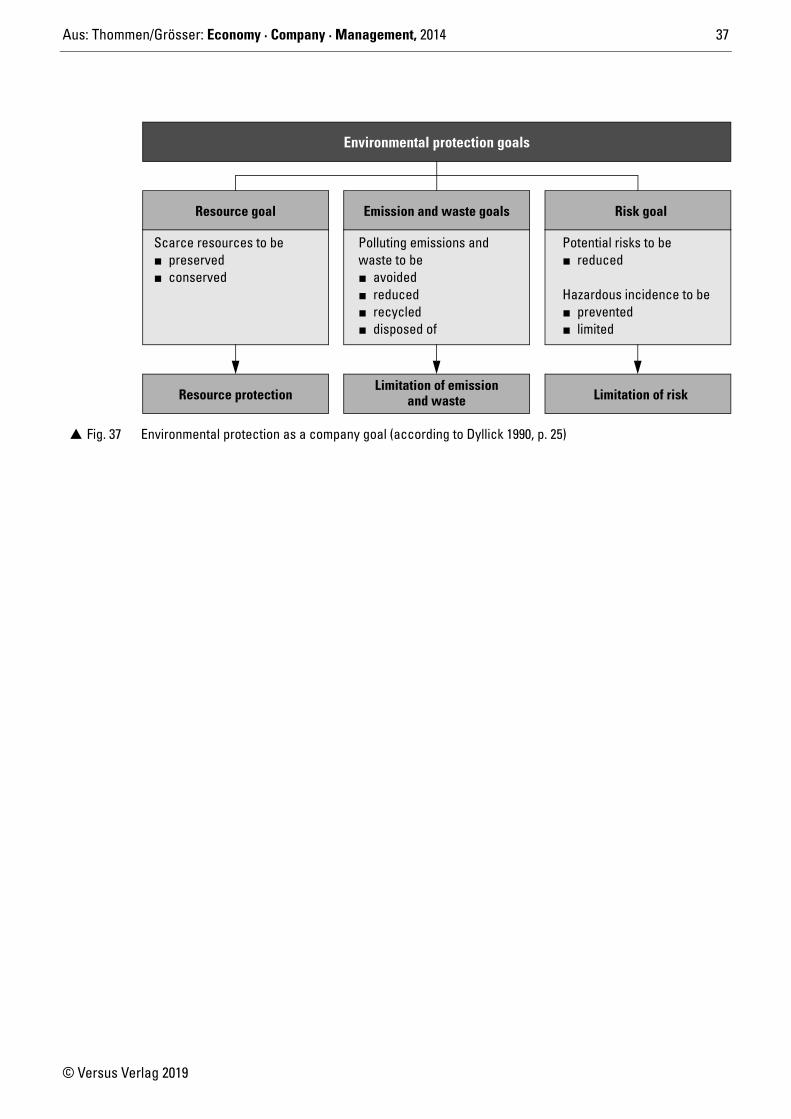

� Fig. 37 Environmental protection as a company goal (according to Dyllick 1990, p. 25)

Resource goal Emission and waste goals Risk goal

Resource protectionLimitation of emission

and waste Limitation of risk

Scarce resources to be� preserved� conserved

Polluting emissions and waste to be� avoided� reduced� recycled� disposed of

Potential risks to be� reduced

Hazardous incidence to be� prevented� limited

Environmental protection goals

Aus: Thommen/Grösser: Economy · Company · Management, 2014 38

© Versus Verlag 2019

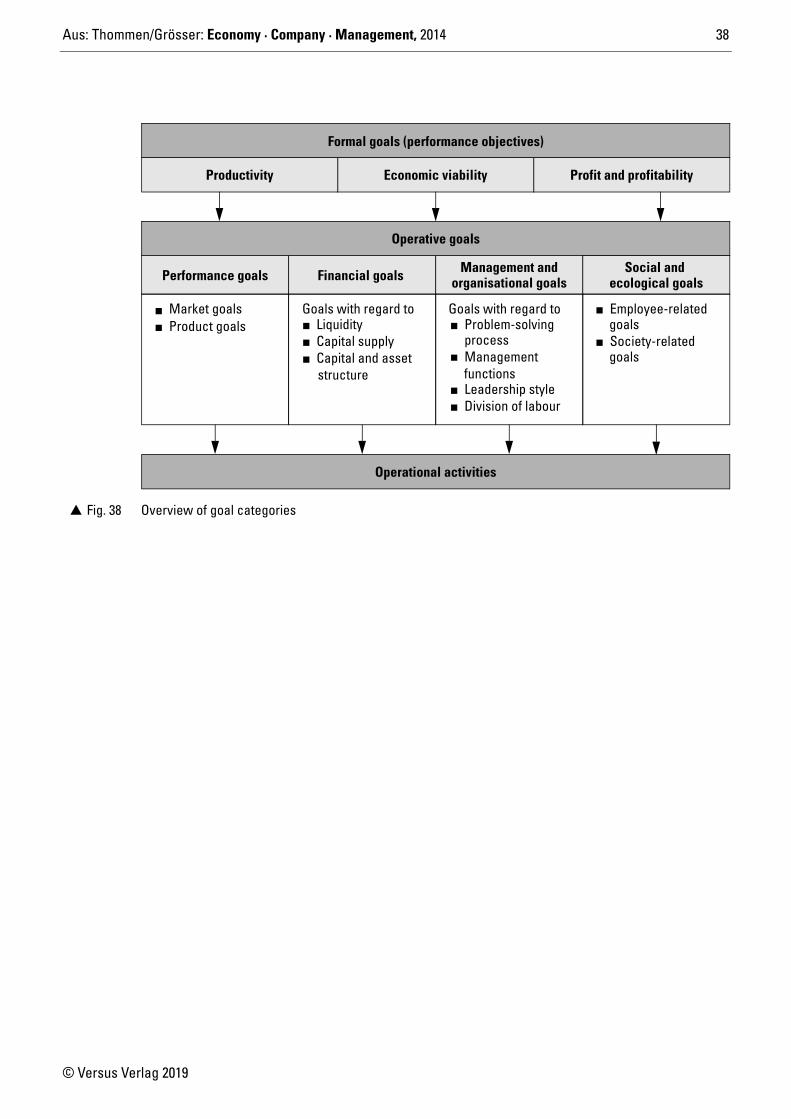

� Fig. 38 Overview of goal categories

Operative goals

Performance goals

� Market goals� Product goals

Financial goals

Goals with regard to

� Capital supply� Liquidity

� Capital and asset

Management and

Goals with regard to� Problem-solving

� Managementprocess

functions� Leadership style� Division of labour

Social and

� Employee-related

� Society-related

Formal goals (performance objectives)

Operational activities

organisational goals ecological goals

structure

goals

goals

Productivity Economic viability Profit and profitability

Aus: Thommen/Grösser: Economy · Company · Management, 2014 39

© Versus Verlag 2019

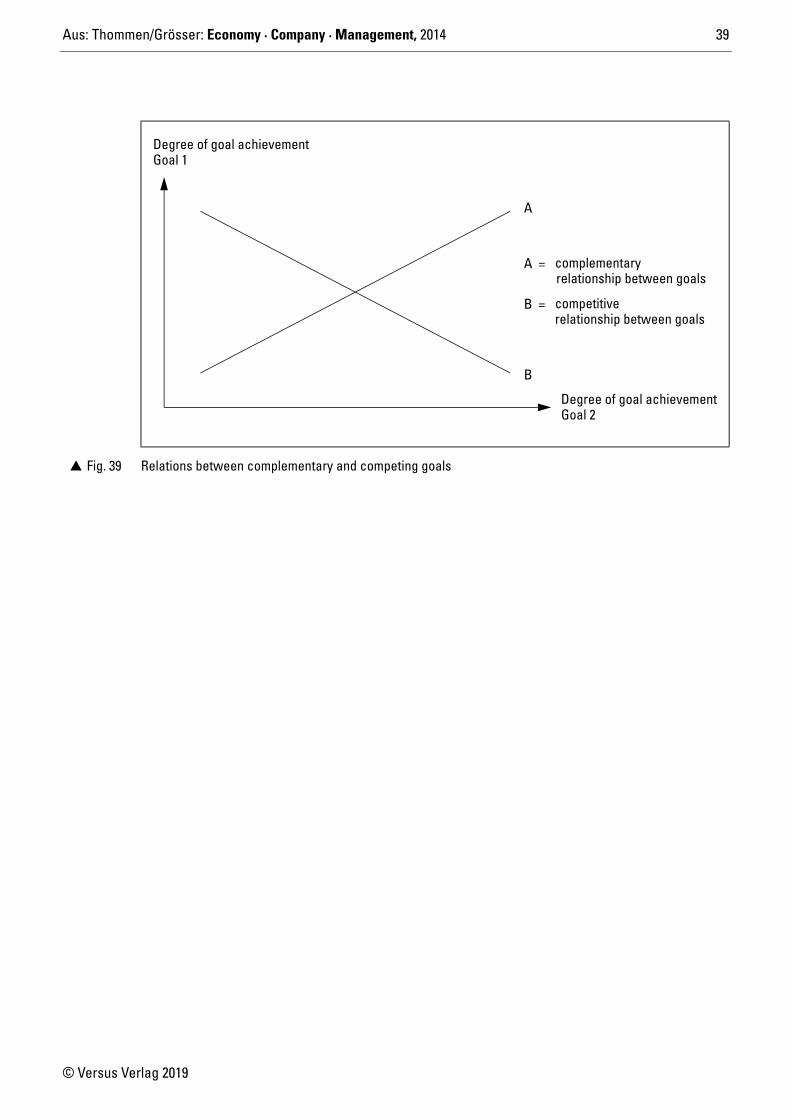

� Fig. 39 Relations between complementary and competing goals

Degree of goal achievementGoal 1

A

B

A =

B =

Degree of goal achievementGoal 2

relationship between goals

relationship between goals

complementary

competitive

Aus: Thommen/Grösser: Economy · Company · Management, 2014 40

© Versus Verlag 2019

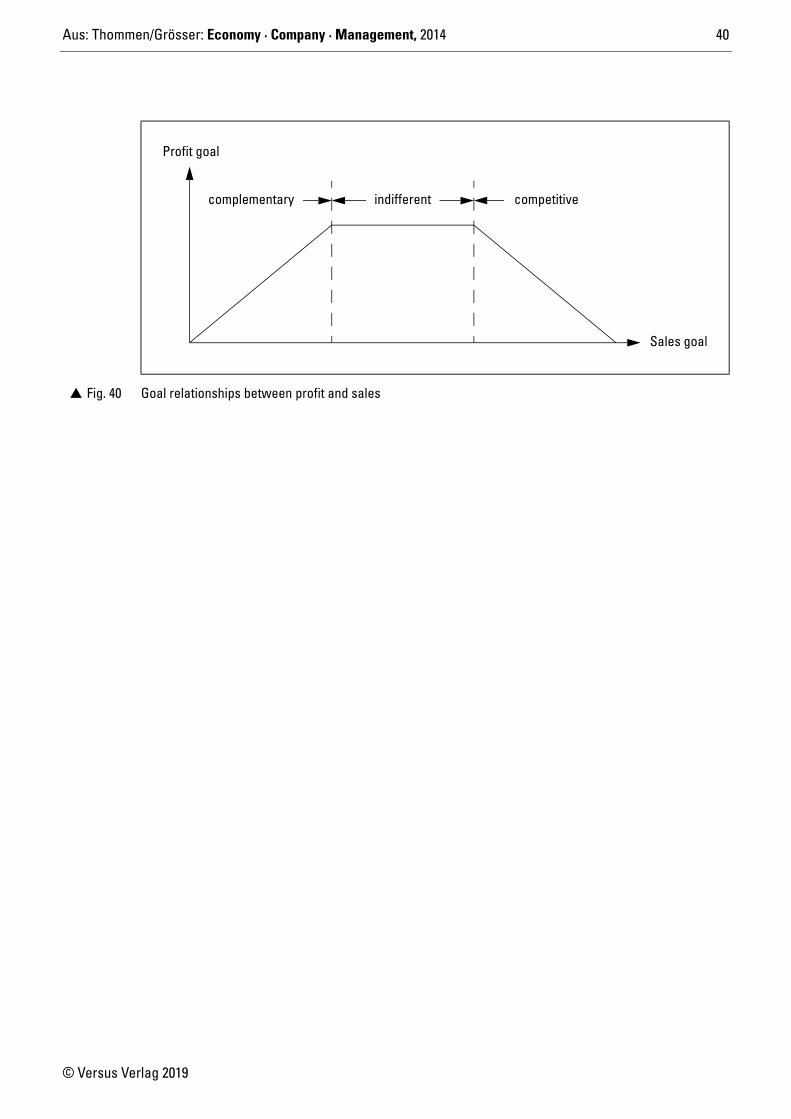

� Fig. 40 Goal relationships between profit and sales

Profit goal

complementary

Sales goal

indifferent competitive

Aus: Thommen/Grösser: Economy · Company · Management, 2014 41

© Versus Verlag 2019

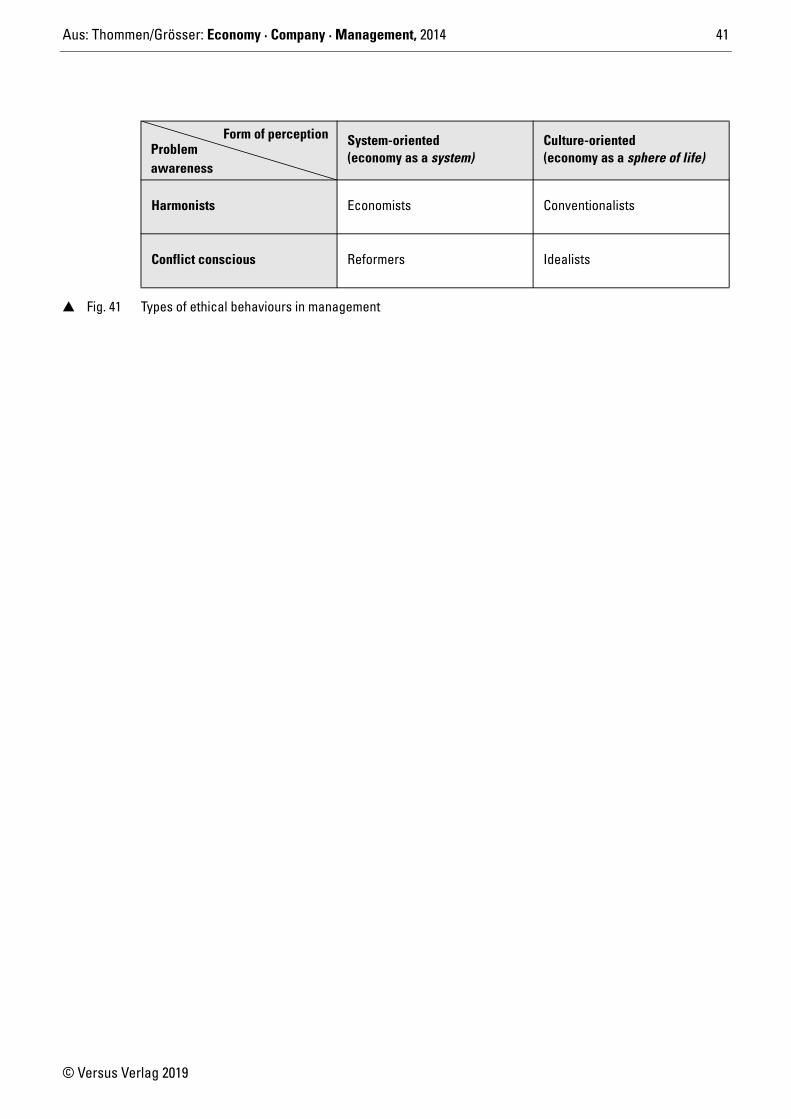

System-oriented(economy as a system)

Culture-oriented (economy as a sphere of life)

Harmonists Economists Conventionalists

Conflict conscious Reformers Idealists

� Fig. 41 Types of ethical behaviours in management

Form of perceptionProblemawareness

Aus: Thommen/Grösser: Economy · Company · Management, 2014 42

© Versus Verlag 2019

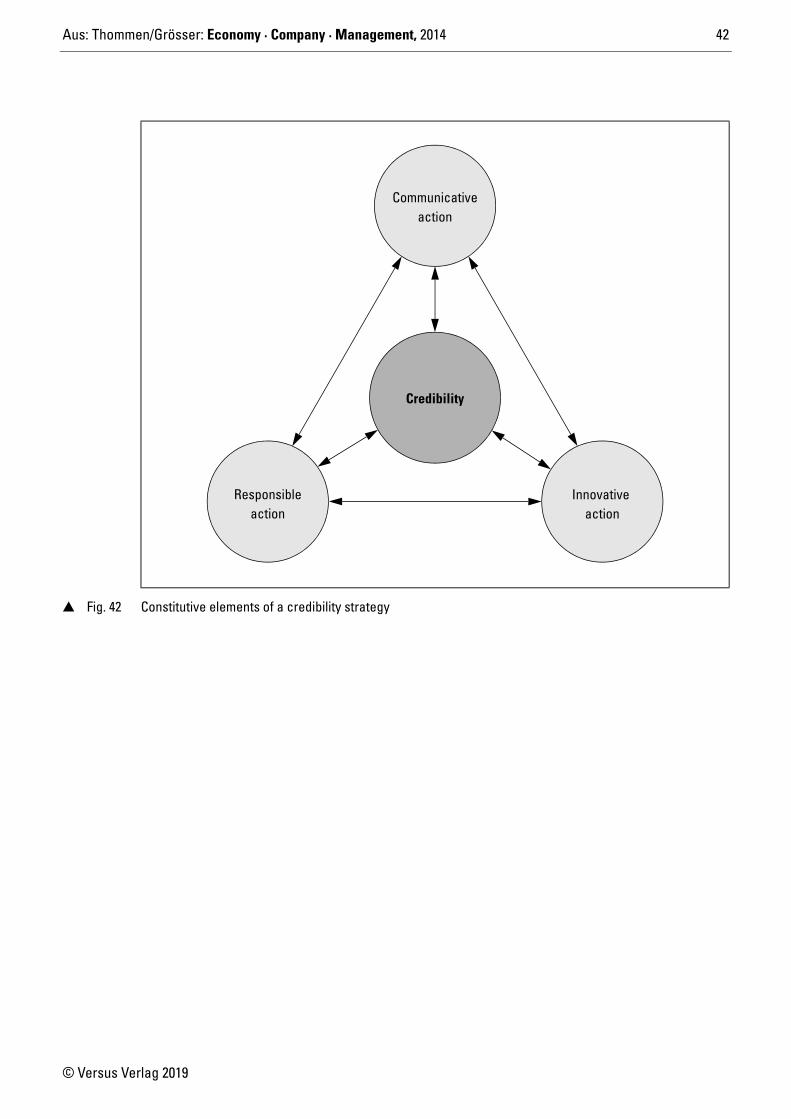

� Fig. 42 Constitutive elements of a credibility strategy

Credibility

Communicativeaction

Responsibleaction

Innovative action

Aus: Thommen/Grösser: Economy · Company · Management, 2014 43

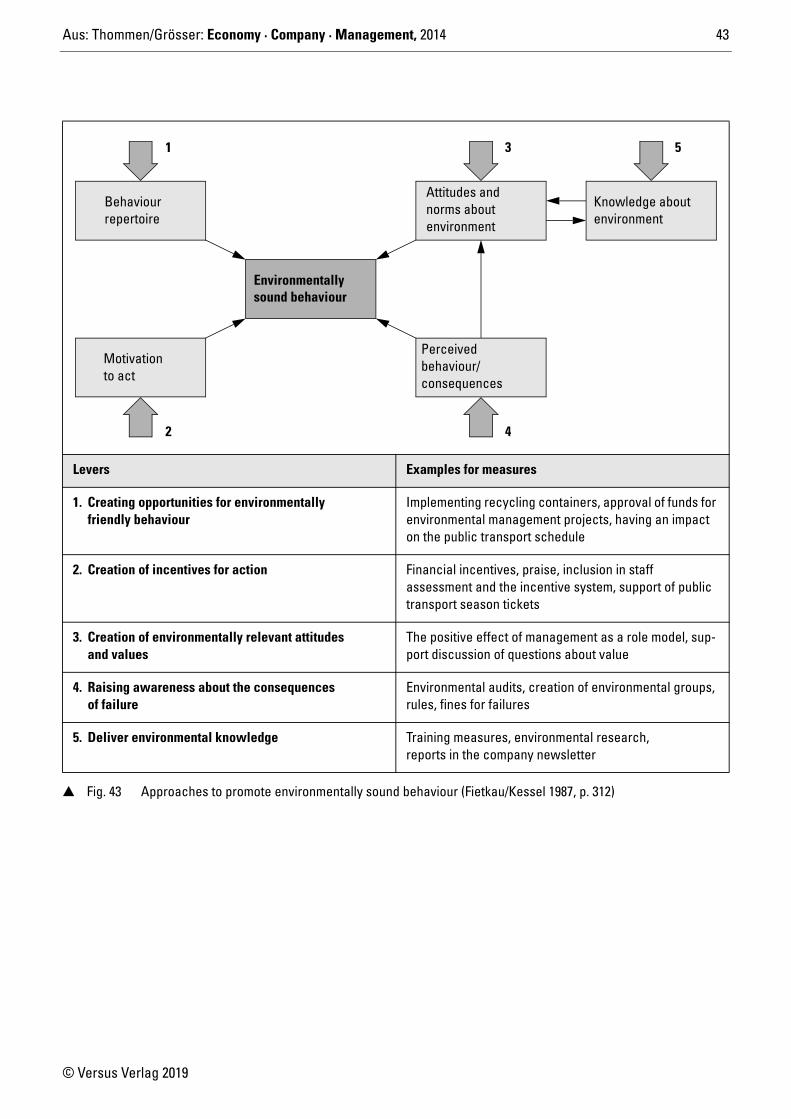

© Versus Verlag 2019

Levers Examples for measures

1. Creating opportunities for environmentally friendly behaviour

Implementing recycling containers, approval of funds for environmental management projects, having an impact on the public transport schedule

2. Creation of incentives for action Financial incentives, praise, inclusion in staff assessment and the incentive system, support of public transport season tickets

3. Creation of environmentally relevant attitudes and values

The positive effect of management as a role model, sup-port discussion of questions about value

4. Raising awareness about the consequences of failure

Environmental audits, creation of environmental groups, rules, fines for failures

5. Deliver environmental knowledge Training measures, environmental research, reports in the company newsletter

� Fig. 43 Approaches to promote environmentally sound behaviour (Fietkau/Kessel 1987, p. 312)

Motivationto act

Behaviourrepertoire

Environmentallysound behaviour

Attitudes andnorms aboutenvironment

Perceived behaviour/consequences

Knowledge aboutenvironment

1

2

3 5

4