Globale Anforderungen der Flugzeugentwicklung ...gelhfrankfurt.de/PDF DATEIEN/2016-11-11 Globale...

39

PRIVATE AND CONFIDENTIAL © Bombardier Inc. or its subsidiaries. All rights reserved. Globale Anforderungen der Flugzeugentwicklung Technologieentwicklung und Paradigmenwechsel Sichtweise Betreiber – Entwickler - Einkauf Nico Buchholz, Sr. Vice President & CPO Sources all charts: Bombardier, Lufthansa Fleet Management, N.Buchholz incl 2013 & European Business School lecturing papers

Transcript of Globale Anforderungen der Flugzeugentwicklung ...gelhfrankfurt.de/PDF DATEIEN/2016-11-11 Globale...

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

ba

rdie

r In

c. o

r its s

ub

sid

iarie

s. A

ll rig

hts

re

se

rved

.

Globale Anforderungen

der Flugzeugentwicklung

Technologieentwicklung

und Paradigmenwechsel

Sichtweise Betreiber –

Entwickler - Einkauf

Nico Buchholz, Sr. Vice President & CPO

Sources all charts:

Bombardier, Lufthansa Fleet

Management, N.Buchholz incl

2013 & European Business

School lecturing papers

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

2

Corporate structure

Global aerospace and rail transportation leader with $18.2B in revenues

1. Bombardier Inc. owns 100% of the CRJ Series and Q Series commercial aircraft programs.

2. Including intersegment revenues

Note: Revenues are for the fiscal year ended December 31, 2015. The C Series Aircraft Limited Partnership did not

recognize any revenues in 2015.

30%49.5%

50.5% 70%100%1 100%

Bombardier Inc.Government of Québec

Caisse de dépôt et placement du Québec (CDPQ)

C Series Aircraft Limited

Partnership

Bombardier

Commercial

Aircraft

Bombardier

Business

Aircraft

Bombardier

Aerostructures

and Engineering

Services

Bombardier

Transportation

100%

Revenues

$7.0B

Revenues2

$1.8B

Revenues

$8.3B

Revenues

$2.4B

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

3

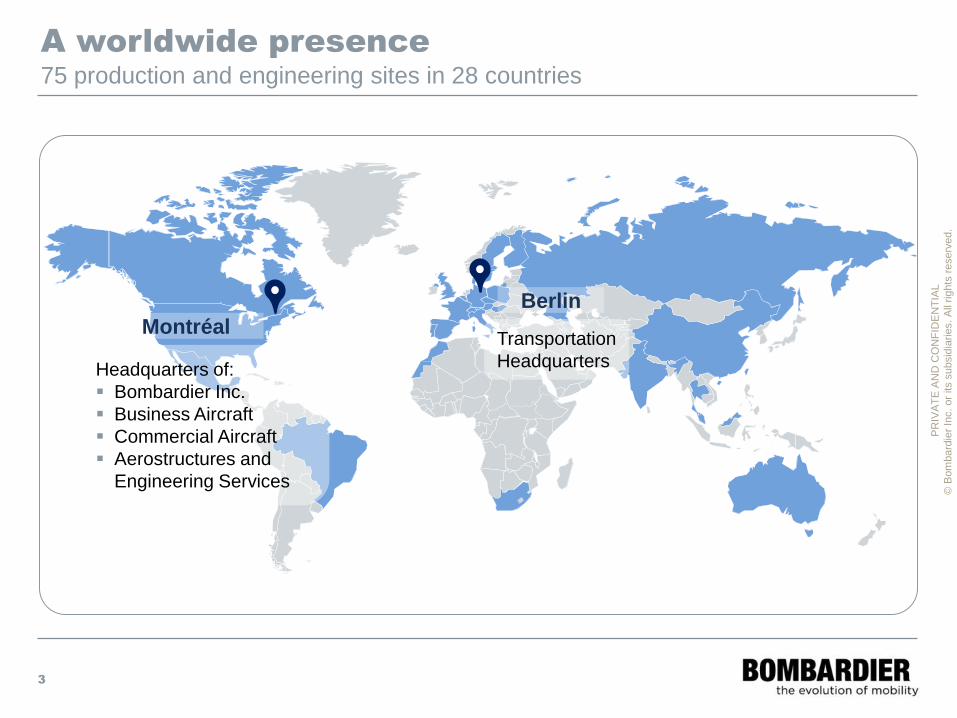

A worldwide presence

75 production and engineering sites in 28 countries

Montréal

Berlin

Headquarters of:

Bombardier Inc.

Business Aircraft

Commercial Aircraft

Aerostructures and

Engineering Services

Transportation

Headquarters

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

4

TRANSPORTATION

Market share by region

We have the broadest portfolio of rail solutions globally

In Europe, BT is the

market leader in all

major rolling stock

segments

Market leader for

metros in North

America, the biggest

segment of the region

Strong in India and

leader in the fast

growing Australian

market

Highest global

market share, making

BT the industry leader

outside China

Queensland Rail

New Generation

R179 New YorkRegio 2N FranceTRAXX South Africa

#2

#1 BT ~32%

#2 #2#3

BT ~38%

#3

BT ~18%

OthersOthers

OthersCompetitor

#2

#3

BT ~ 22%

Others

Global Rolling Stock market1 Europe1 North America 1,2 Asia-Pacific excl. China1

1. Based on BT management's tracking of published Rolling Stock orders in 2010-14 outside China; excluding

Services, Systems and Signalling, and Diesel Locomotives outside Europe

2. North America comprises United States, Canada and Mexico

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Today fleet decisions (should) follow a clear process,

market requirement and business case

Today’s World

CAPEX & CVA – clear value added

Concise risk assessments

Linkage to company value proposition

Low seatmile cost with high performance / comfort / ecology / …

Sustainable

Market driven and flexible

…but what experience is the passenger after (business, holiday, shopping,..)

1950ies: Pilots

1960/70ies:

Engineers

1980ies: Commercial

(Marketing)

today: Economic-

ecologic awareness

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Squaring the circle from the airline ops view

Plus

Determine a low complexity fleet,

market driven multiple aircraft

sizes offering high flexibility in

operation and performance while

being state of the (technical) art

and sustainable highly economical

with the least possible

environmental impact.

Conflicting Interests

Homogeneous fleet vs Operational flexibility

Economies of Scale vs Product differentiation

Fleet commonality vs Risk mitigation/-spread

Innovative aircraft vs Low capital expenditure

Fast airport turnaround vs economies of scale

Source: EBS, WHU lecturing material and Lufthansa Fleetmanagement

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

ba

rdie

r In

c. o

r its s

ub

sid

iarie

s. A

ll rig

hts

re

se

rved

.

Definition of game changing• Technology

• Business environment

• Lead times and planning “security”

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

ba

rdie

r In

c. o

r its s

ub

sid

iarie

s. A

ll rig

hts

re

se

rved

.

Globale Anforderungen bei der Flugzeugentwicklung

8 4000 metres offering the world……with the right tools

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

General Overview

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

10

Some historic background

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Aircraft 1948: 2290 1998: >15500 2010: > 20000

Passengers 1948: 24 million 1998: 1285 million

Passenger journeys 1945: 9 million 1999: 1,5 billion 2010: >2 billion

History of commercial aviation

Speed, range, sizeprovided economic leaps to foster

growth of the industry

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Airliner evolutionary leaps – transportation efficiency gains so

far

1950 1960 1970 1980 1990 2000 2010

10 0000

20 0000

30 0000

40 0000

50 0000

60 0000

Seat kilometres per hour

DC-8-63

747-400

A380-800

DC-10-30/L1011-200

MD-11747-200 Combi

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

t

Ope

ratin

g C

ost

B727

DC-9

B737-300

MD-80

A320Fam

B737NG

All innovations and experience

from airline/MRO operations

transferred into new aircraft

1980 20001990 20XX1970

New technologies have delivered more efficient aircraft from platform to platform

??

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Group Fleet Strategy and Aircraft Evaluation - Reasoning

Plan Buy Fly Sell

Neutral, „marketing-free“ Aircraft Evaluation

• Coordinated input of LH-group requirements in new aircraft programs / designs

• Influence and judge manufacturers‘ product strategies through constant dialogue

• Independent aircraft evaluation (economical and operational)

• perform a standardized, consistent cost and performance benchmark of competing

existing and projected aircraft

• Negotiation of performance guarantees in purchasing campaigns and tracking of

compliance

• Interface to external R&D establishments

• Issue fleet development recommendations to the LH-group members

Fleet Mgmt

Sources: Lufthansa Fleet Management 2013 & European Business School

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Technology Trends…

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

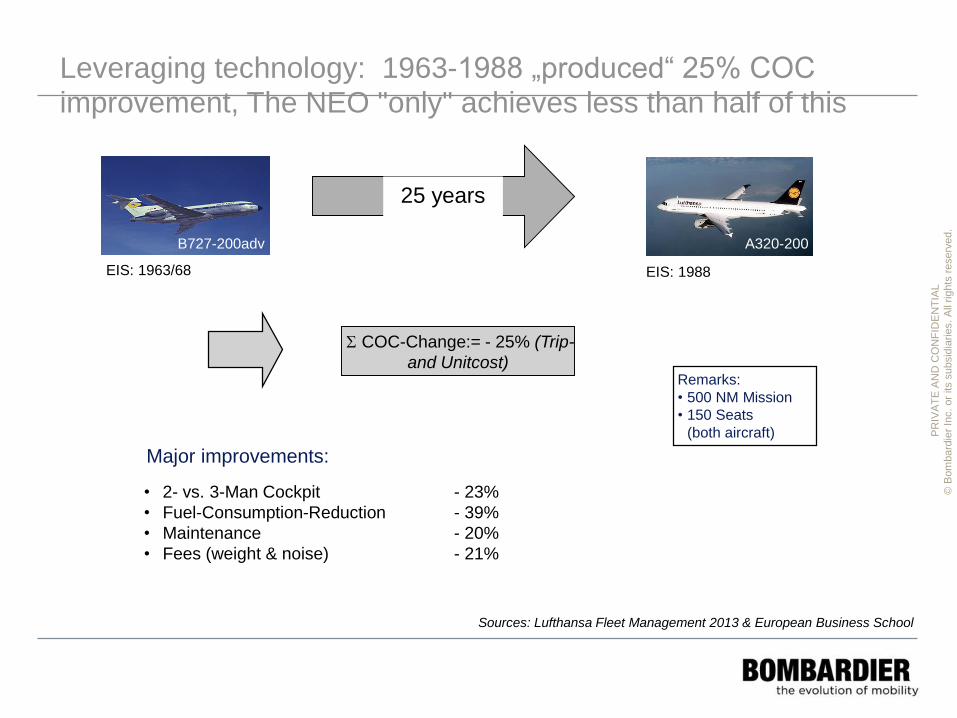

25 years

Remarks:

• 500 NM Mission

• 150 Seats

(both aircraft)

EIS: 1963/68

B727-200adv A320-200

EIS: 1988

S COC-Change:= - 25% (Trip-

and Unitcost)

• 2- vs. 3-Man Cockpit - 23%

• Fuel-Consumption-Reduction - 39%

• Maintenance - 20%

• Fees (weight & noise) - 21%

Major improvements:

Leveraging technology: 1963-1988 „produced“ 25% COC

improvement, The NEO "only" achieves less than half of this

Sources: Lufthansa Fleet Management 2013 & European Business School

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

ba

rdie

r In

c. o

r its s

ub

sid

iarie

s. A

ll rig

hts

re

se

rved

.

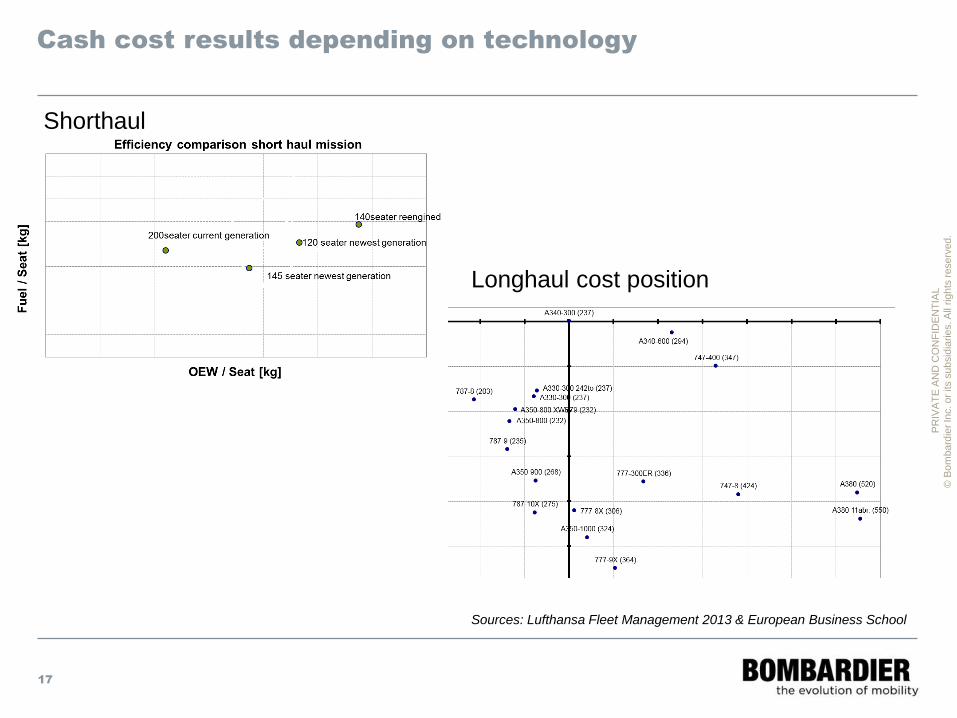

Cash cost results depending on technology

17

Sources: Lufthansa Fleet Management 2013 & European Business School

Shorthaul

Longhaul cost position

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Economies of scale and customer needs – the reality!

RELATIVE COST POSITIONS

THEN AND TOMORROW

ALL DATA IS THERE SINCE LONG

…..EVALUATE OR CONCLUDE

The challenge of changing algorythms…..

0

50

100

150

Range

noise

seatmilecost

profitper

flight

tripcost

500 seater 300 seaterTrip cost = risk

Seatm

ilecost

= r

ew

ard

better

bette

r

future

Aircraft size increasing

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Co

st/

SK

O

Size

Co

st/

SK

O

Size

Size200 300 400 500 Size250

300

400

500

PA

X a

nd

bre

ak

eve

n

PA

X a

nd

bre

ak

eve

n

danger of uncontrolled yield errosion; market

growth necessary to achieve "unit cost"

with introduction of "new A/C technologies" no

inherent growth necessary to retain unit cost

level

traditional Situation starting 2018

Due to different product life cycles there will be an era without

economies of scale starting in the second half of this decade

Sources: Lufthansa Fleet Management 2013 & European Business School

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Capital Cost

Cash-cost dominate on long haul aircraft

Cash Operating Cost (COC)

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

To manage cost is to understand the levers that

impact each cost element; Cash cost determine the

quality of the asset

Fuel

Total Maintenance Cost

Landing Fees

Handling Fees

Navigation Fees

Cockpit Crews

Cabin Crews

typ

ica

l ca

sh o

pe

ratin

g c

ost

(CO

C)

of

long

hau

l a

ircra

ft

Cost elements have to be measured for their

competitive sustainability100%

Source: Corporate Fleet Strategy and Aircraft Evaluation

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

The payload-range of an aircraft to assess

the most efficient production tool

OEW

Range =

OEWcost

+ PayloadRevenue & cost

= MZFW + Fuelcost

= MTOW

given variable

Useable Payload is determined by Aircraft Weight and Design

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

What is really driving Airlines? Influencing and Stakeholders

Fleet is just a tool…Age should not be a reason, money is

MarketNetwork

Economy ,Competiton

Passengers

consumer patterns

Population growth

ManufacturersTechnology

Aircraft

EnvironmentNoise

Emissions

ETS

ResearchFuture Technologies

Innovative Solutions

Mobility patterns

InfrastructureCongestion

AirlineBusiness Model

Fleet Strategy

Cost Structure

Risk

RegulationsOpen-Skies

Traffic Rights

• More electric / solar

• Hi Integrated Systems & Big Data

• Weight (20%) and reliability

• Aero configuaration close to 10%

(shape and morphing wing)

• Speed, range

• Additive manufacturing

• Engines

• ….

• « reinvent » flying

• Passenger centric

• ….

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

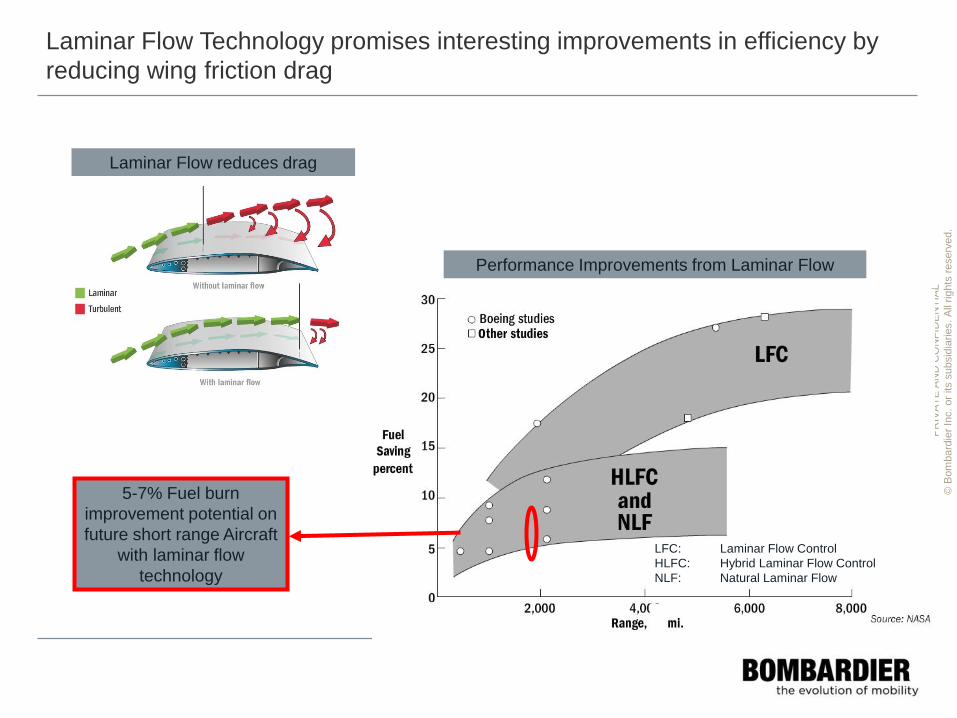

LFC: Laminar Flow Control

HLFC: Hybrid Laminar Flow Control

NLF: Natural Laminar Flow

Performance Improvements from Laminar Flow

Laminar Flow reduces drag

Laminar Flow Technology promises interesting improvements in efficiency by

reducing wing friction drag

5-7% Fuel burn

improvement potential on

future short range Aircraft

with laminar flow

technology

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

25

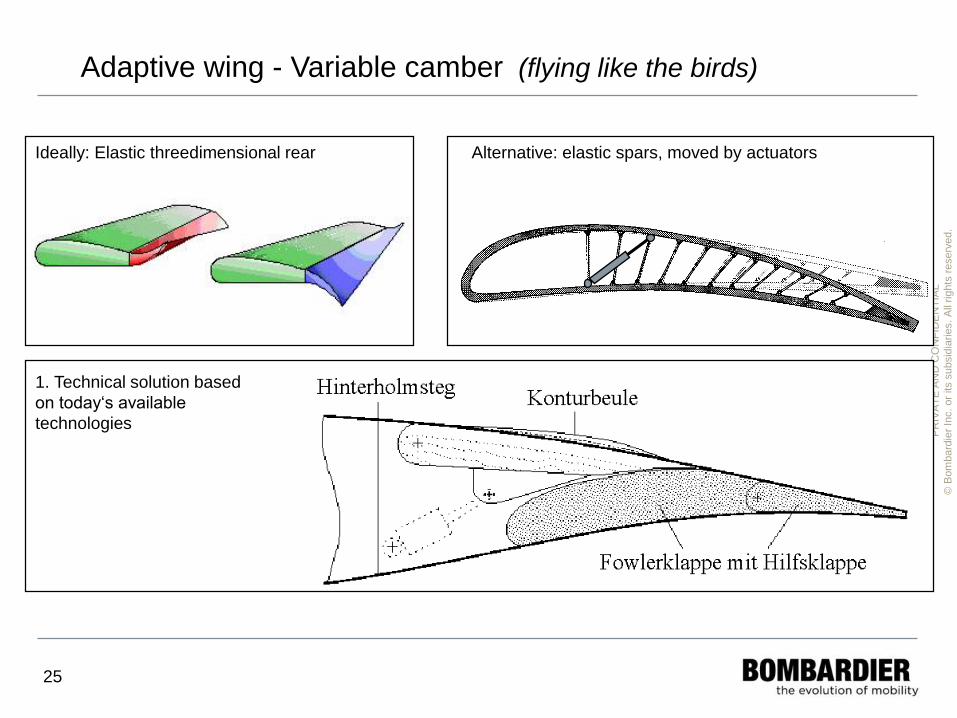

Adaptive wing - Variable camber (flying like the birds)

Alternative: elastic spars, moved by actuatorsIdeally: Elastic threedimensional rear

1. Technical solution based

on today‘s available

technologies

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

XC-120 Pack Plane

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

„Oblique Flying Wing“

Source: unknown

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

28

Blended Wing Concept

Source: Aerospace Testing October 2007

July 2007

test flight

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

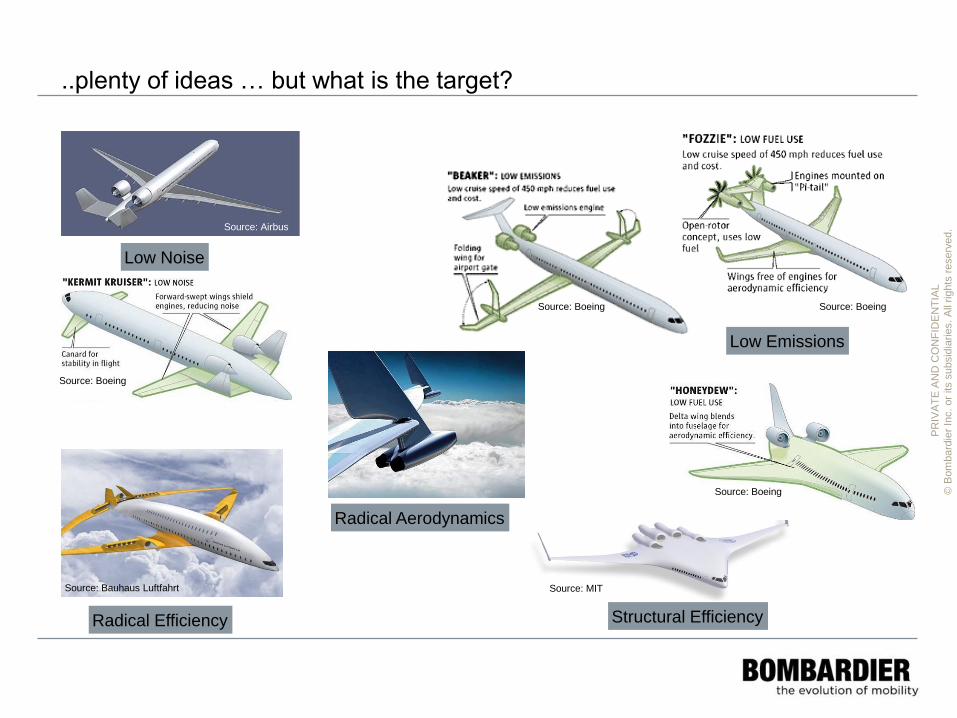

..plenty of ideas … but what is the target?

Source: Bauhaus Luftfahrt

Radical Efficiency

Radical Aerodynamics

Low Noise

Source: Airbus

Source: Boeing

Structural Efficiency

Source: MIT

Low Emissions

Source: Boeing Source: Boeing

Source: Boeing

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

The Future…Engine Design has tradeoffs

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

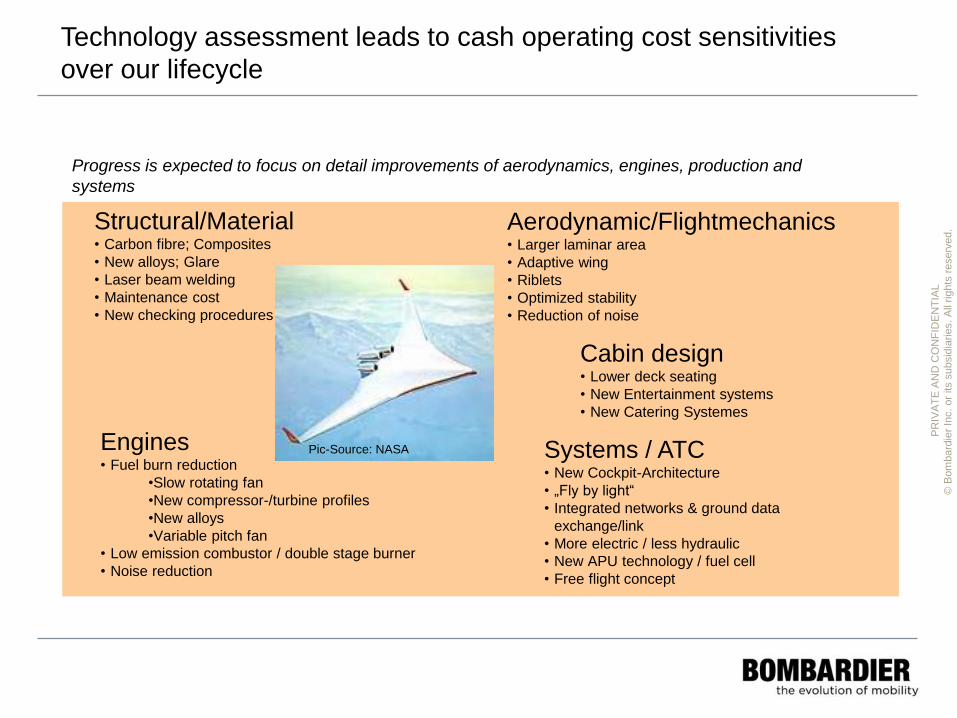

ed.Structural/Material

• Carbon fibre; Composites

• New alloys; Glare

• Laser beam welding

• Maintenance cost

• New checking procedures

Engines• Fuel burn reduction

•Slow rotating fan

•New compressor-/turbine profiles

•New alloys

•Variable pitch fan

• Low emission combustor / double stage burner

• Noise reduction

Aerodynamic/Flightmechanics• Larger laminar area

• Adaptive wing

• Riblets

• Optimized stability

• Reduction of noise

Systems / ATC• New Cockpit-Architecture

• „Fly by light“

• Integrated networks & ground data

exchange/link

• More electric / less hydraulic

• New APU technology / fuel cell

• Free flight concept

Cabin design• Lower deck seating

• New Entertainment systems

• New Catering Systemes

Technology assessment leads to cash operating cost sensitivities

over our lifecycle

Pic-Source: NASA

Progress is expected to focus on detail improvements of aerodynamics, engines, production and

systems

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

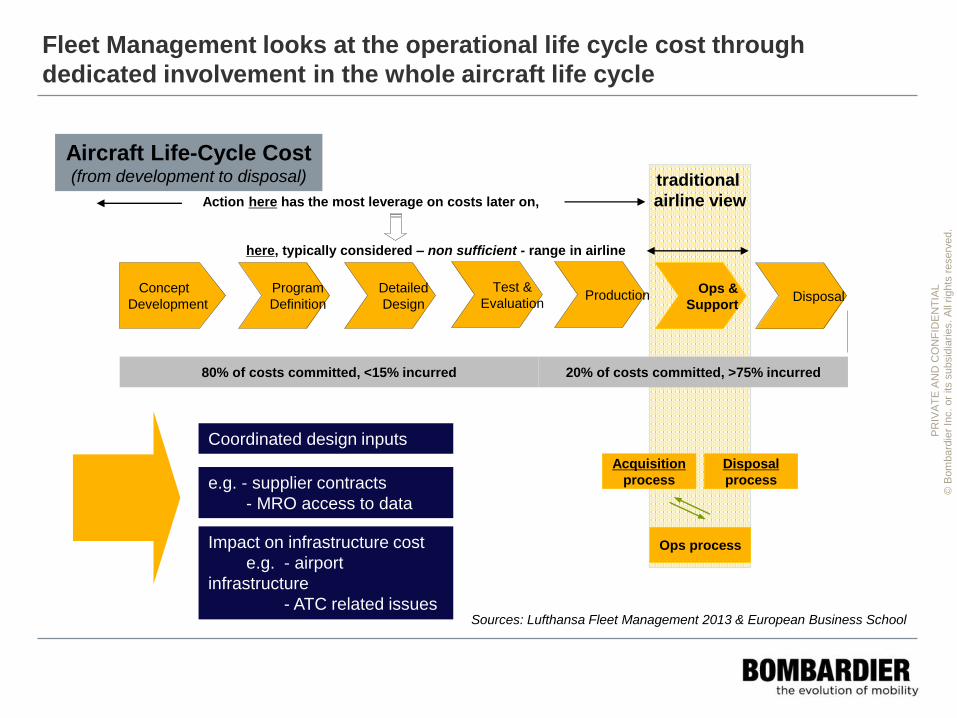

Concept

Development

Detailed

Design

Program

Definition

Test &

EvaluationProduction

Ops &

SupportDisposal

80% of costs committed, <15% incurred

Acquisition

process

Ops process

Disposal

process

Fleet Management looks at the operational life cycle cost through

dedicated involvement in the whole aircraft life cycle

20% of costs committed, >75% incurred

traditional

airline view

Aircraft Life-Cycle Cost(from development to disposal)

e.g. - supplier contracts

- MRO access to data

Impact on infrastructure cost

e.g. - airport

infrastructure

- ATC related issues

Coordinated design inputs

Action here has the most leverage on costs later on,

here, typically considered – non sufficient - range in airline

Sources: Lufthansa Fleet Management 2013 & European Business School

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Some evaluation points…………

Performance Data

Range, Speed, Take-off and Landing

Capabilities

Cash Operating Cost

Fuel, Fees, Maintenance, Emission Cost

Technology and flexibility

Environmental issues

Noise-, CO2´- and pollution emission

Cabin Product

Cabin comfort, seat width

Fleet Strategy

Industry Politics

Risk assessment

Assessment of competitors

Infrastructure issues

Sources: Lufthansa Fleet Management 2013 & European Business School

Size / payload

Range

Speed

Belly-Volume

T/O performance

Noise and emissions

Passenger comfort

Infrastructure at airports

$ Purchase price

$ Value keeping, residual value

$ Empty weight

$ Crewing

$ Fuel burn

$ Maintenance cost

$ Fleet commonality

$ Product support available

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Revenue

Data and IT Tools

Maximize Yield and Load

Factor for increased profitability

Design of

pricing

products

Setting of

price levels

and conditions

Steering

availability of

booking classes

Initiation of

capacities

adjustments

Framework Airline Business

The airline product is perishable.

An empty seat is worthless after

the plane is airborne.

We are active on the global

market. Others worldwide are

competing for the same customers

(valid for airlines and OEMs)

A booking does not guarantee a

sold seat yet.

Demand varies significantly by

time of day and season.

PricingYield

Management

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

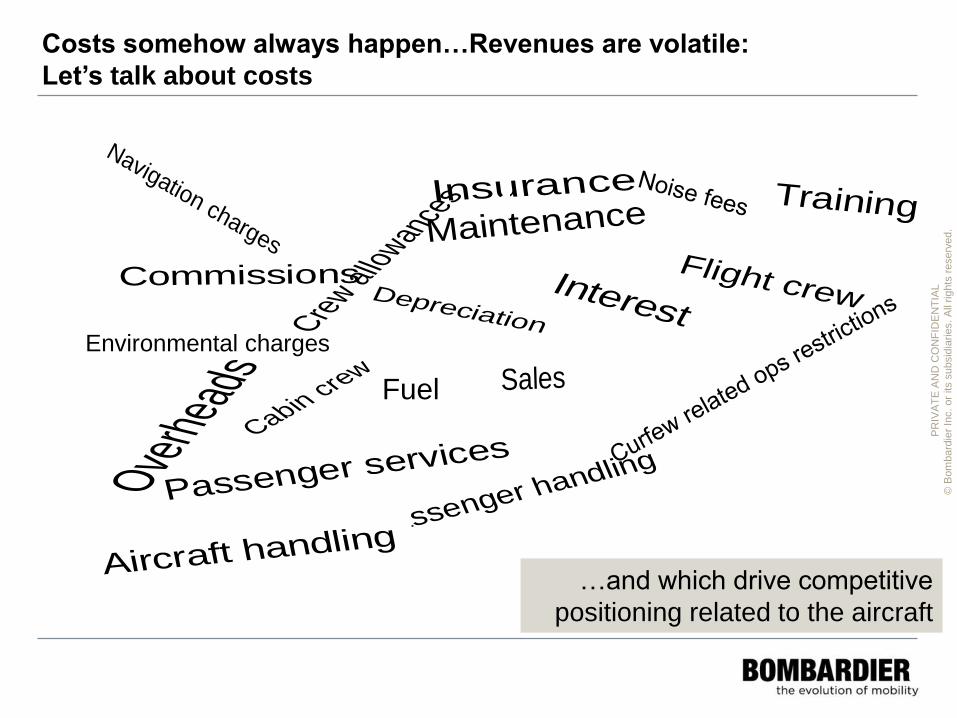

Overhe

ads Sales

Flight crew

Fuel

Maintenance

Cabin crew

Training

Passenger handling

Aircraft handling

Navigation charges

Commissions

Passenger services

Depreciation

Interest

Insurance

Crew al

lowan

ces

Costs somehow always happen…Revenues are volatile:

Let’s talk about costs

Environmental charges

…and which drive competitive

positioning related to the aircraft

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

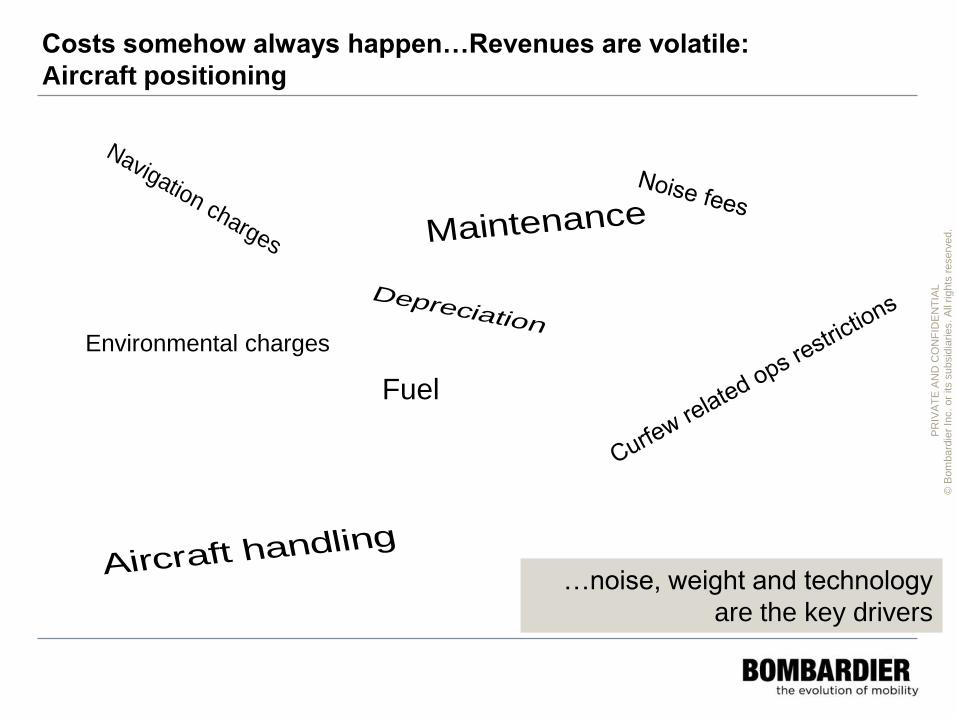

Fuel

Maintenance

Aircraft handling

Navigation charges

Depreciation

Costs somehow always happen…Revenues are volatile:

Aircraft positioning

Environmental charges

…noise, weight and technology

are the key drivers

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

nswers

uestionsQ

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Danke

PR

IVA

TE

AN

D C

ON

FID

EN

TIA

L

© B

om

bard

ier

Inc. or

its s

ubsid

iarie

s. A

ll rig

hts

reserv

ed.

Caution Regarding Forward-Looking Statements

This presentation includes forward-looking statements, which may involve, but are not limited to: statements with respect to the Corporation’s objectives, guidance, targets, goals, priorities,

market and strategies, financial position, beliefs, prospects, plans, expectations, anticipations, estimates and intentions; general economic and business outlook, prospects and trends of an

industry; expected growth in demand for products and services; product development, including projected design, characteristics, capacity or performance; expected or scheduled entry-into-

service of products and services, orders, deliveries, testing, lead times, certifications and project execution in general; competitive position; the expected impact of the legislative and

regulatory environment and legal proceedings on the Corporation’s business and operations; available liquidities and ongoing review of strategic and financial alternatives; the receipt and

use of the remaining investment by the Government of Québec in the C Series Aircraft Limited Partnership (the C Series Investment); the effects of the C Series Investment and of the

private placement of a minority stake in Transportation to the CDPQ (the CDPQ Investment and, with the C Series Investment, the Investments) on the range of options available to us,

including regarding the Corporation’s participation in future industry consolidation; the capital and governance structure of the Transportation segment following the CDPQ Investment, and of

the Commercial Aircraft segment following the C Series Investment; the impact and expected benefits of the Investments on the Corporation’s operations, infrastructure, opportunities,

financial condition, access to capital and overall strategy; and the impact of the sale of equity on the Corporation’s balance sheet and liquidity position. The implementation of the Share

Consolidation is subject to a number of conditions, including but not limited to, Toronto Stock Exchange approval. The Board of Directors has authority, notwithstanding approval of the

Share Consolidation by shareholders, to determine in its discretion not to proceed with the Share Consolidation, without further approval or action by, or prior notice to, shareholders. At this

time, no decision has been made by the Board of Directors and there can be no assurance that the Share Consolidation will be implemented as proposed or at all, or as to the timing thereof,

or that the Share Consolidation will result in the contemplated initial post-consolidation share price of Class A Shares or Class B Subordinate Voting Shares.

Forward-looking statements can generally be identified by the use of forward-looking terminology such as “may”, “will”, “expect”, “intend”, “anticipate”, “plan”, “foresee”, “believe”, “continue”,

“maintain” or “align”, the negative of these terms, variations of them or similar terminology. By their nature, forward-looking statements require management to make assumptions and are

subject to important known and unknown risks and uncertainties, which may cause actual results in future periods to differ materially from forecast results. While management considers their

assumptions to be reasonable and appropriate based on information currently available, there is risk that they may not be accurate.

Certain factors that could cause actual results to differ materially from those anticipated in the forward-looking statements include, but are not limited to, risks associated with general

economic conditions, risks associated with the Corporation’s business environment (such as risks associated with the financial condition of the airline industry, of business aircraft customers,

and of the rail industry; trade policy; increased competition; political instability and force majeure), operational risks (such as risks related to developing new products and services;

development of new business; the certification and homologation of products and services; fixed-price commitments and production and project execution; pressures on cash flows based on

project-cycle fluctuations and seasonality; the Corporation’s ability to successfully implement the Corporation’s strategy and transformation plan; doing business with partners; product

performance warranty and casualty claim losses; regulatory and legal proceedings; the environment; dependence on certain customers and suppliers; human resources; reliance on

information systems; reliance on and protection of intellectual property rights; and adequacy of insurance coverage), financing risks (such as risks related to liquidity and access to capital

markets; retirement benefit plan risk; exposure to credit risk; existing debt and interest payment requirements; certain restrictive debt covenants; financing support provided for the benefit of

certain customers; and reliance on government support), market risks (such as risks related to foreign currency fluctuations; changing interest rates; decreases in residual values; increases

in commodity prices; and inflation rate fluctuations). For more details, see the Risks and uncertainties section in Other in the Management’s Discussion and Analysis (MD&A) of the

Corporation’s financial report for the fiscal year ended December 31, 2015. For additional information with respect to the assumptions underlying the forward-looking statements made in this

presentation, refer to the Guidance and forward-looking statements sections in the MD&A of the Corporation’s financial report for the fiscal year ended December 31, 2015.

Readers are cautioned that the foregoing list of factors that may affect future growth, results and performance is not exhaustive and undue reliance should not be placed on forward-looking

statements. The forward-looking statements set forth herein reflect management’s expectations as at the date of this presentation and are subject to change after such date. Unless

otherwise required by applicable securities laws, the Corporation expressly disclaims any intention, and assumes no obligation to update or revise any forward-looking statements, whether

as a result of new information, future events or otherwise. The forward-looking statements contained in this presentation are expressly qualified by this cautionary statement.

All amounts in this presentation are expressed in U.S. dollars unless otherwise indicated.

Bombardier Inc. and its subsidiaries’ names, abbreviations thereof, logos, and product and service designators are all either the registered or unregistered trademarks or trade names of

Bombardier Inc. and its subsidiaries. Names, abbreviations of names, logos, and product and service designators of other companies are either the registered or unregistered trademarks or

trade names of their respective owners. Use of names, abbreviations of names, logos, and product and service designators of other companies does not imply any endorsement by any other

such company.