Dissertation full text - Universit¤t St.Gallen

245

I The Competitiveness of Ghana’s Industry D I S S E R T A T I O N der Universität St.Gallen, Hochschule für Wirtschafts-, Rechts- und Sozialwissenschaften (HSG) zur Erlangung der Würde eines Doktors der Staatswissenschaften vorgelegt von Anton Fidelis Hoefter von Wollerau (Schwyz) Genehmigt auf Antrag der Herren Prof. Dr. Jean-Max Baumer und Prof. Dr. Hans Georg Graf Dissertation Nr. 2494 Difo-Druck GmbH, Bamberg

Transcript of Dissertation full text - Universit¤t St.Gallen

I

The Competitiveness of Ghana’s Industry

D I S S E R T A T I O N der Universität St.Gallen,

Hochschule für Wirtschafts-, Rechts- und Sozialwissenschaften (HSG)

zur Erlangung der Würde eines Doktors der Staatswissenschaften

vorgelegt von

Anton Fidelis Hoefter

von

Wollerau (Schwyz)

Genehmigt auf Antrag der Herren

Prof. Dr. Jean-Max Baumer

und

Prof. Dr. Hans Georg Graf

Dissertation Nr. 2494

Difo-Druck GmbH, Bamberg

II

Die Universität St.Gallen, Hochschule für Wirtschafts-, Rechts- und Sozial-wissenschaften (HSG), gestattet hiermit den Druck der vorliegenden Dissertation, ohne damit zu den darin ausgesprochenen Anschauungen Stellung zu nehmen.

St. Gallen, den 23. Januar 2001

Der Rektor:

Prof. Dr. Peter Gomez

III

Meiner Familie mit Dank für die Geduld und Unterstützung

IV

Preface

The motivation to write a thesis on Ghana was born out of a friendship with late Father Joseph Apuri from Navrongo, Ghana. A good friend of my father from University, I had gotten to know him already as a child, and continued to be fascinated by his home country and the challenges of his people. Although I have not contributed a lot, I hope that a part of this work could provide some explanation and help on how to improve the economic conditions of Ghana.

Many people have helped me to complete this thesis. In Ghana, I had the opportunity to talk to a large number of people, and I would like to thank all my interview partners for their time and interest in my work, and the hospitality that many of them offered.

Without the advice and support of Prof. Jean-Max Baumer, this thesis would not have been possible. I would like to thank him for his help, encouragement and patience during this time. I would also like to thank Prof. Dr. Hans Georg Graf for his valuable input and advice.

McKinsey & Company has given me the opportunity to work part-time for some months to get this thesis off the ground, and many of my there friends have helped and encouraged me during these years.

I am particularly grateful to my friends from St.Gallen. Hans-Gereon Früh, Andreas Steininger, Jürgen Krotzinger, Benedikt Braumann, Katharina Fehr, Pascal Guillet and Thomas Petermann (in no particular order) were always there for long discussions, and helped with their input and support.

Special thanks goes to my family. My parents who have always encouraged and supported me. And particularly my wife and friend Myriam, for giving her loving patience to a husband who had to combine a normal working day with an academic project. Our son Richard accompanied us during the last months of this thesis and motivated me to complete this work.

Zürich, January 30 Anton Hoefter

V

Overview of content Overview of content V Table of content VII Table of figures XIII Table of tables XIV Abbreviations XV

I INTRODUCTION 1

1 Motivation 1

2 Research approach 3

II OVERVIEW OF GHANA’S ECONOMY 7

3 The political background of Ghana’s economic development 7

4 The structure of Ghana’s economy 21

5 The role of foreign trade in Ghana’s economy 30

6 Other research on Ghana’s competitiveness 34

III THEORETICAL AND METHODOLOGICAL CONCEPTS 41

7 Competitiveness – a definition 41

8 Theoretical approach 45

9 Methodology to measure competitive advantage 61

10 Methodology to explain impact of determinants of competitive advantage 68

IV ANALYSIS OF COMPETITIVENESS OF GHANA’S INDUSTRIES 71

11 Ghana’s competitive and uncompetitive industries 71

12 The competitive advantage of the Aluminum industry 78

13 The competitive advantage of the Cocoa industry 94

VI

14 The competitive advantage of the Food industry 111

15 The competitive advantage of the Gold industry 125

16 The competitive advantage of the Timber and Furniture Industry 138

17 The competitive disadvantage of the Textile and Garment industry 151

V CONCLUSIONS ON DETERMINANTS OF COMPETITIVE ADVANTAGE 163

18 Factor conditions 163

19 Demand conditions 177

20 Related and supporting industries 181

21 Strategy, structure, and rivalry 184

22 Government 192

23 Summary - the challenges of Ghana’s Diamond of National Advantage 208 Sources 214

VII

Table of content Overview of content V Table of content VII Table of figures XIII Table of tables XIV Abbreviations XV

I INTRODUCTION 1

1 Motivation 1

2 Research approach 3 2.1 Main question and contribution 3 2.2 Framework for analysis 3 2.3 Working hypothesis 4 2.4 Data availability 5 2.5 Structure and research design 5

II OVERVIEW OF GHANA’S ECONOMY 7

3 The political background of Ghana’s economic development 7 3.1 The political economy of Ghana until 1983 7

3.1.1 Trade in gold and slaves main source of profit before colonialism 7 3.1.2 Specialization on cocoa during colonial rule 8 3.1.3 The history of decline: 1957 to 1983 9 3.1.4 The basis for decline: Nkrumah’s industrialization program 11 3.1.5 “Killing the golden geese”, the consequences of failed policies 15

3.2 Economic reforms after 1983 16 3.2.1 Main elements of Ghana’s Economic Reform Program 17 3.2.2 Political structure since 1992 19

4 The structure of Ghana’s economy 21 4.1 Ghana’s macroeconomic development after the ERP 21 4.2 Sectoral structure of Ghana’s economy 23

4.2.1 Agricultural sector 24 4.2.2 Mining and manufacturing sector 26 4.2.3 Service sector 28

VIII

5 The role of foreign trade in Ghana’s economy 30 5.1 Overview of Ghana’s export structure 30 5.2 Overview of Ghana’s import structure 33

6 Other research on Ghana’s competitiveness 34 6.1 Ghana’s competitiveness based on real exchange rate movements 34 6.2 Other research on Ghana’s competitiveness 35

6.2.1 Competitiveness reports 35 6.2.2 Degree of economic freedom reports 37 6.2.3 Evaluation of research on competitiveness 39

III THEORETICAL AND METHODOLOGICAL CONCEPTS 41

7 Competitiveness – a definition 41

8 Theoretical approach 45 8.1 “Diamond of National advantage” 45 8.2 Innovation as driver of competitive advantage 47 8.3 Review of work leading to “Competitive Advantage of Nations” 49

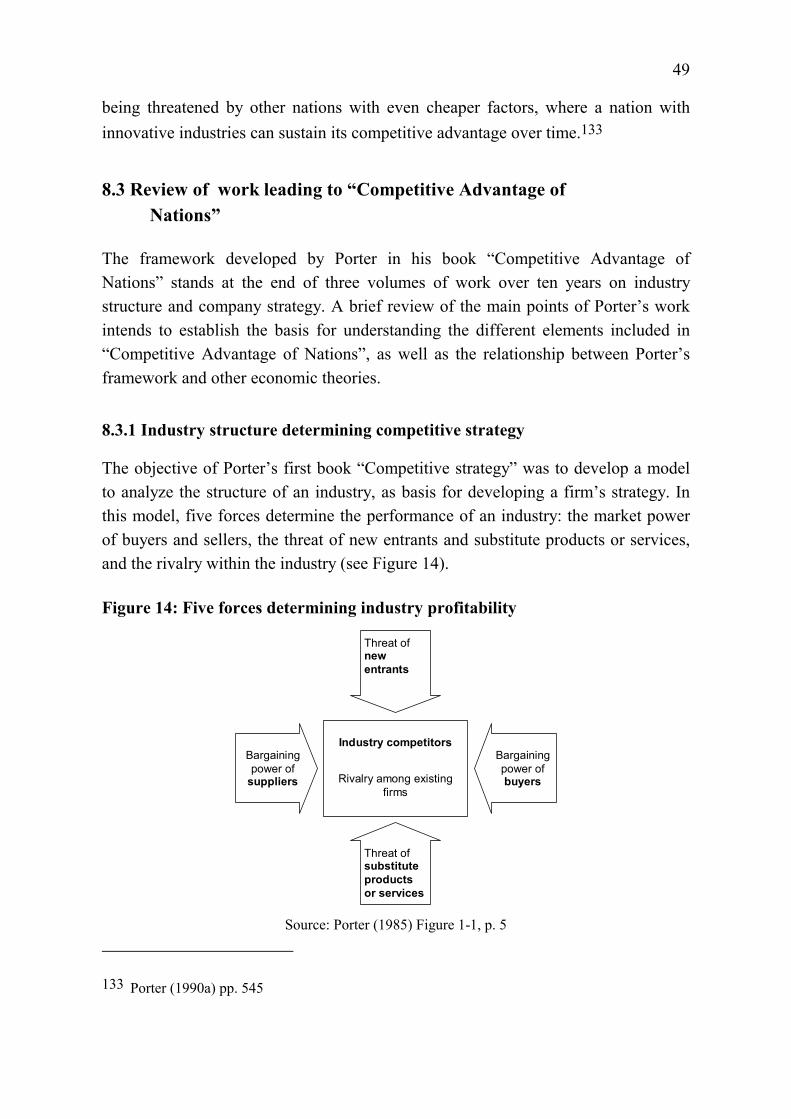

8.3.1 Industry structure determining competitive strategy 49 8.3.2 Management of firm’s value chain to gain competitive advantage 50 8.3.3 National attributes as determinant of national competitive advantage 51

8.4 Comparison of Porter with neoclassical approaches 53 8.5 A short critique of Porter’s Competitive Advantage of Nations 57 8.6 Adaptation of Porter approach to specific situation of Ghana 59

9 Methodology to measure competitive advantage 61 9.1 World market share of exports as indicator for competitive advantage 61 9.2 Measuring the World market export share of Ghana’s industry 64

9.2.1 Poor quality of Ghana export data 64 9.2.2 Most exports from gold and cocoa 65

9.3 Revised methodology to measure the competitiveness of Ghana’s industry 66

10 Methodology to explain impact of determinants of competitive advantage 68

IX

IV ANALYSIS OF COMPETITIVENESS OF GHANA’S INDUSTRIES 71

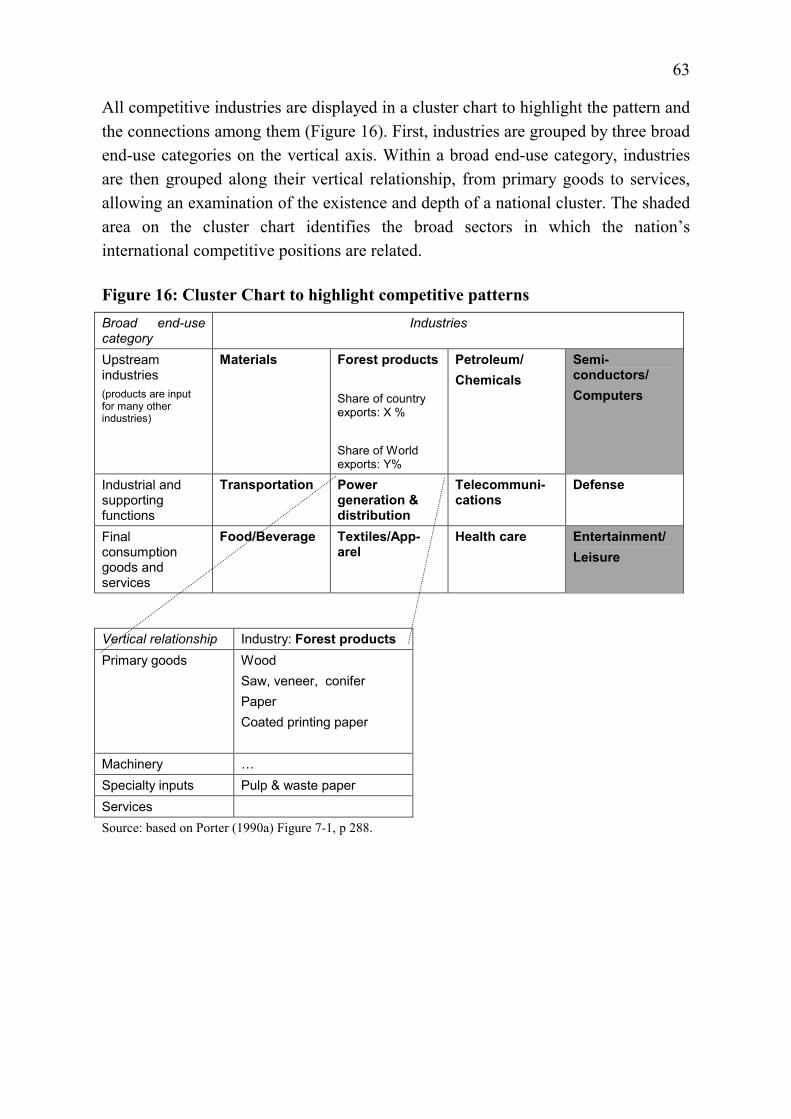

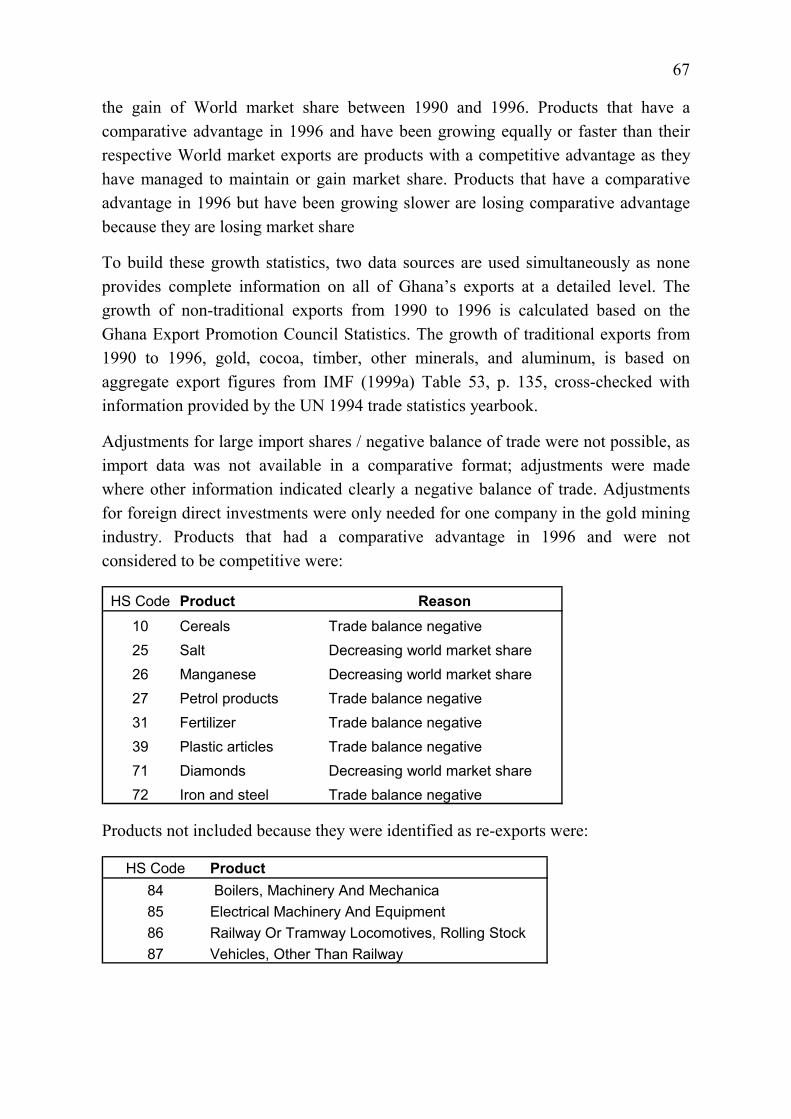

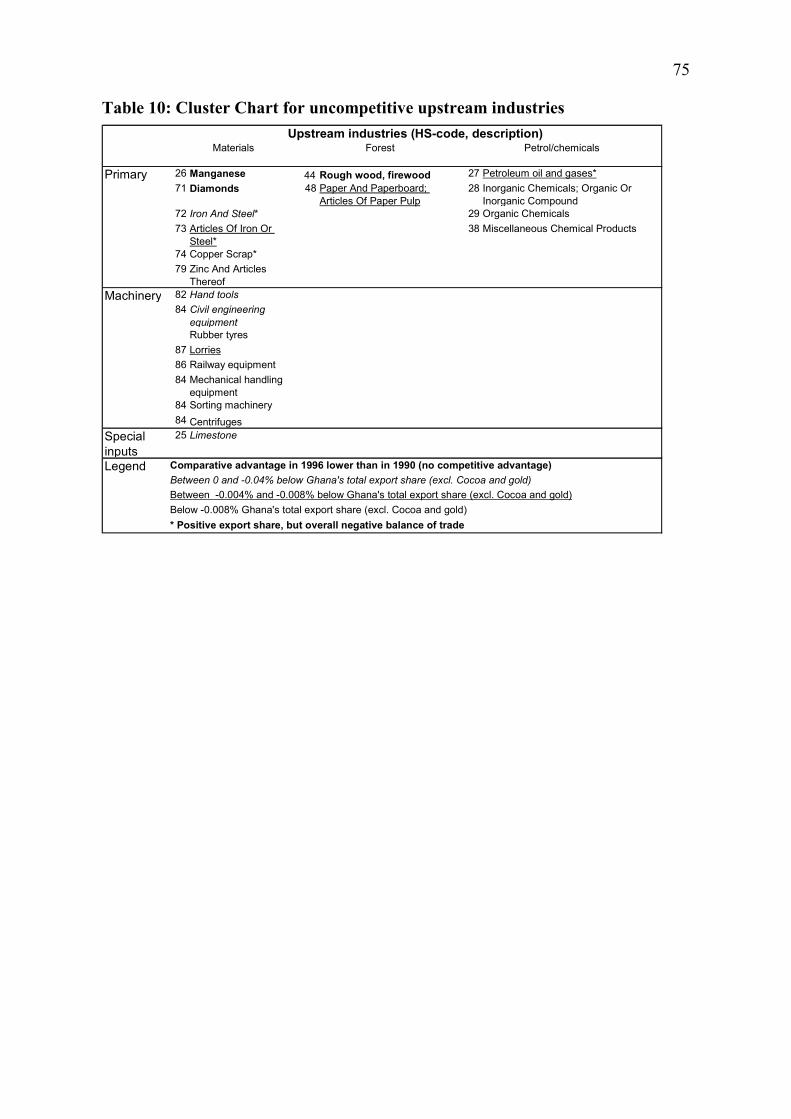

11 Ghana’s competitive and uncompetitive industries 71 11.1 Ghana’s competitive industries 71 11.2 Ghana’s uncompetitive products 74 11.3 Selection criteria for industry analysis 77

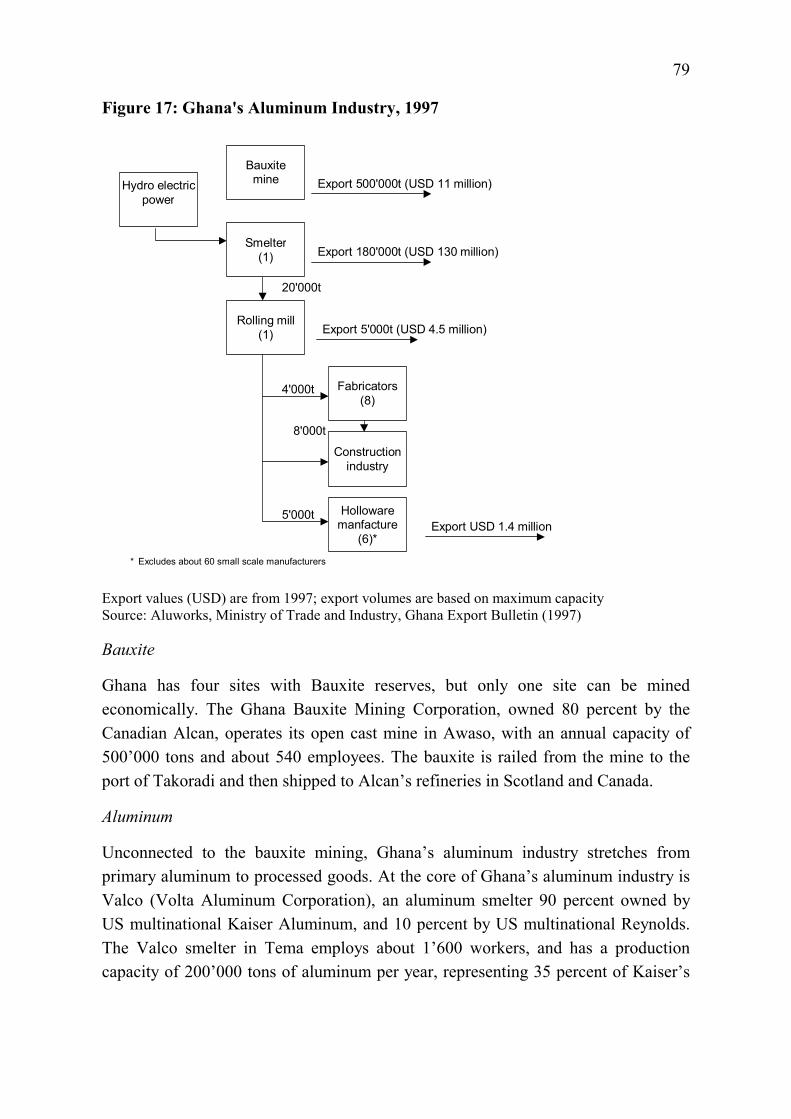

12 The competitive advantage of the Aluminum industry 78 12.1 Structure of Ghana’s Aluminum industry 78

12.1.1 Buyers 80 12.1.2 Competition 81 12.1.3 Substitutes 83

12.2 History of Ghana’s Aluminum industry 83 12.3 Aluminum’s Diamond of National Advantage 85

12.3.1 Factor conditions 86 12.3.2 Domestic demand conditions 88 12.3.3 Relating and supporting industries 89 12.3.4 Firm structure, strategy and rivalry 90 12.3.5 Influence of Government Policy 91

12.4 Summary and conclusion on Ghana’s Aluminum industry 92

13 The competitive advantage of the Cocoa industry 94 13.1 Structure of Ghana’s Cocoa industry 94

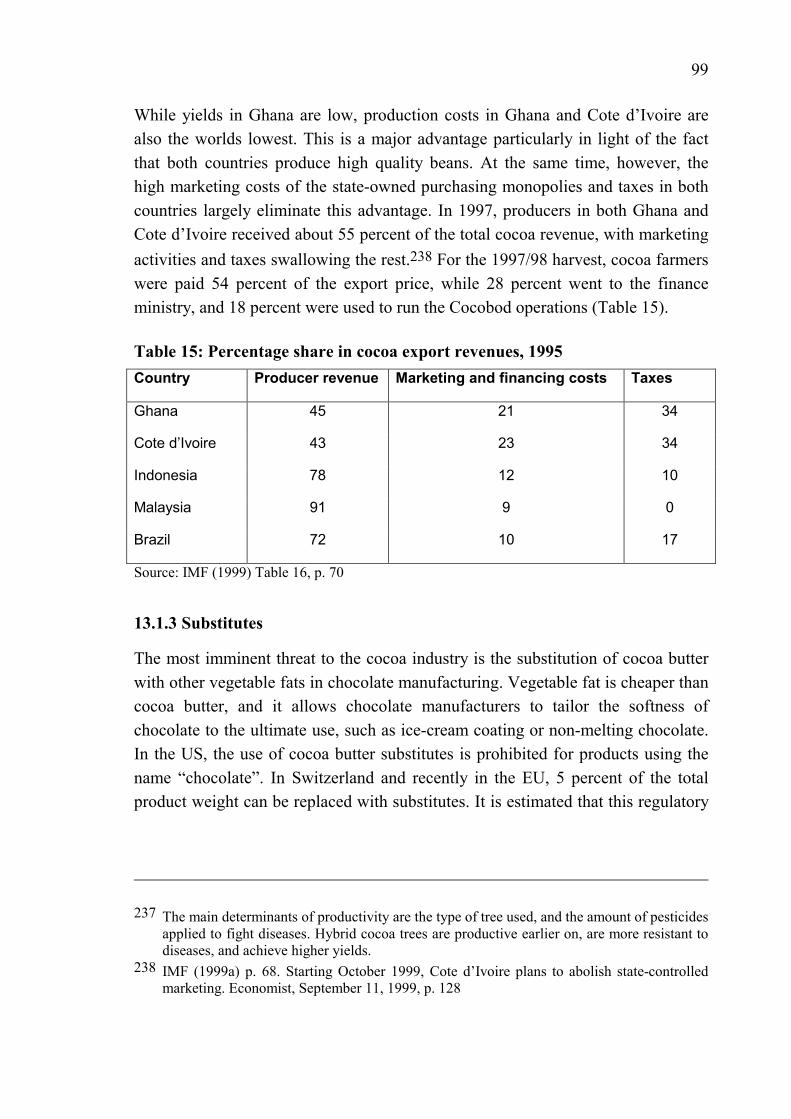

13.1.1 Buyers 96 13.1.2 Competition 97 13.1.3 Substitutes 99

13.2 History of Ghana’s Cocoa industry 100 13.3 Cocoa’s Diamond of National Advantage 103

13.3.1 Factor conditions 103 13.3.2 Domestic demand conditions 106 13.3.3 Related and supporting industries 106 13.3.4 Firm structure, strategy and rivalry 106 13.3.5 Influence of Government Policy 107

13.4 Summary and conclusion on Ghana’s Cocoa industry 108

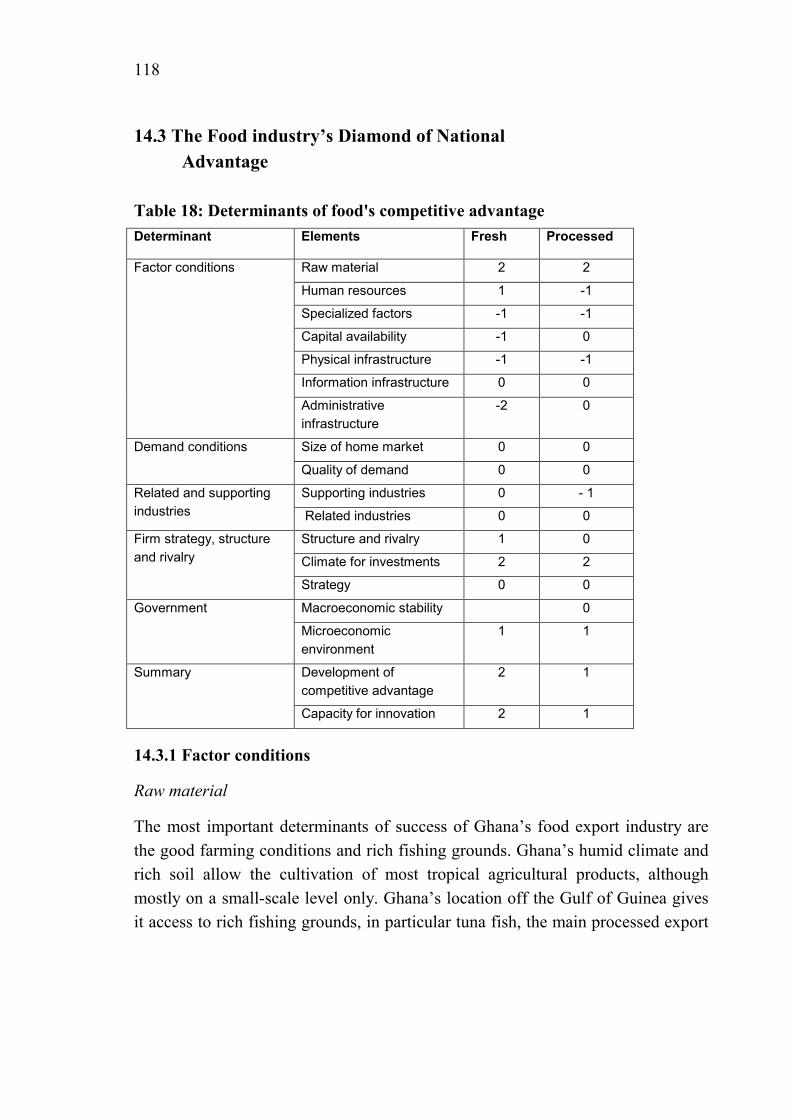

14 The competitive advantage of the Food industry 111 14.1 Structure of the Ghana’s Food industry 111

14.1.1 Buyers 113

X

14.1.2 Competition 114 14.2 History of Ghana’s Food industry 115 14.3 The Food industry’s Diamond of National Advantage 118

14.3.1 Factor conditions 118 14.3.2 Domestic demand conditions 121 14.3.3 Related and supporting industries 121 14.3.4 Firm structure, strategy and rivalry 121 14.3.5 Influence of Government Policy 123

14.4 Summary and conclusion on Ghana’s Food industry 123

15 The competitive advantage of the Gold industry 125 15.1 Structure of Ghana’s Gold mining industry 125

15.1.1 Buyers 126 15.1.2 Competition 126 15.1.3 Substitutes 127

15.2 History of Ghana’s Gold mining industry 127 15.3 Gold mining’s Diamond of National Advantage 130

15.3.1 Factor conditions 130 15.3.2 Domestic demand conditions 133 15.3.3 Related and supporting industries 133 15.3.4 Firm structure, strategy and rivalry 134 15.3.5 Influence of Government Policy 135

15.4 Summary and conclusion on Ghana’s Gold mining industry 136

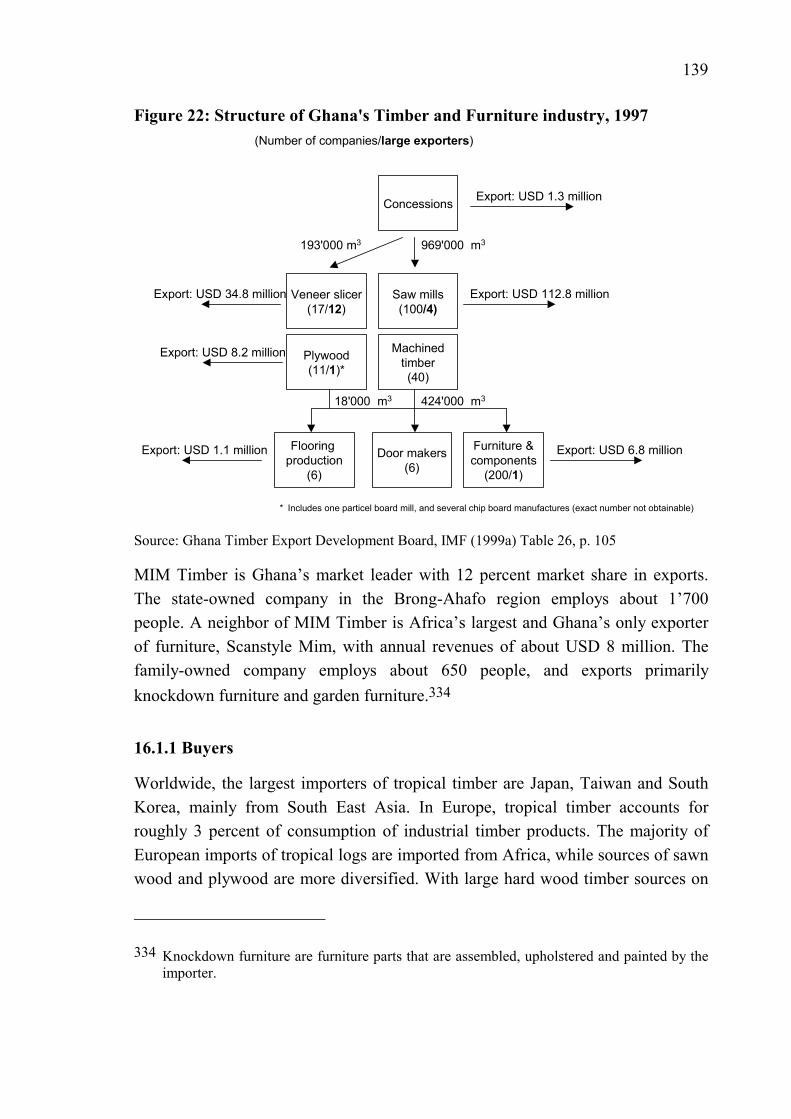

16 The competitive advantage of the Timber and Furniture Industry 138 16.1 Structure of Ghana’s Timber and Furniture industry 138

16.1.1 Buyers 139 16.1.2 Competitors 141 16.1.3 Substitutes 142

16.2 History of Ghana’s Timber and Furniture industry 142 16.3 Timber and Furniture’s Diamond of National Advantage 144

16.3.1 Factor conditions 145 16.3.2 Domestic demand conditions 147 16.3.3 Related and supporting industries 147 16.3.4 Firm structure, strategy and rivalry 147 16.3.5 Influence of Government Policy 149

16.4 Summary and conclusion on Ghana’s Timber and Furniture industry 149

XI

17 The competitive disadvantage of the Textile and Garment industry 151 17.1 Structure of Ghana’s Textile and Garment industry 151

17.1.1 Buyers 152 17.1.2 Competition 153 17.1.3 Substitutes 154

17.2 History of Ghana’s Textile and Garment industry 154 17.3 Textile and Garment’s Diamond of National Advantage 156

17.3.1 Factor conditions 157 17.3.2 Domestic demand conditions 158 17.3.3 Related and supporting industries 159 17.3.4 Firm structure, strategy and rivalry 159 17.3.5 Influence of Government Policy 160

17.4 Summary and conclusion on Ghana’s Textile and Garment industry 161

V CONCLUSIONS ON DETERMINANTS OF COMPETITIVE ADVANTAGE 163

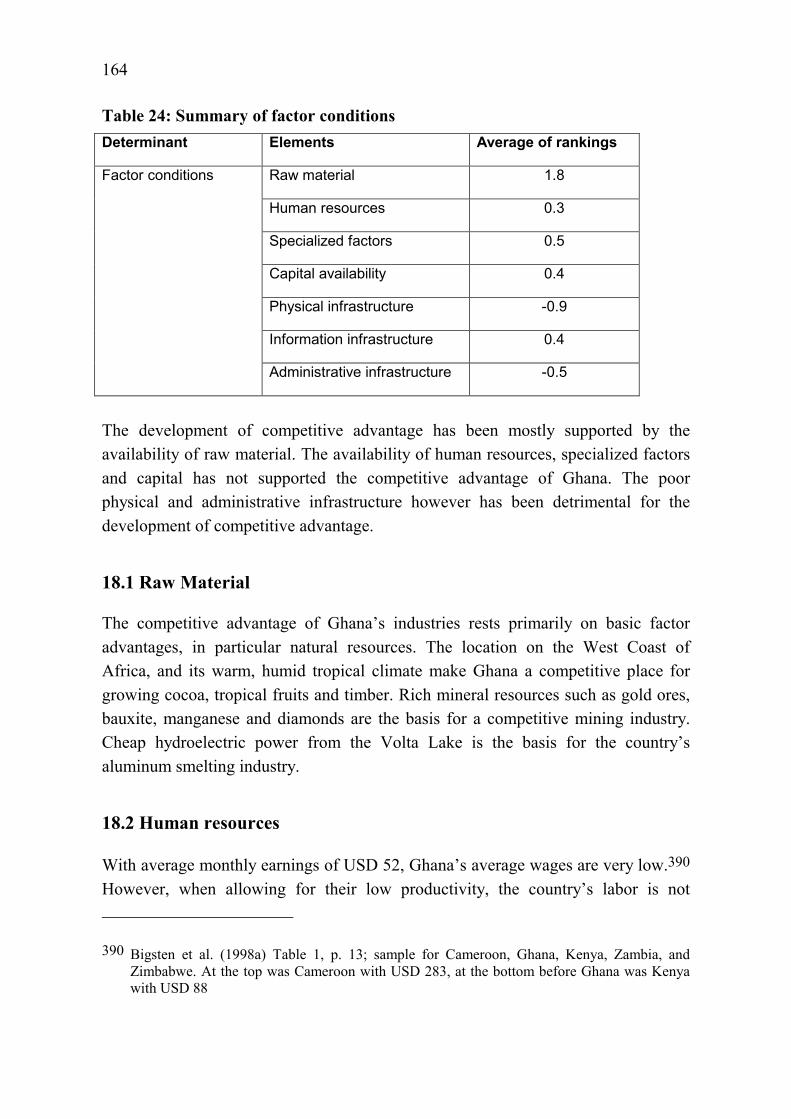

18 Factor conditions 163 18.1 Raw Material 164 18.2 Human resources 164

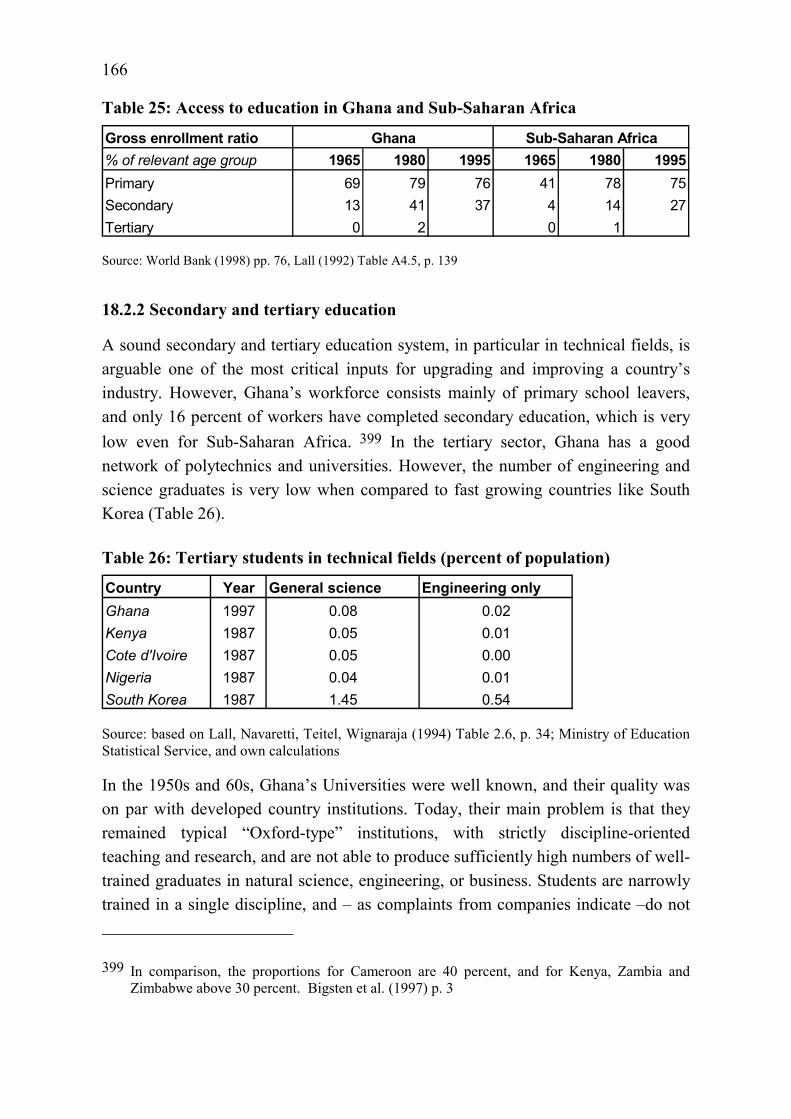

18.2.1 Basic education level 165 18.2.2 Secondary and tertiary education 166 18.2.3 Internal training 167

18.3 Specialized factors 168 18.3.1 Research and development 168 18.3.2 Management and entrepreneurship 168

18.4 Capital availability 169 18.5 Physical infrastructure 171 18.6 Information infrastructure 173 18.7 Administrative infrastructure 174 18.8 Conclusions on Ghana’s factor conditions 175

19 Demand conditions 177 19.1 Size of Ghana’s home market 178 19.2 Quality of Ghana’s home market demand 178 19.3 Conclusions on Ghana’s home demand 179

XII

20 Related and supporting industries 181 20.1 Presence of supporting industries 181 20.2 Presence of related industries 182 20.3 Conclusions on Ghana’s related and supporting industry 182

21 Strategy, structure, and rivalry 184 21.1 Structure and rivalry 184 21.2 Climate for investments 185

21.2.1 Investment and trade laws, taxes 186 21.2.2 Labor market policies 187 21.2.3 Political and economic uncertainty 187

21.3 Strategy 188 21.3.1 Strategic focus 188 21.3.2 Value chain presence 189 21.3.3 Management practices and goals of individuals 189

21.4 Conclusion on strategy and structure of Ghana’s industry 191

22 Government 192 22.1 The role of government in promoting competitive advantage 192

22.1.1 Ensure macroeconomic stability 192 22.1.2 Provide enabling microeconomic environment 193

22.2 Ghana’s macroeconomic and microeconomic track record 193 22.3 Ghana’s macroeconomic environment 195 22.4 Ghana’s microeconomic environment 197

22.4.1 Government influence on factor conditions 197 22.4.2 Government influence on demand conditions 203 22.4.3 Government influence on related and supporting industries 203 22.4.4 Government influence on firm strategy, structure, and rivalry 204

22.5 Conclusions on Ghana’s government 206

23 Summary - the challenges of Ghana’s Diamond of National Advantage 208 23.1 Nature of competitive advantage 208 23.2 Capacity to innovate 211 23.3 Conclusion 212 Sources 214

Literature 214 Interviews 227

XIII

Table of figures FIGURE 1: GOVERNMENT REVENUES FROM COCOA, 1956 - 1985 (PERCENT OF TOTAL) 12 FIGURE 2: COCOA PRODUCTION AND PRODUCER PRICES, 1950 - 1989 13 FIGURE 3: KEY ECONOMIC INDICATORS, 1965 - 1983 15 FIGURE 4: REAL EXCHANGE RATE CEDI/USD 1951 - 1985 16 FIGURE 5: DEVELOPMENT OF REAL GDP PER CAPITA, 1975 - 1998 22 FIGURE 6: FOREIGN DIRECT INVESTMENT INFLOW 1987 - 1998 23 FIGURE 7: GHANA’S GDP STRUCTURE, 1972-1996 24 FIGURE 8: AVERAGE PRODUCTIVITY RELATIVE TO BEST PRACTICE IN GHANA 25 FIGURE 9: EXPORT SHARE IN GDP BY EXPENDITURE CATEGORY, 1993 - 1997 31 FIGURE 10: EXPORT VALUES OF MAJOR PRODUCTS, 1983 – 1997 31 FIGURE 11: GHANA'S TOP TEN EXPORT DESTINATIONS, 1996 32 FIGURE 12: AFRICA'S COMPETITIVENESS INDEX, 2000 36 FIGURE 13: THE DIAMOND OF NATIONAL ADVANTAGE 45 FIGURE 14: FIVE FORCES DETERMINING INDUSTRY PROFITABILITY 49 FIGURE 15: FOUR GENERIC STRATEGIES 51 FIGURE 16: CLUSTER CHART TO HIGHLIGHT COMPETITIVE PATTERNS 63 FIGURE 17: GHANA'S ALUMINUM INDUSTRY, 1997 79 FIGURE 18: STRUCTURE OF GHANA'S COCOA INDUSTRY, 1997 95 FIGURE 19: EXPORTS OF RAW AND PROCESSED COCOA FOR MAJOR EXPORTERS, 1990 97 FIGURE 20: STRUCTURE OF GHANA'S FOOD INDUSTRY, 1997 113 FIGURE 21: GOLD PRODUCTION 1901 - 1995 129 FIGURE 22: STRUCTURE OF GHANA'S TIMBER AND FURNITURE INDUSTRY, 1997 139 FIGURE 23: STRUCTURE OF GHANA'S TEXTILE AND GARMENT INDUSTRY, 1997 152 FIGURE 24: INFLATION, EXCHANGE RATE AND INTEREST RATES IN GHANA, 1992 - 1997 196 FIGURE 25: TERMS OF TRADE AND PRICE DEVELOPMENT OF COCOA, GOLD, ALUMINUM 209

XIV

Table of tables TABLE 1: STRUCTURE AND RESEARCH DESIGN 5 TABLE 2: CHRONOLOGY OF MAJOR EVENTS, 1957 - 1996 10 TABLE 3: RELATIVE PRODUCTION VOLUME OF FOOD CROPS, 1962 – 1988 14 TABLE 4: DEVELOPMENT OF GHANA'S MANUFACTURING STRUCTURE, 1987 – 1993 28 TABLE 5: MAIN TRADE INDICATORS, 1989-1997 30 TABLE 6: CONSTRAINTS ON ECONOMIC FREEDOM IN GHANA, 1997 39 TABLE 7: OVERVIEW OF ELEMENTS OF COMPETITIVE ADVANTAGE REVIEWED 69 TABLE 8: CLUSTER CHART FOR COMPETITIVE UPSTREAM INDUSTRIES 72 TABLE 9: CLUSTER CHART FOR COMPETITIVE FINAL CONSUMPTION GOODS 73 TABLE 10: CLUSTER CHART FOR UNCOMPETITIVE UPSTREAM INDUSTRIES 75 TABLE 11: CLUSTER CHART FOR UNCOMPETITIVE FINAL CONSUMPTION GOODS 76 TABLE 12: DETERMINANTS OF ALUMINUM'S COMPETITIVE ADVANTAGE 85 TABLE 13: MARKET LEADERSHIP IN WORLD COCOA INDUSTRY 96 TABLE 14: OVERVIEW OF COCOA PRODUCER COUNTRY CHARACTERISTICS 98 TABLE 15: PERCENTAGE SHARE IN COCOA EXPORT REVENUES, 1995 99 TABLE 16: DETERMINANTS OF COCOA'S COMPETITIVE ADVANTAGE 103 TABLE 17: WHOLESALE PRICES FOR PINEAPPLES, 1997 114 TABLE 18: DETERMINANTS OF FOOD'S COMPETITIVE ADVANTAGE 118 TABLE 19: DETERMINANTS OF GOLD MINING’S COMPETITIVE ADVANTAGE 130 TABLE 20: EXPORTS OF GHANESE TIMBER PRODUCTS BY DESTINATION, USD '000, 1996 140 TABLE 21: DETERMINANTS OF TIMBER’S COMPETITIVE ADVANTAGE 144 TABLE 22: COST AND PRODUCTIVITY COMPARISONS FOR SHIRT PRODUCTION, 1994 154 TABLE 23: DETERMINANTS OF TEXTILE AND GARMENT'S COMPETITIVE ADVANTAGE 156 TABLE 24: SUMMARY OF FACTOR CONDITIONS 164 TABLE 25: ACCESS TO EDUCATION IN GHANA AND SUB-SAHARAN AFRICA 166 TABLE 26: TERTIARY STUDENTS IN TECHNICAL FIELDS (PERCENT OF POPULATION) 166 TABLE 27: RATES OF RETURN (PERCENT) TO HUMAN CAPITAL IN GHANA 168 TABLE 28: FINANCIAL MARKET RATES, 1991-1997 170 TABLE 29: GHANA'S PHYSICAL INFRASTRUCTURE COMPARED TO SELECTED COUNTRIES 171 TABLE 30: SUMMARY OF DEMAND CONDITIONS 177 TABLE 31: SUMMARY OF RELATED AND SUPPORTING INDUSTRIES 181 TABLE 32: SUMMARY OF FIRM STRUCTURE, STRATEGY, AND RIVALRY 184 TABLE 33: SUMMARY OF GOVERNMENT DETERMINANTS 193 TABLE 34: WORLD BANK EVALUATION OF GHANA’S ECONOMIC REFORMS - OVERVIEW 194 TABLE 35: GOVERNMENT SPENDING ON EDUCATION AND ECONOMIC SERVICES 198 TABLE 36: PUPIL/TEACHER RATIOS AND PERCENTAGE OF TRAINED TEACHERS 199 TABLE 37: PUBLIC EXPENDITURE ON EDUCATION, SELECTED COUNTRIES 200 TABLE 38: SAVING AND INVESTMENT (PERCENT OF GDP) 201 TABLE 39: OVERVIEW OF BUSINESS REGULATION CHANGES 205

XV

Abbreviations CAGR Compound annual growth rate

CMB / Cocobod Cocoa Marketing Board

ECOWAS Economic Community of West African States

e.g. For example

ERP Economic Reform Program

EU European Union

FAO Food and Agricultural Organization

FDI Foreign direct investment

FOB Free-on-board

GATT General Agreement on Tariffs and Trade

GDP Gross domestic product

GNP Gross national product

ha Hectares

HS Harmonized System (trade classification system)

i.e. that is to say

IMD IMD School, Lausanne

IMF International Monetary Fund

kg Kilogram

km Kilometer

MWh / gWh Mega Watt hours / Giga Watt hours

N/A Not available

OECD Organization for economic cooperation and development

p.a. Per annum

R&D Research and Development

SITC Standard International Trade Classification

SOE State-owned enterprise

UKP British pound

UN United Nations

US United States

USD US Dollar

1

I INTRODUCTION

Chapter 1 of the introduction describes the importance of analyzing the competitiveness of Ghana’s industries. The second chapter outlines the research approach with the main questions, the framework for analysis and the research design.

1 Motivation

Over the last 15 years, Ghana has become a showcase of successful macroeconomic reforms and stabilization programs.1 Starting with its economic reform program in 1983, Ghana’s government has managed to achieve a broad budget balance, to implement a system of flexible exchange rates, and to liberalize the country’s trade regime. Also, it started to install an investor-friendly regulatory environment, initiated the privatization of 230 state owned enterprises, and began to significantly reduce the export tax on cocoa, the country’s second most important export product after gold. However, the currently low GDP growth rates indicate that this has not been sufficient. Even though the structural adjustment program provided the basis for sustainable economic development, Ghana’s economic performance has been relatively disappointing. Between 1985 and 1995, Ghana’s total GNP grew by 4.2 % p.a., and real GDP per capita had an average annual growth of 1.3 percent. Exports, though they had been growing at a rate of 7.5 percent annually between 1990 and 1997, made up only 13 percent of GDP between 1990 and 1995.

Ultimately, a nation’s productivity, the prerequisite for prosperity, is the sum of the productivity of its companies. Their productivity is driven by three variables: (1) stable political and legal institutions coupled with macroeconomic stability; (2) an enabling microeconomic business environment, such as infrastructure and education standards; (3) the strategies and operational structures of the private sector, which determine the sophistication with which companies produce and compete.2 The objective of Ghana’s current government is to make Ghana a middle-income country within one generation. To achieve this, it plans to double Ghana’s annual economic growth rate from the

1 Reflected in articles and comments like NZZ December 19, 1994, p. 11 “Ghana weiterhin Westafrikas Hoffnungsträger”; and World Bank (1994) p. 69: “Ghana as most advanced trade policy reformer in Sub-Saharan Africa after Mauritius”

2 See Porter (1998a) p. 41

2

current 4 percent to about 8 percent for the next 30 years, with agriculture’s share dropping to 20 percent of GDP, and industry’s share rising to 37 percent by the year 2020.3 To realize this ambitious growth target for industrial development, Ghana needs much more vigorous private sector participation and investments from home and abroad. However, “while much progress has been made in understanding the macroeconomic side of development, there has been an increasing recognition that macroeconomic reform is necessary but not sufficient. As, or more, important are the microeconomic foundations of development, rooted in the nature of firm strategies and in the institutions, resources, and policies that constitute the environment in which firms compete.”4 Ghana has worked intensively on implementing structural reforms and providing a stable macroeconomic environment, but the effect has not met its expectations. This could be either because the macroeconomic reforms did not go far enough, or because other conditions needed for the successful development of industries5 have been lacking. To guide the actions of Ghana’s government, an analysis is needed on the conditions of the variables that are responsible for the success or failure of industries, and how these conditions should be improved.

3 Presidential Report to Parliament (1995) p. vii; for the industrial sector this translates into 12% annual growth, ibid. p. 36

4 Porter (1997) p. x 5 In the context of this work, ‘industry’ is used to describe a sector of the nation’s economy, equal

to the German connotation ‘Industriezweig’ or ‘Branche’. Unlike many research papers on Africa’s and Ghana’s industrial development (see for instance Teal (1998a&b); Elbadawi (1999); Biggs et al. (1996); Lall, Navaretti, Teitel, Wignaraja (1994)) the focus here is not exclusively on the performance of the manufacturing sector, but includes all sectors of the economy.

3

2 Research approach

2.1 Main question and contribution

The objective of this thesis is to understand the specific conditions that enabled individual industries in Ghana to become internationally competitive. The main questions of my thesis are:

¶ Which industries in Ghana are globally competitive?6

¶ What are the success conditions that have led to a competitive advantage of certain industries in Ghana?

The contribution of this research has two elements. The first is the application of Porter’s framework developed in “Competitive Advantage of Nations” to Ghana, to analyze and explain the competitiveness of Ghana’s industry. The second element is the conclusions from the analysis of Ghana’s industry. These conclusions could be the basis for policy actions to improve the current conditions for competitiveness.

2.2 Framework for analysis

To analyze the industry of Ghana and to determine the conditions that make certain industries successful, a framework is required that allows structuring all the factors influencing an industry’s competitiveness in a consistent and convincing way.

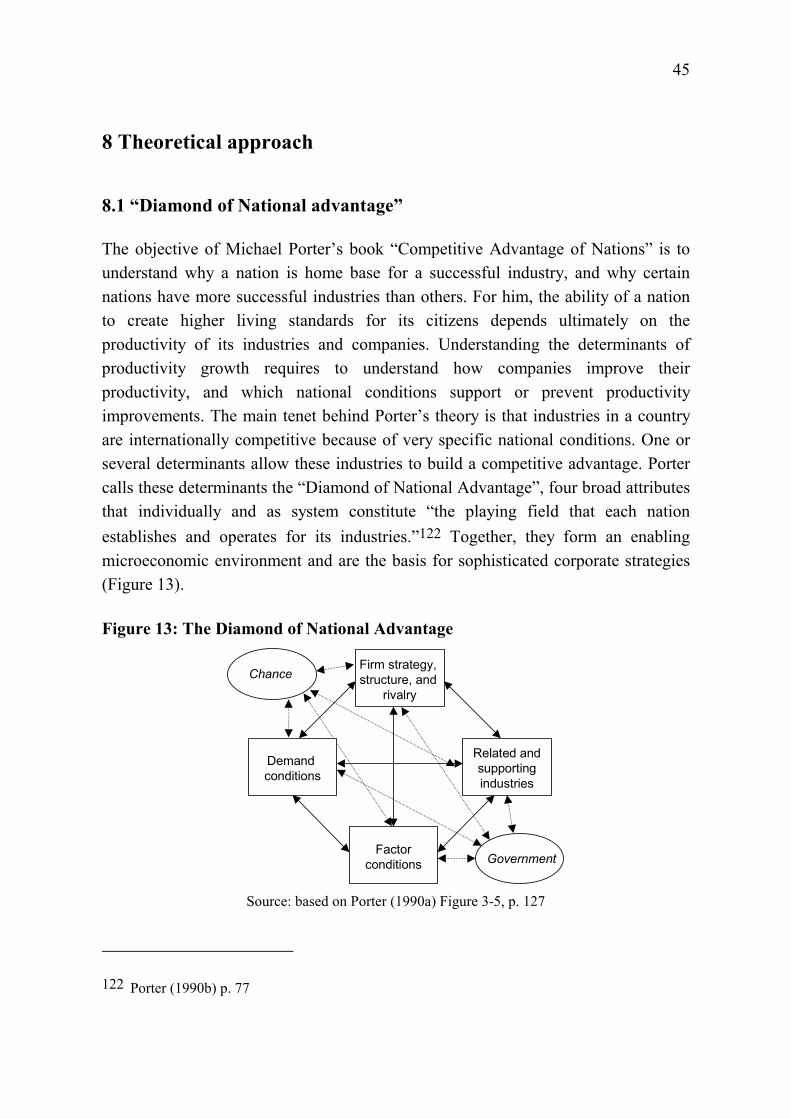

The framework used in this thesis is based on Michael Porter’s ‘Diamond of National Advantage’; a framework developed to answer the question why a nation is home base for a globally competitive industry.7 There are two major reasons for using this framework to analyze the competitiveness of the Ghanaian industry. First, it is internally consistent, with an empirically tested methodology, based on extensive empirical research on several industries in ten countries.8 Second, it goes down to the level of the individual industries, and produces very specific recommendations on what to change to make a particular industry more successful.

6 For the definitions of “industry” and “competitiveness” see Chapter 7 7 Developed in Porter (1990a &b)

4

The ‘Diamond of National Advantage’ as a framework encompasses the influencing factors on a company’s productivity: the macroeconomic conditions, the microeconomic business environment, and a company’s strategy and organization.

The framework will be adapted to the specific conditions of Ghana and changed to incorporate aspects that are different from Porter’s original question.9 In this adapted form, the framework allows to structure the answer to the two main questions of this thesis: Which industries located in Ghana are internationally competitive, and what are the conditions that enabled them to be internationally successful. The answer is then the basis for a discussion on how Ghana’s ‘Diamond of National Advantage’ could be upgraded and improved.

2.3 Working hypothesis

In Ghana, there are companies and industries that are able to successfully compete on the World market. They are internationally competitive because of certain conditions in Ghana, and because the economic reform program has improved some conditions for doing business in Ghana. Other industries, however, in which both the government and the private sector have invested significantly, have not managed to compete successfully on the World market, or against imports.

Two main hypotheses will be analyzed:

1. The continuing dependence on natural resources did not create advanced factors such as specially skilled labor or innovative processes

2. Ghana’s structural adjustment program has not gone far enough, and regulatory uncertainty, unpredictable macroeconomic policy and bureaucratic inefficiency did not create a microeconomic environment conducive to business

The analysis of competitive industries in Ghana should allow us to verify whether these hypotheses are correct, or whether other reasons are responsible for the competitiveness of Ghana’s industries.

8 Porter (1990b) p. 76 9 One of the most important adaptations is the focus on all companies within Ghana. Porter only

analyzed the companies that had their home base in the nation researched. This thesis will also look at foreign direct investment in Ghana to understand the overall attractiveness of a country’s economic environment.

5

2.4 Data availability

The main challenge to overcome in this thesis was to work with partially incomplete and inconsistent information. As in many other developing countries, Ghana’s statistical data is often incomplete, or inconsistent if compared across different sources. This concerns in particular data on Ghana’s trade activities, information on foreign investment activities, and information on the structure of industries or individual companies. To alleviate the problem of unreliable information, all important information was reviewed with personal interviews and crosschecked with information from other sources as far as possible.

2.5 Structure and research design

The thesis has five major parts. After the introduction, the second part provides a brief overview on the structure of Ghana’s economy. The third part is a critical review of the Porter theory and methodology, with adaptations to the methodology to apply it to Ghana. The fourth part is the application of the methodology to analyze the competitiveness of Ghana’s industry. The fifth part summarizes the findings from the analysis of Ghana’s competitive industries to describe Ghana’s determinants of competitive advantage (Table 1).

Table 1: Structure and research design I. Introduction

II. Overview of Ghana’s Economy III. Theoretical and methodological concepts

Theoretical approach Methodology IV. Analysis of competitiveness of Ghana’s industries

V. Conclusions on determinants of competitive advantage Factor

conditions Demand

conditions Related & Supporting industries

Strategy, Structure, & Rivalry

Influence of Government

Policy

6

7

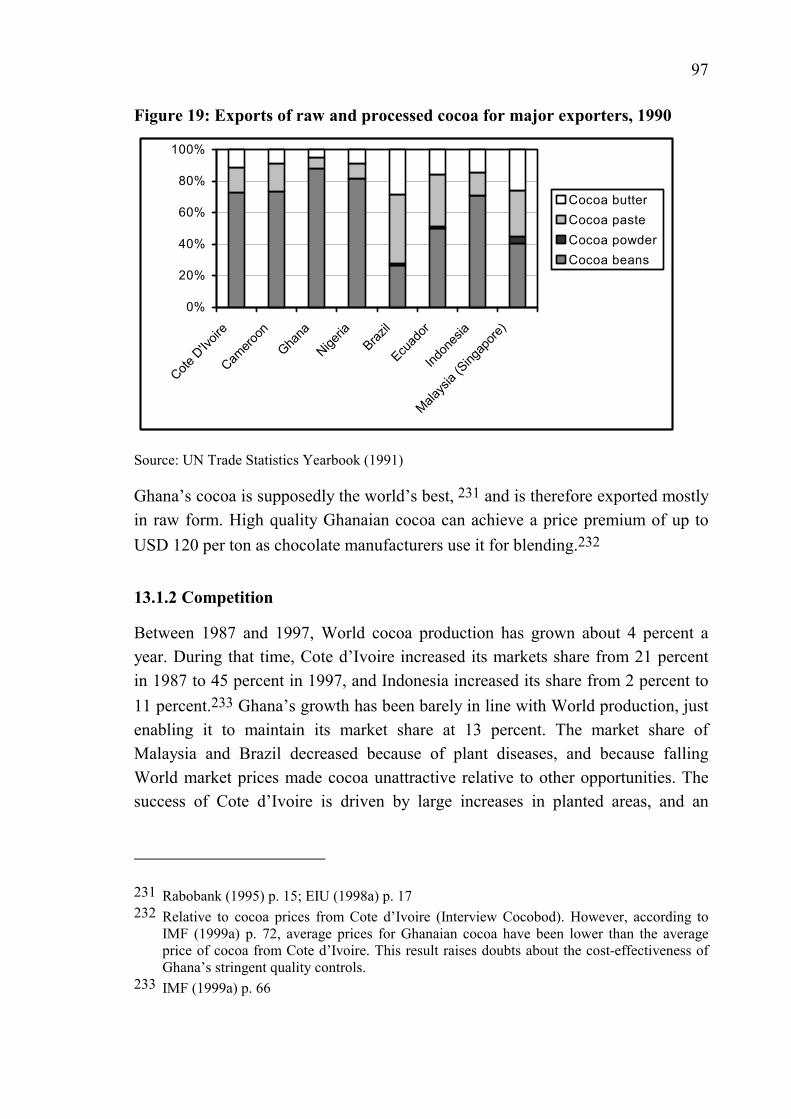

II OVERVIEW OF GHANA’S ECONOMY

Part II provides an overview of Ghana’s economy and its development, for a better understanding of the general conditions for Ghana’s industries and companies. Chapter 3 describes the historic developments that have formed the structure of Ghana’s economy. In Chapter 4 the current economic situation of Ghana is described, followed by a brief look at the three main sectors of the economy. Chapter 5 discusses the role of trade in the Ghanaian economy. Chapter 6 is a review of the current research on Ghana’s competitiveness.

3 The political background of Ghana’s economic development

The objective of this chapter is to give a brief overview on the political economy of Ghana. The first part explains the main political elements responsible for the country’s decline from independence until the start of structural economic reforms in 1983. The second part describes what actions were taken in the economic reform program to reverse Ghana’s economic decline.

3.1 The political economy of Ghana until 1983

Ghana’s current economic structure is significantly dominated by the activities and structures that were established with the beginning of colonialism in the 19th century, and that have been subsequently reinforced throughout independence until today.

3.1.1 Trade in gold and slaves main source of profit before colonialism

West Africa has been connected to Europe already for several hundred years through the trade across the Sahara. In the 15th century, the Portuguese were the first Europeans to establish a trading mission on the Gold Coast, followed by the English, Swedish, Danish and Dutch. In that time, trade with Ghana was mainly in gold. In the 16th century, about 10% of the global gold production were mined in Ghana.10

Gold, however, was soon to be replaced by slaves: for about two centuries, the coastal and Ashanti tribes provided more than half a million slaves to European traders, not

10 Von Gnielinski (1986) p. 76

8

counting those that had died while being captured, or during the transportation to the coast.11 The effects of the slave trade were clearly detrimental to the development of the Gold Coast. The continuous raids on villages disrupted all economic activities in the country, and mostly the young and vigorous were captured as slaves. Mining was abandoned because mining workers from Benin were pulled away by the slave trade,12 and early cottage manufacturing activities were eroded by cheaper imports from Europe as payments for slaves.

3.1.2 Specialization on cocoa during colonial rule

The end of the slave trade in the 19th century marked the beginning of the British Gold Coast colony. Several wars were started between the Ashanti and the coastal tribes, whose living had depended upon slave trade. As these wars started to touch the interests of British merchants, the British government decided to intervene, won the war against all parties involved, and proclaimed the Gold Coast formally as a colony.

West Africa was not chosen to be a settler’s colony, and the British governed their West African colonies indirectly, by establishing close relationships with the local rulers. The West African colonies were an excellent location to produce cash crops like cocoa, coffee, cotton, and rubber, in exchange for manufactured items from Europe.13 The Gold Coast became the most important producer for cocoa and gold, and by 1911 the country was the world’s largest cocoa exporter, producing about 40% of the total World supply between 1920 and 1940.14 The cocoa production itself remained almost entirely in African hands, and is still today dominated by smallholder farming. However, cocoa trade was firmly controlled by European trading houses and the colonial government. As a result of improved transportation and communication, companies like Cadbury’s were able to establish their own agencies, displacing most African trading firms.15 These trading oligopolies also had sole import and distribution rights for certain British goods, and pushed small newcomers out of the market through destructive price-cutting.

11 La Verle (1995) p. 133 12 Agbodeka (1992) p. 34; see also Petchenkine (1993) pp. 147 13 Agbodeka (1992) p. 71 14 Rimmer (1992) p. 20 15 In the mid 1930s, less than 1% of the cocoa shipped abroad came from indigenous traders, while

the top four Gold Coast trading firms controlled 70% of the exports. Kennedy (1988) p. 36 and 39

9

The British rule provided a relatively stable legal and political structure, and led to a remarkable increase in agricultural output, and investments in infrastructure and education.16 However, while the British initiated the building of infrastructure to transport the cash crops to the coast, they prevented the development of indigenous industries in order to keep the colonies as a protected market for their own manufactured exports.17 In several industries, trading licenses had to be acquired from the government, making most kinds of business more or less illegal for Africans. By forbidding or licensing the import of machinery, and with export bans on items such as locally woven cloth, the government consciously clamped down all major industrialization efforts.18 Ghanaians had limited access to financing because of the difficulty of getting a collateral to secure bank loans, as most of the land was still owned communally.19 As a result, African entrepreneurs and traders were confined to traditional activities in which the European firms had no commercial interests. This was mostly internal trade in foodstuffs between the forest and Savannah areas of West Africa, or small-scale commercial ventures at the bottom of the European trading hierarchy. When the British left the Gold Coast, the colony was focused on the extraction of minerals and the production of cash crops. While the Africans had solid trading experience, there was no industrial base, and limited entrepreneurial experience to manage large industrial corporations.

3.1.3 The history of decline: 1957 to 1983

Ghana started independence with over UKP 500 Million in foreign exchange reserves, and a GDP per capita of about USD 300, making it a middle-income country with a per capita income equal to South Korea at that time.20 Even though a solid industrial base was lacking, the country had inherited from the British a sound economy that had experienced sustained growth over the past decades.21 In fact, the economy appeared

16 Kennedy (1988) p. 12 17 See also Frimpong-Ansah (1991) p. 47 on the theory of that a colonial predatory state survives

primarily because of superior military technology, and has no real interest in the development of a colony if this conflicts with the economic goal of the ruling country.

18 Agbodeka (1992) p. 135 19 Kennedy (1988) p. 40 20 Leith, Lofchie (1993) p. 226 21 Alpine, Pickett (1993) p. 91

10

stable and prosperous, with the country being the worlds leading cocoa producer, boasting a well-developed infrastructure and relatively advanced education system.22

By 1983, after 36 years of independence (Table 2), Ghana had a GDP per capita of USD 300, not higher than at the beginning of independence. Production of cocoa, the main export product over all these years, had dropped from a peak of 572,000 tons in 1964 to 180,000 tons in 1983. Between 1960 and 1982, the productivity of labor had declined by 3.6 percent p.a., and the productivity of capital declined 2.0 percent p.a., with total factor productivity for all sectors of the economy decreasing by 2.3 percent p.a.

Table 2: Chronology of major events, 1957 - 1996 Year Events

1957 Independence, Nkrumah as prime minister

1964 Single party (CPP) government

1965 1st serious drop in World market price of cocoa (from USD 467/t to USD 91/t)

1966 Military coup against Nkrumah and establishment of National Liberation Council (NLC)

1967 Devaluation of cedi from 0.71 cedi/USD to 1.02 cedi/USD

1969 Election of K. Busia

1971 2nd serious drop in World market price of cocoa (from USD 517/t to USD 289/t), devaluation of cedi from 1.02/USD to 1.82/USD, followed by urban unrest

1972 Military coup overthrows Busia, and establishment of National Redemption Council under Acheampong, revaluation of cedi to 1.15/USD, import and exchange controls tightened

1975 Acheampong replaces NRC by Supreme Military Council.

Investment Policy Decree to establish minimum 55 percent Ghanaian ownership of all manufacturing enterprises

1978 Acheampong replaced by General Akuffo, cedi devalued to 2.75/USD, triggering urban strikes and unrest

1979 Military coup by J.J. Rawlings, SMC replaced by lower ranks with Armed Forces Revolutionary Council, elections won by Limann

1981 New coup by Rawlings to establish Provisional National Defense Council

1982/83 Series of disastrous events: drought and fires, murder of judges, expulsion of 1 million Ghanaians from Nigeria, failed coup attempt, 3rd serious drop in World market price of cocoa (from USD 2935/t to USD 980/t)

1983 Economic Recovery Program launched, cedi devalued to 30/USD

1986 Auction system for foreign exchange introduced, import licensing abandoned, new mining code established

22 La Verle (1995) p. 134

11

1988 Foreign exchange bureaus established

1989 Initialization of privatization of State-owned enterprises (SOEs)

1992 New constitution introduced, with multiparty elections. Retired flight-lieutenant J.J. Rawlings elected as president

1994 Implementation of fully liberalized investment code

1996 J.J. Rawlings reelected to president for second term, leading National Democratic Congress has 132 (of 200) seats in parliament

Source: Leith, Lofchie (1993) Table 6.1, p. 231; EIU (1997a) pp. 7; Dordunoo, Nyanteng (1997) pp. 18

As will be shown further on, the origin of Ghana’s economic decline was the transfer of resources from the highly profitable cocoa sector to finance state-owned industries, coupled with a regime of import substitution that protected indigenous companies from efficient foreign competition. Rampant corruption and private rent seeking aggravated the detrimental effects of this policy, which was nourished by a system of import licenses and foreign exchange quotas. The consequence of this policy was a steady decline of cocoa exports, leading to serious balance of payment deficits, high inflation, and finally to the collapse of the economy in 1983.

3.1.4 The basis for decline: Nkrumah’s industrialization program

When Nkrumah took over as the first president of Ghana, he believed that growth and development in Ghana would only come from massive investment into the mechanization of agriculture and industrial development. His economic goal was to diversify Ghana’s economic base through industrialization, thereby reducing the country’s exposure to World commodity price fluctuations.

Industrialization was to be achieved with two instruments: a protectionist trade regime, and state-owned enterprises. Ghana’s entrepreneurial class was judged too small to take over a leading role in such a massive industrialization effort, and a strong local entrepreneurial class also represented a political threat.23 In line with Nkrumah’s socialist background, it was the government that had to assume responsibility for both the selection of appropriate sectors, and the management of the state-owned enterprises. The main source of revenues for this massive industrialization program was the export earnings from agricultural commodities, primarily cocoa (Figure 1).

23 Aryeetey, Baah-Nuakoh, Duggleby, Hettige, Steel (1994), p. 4

12

Figure 1: Government revenues from cocoa, 1956 - 1985 (percent of total)

0%

5%

10%

15%

20%

25%

30%

35%

40%

1956-60 1961-65 1966-70 1971-75 1976-80 1981-85

Source: Jakobeit (1991) Table 12.2

Since 1939, colonial statutory marketing boards controlled the export of cocoa and other cash crops. Originally, the purpose of these produce-buying boards was to cut the link between fluctuating World prices and local prices. The Cocoa Marketing Board (CMB) would buy the goods at from the producer at a fixed price, and sell them at the World price. Depending on the direction of change, it might either make a loss or a surplus. The surplus would be kept as a stabilization reserve to finance deficits of other seasons. In reality, however, the statutory monopoly boards had already in colonial times produced a high rate of enforced and collectivized savings,24 and functioned almost never to design. The marketing boards acted as monopsonies, paying fixed prices to African farmers well below World market export prices. The accumulated funds were either invested in British government securities – leading to large outflows of capital to finance the British wars – or were used for investments in infrastructure building.25 After independence, the CMB became the funding agency for government development plans, as well as a source of public employment and political patronage. 26 Between 1949 and 1985, payments to farmers exceeded the CMB’s FOB sales only once, and in only 14 years did the farmers receive more than 50% of the gross value of their crops (Figure 2).

24 Rimmer (1992) p. 42 25 Kennedy (1988) p. 15, Schmidt-Kallert (1994) p. 41. Compare Rimmer (1992) pp. 41 for a

detailed account on the differences between original objectives and reality. 26 By the end of 1982, the Cocoa Marketing Board had more than 100’000 people on its payroll.

Rimmer (1992) pp. 201

13

Figure 2: Cocoa production and producer prices, 1950 - 1989

0

100

200

300

400

500

600

700

1955

/56

1957

/58

1959

/60

1961

/62

1963

/64

1965

/66

1967

/68

1969

/70

1971

/72

1973

/74

1975

/76

1977

/78

1979

/80

1981

/82

1983

/84

1985

/86

1987

/88

Crop year

CMBpurchases('000 tons)

Real producerprice per ton,indexed (1963= 500)

Source: Jakobeit (1991) Table 12.2; Leith, Lofchie (1993) Table 6.2, p. 232

The CMB was a central instrument to shift resources from the rural population to the urban dwellers. To promote industrial development, the government was willing to sacrifice the interests of the farmers, since its political survival depended primarily on the happiness of urban workers,27 and because only little opposition was expected from the rural population.28

To limit the impact of reduced prices for export crops, a large number of farmers switched to alternative products that were not under the control of the government, but could be sold freely in the market. As a result, food production fell continuously, with

27 The push towards independence had been initialized by urban riots in 1948. Unemployment among ex-servicemen and primary school leavers, a shortage of housing and sharp rises in the cost of imported consumer goods were the main reasons for the urban discontent. The urban social groupings were the main constituents of Nkrumah's Convention People’s Party, the main political force in the Gold Coast and Ghana until 1966. The political power of urban workers was revealed again in 1972, when the Busia government was overthrown in a military coup after it had tried to devalue the cedi. This devaluation prompted again urban unrest since prices of imported consumer goods had gone up. Bates (1981) p. 33; Leith, Lofchie (1993) p. 228

28 The cost of organized opposition is significantly higher for the rural population than for the urban population. Their attachment to their land limits their possibilities to participate in national politics, and being disunited, there was no effective way to protect their interests. As a result, farmers used the market as a less costly alternative, and shifted production to other products. See Bates (1981) p. 82

14

the food self-sufficiency ratio dropping from 83 percent in 1961-66 to 71 percent in 1978-80 (Table 3).29

Table 3: Relative production volume of food crops, 1962 – 1988

1962 1982 1988

Cocoa 100 56 48

Rice 100 116 270

Maize 100 157 341

Millet 100 117 295

Sorghum 100 81 170 Source: Alpine, Pickett (1993) Table 25

Ghana’s method of implementing its import substituting industrialization policy led to dismal results from the beginning. The number and range of industries chosen for protection were vast, and no economic criterion for their selection could be identified.30 A chaotic mix of subsidized credits, tariffs, import quotas, exchange controls and outright import bans granted protection from cheaper imports.31 The state-owned enterprises (SOEs) had virtually unlimited borrowing rights from the banking system, and made substantial losses early on.32

To add to the inefficiency of Ghana’s SOEs33 and the poor performance of the agricultural sector, personal rent seeking consumed even more of the country’s economic resources. The public service organization was not very well developed and driven beyond its capabilities.34 The weakness of the administration combined with the political elements of import licensing and state-owned industries provided ample

29 La Verle (1995) p. 159 30 Well illustrated by the fact that at the end of the 1970s, Ghana had 36 car assembly plants and 40

pharmaceutical manufacturers. Asamoa (1996) p. 80 31 See also Pickett, Shaeldin (1990) pp. 25 32 Leith, Lofchie (1993) p. 237. For background on the ideological foundations of Ghana’s

industrialization policy see ibid. pp. 240 33 See Rimmer (1992) p. 91. In 1967, out of a sample of 40 firms, broadly representative for large-

scale manufacturing, only six were efficient in the sense that they were transforming domestic resources into foreign exchange at a rate equal or less than the official value. A further four companies were efficient if the shadow exchange rate was considered. In the large mechanized farms, the production of rice fell from 1.11 tons/ha in 1962 to 0.59 tons/ha in 1982. Alpine, Pickett (1993) Table 14

34 Frimpong-Ansah (1991) p. 44

15

opportunity for personal enrichment in public office.35 Incidents involving massive corruption became known early on, but were popularly tolerated.36 Personal rent seeking, coupled with strong interest groups, also explains why the policies that had shown to be ineffective already in the mid 1960s, were pursued for almost twenty more years.37

3.1.5 “Killing the golden geese”, the consequences of failed policies

Ghana’s desolate economy in the early 1980s was marked by chronic inflation, fueled by fiscal deficits (Figure 3).38

Figure 3: Government surplus and inflation, 1965 - 1983

-60

-40

-20

0

20

40

60

1965 1970 1975 1976 1977 1978 1979 1980 1981 1982 1983

0

20

40

60

80

100

120

140Governmentsurplus (cedis100 million),left axis

Rate ofinflation(percent), rightaxis

Source: Leith, Lofchie (1993) Table 6.2, p. 232

Between 1965 and 1980, agricultural output increased at an average annual rate of 1.6 percent, while manufacturing grew by 2.5 percent per year.39 The implicit taxation of

35 Import licenses and tariffs were based on 6-digit code, allowing a very precise definition of the relevant products. This indicates that they were geared towards the protection of individual firms. Furthermore, import licenses were issued for a commission, payable to the responsible minister in person. Bates (1981) p. 67 & p. 101

36 In Ashanti, using political authority to accumulate, display and enjoy wealth is part of an indigenous historical tradition, and patronage is even socially obligatory. Rimmer (1992) p. 46

37 Leith, Lofchie (1993) p. 245 38 Alpine, Pickett (1993) p. 91 39 Pickett, Shaeldin (1990) p. 22

16

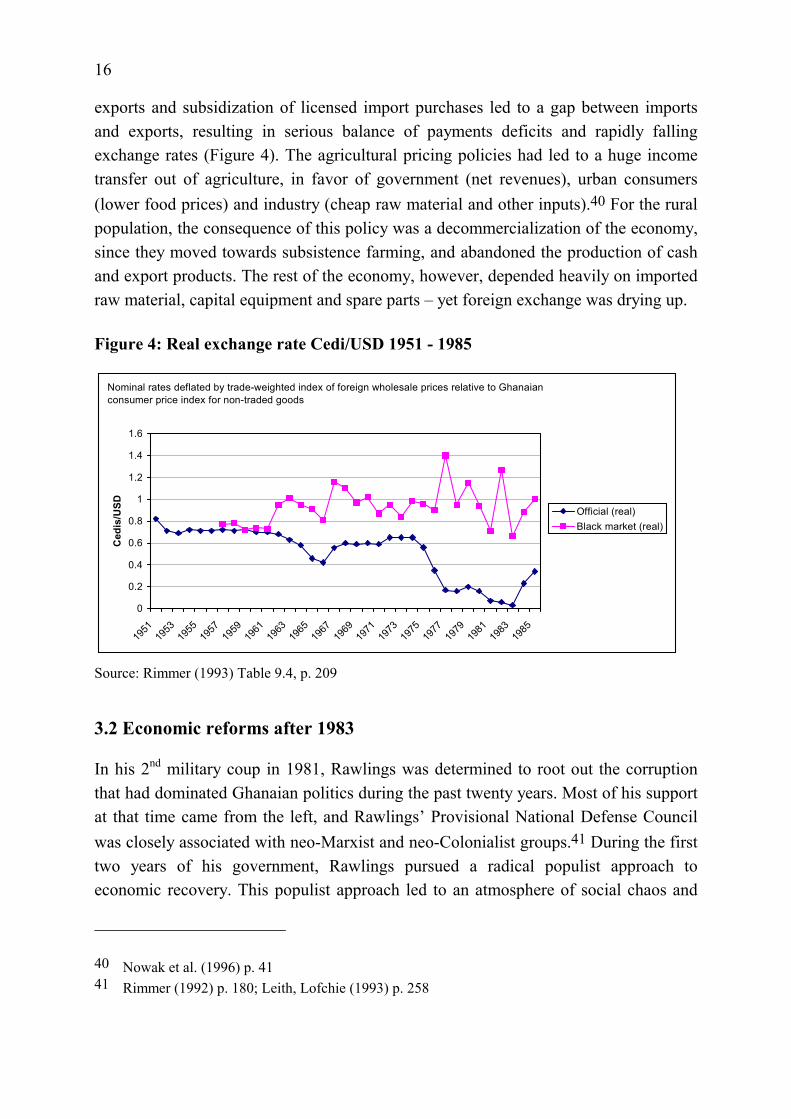

exports and subsidization of licensed import purchases led to a gap between imports and exports, resulting in serious balance of payments deficits and rapidly falling exchange rates (Figure 4). The agricultural pricing policies had led to a huge income transfer out of agriculture, in favor of government (net revenues), urban consumers (lower food prices) and industry (cheap raw material and other inputs).40 For the rural population, the consequence of this policy was a decommercialization of the economy, since they moved towards subsistence farming, and abandoned the production of cash and export products. The rest of the economy, however, depended heavily on imported raw material, capital equipment and spare parts – yet foreign exchange was drying up.

Figure 4: Real exchange rate Cedi/USD 1951 - 1985

Nominal rates deflated by trade-weighted index of foreign wholesale prices relative to Ghanaian consumer price index for non-traded goods

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1951

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

Ced

is/U

SD Official (real)Black market (real)

Source: Rimmer (1993) Table 9.4, p. 209

3.2 Economic reforms after 1983

In his 2nd military coup in 1981, Rawlings was determined to root out the corruption that had dominated Ghanaian politics during the past twenty years. Most of his support at that time came from the left, and Rawlings’ Provisional National Defense Council was closely associated with neo-Marxist and neo-Colonialist groups.41 During the first two years of his government, Rawlings pursued a radical populist approach to economic recovery. This populist approach led to an atmosphere of social chaos and

40 Nowak et al. (1996) p. 41 41 Rimmer (1992) p. 180; Leith, Lofchie (1993) p. 258

17

further decline, and Ghana was unsuccessful in getting assistance from the “true friends of Africa”, the Soviet Union, Eastern Europe, Cuba or Libya.42 By 1983, the lack of external support and a series of other events such as the drop in cocoa prices and the expulsion of a large number of Ghanaians from Nigeria had brought Ghana close to economic collapse. When Rawlings turned to the IMF and the World Bank as lenders of last resort, neither would provide financial aid without major economic reforms.43

The virtual breakdown of the country’s economy enabled Rawlings to break with the politics of the past. Even though the detrimental effects of the policies of the 1970s had been transparent before, they were kept alive because they generated rents for the supporters of these regimes. In the beginning of the 1980s, however, the real exchange rate had dropped to 10 percent of the rate at independence. Export earnings had been eroded, credits from donors and commercial sources dried up, and there was no more foreign exchange available for distribution of rent-generating import licenses. The glue that held the former regimes together had vanished. The reforms were widely supported, as there was no additional hardship from the structural adjustment measures. The educational system and health care had ceased to deliver services to the majority of the population.44 And finally, the real purchasing power had already fallen as the official prices, salaries and exchange rates had no economic function anymore.

3.2.1 Main elements of Ghana’s Economic Reform Program

Ghana’s Economic Recovery Program (ERP) had five key objectives:45 (1) The realignment of relative prices to encourage production and exports; (2) a progressive shift from direct intervention towards the reliance on market forces; (3) the restoration of fiscal and monetary discipline; (4) the rehabilitation of social and economic infrastructure; and (5) structural and institutional reforms to enhance the efficiency of the economy and to encourage the expansion of savings and investments.

42 Rimmer (1992) p. 180 See also Ahiakpor (1985) for an account about Rawlings’ transformation. This brief period of radicalism has not yet been forgotten by many Ghanaian business people, who still do not sincerely trust in Rawlings’ economic policy, and are skeptical about his attitude towards private business.

John Kufuor defeated presidential candidate of the opposition NPP in 1996, has been cited with the words in the Financial Times, June 22, 1998 (Database download): “Fidel Castro remains his idol. His closest advisers have been card-carrying communists.”

43 Leith, Lofchie (1993) p. 266 44 Compare Leith, Lofchie (1993) p. 263, and p. 259 45 See Kapur et al. (1991) for a detailed description

18

The devaluation of the cedi and the liberalization of the exchange rate were the first reform steps undertaken. As a start in 1983, the Rawlings government introduced export bonuses and import surcharges, two measures that had the same effect as devaluation but needed not to be communicated as such.46 After half a year, the taboo of devaluation had been broken, and the government devalued the cedi continuously until 1986, when it introduced an auction system to depoliticize the exchange rate policy and to remove the burden of acting from the government. As a final step, the government absorbed the remaining parallel market in 1988 by establishing foreign exchange bureaus.47 In the view of many Ghanaians, the creation of these exchange bureaus had made market-determined foreign exchange a permanent fixture, the basis for the belief in the sustainability of the economic reforms.48 In parallel to the liberalization of the exchange rate reform, the country’s trade and investment policies were reformed. The government eliminated the highly complex import licensing system that had been the basis for political favourism and corruption. For almost all imports a uniform tariff was established.

While trade reforms were implemented very rapidly, the complex legal and regulatory framework for investments and corporate taxes was dismantled only slowly. In 1991, the government called in an advisory group to identify constraints on the private sector and to pave the way to revisions in the regulatory framework.49 However, a fully liberalized investment code was only established in 1994, incorporating a broad range of investment incentives. The privatization of Ghana’s SOEs was initiated in 1987, but started only in 1992. During the first phase of the ERP, Ghana’s reform strategy was not to reduce the SOE sector, but to expose it to competition as a forcing device. Only after 1992 did the divestiture program really start. By the end of 1998, 212 of the more than 300 SOEs had been either sold or liquidated. However, sectors such as transportation (airlines, ports) and utility (electricity, oil) are still government monopolies dominated by SOEs.50

46 Rawlings exchange rate policy was not in line with the ‘cold turkey’ policy recommended by the IMF, as he considered this equal to political suicide. Urban unrest and political turmoil had always followed devaluation of the cedi in previous regimes, with the consequence that all Ghanaian governments used every trick to disguise devaluation. See Herbst (1993) p. 53

47 Kapur (1991) pp. 17 - 21 48 Leith, Lofchie (1993) p. 271 49 Nowak et al. (1996) p. 38 50 Divestiture Implementation Committee, Web page (April 1998)

19

Together with the institutional reforms, Ghana also made strong efforts to adjust its fiscal and monetary policy. To establish a solid fiscal basis, Ghana simplified and rationalized its tax system to improve both its efficiency and equity.51 On the income side, tax exemptions and tax brackets were reformed to reduce the progressivity of personal income tax, corporate taxes were reduced and sectoral differences were removed. Expenditures were cut and restructured to favor development and rehabilitation activities. The main measures were a reduction of subsidies for agricultural inputs coupled with the removal of price controls, the introduction of cost recovery programs in health care and education,52 and a significant reduction of the civil service.53 In order to keep a stable monetary environment and to enable credits to the private sector, restrictive monetary and credit policies were implemented to reduce government borrowing from the banking system. Monetary control was to rely on market-based instruments, and credit controls and administrative interest rates were dismantled. To rebuild the country’s decrepit infrastructure and to start industrial production, a USD 4.2 billion program was prepared by the IMF and the World Bank for infrastructure repair, energy imports, and the import of key inputs for the export industries.54

3.2.2 Political structure since 1992

Since 1992, Ghana is a constitutional democracy based on the US system, with executive power in the president, who is elected by universal suffrage every four years, with tenure limited to two four-year terms. The cabinet is appointed by the president and approved by a single-chamber parliament.

Ghana’s last elections in 1996 resulted in a second term of Rawlings and his party, the National Democratic Congress. Support for the NDC comes mainly from rural areas, where people have benefited most from the economic reforms. Ghana has two major opposition parties: one is the People’s Convention Party, which consists largely of left leaning groups and Nkrumahists. The other opposition force is the New Patriotic Party,

51 Roe, Schneider (1992) p. 75 52 The impact of these measures was not so adverse because formal charging combined with

improved availability of items such as textbooks and drugs partly replaced the informal costs of delays and bribes associated with a system characterized by chronic shortages and very low quality of service. Roe, Schneider (1992) p. 75

53 Relative to the size of the population, Ghana in 1992 still had one of the largest civil services in Africa. Leechor (1994) p. 167

54 La Verle (1995) p. 145

20

which is dominated by lawyers, academics and business people, and is largely identified with the Ashanti region.55

55 EIU (1998b) p. 8

21

4 The structure of Ghana’s economy

The objective of this chapter is to first describe the impact of the ERP on Ghana’s economy, and then to briefly introduce the characteristics of Ghana’s agricultural, industrial, and service sector.

4.1 Ghana’s macroeconomic development after the ERP

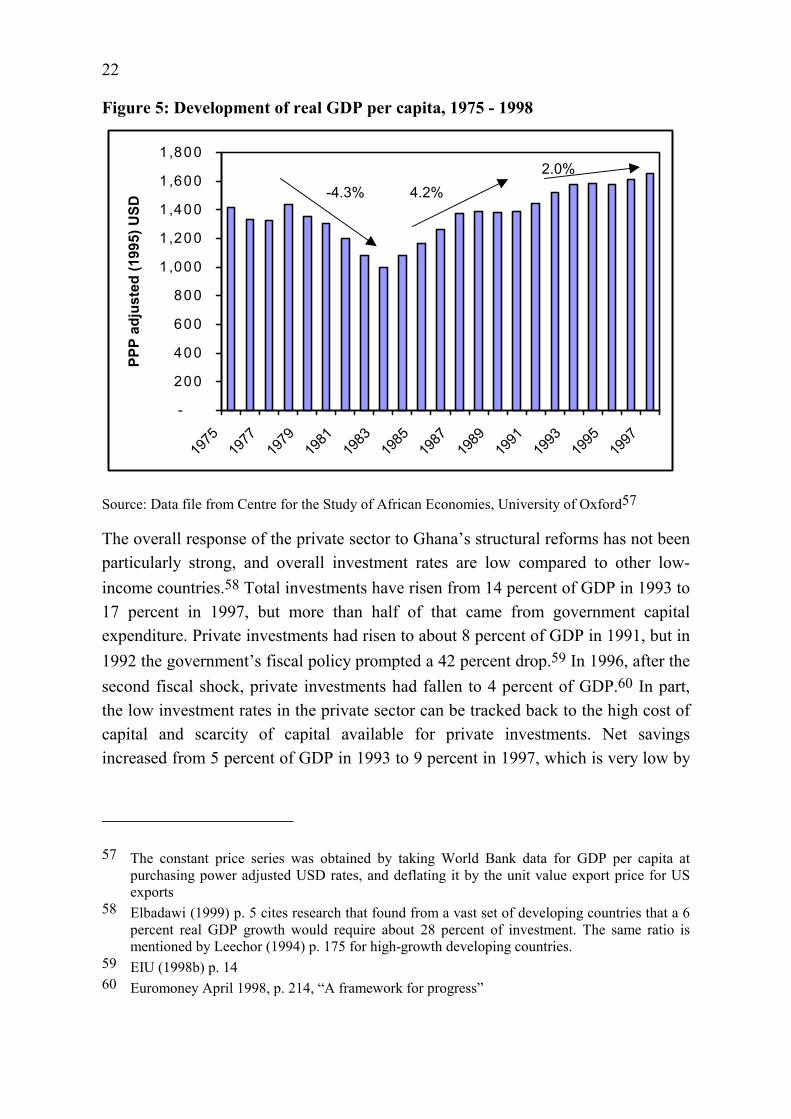

Ghana’s reform program was implemented in three phases: In the first phase between 1983 and 1986, the focus was on getting prices right, and on reducing the government’s budget deficit by increasing revenues. Between 1987 and 1990, efforts were concentrated on the initiation of structural changes, such as the liberalization of the exchange rate and the trade system, the start of the SOE divestiture program, and civil service reforms. In the third phase, after 1990, the government started to look at the more demanding structural and institutional reforms.56

The implementation of these policies resulted in a major turnaround between 1983 and 1991. Inflation declined, the overall balance of payment position stabilized, and GDP growth recovered from negative numbers to about 5.5 percent p.a., and the real GDP per capita grew by 4.2 percent p.a. After 1991, Ghana’s macroeconomic performance suffered a marked downturn. In 1992, as part of its election campaign, the government granted large increases in wages and benefits for public sector employees. This fiscal shock helped to fuel inflation, and led to an increase in government debt. In the election year 1996, the government repeated the same mistakes as in 1992, when spending levels were massively increased and the government deficit rose from 6 percent to 10 percent of the GDP. Between 1992 and 1998, GDP growth averaged 4.2 percent, and real GDP per capita 2.0 percent p.a. (Figure 5).

56 Kapur et al. (1991) p. 57

22

Figure 5: Development of real GDP per capita, 1975 - 1998

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1975

1977

1979

1981

1983

1985

1987

1989

1991

PPP

adju

sted

(199

5) U

SD

Source: Data file from Centre for the Study of African Economies, Unive

The overall response of the private sector to Ghana’s structuraparticularly strong, and overall investment rates are low coincome countries.58 Total investments have risen from 14 perc17 percent in 1997, but more than half of that came fromexpenditure. Private investments had risen to about 8 percent o1992 the government’s fiscal policy prompted a 42 percent drosecond fiscal shock, private investments had fallen to 4 percethe low investment rates in the private sector can be tracked bcapital and scarcity of capital available for private inveincreased from 5 percent of GDP in 1993 to 9 percent in 1997

57 The constant price series was obtained by taking World Bank dapurchasing power adjusted USD rates, and deflating it by the unit exports

58 Elbadawi (1999) p. 5 cites research that found from a vast set of depercent real GDP growth would require about 28 percent of invementioned by Leechor (1994) p. 175 for high-growth developing cou

59 EIU (1998b) p. 14 60 Euromoney April 1998, p. 214, “A framework for progress”

% %

2.0

4.2% -4.31993

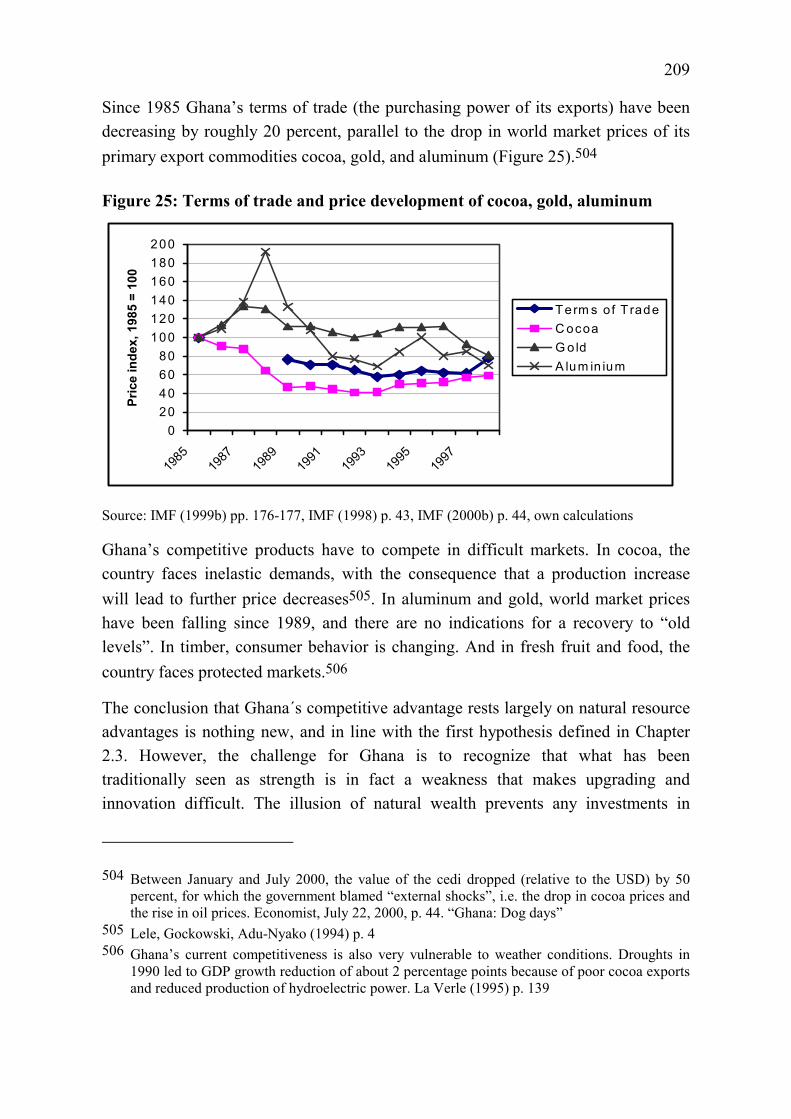

1995

1997

rsity of Oxford57

l reforms has not been mpared to other low-ent of GDP in 1993 to government capital

f GDP in 1991, but in p.59 In 1996, after the nt of GDP.60 In part,

ack to the high cost of stments. Net savings , which is very low by

ta for GDP per capita at value export price for US

veloping countries that a 6 stment. The same ratio is ntries.

23

international and also by Sub-Saharan African standards.61 In addition, uncertainty about the government’s long-term attitude towards private enterprises probably increased the cost of capital and further reduced the incentives for capital investments.

Foreign aid, debt, and direct investments have financed most of Ghana’s increase in investments. In 1997, per capita aid averaged about USD 50, more than double the Sub-Saharan average, and contributed about 55 percent to the total investment level.62 Foreign direct investments (see Figure 6) were substantial between 1993 and 1996 when the gold mining industry was privatized, but have declined since then.

Figure 6: Foreign direct investment inflow 1987 - 1998

050

100150200250

1987-1992(avg)

1993 1994 1995 1996 1997 1998

USD

mill

ion

Source: UNCTAD (1999), Annex table B.1, p. 478

4.2 Sectoral structure of Ghana’s economy

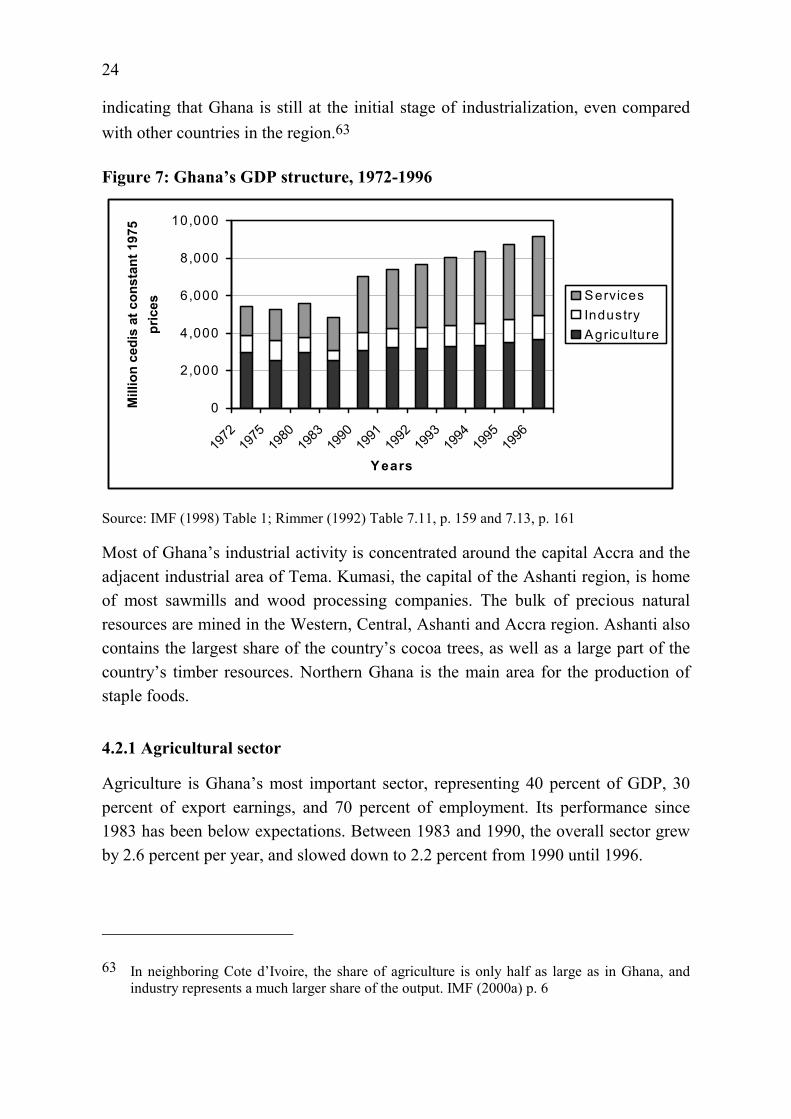

Ghana’s economy continues to be dominated by the agricultural sector. Although its importance has diminished since 1972, it is still responsible for 40 percent of the GDP. The second largest sector after agriculture is the service sector, in particular trading. Industry only commands about 15 percent of the GDP (see Figure 7),

61 Saving rates from CEPA (1998) p. 17. The Sub-Saharan average is about 13 percent; the Asian average is about 28 percent of GDP. Leechor (1994) p. 174

62 IMF (2000a) p. 16. According to CEPA (1998) p. 25, foreign aid made up 70 percent of total government development capital expenditure.

24

indicating that Ghana is still at the initial stage of industrialization, even compared with other countries in the region.63

Figure 7: Ghana’s GDP structure, 1972-1996

0

2,000

4,000

6,000

8,000

10,000

1972

1975

1980

1983

1990

1991

1992

1993

1994

1995

1996

Y ears

Mill

ion

cedi

s at

con

stan

t 197

5 pr

ices

ServicesIndustryAgriculture

Source: IMF (1998) Table 1; Rimmer (1992) Table 7.11, p. 159 and 7.13, p. 161

Most of Ghana’s industrial activity is concentrated around the capital Accra and the adjacent industrial area of Tema. Kumasi, the capital of the Ashanti region, is home of most sawmills and wood processing companies. The bulk of precious natural resources are mined in the Western, Central, Ashanti and Accra region. Ashanti also contains the largest share of the country’s cocoa trees, as well as a large part of the country’s timber resources. Northern Ghana is the main area for the production of staple foods.

4.2.1 Agricultural sector

Agriculture is Ghana’s most important sector, representing 40 percent of GDP, 30 percent of export earnings, and 70 percent of employment. Its performance since 1983 has been below expectations. Between 1983 and 1990, the overall sector grew by 2.6 percent per year, and slowed down to 2.2 percent from 1990 until 1996.

63 In neighboring Cote d’Ivoire, the share of agriculture is only half as large as in Ghana, and industry represents a much larger share of the output. IMF (2000a) p. 6

25

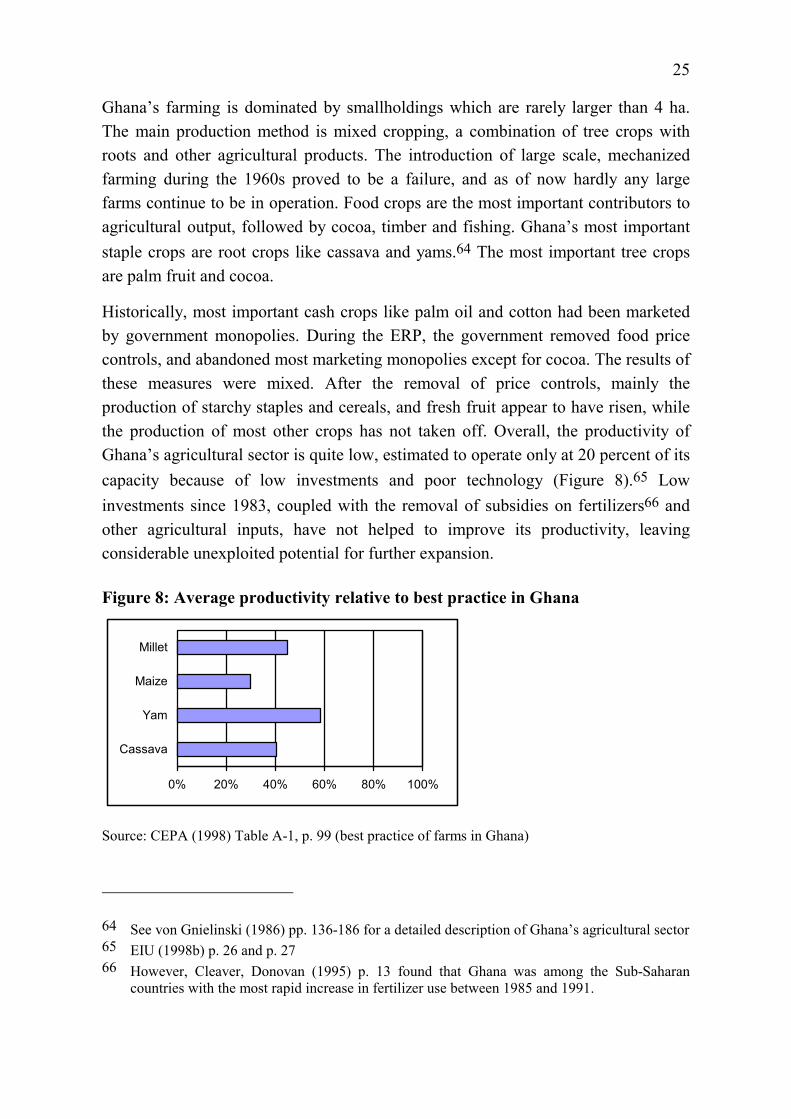

Ghana’s farming is dominated by smallholdings which are rarely larger than 4 ha. The main production method is mixed cropping, a combination of tree crops with roots and other agricultural products. The introduction of large scale, mechanized farming during the 1960s proved to be a failure, and as of now hardly any large farms continue to be in operation. Food crops are the most important contributors to agricultural output, followed by cocoa, timber and fishing. Ghana’s most important staple crops are root crops like cassava and yams.64 The most important tree crops are palm fruit and cocoa.

Historically, most important cash crops like palm oil and cotton had been marketed by government monopolies. During the ERP, the government removed food price controls, and abandoned most marketing monopolies except for cocoa. The results of these measures were mixed. After the removal of price controls, mainly the production of starchy staples and cereals, and fresh fruit appear to have risen, while the production of most other crops has not taken off. Overall, the productivity of Ghana’s agricultural sector is quite low, estimated to operate only at 20 percent of its capacity because of low investments and poor technology (Figure 8).65 Low investments since 1983, coupled with the removal of subsidies on fertilizers66 and other agricultural inputs, have not helped to improve its productivity, leaving considerable unexploited potential for further expansion.

Figure 8: Average productivity relative to best practice in Ghana

0% 20% 40% 60% 80% 100%

Cassava

Yam

Maize

Millet

Source: CEPA (1998) Table A-1, p. 99 (best practice of farms in Ghana)

64 See von Gnielinski (1986) pp. 136-186 for a detailed description of Ghana’s agricultural sector 65 EIU (1998b) p. 26 and p. 27 66 However, Cleaver, Donovan (1995) p. 13 found that Ghana was among the Sub-Saharan

countries with the most rapid increase in fertilizer use between 1985 and 1991.

26

Given the current level of technology, farming labor is already scarce.67 No “Green Revolution” as in Asia is likely to take place as long as slow technological innovation and poor infrastructure blunt farmer’s incentives to switch from extensive subsistence farming to market-focused, intensive production. No agricultural machinery is used, irrigation is absent, and a large part of the land is still under shifting cultivation.68 Outputs remain very vulnerable to weather conditions,69 which has a large effect on the country’s export earnings as well as domestic inflation. A large amount of the output is wasted along the value chain – mainly because of the absence of adequate storage facilities, very poor rural roads and the dominance of human portage.70

The growth experience from Asia points towards agriculture as initial impetus for rapid development. Profits from agriculture would create export surpluses, which can then be used to finance growth in manufacturing and manufactured exports. Ghana, however, has not been able to achieve a similar agriculture-led growth path. The key shortcomings of its reforms were, as critiques point out, a too slow upgrading of the agricultural infrastructure, such as extension services, feeder roads, and urban markets. At the same time, the slow removal of marketing and distribution monopolies gave farmers not enough incentives to push up their production.71

4.2.2 Mining and manufacturing sector

Between 1990 and 1996, the total sector has grown at 4.2 percent, with most of the growth coming from the mining and construction-related sector. Ghana’s mining sector is dominated by gold mining. With the introduction of a new mineral law in 1986 and the privatization of the country’s largest gold mines, the mining industry has been thriving, and gold output has increased more then five-fold between 1987 and 1996 (see Figure 21: Gold production 1901 - 1995, p. 129). Ghana is one of the

67 World Bank (1993) p. 33 68 Cleaver, Donovan (1995) p. 24 69 Only about 1.1 percent of West Africa’s arable land is irrigated. See Aspesi, Lloyd, Crenshaw,

D’Oyen, Yeboah-Amankwah, Abiola (1998) 70 Aspesi, Lloyd, Crenshaw, D’Oyen, Yeboah-Amankwah, Abiola (1998) estimate that every

year in Ghana about USD 110 million of maize are being lost between the field and end consumer, mainly because of the inability to draw on a sufficiently large labor pool during the harvest, old storage facilities, and bad transportation.

71 See Nowak et al. (1994) p. 42

27

world’s largest exporters of manganese, and mines some bauxite and diamonds. The diamond, manganese and bauxite sectors have also recovered after considerable contraction during the decline in the 1970s, increasing its output by almost 50 percent between 1990 and 1996.72

The impact of the ERP on the manufacturing sector has been mixed. Ghana has a broad industrial base across almost all sectors. Most of today’s larger manufacturing companies were established as state-owned enterprises in the 1960s. Between 1983 and 1990, the manufacturing sector grew by 8.1 percent per year, benefiting from the availability of imported inputs, which enabled them to use their existing excess capacity. From 1990 onwards, growth slowed to 2.2 percent, mainly because of the exposure to import competition; and the abandonment of subsidies forced companies to rationalize and improve their performance. Employment in manufacturing fell from 78’000 in 1987 to 28’000 in 1993,73 and the number of companies between 1987 and 1993 declined by 21 percent, from 634 companies to 500 companies (Table 4).

The largest sector in manufacturing – based on gross output – are the non-ferrous metal industry, the wood industry, food manufacturing, chemical products and tobacco manufacturing, which accounted for 54 percent of the gross output in 1993.74 Most seriously hit by import competition were the food, textile, furniture and chemical industry, where a significant number of companies were forced to close down. While both the food and chemical industry managed to recover in terms of output, the textile industry continues to do badly.

72 IMF (2000a) p. 10 73 African Development Bank, cited in Lall (1995) p. 2025, not fully consistent with Ghana’s

Manufacturing Survey cited below. 74 Based on Ghana Manufacturing Survey 1993. Another survey had been planned for 1998, but

was not executed because of lack of financing.

28

Table 4: Development of Ghana's manufacturing structure, 1987 – 199375 USD million (at average rate)Industry 1987 1993 1987 1993 1987 1993 1987 1993Food manufacturing 88 43 11'628 7'418 135 146 42 51Beverage industry 27 27 5'057 3'418 84 97 68 56Tobacco manufacturers 4 3 1'856 1'060 66 124 59 110Textile, wearing apparel and leather 117 43 14'018 10'654 72 98 35 31Wood and cork products excl. furniture 97 81 18'328 21'987 83 163 43 93Furniture and fixture excl. metal 67 29 3'886 2'855 10 10 5 5Manufacture of paper products 5 13 761 1'461 6 25 3 11Printing, publishing and allied industries 40 48 4'518 4'391 13 24 8 8Manufacture of industrial chemicals 13 7 747 512 10 24 4 5Manufacture of other chemical products 37 42 3'729 4'455 59 142 21 54Petroleum refineries 2 2 678 399 165 95 37 50Manufacture of rubber products 5 6 1'140 2'741 5 6 3 3Manufacture of other plastic products 5 31 319 2'963 3 43 2 16Manufacture of non metallic minerals 30 30 3'133 3'305 34 88 16 27Iron and steel basic industries 3 3 571 1'362 5 16 2 4Non-ferrous metal basic industries 6 5 2'276 2'483 207 171 83 50Metal products 31 41 2'978 3'553 26 51 12 21Manufacture of machinery 12 11 946 646 2 5 1 2Electrical machinery, appliances 13 18 935 1'166 8 23 4 9Other 32 17 1'767 1'827 8 17 3 4Total Manufacturing Sector 634 500 79'271 78'656 1'001 1'372 452 610

Companies Persons engaged Gross output Value added

Source: Ministry of Trade and Industry (Ghana Manufacturing Survey, 1987); Addo, Julemun, Sonntagbauer (1995)

In general, firms operating in export-oriented sectors, and established multinationals have fared better than small and medium-scale industries, because these companies had better access to credit and better marketing opportunities for their products,76 and they were better able to circumvent the problems resulting from poor infrastructure. Most hard hit were large, inefficient SOEs, which suffered not only from huge inefficiencies and management faults, but also from high wages and non-wage liabilities.

4.2.3 Service sector

Ghana’s service sector has been the fastest growing sector of the economy, with a growth rate of 5.9 percent between 1990 and 1996. The bulk of service activities are in trading and public services. Trading in particular is one of the activities that benefited from the contraction of the manufacturing services and absorbed part of

75 Includes companies with more than 20 employees 76 Teal (1995) p. 4; Financial Times, July 9, 1996: “Ghana 1996: Hard times for manufactures”

29

their unemployed workers.77 Transportation services have grown only slowly because of substantial structural problems, such as a poor road and railway system.

One of Ghana’s promising service sectors is tourism, which has become the country’s third largest foreign exchange earner.78 The country’s main attractions are the beaches and the former slave castles along the Atlantic coast, and the cities Accra and Kumasi.

After the initiation of the ERP, Ghana’s financial sector incurred serious difficulties. The devaluation of the cedi had raised the external liabilities of the banks, and at the same time weakened many of their customers who depended on imported material. The financial sector reform program was initiated in 1988. Its main elements were the introduction of a new regulatory base with new capital adequacy rules, a clean-up of the banks’ balance sheets through a swap of all nonperforming loans against government loans, and individual restructuring for some distressed banks.79 The largest commercial banks have been privatized, and in 1990 a stock exchange was established. Today, there are six commercial banks with about 280 branches across the country, the three largest banks, Ghana Commercial Bank, Standard Chartered, and Barclays, share 70 percent of the deposit volume. Three development banks focus on the manufacturing, agricultural, and construction sector. Five merchant banks are specialized on corporate finance activities. About 120 rural banks, owned and managed by local residents, provide financing for small-scale agricultural activities and cottage industries. In addition, there are about 16 insurance companies active in Ghana, as well as several security brokerages, export financing and leasing companies, and venture capital funds. The Ghana stock exchange, currently the fifth largest in Africa, has 21 companies listed. At 4 percent turnover and with very high bid/ask spreads, the country’s stock market remains one of the world’s least liquid exchanges.80 Ashanti Goldfields accounts for 64 percent of the USD 1.4 billion market capitalization.81 Besides Ashanti, the manufacturing and brewing sector dominate the exchange, followed by the banking sector. Many of the listed companies are local subsidiaries of foreign multinationals.

77 See also Canagarajah, Mazumdar (1997) p. 50 78 US Department of Commerce (2000) Chapter 1 79 Kapur (1991) p. 60 80 EIU (1999) p. 21 81 Year end 1998

30

5 The role of foreign trade in Ghana’s economy

Ghana’s total volume of foreign trade, both imports and exports after exclusion of aid-funded imports, is about 35 percent of GDP – considerably lower than the trade level for other high-growth countries, which are often above 100 percent of GDP.82

Ghana’s exports continue to be dominated by primary commodities, namely gold and cocoa. The country’s terms of trade have been declining rapidly between 1989 and 1993 as a result of falling gold and cocoa prices.83 Capital goods, intermediate goods, and fuel and energy dominate Ghana’s import bill.84 Increasing energy shortages requiring additional fuel imports, and a decline in gold prices have led to a worsening of Ghana’s trade balance particularly in 1997 (Table 5).

Table 5: Main trade indicators, 1989-1997

USD million 1989 1990 1992 1993 1994 1995 1996 1997 1998

Total exports 808 897 988 1,064 1,227 1,431 1,810 1,810 2,091

Total imports 1,006 1,205 1,457 1,728 1,580 1,687 2,296 3,041 2,897

Trade balance -198 -308 -468 -664 -353 -256 -485 -1,231 -806

Terms of Trade (1985=100) 76.7 71 65 58 60 64 62 62 78 Source: IMF (1999a) Table 51&52, pp. 133-134; IMF (2000) Table 33 & 34, pp. 43-44

5.1 Overview of Ghana’s export structure

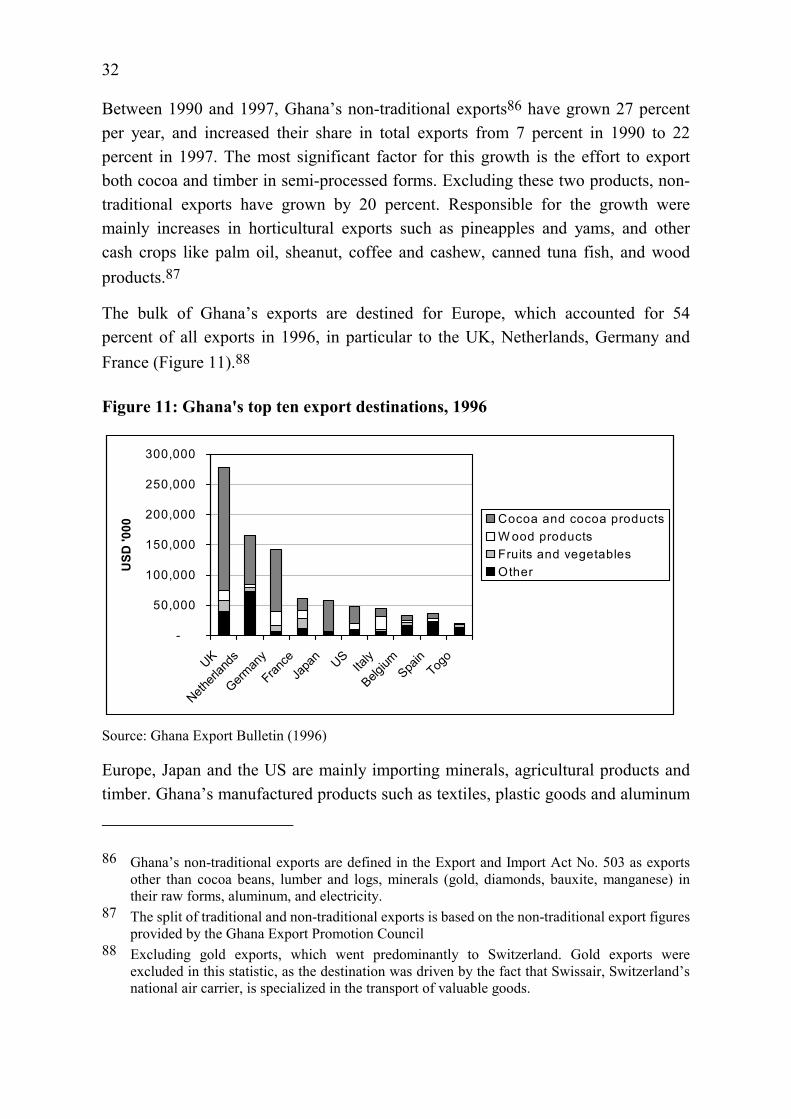

Between 1990 and 1997, Ghana’s total exports have grown 7.5 percent per year, from USD 897 million to USD 1.5 billion. While in 1990, exports made up 16 percent of GDP, by 1997 its share had grown to 25 percent of GDP (Figure 9).

82 Leechor (1994) p. 175 83 The terms of trade express the purchasing power of a country’s exports in terms of the imports