We investigate the effect of better access to ... - CORE Argentinean –rms, Bustos ... production...

46

econstor www.econstor.eu Der Open-Access-Publikationsserver der ZBW – Leibniz-Informationszentrum Wirtschaft The Open Access Publication Server of the ZBW – Leibniz Information Centre for Economics Standard-Nutzungsbedingungen: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Zwecken und zum Privatgebrauch gespeichert und kopiert werden. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich machen, vertreiben oder anderweitig nutzen. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, gelten abweichend von diesen Nutzungsbedingungen die in der dort genannten Lizenz gewährten Nutzungsrechte. Terms of use: Documents in EconStor may be saved and copied for your personal and scholarly purposes. You are not to copy documents for public or commercial purposes, to exhibit the documents publicly, to make them publicly available on the internet, or to distribute or otherwise use the documents in public. If the documents have been made available under an Open Content Licence (especially Creative Commons Licences), you may exercise further usage rights as specified in the indicated licence. zbw Leibniz-Informationszentrum Wirtschaft Leibniz Information Centre for Economics Flach, Lisandra; Irlacher, Michael Working Paper Product versus Process: Innovation Strategies of Multi-Product Firms CESifo Working Paper, No. 5405 Provided in Cooperation with: Ifo Institute – Leibniz Institute for Economic Research at the University of Munich Suggested Citation: Flach, Lisandra; Irlacher, Michael (2015) : Product versus Process: Innovation Strategies of Multi-Product Firms, CESifo Working Paper, No. 5405 This Version is available at: http://hdl.handle.net/10419/113735

Transcript of We investigate the effect of better access to ... - CORE Argentinean –rms, Bustos ... production...

econstor www.econstor.eu

Der Open-Access-Publikationsserver der ZBW – Leibniz-Informationszentrum WirtschaftThe Open Access Publication Server of the ZBW – Leibniz Information Centre for Economics

Standard-Nutzungsbedingungen:

Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichenZwecken und zum Privatgebrauch gespeichert und kopiert werden.

Sie dürfen die Dokumente nicht für öffentliche oder kommerzielleZwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglichmachen, vertreiben oder anderweitig nutzen.

Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen(insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten,gelten abweichend von diesen Nutzungsbedingungen die in der dortgenannten Lizenz gewährten Nutzungsrechte.

Terms of use:

Documents in EconStor may be saved and copied for yourpersonal and scholarly purposes.

You are not to copy documents for public or commercialpurposes, to exhibit the documents publicly, to make thempublicly available on the internet, or to distribute or otherwiseuse the documents in public.

If the documents have been made available under an OpenContent Licence (especially Creative Commons Licences), youmay exercise further usage rights as specified in the indicatedlicence.

zbw Leibniz-Informationszentrum WirtschaftLeibniz Information Centre for Economics

Flach, Lisandra; Irlacher, Michael

Working Paper

Product versus Process: Innovation Strategies ofMulti-Product Firms

CESifo Working Paper, No. 5405

Provided in Cooperation with:Ifo Institute – Leibniz Institute for Economic Research at the University ofMunich

Suggested Citation: Flach, Lisandra; Irlacher, Michael (2015) : Product versus Process:Innovation Strategies of Multi-Product Firms, CESifo Working Paper, No. 5405

This Version is available at:http://hdl.handle.net/10419/113735

Product versus Process: Innovation Strategies of Multi-Product Firms

Lisandra Flach Michael Irlacher

CESIFO WORKING PAPER NO. 5405 CATEGORY 8: TRADE POLICY

JUNE 2015

An electronic version of the paper may be downloaded • from the SSRN website: www.SSRN.com • from the RePEc website: www.RePEc.org

• from the CESifo website: Twww.CESifo-group.org/wp T

ISSN 2364-1428

CESifo Working Paper No. 5405

Product versus Process: Innovation Strategies of Multi-Product Firms

Abstract We investigate the effect of better access to foreign markets on innovation strategies of multi-product firms in industries with different scope for product differentiation. Industry-specific demand and cost linkages induce a distinction between the returns to innovation. In differentiated industries, cannibalization is lower and firms invest more in product innovation. In homogeneous industries, firms internalize intra-firm spillovers and invest more in process innovation. We test these predictions using Brazilian firm-level data. Following an exchange rate devaluation, firms have better access to foreign markets and exploit economies of scale in innovation. We evaluate the differential effects across industries and show that the type of innovation depends on the degree of product differentiation.

JEL-Code: F120, F140, L250.

Keywords: multi-product firms, innovation, product differentiation, cannibalization effect, spillovers, market size effect.

Lisandra Flach Department of Economics

University of Munich 80539 Munich / Germany

Michael Irlacher Department of Economics

University of Munich 80539 Munich / Germany

June 15, 2015 We are grateful to Daniel Baumgarten, Carsten Eckel, Kalina Manova, Thierry Mayer, Emanuel Ornelas, Jennifer Poole, Jens Suedekum, and participants at the 16th Workshop International Economics in Goettingen 2014, European Economic Association in Toulouse, European Trade Study Group in Munich, FIW Research Conference in Vienna, Midwest International Economics Group in Columbus and IO-Trade Seminar Munich for their helpful comments. Part of this paper was written while one of the coauthors (Lisandra Flach) was visiting the Brazilian Statistical Office (IBGE), whose support and hospitality is gratefully acknowledged. Financial support from SFB TR 15 is gratefully acknowledged. Felix Roellig provided excellent research assistance.

1 Introduction

Successful manufacturing �rms continuously innovate to maintain their position in the mar-

ket and to attend consumers�demand. Recent contributions in the international trade liter-

ature emphasize the importance of intra-�rm adjustments through innovation in explaining

welfare gains from trade liberalization, besides the well-established intra-industry gains from

entry and exit of �rms. This literature highlights innovation as a new dimension into the re-

lationship between exporting and productivity: Better access to foreign markets encourages

�rms to invest in more sophisticated manufacturing technologies, which increases produc-

tivity.1 Consequently, innovation and productivity improvements within the �rm account

for a large fraction of productivity gains at the industry level.2 Moreover, variety-loving

consumers bene�t not only from new products of entering �rms but, �rst and foremost,

from product innovation by incumbent �rms.3 Therefore, understanding innovation strate-

gies and within-�rm adjustments of multi-product �rms (MPFs) is crucial for the analysis

of aggregate productivity and variety gains.

MPFs account for the majority of trade �ows and are omnipresent in all industries.

In terms of innovation activities, their investments account for a large fraction of aggregate

changes in industry-level productivity and product variety (Bernard et al. (2010), Broda and

Weinstein (2010), Lileeva and Tre�er (2010), Bustos (2011)). However, with the exception of

Dhingra (2013) (which is discussed later in detail), innovation in trade models happens only in

one dimension, whereas in reality �rms face a trade-o¤between investments in cost reduction

and product variety. This raises the question of how and why �rms in di¤erent industries

make their choices between di¤erent types of innovation, with di¤erent implications in terms

of welfare gains within industries.

The contribution of the paper is to investigate, theoretically and empirically, the inno-

vation strategies of MPFs, focusing on within-�rm adjustments. An increase in market size

increases the incentives for �rms to invest in innovation. However, demand and cost linkages

induce a trade-o¤ between product and process innovation. Crucially, such linkages are only

1Lileeva and Tre�er (2010) as well as Bustos (2011) show that following a tari¤ cut �rms increase theirinvestments in technology. Lileeva and Tre�er (2010) use tari¤ cuts associated with the US-Canadian freetrade agreement and show that Canadian �rms increased labor productivity and used more sophisticatedmanufacturing technologies. Furthermore, access to larger markets induced �rms to engage more in productinnovation. For Argentinean �rms, Bustos (2011) �nds an increase in innovation expenditures between 0.20and 0.28 log points following the average reduction in Brazil�s tari¤s.

2Doraszelski and Jaumandreu (2013) show for Spanish �rms that investments in R&D are the primarysource of productivity growth. Within sectors, between 65 percent and 90 percent of productivity growtharises through intra-�rm productivity enhancing activities.

3Recent evidence of US bar code data in Broda and Weinstein (2010) highlights the importance of thischannel. They show that at a four-year period, 82 percent of product creation happens within existing �rms.Therefore only 18 percent of total household expenditure is on products of entering �rms.

1

present in an MPF setting. Firms may decide to expand their product range or to lower

production costs, and the net e¤ect in terms of returns to innovation is a priori unclear.

In a simple model of MPFs, we show that returns to product and process innovation are

industry-speci�c and uncover a mechanism related to the degree of product di¤erentiation

that explains this relation. On the one hand, by introducing new products �rms internalize

demand linkages, which may reduce demand for its own varieties. On the other hand, as a

novel feature of our model, by investing in process innovation �rms may internalize intra-

�rm spillover e¤ects between production lines. To understand the role played by the degree

of di¤erentiation in this mechanism, consider two �rms in sectors with di¤erent scope for

product di¤erentiation. A �rm producing multiple products in a homogeneous industry has

rather low returns from investing in new products as doing so may crowd out demand for

its own products. This e¤ect is known as the �cannibalization e¤ect�in the literature. On

the other hand, investments in process-optimizing technologies may generate a larger return,

since the bene�ts from spillover e¤ects across production lines are larger. With more similar

production processes, the knowledge learned in the production process of more homogeneous

products is applicable to a large fraction on the entire product portfolio. For �rms in highly

di¤erentiated industries, the mechanism works exactly the other way round.

Our theoretical model builds on Eckel and Neary (2010) and Eckel et al. (2015). Each �rm

produces a bundle of products which are linked on the cost side by a �exible manufacturing

technology. The latter captures the idea that - besides a core competence - MPFs can expand

their portfolio with varieties that are less e¢ cient in production.4 However, our theory

introduces several novel features. First, we explicitly allow for two types of R&D. Therefore,

we assign �xed costs to additional products to model the decision on optimal scope, which

is closer to the notion of product innovation.5 Second, �rms can invest in product-speci�c

process innovation. Process innovation is costly and re�ects economies of scale, such that

�rms invest more in large-scale varieties, close to their core competence. Third, another novel

feature of our framework is to allow for spillover e¤ects between the production processes

within the �rm. We relate the strength of these cost linkages to the degree of product

di¤erentiation in a sector. This occurs because products that are closer substitutes tend to

have more similar production processes (in comparison to highly di¤erentiated products).

Our framework has important implications for understanding how �rms react to trade

openness and to changes in market size. In particular, the model provides two main testable

predictions. (1) We show that, following an increase in market size, �rms invest more in

4The idea that �rms possess a core competency is also featured in models with MPFs by Qiu and Zhou(2013), Arkolakis et al. (2014), and Mayer et al. (2014).

5In our framework, we always refer to product innovation as an increase in product scope.

2

both product and process innovation. Since process innovation re�ects economies of scale,

access to a larger market promotes technology upgrading. Furthermore, access to larger

markets reduce the perceived costs of product innovation, which encourages MPFs to extend

their product scope. (2) However, in our framework, demand and cost linkages related

to the degree of product di¤erentiation determine returns to innovation. We show that in

highly di¤erentiated industries, the cannibalization e¤ect is lower and, therefore, �rms invest

more in product innovation. In homogeneous industries, �rms internalize higher intra-�rm

spillover e¤ects and invest more in process innovation.

The predictions from the model are tested using detailed �rm-level data, which has two

distinctive features. First, we can exploit detailed information on innovation investments by

�rms, mainly over the years 1998-2000. Second, the event of a major and unexpected ex-

change rate devaluation in January 1999 provides an important source of exogenous variation.

For Brazilian exporters, the currency devaluation made their products more competitive at

home and abroad and, therefore, the shock may be interpreted as an increase in market size.

Moreover, we are interested in how �rms in di¤erent industries reacted to the exchange rate

shock, in order to test prediction (2) from the model. To tackle this issue empirically, we

use information on di¤erent types of innovation combined with the degree of di¤erentiation

of the industry.

Our empirical results reveal that �rms increased their innovation e¤orts in both product

and process innovation following the exchange rate devaluation. However, detailed infor-

mation on the degree of di¤erentiation and on the types of innovation conducted by �rms

allows us to evaluate di¤erential e¤ects across industries. Using a continuous measure of

the degree of di¤erentiation in an industry, we show that �rms in more di¤erentiated indus-

tries invest more in product innovation, while �rms in more homogeneous industries invest

more in process innovation. Our results are robust to di¤erent measures of the degree of

di¤erentiation, hold for di¤erent estimation strategies (we estimate the incidence of innova-

tion using probit, linear probability model, and seemingly unrelated regression), and remain

stable when adding several control variables.

Our paper is closely related to the literature on MPFs in international trade that features

a cannibalization e¤ect.6 Our theory builds on Eckel et al. (2015), who incorporate an

endogenous investment in product quality in the framework by Eckel and Neary (2010).

We abstract from investments in quality and instead focus on investments in product and

process innovation. The paper that is closest in spirit to ours is Dhingra (2013), who also

6Eckel and Neary (2010) and Dhingra (2013) introduce cannibalization e¤ects. However, this feature isnot considered in many recent models of MPFs that assume monopolistic competition. One exception is themodel proposed by Feenstra and Ma (2008).

3

considers an innovation trade-o¤ of MPFs. Dhingra (2013) proposes a model of MPFs with

intra-brand cannibalization that induces a distinction between the returns to product and

process innovation. Her framework explains how �rms react to trade liberalization in terms

of innovation investments. Following a trade liberalization, �rms face higher competition

from foreign �rms and, therefore, reduce investments in product innovation to mitigate

internal competition (cannibalization e¤ect). On the other hand, �rms increase investments

in process innovation because of economies of scale. In contrast to her theoretical framework,

we build a framework with demand and cost linkages to evaluate heterogeneous responses of

�rms in di¤erent industries. Moreover, using detailed �rm-level data, we test the predictions

from the model. In terms of the way we model innovation, the key di¤erences between our

paper and that of Dhingra (2013) are that we (1) allow for �exible manufacturing and (2)

introduce cost linkages related to the degree of di¤erentiation that generate spillover e¤ects

within the �rm. Therefore, our model is able to generate novel predictions regarding the two

types of innovation depending on the degree of di¤erentiation of the industry.

Our paper is also related to the literature emphasizing the complementary between mar-

ket size and innovation behavior of �rms that leads to gains from trade. Since innovation is

costly, changes in market size tend to encourage �rms to incur these costs because of scale ef-

fects. Models such as Grossman and Helpman (1991) investigate the gains from trade arising

from innovation investments in a setting with homogeneous �rms. At the �rm-level, several

papers have investigated the relation between changes in market size and innovation. Lileeva

and Tre�er (2010) investigate theoretically and empirically how changes in market size en-

couraged �rms to innovate. Using responses of Canadian plants to the elimination of U.S.

tari¤s, they �nd that plants more induced by the tari¤ cuts increase more their investments

in innovation. Yeaple (2005), Verhoogen (2008), and Aw et al. (2011) investigate further

channels that relate market size with �rm-level innovation and within-�rm adjustments.

2 The Model

Our theory draws on a simple model of MPFs that choose their optimal spending on product

and process innovation. Both types of innovation are costly and, therefore, �rms weight the

returns to innovation against the costs. The returns to innovation are in the focus of this

paper and constitute the main testable predictions from the model. First, we show that the

returns to product and process innovation are higher in a larger market. Second, we point out

that �rms in sectors with homogeneous products focus on optimizing production processes

while �rms in more di¤erentiated industries concentrate on innovating new products. These

innovation patterns follow from demand and cost linkages, both related to the degree of

4

product di¤erentiation in a sector. Since these linkages determine the returns to innovation,

we will introduce them at the very outset.

We begin with a detailed analysis of consumer behavior and the underlying preference

structure in section 2.1. In this part, we show how the demand linkages enter our framework

and relate them to the degree of product di¤erentiation in a sector. In section 2.2, we present

the �rm side of the model. We start with the production cost function, which is characterized

by �exible manufacturing. Moreover, �rms can undertake investments in process innovation

to reduce production costs of a product, which may generate spillovers between production

lines. We refer to this feature as a cost linkage and argue that its strength decreases in

the degree of product di¤erentiation. Firms consider both linkages when maximizing their

pro�ts. Finally, section 2.3 derives the equilibrium of the model and establishes the main

testable predictions from the theory.

2.1 Consumer Behavior: Preferences and Demand

Our economy consists of L consumers who maximize their utility over the consumption of

a homogeneous and a di¤erentiated good. To be more speci�c, we assume that consumers

buy a set of goods out of a potential set e of the di¤erentiated product. Our speci�cationof preferences follows Eckel et al. (2015), though we add an additional numeraire good and

assume a quasi-linear utility in the following form:7

U = q0 + u1, (1)

where q0 is the consumption of the homogeneous good. We conduct our analysis in partial

equilibrium where the outside good absorbs any income e¤ects. Utility over the di¤erentiated

variety is de�ned in a standard quadratic function as follows

u1 = aQ�1

2b

�(1� e)

Zi2e q(i)

2di+ eQ2�, (2)

where a and b represent non-negative preference parameters. In this speci�cation, q (i) de-

notes per variety consumption and Q �Ri2e q(i)di stands for total consumption of the

representative consumer. The parameter e plays a very important role in our model and

describes the degree of product di¤erentiation. We assume that e lies strictly between zero

and one and de�ne the parameter as an inverse measure for product di¤erentiation. This

means that lower values of e imply more di¤erentiated and hence less substitutable prod-

7The preferences in Eckel et al. (2015) capture an additional component addressing the utility whichaccrues from consuming goods of higher quality.

5

ucts. Throughout the analysis, we will distinguish industries along the degree of product

di¤erentiation. We simply refer to a homogeneous industry as an industry with a relatively

high value of e. Accordingly, a di¤erentiated industry means an industry with a value of e

close to zero. A detailed discussion of the role of the parameter e in our model will follow

later on in the analysis.

Consumers maximize utility subject to the budget constraint q0 +Ri2e p(i)q(i)di = I.

Hence, individual income I is spent on consumption of the outside good and the potential

basket e of the di¤erentiated good. p (i) is the price of variety i and the numeraire goodis sold at a price p0 = 1. We assume that consumers demand a positive amount of the

outside good q0 > 0 to ensure consumption of the di¤erentiated good. Maximizing utility

and aggregating individual demand functions yields a linear market demand:8

p(i) = a� b0 [(1� e)x(i) + eX] : (3)

We de�ne � e as the subset of varieties which is actually consumed. x (i) describes

the market demand for variety i and consists of the aggregated demand of all consumers

Lq (i) for that speci�c variety. X �Ri2 x(i)di is the total volume of consumption of all

di¤erentiated goods. Furthermore, a describes the demand intercept and b0 � bLde�nes an

inverse measure for the size of the market. Direct demand of variety i is given by

x (i) =a

b0 (1� e+ e�) �1

b0 (1� e)p (i) +e�

b0 (1� e+ e�) (1� e)p; (4)

where � describes the measure of consumed varieties in . The average price of di¤erentiated

varieties in the economy is given by p = 1=�Ri2 p (i) di.

As demand linkages will play a crucial role in our model, we conclude this section by

analyzing how the degree of product di¤erentiation a¤ects the cross elasticity between any

two varieties and the price elasticity of demand. The cross elasticity of variety i with respect

to variety j is given by "i;j � j(@x (i) =@x (j)) (x (j) =x (i))j = ex (j) = (1� e)x (i). It isstraightforward to see that for given output levels, "i;j is higher in more homogeneous sectors.

For a �rm this means: The closer is the substitutability between its varieties, the more does

the output of any additional variety reduce the demand for the other products within its

portfolio (i.e. the stronger are the demand linkages in a sector).

In addition to the cross elasticities, we also compute the price elasticity of demand to

relate e to our empirical measure of di¤erentiation. The empirical part of the paper uses the

Khandelwal (2010) classi�cation as the preferred measure for product di¤erentiation. This

8Given the quasi-linear upper-tier utility, there is no income e¤ect, thereby implying that the marginalutility of income � = 1.

6

measure is created by evaluating changes in prices conditional on market shares: A product is

classi�ed as more di¤erentiated if the �rm can increase prices without losing market shares.

To connect this to our theoretical model, we compute the price elasticity of demand and

show how it responds to a change in the degree of di¤erentiation in a sector. Given the

linear demand system in Eq. (3), there exists an upper bound of the price, where demand

x(i) is just driven to zero:

pmax � (1� e) a+ e�p(1� e+ e�) . (5)

Following Melitz and Ottaviano (2008), we express the price elasticity of demand as

"i �����@x (i)@p (i)

p (i)

x (i)

���� = p (i)

(pmax � p (i)) , (6)

by combining Eqs. (4) and (5). Inspecting the latter expression clari�es the role of the

degree of product di¤erentiation e in determining the demand linkages in our model. It can

easily be shown that, ceteris paribus, the choke price pmax decreases and, therefore, the price

elasticity "i increases when products become more homogeneous.

@pmax

@ejp;�=const= �

� (a� p)(1� e+ e�)2

< 0. (7)

This implies that the parameter e in our theoretical model is closely related to the Khandelwal

(2010) measure of di¤erentiation which we use in the empirical part of our paper.

2.2 Firm Behavior: Optimal Product and Process Innovation

In this section, we consider technology and optimal �rm behavior. We rely on the monopoly

case, for three main reasons. First, we focus on intra-�rm adjustments, and therefore, com-

petition between �rms plays only a second-order role.9 Second, the vast majority of �rm

investments happen within existing �rms (see Bernard et al. (2010) and Broda and We-

instein (2010) for product innovation and Doraszelski and Jaumandreu (2013) for process

innovation), and hence, we abstract from �rm entry. Third, in the empirical part of the

paper, we investigate data on �rm adjustments following an exchange rate devaluation for

incumbent �rms. Moreover, the exchange rate devaluation leads to better access to foreign

markets without increasing competition. Hence, our way of writing the theory is motivated

by deriving predictions that can directly be addressed in the empirical analysis.

We construct a theoretical model in which MPFs optimally choose between two types

9The model could be extended to the oligopoly case. See the Appendix in Eckel et al. (2015).

7

of investment. Firstly, �rms invest in new product lines and thereby extend their product

portfolio. Secondly, �rms may decide for each of their products how much to invest in

the production technology. Both types of investment depend on the degree of product

di¤erentiation through the demand and cost linkages taken into account by a �rm. In the

previous section, we have already introduced the demand linkages into our model. We argue

that the demand linkages in particular determine the returns to product innovation. While

deciding on the optimal number of products, the �rm considers the negative impact of the

marginal good on the demand for the rest of its products. Hence, the more similar are the

products within the portfolio, the stronger will be the cannibalization e¤ect of the marginal

variety. Consequently, we show that the optimal product range will be smaller in a more

homogeneous sector.

As a novel feature of our model, we introduce cost linkages and relate them to the degree

of product di¤erentiation. In particular, the strength of the cost-linkages determines the

returns to process innovation in our model. Firms may decide for each product how much

to invest. However, we argue that there are intra-�rm spillover e¤ects between the varieties.

This means that a �rm can use parts of the process R&D of one product for other products

in its portfolio. To which extent product-speci�c R&D is applicable to other processes

depends on the similarity of production processes and, therefore, on the degree of product

di¤erentiation. Thus, �rms in homogeneous sectors will invest more in process innovation as

they can internalize more spillovers between production lines.

Production Technology Production is characterized by �exible manufacturing. We fol-

low Eckel and Neary (2010) and assume that �rms have a core competence i = 0, which

denotes the product where the �rm is most e¢ cient in production. Besides the core variety,

an MPF can produce additional varieties with rising marginal costs. Production costs for

variety i without investments are given by c (i) = c + c1i. For the sake of simplicity, we

assume a linear cost function, though this is not required to derive our results.

Firms can reduce production costs through variety speci�c process innovation. Further-

more, we allow for investment spillovers between products. To reduce production costs of

variety i, a �rm undertakes process innovation k (i) which reduces production costs at a

diminishing rate. The variety speci�c costs savings from innovation are given by 2k (i)0:5.

As mentioned earlier, part of the process optimization of one variety is applicable to all other

varieties, which implies that production of variety i bene�ts from all investments undertaken

on all the other products K�i �Rni k (i)

0:5 di. The degree to which knowledge is applicable

8

to other products depends on the spillover parameter

� (e) 2 (0; 1) with �0 (e) > 0. (8)

� (e) is a key parameter of our model which captures the idea that more homogenous products

also imply more similar production processes. Therefore, product speci�c investments are

better applicable to the entire product portfolio in a more homogenous sector leading to

higher investment spillovers between similar products. We will de�ne a functional form for

this parameter later on in the analysis.

Considering these aspects, production costs of variety i are given by:

c (i) = c+ c1i��2k (i)0:5 + 2� (e)K�i

�: (9)

This can be rearranged to

c (i) = c+ c1i��2 (1� � (e)) k (i)0:5 + 2� (e)K

�, (10)

where in analogy to X, K =R �0k (i)0:5 di denotes total investment in process innovation.

Pro�t Maximization In our setup, an MPF simultaneously chooses optimal scale x (i)

and process innovation k (i) per product as well as optimal product scope �. Process inno-

vation is carried out at a rate rk and product innovation requires building a new production

line at a rate r�. Total pro�ts are given by:

� =

Z �

0

�p(i)� c� c1i+ 2 (1� � (e)) k (i)0:5 + 2� (e)K

�x(i)di�

Z �

0

rkk (i) di� �r�. (11)

Optimal Scale Maximizing pro�ts in Eq. (11) with respect to scale x (i) implies the

following �rst-order condition:10

@�

@x(i)= p(i)� c� c1i+ 2 (1� � (e)) k (i)0:5 + 2� (e)K � b0 (1� e)x (i)� b0eX = 0. (12)

Using the inverse demand in Eq. (3) and solving for x (i) yields optimal scale of variety i:

x(i) =a� c� c1i+ 2 (1� � (e)) k (i)0:5 + 2� (e)K � 2b0eX

2b0(1� e) . (13)

10The second-order condition is negative: @2�@x(i)2

= �2b0 < 0.

9

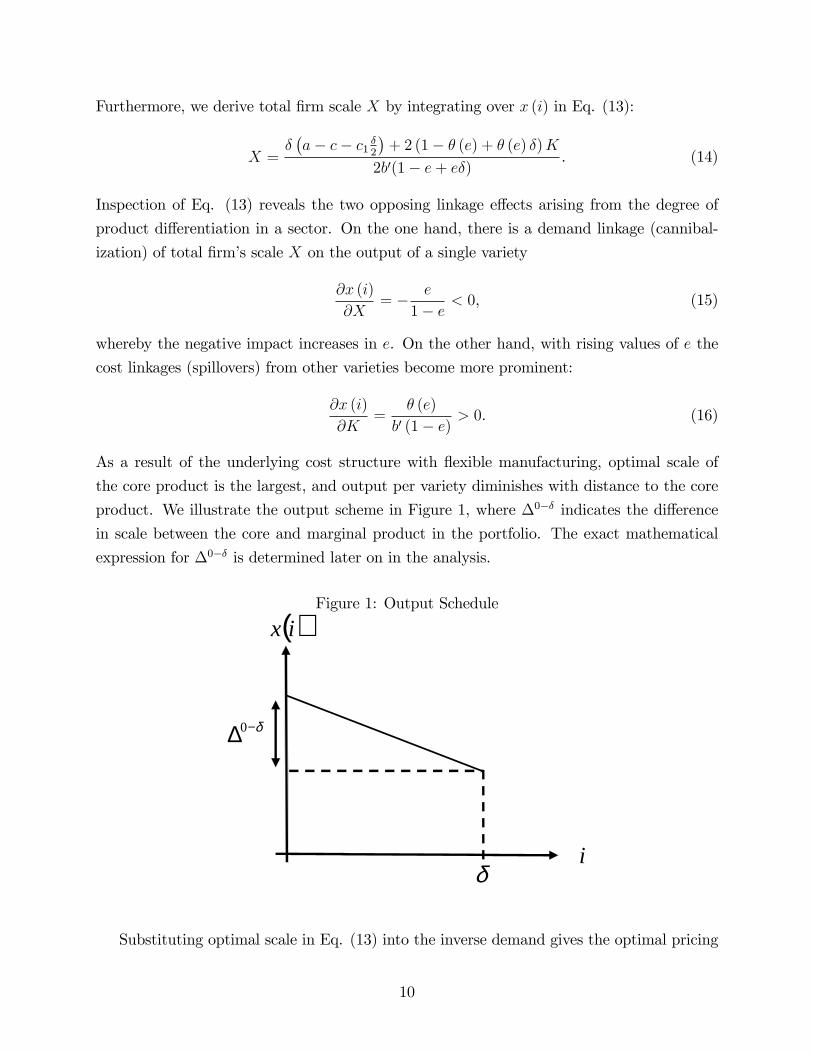

Furthermore, we derive total �rm scale X by integrating over x (i) in Eq. (13):

X =��a� c� c1 �2

�+ 2 (1� � (e) + � (e) �)K

2b0(1� e+ e�) . (14)

Inspection of Eq. (13) reveals the two opposing linkage e¤ects arising from the degree of

product di¤erentiation in a sector. On the one hand, there is a demand linkage (cannibal-

ization) of total �rm�s scale X on the output of a single variety

@x (i)

@X= � e

1� e < 0, (15)

whereby the negative impact increases in e. On the other hand, with rising values of e the

cost linkages (spillovers) from other varieties become more prominent:

@x (i)

@K=

� (e)

b0 (1� e) > 0. (16)

As a result of the underlying cost structure with �exible manufacturing, optimal scale of

the core product is the largest, and output per variety diminishes with distance to the core

product. We illustrate the output scheme in Figure 1, where �0�� indicates the di¤erence

in scale between the core and marginal product in the portfolio. The exact mathematical

expression for �0�� is determined later on in the analysis.

Figure 1: Output Schedule

( )ix

i

δ−∆0

δ

Substituting optimal scale in Eq. (13) into the inverse demand gives the optimal pricing

10

schedule, with the lowest price charged for the core product:

p(i) =1

2

�a+ c+ c1i� 2 (1� � (e)) k (i)0:5 � 2� (e)K

�. (17)

The latter explains why the output of the core competency is sold at the highest scale.

Finally, the price-cost margin for variety i is given by:

p (i)� c (i) = a� c� c1i+ 2 (1� � (e)) k (i)0:5 + 2� (e)K2

. (18)

Optimal Process Innovation Firms can invest in cost-reducing process innovation

for each product in the portfolio. At the optimum, direct savings through lower production

costs plus indirect savings from spillovers on other products are equal to the rate of innovation

costs rk:@�

@k(i)= (1� � (e)) k (i)�0:5 x (i) + � (e) k (i)�0:5X � rk = 0. (19)

Solving for optimal investments in variety i yields:11

k (i) =

�(1� � (e))x (i) + � (e)X

rk

�2. (20)

Eq. (20) shows that optimal investment re�ects economies of scale through both per variety

output x (i) and total �rm outputX. Given that the output of the core variety is the highest,

a �rm will put most e¤ort in optimizing the production process of this variety.12 However,

the �rst-order condition in Eq. (20) implies that the larger the spillovers � (e) on other

products within the �rm, the more equally a �rm spreads investments across products. In

the extreme case of � (e) = 1, investment levels are the same across products.

Lemma 1 Firms concentrate investments in process innovation on their core competencies,since process innovation re�ects economies of scale. However, the investment levels across

varieties become more similar in more homogeneous sectors due to higher spillover e¤ects.

Finally, we substitute Eq. (13) into Eq. (20) and integrate over the expression. This

gives total �rm investment in process innovation

K �Z �

0

k (i)0:5 di =(1� � (e))

��a� �c� c1 �

2

2

�+ 2b0(� (e)� e)�X

2 (b0rk(1� e)� (1� � (e)) (1� � (e) + � (e) �)). (21)

11The second-order condition is given by: @2�@k(i)2 = �0:5

�k (i)

�1:5(1� � (e))x (i) + � (e)X

�< 0, and is

negative as required.12Evidence for economies of scale at the product level can be found in Lileeva and Tre�er (2010).

11

Optimal Product Innovation Choosing optimal product scope means balancing the

bene�ts of the marginal variety against the innovation costs. The �rst-order condition for

scope is given by:

@�

@�= [p(�)� c (�)]x(�) +

��b0ex (�) + 2� (e) k (�)0:5

�X � rkk (�)� r� = 0, (22)

where c (�) = c+ c1�� 2 (1� � (e)) k (�)0:5 � 2� (e)K. In our framework with both cost anddemand linkages, the marginal bene�t of a product is determined by the negative externality

on all other products (cannibalization) and the positive externality (spillovers in process

innovation).13

[p(�)� c (�)]x(�)| {z }Revenue

+f(�b0ex (�))| {z }Cannibalization

+�2� (e) k (�)0:5

�| {z }Spillover

gX =r� + rkk (�)| {z }Inn. Costs

(23)

In the decision to optimize the product range, an MPF takes into account that an additional

product lowers the prices consumers are willing to pay for all other products. This aspect

is captured by the term "Cannibalization" in Eq. (23). The term "Spillover" in Eq. (23)

re�ects the fact that there are spillovers from the marginal product on all other varieties.

Hence, at this point it seems plausible to make a restriction on the parameter values which

determines the net e¤ect of the two linkages.

Condition 1 In Eq. (23), the net impact of the marginal variety on all other varieties isdetermined by the strength of the two linkages in our model. It is plausible to assume that

the net impact of the marginal product on all varieties is negative. Therefore, we restrict the

parameters as follows:

b0rk >2� (e) ((1� � (e))x (�) + � (e)X)

ex (�). (24)

This condition implies that the perceived cost of process innovation may not be too low.

We refer to b0rk as the perceived costs of process innovation, as this term relates the market

size to the innovation costs. Therefore, the perceived costs can fall (1) if rk decreases or

(2) if the market size L increases (recall that: b0 � bL). We argue that this restriction of

parameters ensures realistic properties within our framework. If process innovation would

be too "cheap", �rms would increase product scope only to bene�t from spillovers from the

investment in the marginal variety. The latter does not seem to be a realistic optimal �rm

behavior.

13The second-order condition is given by: @2�@�2

=h�c1 � 2

�b0ex (�)� 2� (e) k (�)0:5

�ix(�) < 0. To see

that this condition is negative as required, consider Condition 1.

12

In the following, we express a �rm�s optimal scope in terms of scale of the marginal

product x (�). To do so, we substitute the output of the marginal variety from Eq. (13) and

its respective price-cost margin from Eq. (18) into the �rst-order condition for scope (22):

x (�) =

srkk (�) + r� � 2� (e) k (�)0:5X

b0 (1� e) . (25)

Considering again Figure 1, the latter expression can be interpreted as follows: The lower is

the output of the marginal variety �, the larger is the product range o¤ered by the �rm.

To provide some further insights into our model, we combine the �rst-order conditions

for scale and scope in Eqs. (13) and (25), to derive an alternative expression for optimal

scale:

x (i) =c1 (� � i) + 2 (1� � (e))

�k (i)0:5 � k (�)0:5

�2b0(1� e) +

srkk (�) + r� � 2� (e) k (�)0:5X

b0 (1� e) . (26)

It is straightforward to see that this expression boils down to Eq. (25) by setting i = � for

the marginal variety. Furthermore, we can use this expression to calculate the di¤erence in

scale of the core (i = 0) versus the marginal variety �, illustrated in Figure 1:

�0�� =c1�

2�b0(1� e)� (1��(e))2

rk

� . (27)

Since the underlying technology is �exible manufacturing, the di¤erence in output increases

in the product range �. The larger is the distance to the core product, the lower will be

the e¢ ciency of the marginal product. The latter e¤ect is magni�ed for higher values of

c1, as this variable determines how much marginal costs increase with rising distance to the

core product. Moreover, �0�� decreases in the strength of the spillovers � (e). As stated in

Lemma 1, �rms concentrate their investment in process R&D on the core varieties. However,

if spillover e¤ects are large, the marginal varieties bene�t more from the investments in the

high-scale core varieties.

Lemma 2 The di¤erence in scale between the core and the marginal variety is determinedby the di¤erence in production costs of the two varieties. The productivity of the marginal

product falls with distance to the core product and rises in the degree of spillovers.

13

2.3 Comparative Statics

In the previous section, we established the baseline theoretical framework. In the next step,

we derive the main predictions that we test in the empirical section. To start with, we analyze

the e¤ects of an increase in the market size L (lower values of b0) on optimal investment levels.

Furthermore, we investigate optimal investment strategies in sectors with di¤erent degrees

of product di¤erentiation. To derive our results, we follow the solution path in Eckel and

Neary (2010), and express the equilibrium equations in terms of X and � only. Moreover, as

already mentioned, we de�ne a functional form for the spillover parameter � (e):

� (e) = e�. (28)

Figure 2 illustrates this functional form and the role of � in determining the strength of

spillovers. Since e 2 [0; 1]; lower values of � translate into a stronger spillover e¤ect. In the

Figure 2: Spillover Parameter

( )eθ

1

0 e1

1=κ1>κ

1<κ

extreme case of � = 0, the total investment in one variety is applicable on all varieties within

the �rm. Obviously, we derive the same result in an industry with no product di¤erentiation

(i.e. e = 1). Letting � grow large decreases the importance of spillovers within the �rm.

Equilibrium In this section, we derive the equilibrium equations of the model applying

the functional form of spillovers in Eq. (28). Combining Eqs. (14) and (21), we derive total

14

�rm scale as:

X =��a� c� c1 �2

�2�b0(1� e+ e�)� (1�e�+e��)2

rk

� . (29)

The term (1�e�+e��)2rk

re�ects cost-savings from process innovation, which induces a �rm to

increase total �rm scale X. Clearly, the strength of the latter e¤ect is mitigated by the

costs for process innovation rk. Plugging Eq. (29) back into Eq. (21) yields total process

innovation as:

K =(1� e� + e��)

rkX. (30)

The parameter � determines the strength of spillovers, where total process innovation is the

largest for � = 0. Inspecting Eqs. (29) and (30) in detail reveals that investments in process

innovation decrease with rising levels of �, i.e. @K@�< 0. Furthermore, process innovation K

re�ects economies of scale as it depends on total �rm scale X. Using information from Eqs.

(20), (29), and (30) together with Eq. (13), we can express optimal scale per variety as:

x (i) =a� c� c1i� 2

�b0e� e�(2(1�e�)+e��)

rk

�X

2�b0(1� e)� (1�e�)2

rk

� . (31)

Within our framework, we have two opposing e¤ects of total scale X on per variety output.

On the one hand, rising total output induces the �rm to invest more in process innovation,

which increases per variety output. On the other hand, rising total scale intensi�es cannibal-

ization within the portfolio. The latter e¤ect reduces per variety output. However, Condition

1 stated in Eq. (24) guarantees that the spillover e¤ect cannot dominate the cannibalization

e¤ect, i.e. @x(i)@X

< 0.

Finally, substituting from Eq. (20) into Eq. (25), we express the �rst-order condition for

scope as:

x (�) =

vuuut r� � (e�X)2

rk�b0 (1� e)� (1�e�)2

rk

� . (32)

The formal derivation of this expression is presented in the Appendix. Eq. (32) implicitly

de�nes product scope � in terms of the output of the marginal variety. Solving for � gives

the explicit expression for product scope:

� =

a� c� 2r�

b0 (1� e)� (1�e�)2rk

��r� � e2�X2

rk

�� 2

�b0e� 2e�(1�e�)

rk

�X�

c1 � 2e2�Xrk

� . (33)

15

Eqs. (32) and (33) reveal that higher costs for product innovation r� decrease the optimal

product range. The latter implies a higher output of the marginal variety � (see Eq. (32)).

Referring to Figure 1, this characterizes a variety closer to the �rm�s core competence.

Inspecting the term 2p� in Eq. (33) reveals the multiplicative structure of the inverse

measure for market size (b0 � bL) and the cost for product innovation r�. This structure

translates an increase in the market size L into lower perceived costs of product innovation

for the �rm.

Inspecting the previous equations indicates that the equilibrium in our model can be

characterized in terms of two endogenous variables: � and X. In Figure 3, Eq. (29) is

labeled by "Scale: X (�)" and describes a positive relationship between total �rm output X

and scope �. Through adding additional products, an MPF can increase its total output.

Eq. (33) establishes a negative relationship between X and �. The downward-sloping curve

"Scope: � (X)" illustrates that rising �rm output intensi�es the cannibalization e¤ect of

the marginal variety. Therefore, an MPF reduces its product scope when its total output

increases. In the intersection of both curves in Figure 3, the two equilibrium conditions for

Figure 3: Equilibrium

δ

X( )Xδ:Scope

( )δX:Scale

scale and scope are satis�ed.14 Once we have determined the equilibrium values of � and X,

we compute the equilibrium value of process innovation K. In the next step, we derive the

main testable predictions from the model.

14A proof that the two curves intersect is provided in the Appendix. We show that the determinant of thecoe¢ cient matrix is always positive. This ensures that the equilibrium is unique and stable.

16

The E¤ects of a Larger Market Size We are interested in the e¤ects of globalization

on product and process innovation. We follow Krugman (1979) and interpret globalization

as an increase in the number of consumers L. As we analyze the behavior of a single MPF,

we neglect the competition e¤ect of globalization. This modeling choice is motivated by

the nature of our empirical analysis, where we investigate the e¤ect of a devaluation of

the Brazilian real. For Brazilian exporters, a devaluation means improved access to foreign

markets since products become cheaper. Therefore, Brazilian �rms can gain foreign market

shares without losing domestic market shares.

An increase in the market size L reduces the slope b0 of the demand function in Eq. (3).

In the Appendix, we derive the total derivatives of the equilibrium conditions in terms of

scale X (Eq. (29)) and scope � (Eq. (33)), which lead to the following results.

We show that increases in the market size lead to higher total �rm output X. Three

di¤erent intra-�rm adjustments lead to this result. The �rst adjustment comes from the

increased demand in the larger market. The second and third adjustments come from the

impact of product and process innovation on total �rm scale X. We show that despite

cannibalization is intensi�ed through the larger X, a �rm will invest in new products in a

larger market. In Figure 3, both curves "Scale: X (�)" and "Scope: � (X)" are shifted to the

right, though "Scope: � (X)" shifts more. The cannibalization e¤ect of increasing �rm scale

X on scope � can be visualized by comparing the product range before and after the shift of

"Scale: X (�)". Technically the increase in product scope is caused by the fact that in Eq.

(33) the costs for product innovation r� enter multiplied by the parameter b0. As explained

earlier in the text, a larger market size reduces the perceived innovation costs for the �rm.

Finally, we analyze the impact of the market size on process innovation K. As discussed

earlier, process innovation is subject to economies of scale as in a larger market innovation

costs can be spread over more units. From inspection of Eq. (30), we see that the rise in �

and X causes more spending in process innovation. Captured by the term (1�e�+e��)2rk

in Eq.

(29), the process innovation e¤ect contributes to the rise in �rm scale X. We summarize

the market size e¤ect on optimal �rm behavior in the following proposition and test these

results in the empirical part of the paper.

Proposition 1 A larger market size L increases total scale X and induces �rms to invest

more in both product � and process innovation K, i.e.

d lnX

d lnL> 0,

d ln �

d lnL> 0, and

d lnK

d lnL> 0. (34)

The mathematical derivation of these results is presented in the Appendix. Furthermore,

we show the e¤ects of a change in the demand intercept a on the optimal behavior of the

17

�rm. The latter comparative static yields qualitatively the same results.

Sectors with Di¤erent Scope for Product Di¤erentiation We derive a second testable

prediction of our model with respect to the degree of product di¤erentiation in a sector. A

simple comparison between brick production and the automotive sector makes it clear that

there is a lot more scope for di¤erentiation in the latter sector. We argue that the degree of

di¤erentiation is crucial in explaining the innovation behavior of �rms. Recall, that degree

of di¤erentiation determines the strength of the two linkages within our framework. A low

degree of di¤erentiation (high e) causes high cannibalization and high spillover e¤ects and,

therefore, promotes process innovation. One can think again of our example of an MPF pro-

ducing bricks that are slightly di¤erentiated. It is plausible to assume that a large fraction of

the investment in the production line of one speci�c brick is applicable to the production of

all other bricks produced by the same �rm. However, introducing one further brick will have

a strong cannibalizing impact on the initial portfolio. Di¤erentiating Eq. (30) with respect

to the degree of product di¤erentiation e keeping �rm size �xed con�rms our intuition:

@ lnK

@ ln e=

�e� (� � 1)(1� e� + e��) > 0. (35)

Let us now assume the other extreme case of a highly di¤erentiated industry, in our

example the automotive sector. Assuming that cars are more di¤erentiated than bricks,

optimizing the production process for one speci�c car will have positive but lower spillovers

on the other cars in comparison to the case of (more homogeneous) bricks. The more

di¤erentiated two cars are, the lower will be the number of identical parts used in production

and, therefore, the lower will be the spillovers in production. However, for a �rm producing

multiple cars, the negative externality of adding an additional car declines the higher is the

degree of di¤erentiation (i.e. the lower is the cannibalization e¤ect). Again, we hold �rm

size �xed and di¤erentiate Eq. (33) with respect to the degree of product di¤erentiation

e. There are two opposing channels at work when considering the e¤ect of the degree of

product di¤erentiation on the product range �. On the one hand, the marginal product

cannibalizes, on the other hand, all initial products bene�t from process-spillovers from

the marginal product. Di¤erentiating Eq. (33) with respect to e leads to a cumbersome

expression, which is presented in the Appendix. Here we show the solution for the case of

the strongest spillover e¤ects. The following derivative reveals that even in this case the

cannibalization e¤ect dominates, which con�rms our intuition.

lim�!0

@ ln �

@ ln e= �b

0e (2X � x (�))�c1 � 2X

rk

��

< 0 (36)

18

The derivation of this expression and further discussion are presented in the Appendix.

We summarize the e¤ect of the degree of product di¤erentiation on optimal innovation

behavior in the following proposition and test the results in the empirical part of the paper.

Proposition 2 Conditional on �rm size, �rms in sectors with a large (low) scope for prod-

uct di¤erentiation will invest more in product (process) innovation. This behavior is caused

by the lower (stronger) demand- and lower (stronger) cost-linkages in a di¤erentiated (ho-

mogeneous) sector.

3 Data

We test the main predictions of the model using Brazilian �rm-level data. For the main

results, we use data for the period 1998-2000. In robustness checks and a falsi�cation exercise,

we extend the analysis for the years 2000-2005. Firm-level data are matched using the unique

�rm tax number and come from two main sources: (i) SECEX (Foreign Trade Secretariat),

which provides information on the universe of products exported by Brazilian �rms and

(ii) Innovation survey from PINTEC (Brazilian Firm Industrial Innovation Survey). We

combine �rm-level data with industry-level data to investigate how di¤erent industries react

to a trade shock in terms of their investments in innovation.

A distinctive feature of the data is the availability of highly detailed information on �rm-

level innovation investments, including several dimensions of product and process innovation.

A further distinctive feature of the data is the event of a major and largely unexpected ex-

change rate shock in the period under analysis. The devaluation made Brazilian products

more competitive in both domestic and foreign markets and, therefore, increased incentives

for �rms to innovate (due to scale e¤ects). However, �rms react in di¤erent ways to the trade

shock depending on the degree of product di¤erentiation of the industry: While more ho-

mogeneous industries have higher incentives to invest more in process innovation because of

spillover e¤ects, di¤erentiated industries have higher incentives to invest in product innova-

tion because of lower cannibalization across products. To tackle this issue, we use information

on di¤erent types of innovation combined with the degree of product di¤erentiation of the

industry.

19

3.1 Innovation Variables

The innovation survey provides detailed information on innovation investments of 3,070

manufacturing exporters for which we can exploit time-varying information.15 The main

questions used in our study for product and process innovation are: 1. Did the �rm introduce

a new product in the period? (product innovation) and 2. Did the �rm introduce new

production processes in the period? (process innovation). Using this information, we create

the variables Productf = 1 if a �rm f in industry i reported important e¤orts to do product

innovation (zero otherwise), and Processf = 1 if the �rm reported process innovation (zero

otherwise).

Product innovation does not necessarily mean an increase in product scope (suggested by

our theory), since �rms could simultaneously add and drop varieties or change the attributes

of existent varieties. Therefore, in order to get closer to our theoretical mechanism, we use a

further question from the survey related to product scope: 3. Importance of the innovation to

increase product scope, Scopef . This categorical variable (with four degrees of importance)

relates innovation to increases in product scope. We transform this variable in a dummy

Scopef = 1 if the �rm reports that it was important or very important to increase scope

(and zero otherwise).

For process innovation, the variable Processf may also not be directly related to the

mechanism we propose in the theory (that some �rms internalize spillover e¤ects and, there-

fore, invest more in process innovation). Thus, to evaluate the importance of spillover e¤ects,

we use information related to increases in the �exibility of the production process. In par-

ticular, we use the following question from the survey: 4. Importance of the innovation to

increase production �exibility, Flexibilityf . Flexibilityf is a categorical variable (with four

degrees of importance) related to the ability of the �rm to make the production process more

�exible and increase the spillover e¤ects among production lines. Therefore, it is consistent

with the mechanism of the theoretical model, predicting that �rms may internalize intra-�rm

spillover e¤ects. The description of variables is found in Table 14 in the Appendix.

The data has the disadvantage of not capturing di¤erences in the intensity of innovation

across �rms (variables are at most categorical, but not continuous). However, for the pur-

poses of our study, we are able to capture the relevant mechanism, referring to the variation

in innovation e¤orts across industries.

Table 1 presents summary statistics for the baseline indicators of innovation in 2000,

following the exchange rate shock.16 About half of the �rms reported changes in process and

15The PINTEC (2000) survey provides information for a total of 3,700 �rms. However, for 630 of theminformation for many variables of interest is only available for the year 2000.16Values are based on a sample of 3,070 �rms (sample used in the paper).

20

42 percent changes in product.17 The interest of the study is to provide more information

on the innovation choices of �rms in di¤erent industries.

Table 1: Percentage of Firms by Innovation Status in the Year 2000

Product innovation Process innovation Product and process innovation42% 48% 28%

3.2 Degree of Product Di¤erentiation

For the analysis across �rms, we create measures of the degree of product di¤erentiation

across sectors ((1� e)s, for a sector s). For that, we match the �rm-level innovation surveywith information on the degree of product di¤erentiation using (1) the Khandelwal (2010)

classi�cation of product di¤erentiation and (2) the Rauch (1999) classi�cation of goods, as

follows:

Khandelwal (2010) Classi�cation of Product Di¤erentiation Khandelwal (2010)

classi�es sectors and products according to the degree of product di¤erentiation and charac-

terizes products as long and short �quality ladders�. The paper uses nested logit estimations

to infer product quality from price and quantity information of products exported to the

United States: The quality of a product increases if its price can rise without losing market

share. Quality ladders for each product are constructed from estimated qualities, calculated

as the di¤erence between the maximum quality (�MAXp ) and minimum quality (�MIN

p ) within

a product p, as follows: �p = �MAXp � �MIN

p . In this speci�cation, �p denotes the di¤erence

between the minimum and maximum of the estimated quality �pct of country c�s exports to

the United States at time t in product p. The higher �p, the higher the degree of product

di¤erentiation, such that the variation in market shares conditional on product prices is

higher. Therefore, the mechanism proposed by Khandelwal (2010) is closely related to the

mechanism we derive in the theory section (see Eqs. (6) and (7)).

We use the Khandelwal (2010) product classi�cation of the ladder length available at the

4-digit SIC1987 classi�cation. This measure is mapped to the 2-digit IBGE classi�cation

of sectors and industries and generates a ladder length �s, as the average ladder over all

products exported in sector s.

1742 percent of �rms conducted product innovation and 14 percent reported only product innovation (noprocess innovation). 48 percent of �rms conducted process innovation and 20 percent only process innovation.28 percent of the �rms reported both product and process innovation.

21

Rauch (1999) Classi�cation of Goods Rauch (1999) classi�es trade data into three

groups of commodities:w, homogeneous (organized exchange) goods, which are goods tradedin an organized exchange; r, reference priced goods, not traded in an organized exchange, butwhich have some quoted reference price, such as industry publications; and n, di¤erentiatedgoods, without any quoted price. Using this classi�cation at the 4-digit SITC product

classi�cation (issued by the United Nations), we create a measure of the share of products

from a �rm classi�ed as di¤erentiated goods: ShDiffs =Nproductss;n

Nproductss;(w+r+n), where ShDiffs

is the share of products produced by sector s classi�ed as di¤erentiated goods. Also in this

case, we map the Rauch (1999) classi�cation of goods to the 2-digit industry classi�cation

of di¤erentiation from IBGE. Moreover, as an alternative measure, we estimate ShSaless =Salesn

TotalSales(w+r+n), where ShSaless is the share of sales of di¤erentiated products in comparison

to total sales in a sector s.18

We use �s as our benchmark measure, since �s provides higher variation in comparison

to ShDiffs: While �s is created from a continuous variable (product ladder), the Rauch

(1999) classi�cation is created from a binary variable (products classi�ed as di¤erentiated or

non-di¤erentiated goods). Thus, ShDiffs may be inaccurate and subject to measurement

error. We keep the Rauch (1999) classi�cation for robustness checks. Summary statistics for

both measures of di¤erentiation are shown in Table 2.

Table 2: Degree of Product Di¤erentiation by Industry

Measures of (1� e)s Observations Mean Std. Deviation Min Max�s 3,070 1.73 0.21 1.10 2.27ShDiffs 3,070 0.73 0.12 0.33 1

3.3 Industry-speci�c Exchange Rates

In January 1999, the Brazilian government announced the end of the crawling peg, allowing

the real to free �oat, with a consequent depreciation of the real by 25 percent (within a

month). Figure 4 shows the evolution of the exchange rate in this period. While the size of

the devaluation did not vary across di¤erent bilateral currencies, it varied across industries

depending on the degree of openness to trade of the industry. We exploit the variation across

time in exchange rates for industries with di¤erent degrees of exposure to global markets

using trade-weighted industry-speci�c exchange rate shocks. In this way, we can empirically

test the theoretical prediction that �rms innovate more following an increase in market size

18However, we believe that the share of di¤erentiated products measured by the number of products(ShDiffs) is a better measure to infer the degree of di¤erentiation in comparison to the sales of products.Estimations using the share of sales (ShSaless) remain signi�cant (results available upon request).

22

(an increase in L in the model). Crucially, since all �rms in our sample are permanent

exporters, we expect them to react to the shock in a similar way.

Figure 4: Monthly Real Exchange Rates for Brazil, 1996-2001

Industry-speci�c exchange rates are constructed using yearly bilateral trade data from

NBER-UN coded by Feenstra et al. (2005) and bilateral exchange rate data from the Inter-

national Monetary Fund. The underlying idea of the industry-speci�c exchange rate shock

is to study how the movements in di¤erent bilateral exchange rates with respect to the real

a¤ected di¤erent industries, depending on how much they trade with other countries. The

bilateral trade data from NBER-UN provides information on bilateral trade �ows at the

4-digit SITC level. The SITC classi�cation is combined with the Brazilian CNAE industry

classi�cation using publicly available concordance tables up to 4-digit CNAE.19 Following

Goldberg (2004) and Almeida and Poole (2013), we calculate the industry-speci�c exchange

rates as follows:

TRERit =Xc

��0:5

XictPcXict

+ 0:5MictPcMict

�� rerct

�, (37)

where i is industry, c is country, and t is time, such that the bilateral real exchange rate rerct,

measured by the Brazilian currency real with respect to the trading partner c, is weighted

by the industry-speci�c trade shares. The industry-speci�c shares are time-varying import

shares ( MictPcMict

) and export shares ( XictPcXict) by industry and bilateral country pair.

19Concordance tables are publicly available at:http://econweb.ucsd.edu/muendler/html/brazil.html#brazsec.

23

Figure 5 shows the trade-weighted industry-speci�c exchange rates for �rms above and

below the mean of product di¤erentiation (high or low mean �s). Two important facts

must be mentioned. First, Figure 5 illustrates a substantial heterogeneity across industries

in the trade-weighted exchange rates. Second, the �gure shows that in both groups of

�rms/industries the distribution of TRERit is very similar, implying that there is no clear

correlation between the degree of product di¤erentiation and the openness of the industry.

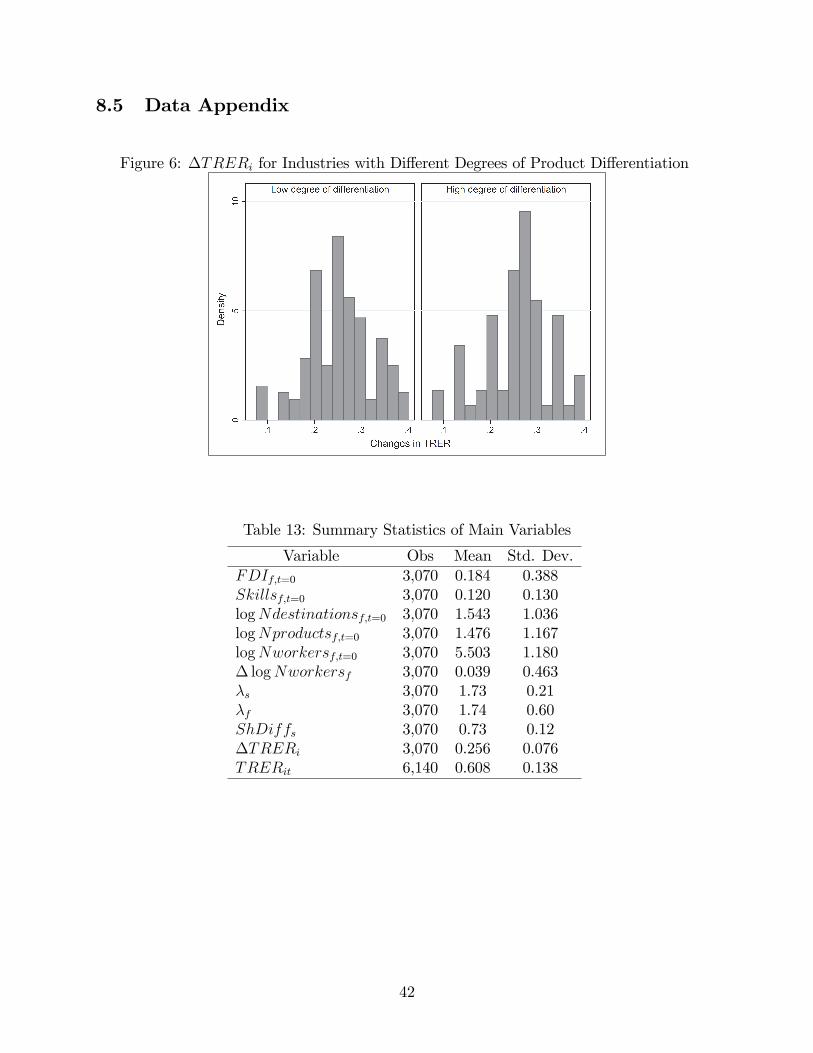

Figure 6 in the Appendix reports changes in trade-weighted exchange rates over time.

The right and left panels reveal that changes in TRERit are similar for both groups of

industries (with high and low degree of di¤erentiation, according to the Khandelwal (2010)

classi�cation).

Figure 5: Industry Variation in Trade-weighted Real Exchange Rates for Firms in Industrieswith High and Low Degrees of Product Di¤erentiation

3.4 Correlation between the Main Variables of Interest

The theoretical model predicts that �rms in more di¤erentiated industries will do more

product and less process innovation in comparison to less di¤erentiated industries. Table 3

shows the correlation between the innovation variables and our main variables for the degree

of di¤erentiation (1� e)s: �s and ShDiffs. We present the correlations in terms of productand process innovation (Productf and Processf ) as well as in terms of our alternative

measures of innovation: While Scopef is related to product innovation (�rms introduce new

varieties and increase product scope), Flexibilityf is related to the ability of the �rm to

24

increase the spillover e¤ects among production lines.

Table 3: Correlation between the Degree of Di¤erentiation and the Outcome Variables

(1� e)s Productf Processf Scopef Flexibilityf�s 0.249*** -0.108** 0.054*** -0.085***ShDiffs 0.048*** -0.029** 0.016** -0.031*Note: *** indicates 1% signi�cance, ** 5% signi�cance, and * 10% signi�cance.

We show that variables related to product innovation (Productf and Scopef) are pos-

itively correlated with the degree of product di¤erentiation. On the other hand, variables

related to process innovation (Processf and Flexibilityf) are negatively correlated with the

degree of product di¤erentiation. Therefore, results in Table 3 are consistent with the pre-

dictions from the theoretical model. Moreover, in the section on robustness checks, we show

that these correlations are not speci�c to the data we use. We combine innovation data for

Brazilian �rms from the World Bank with industry-level data. The correlations between �sand innovation (Productf and Processf) con�rm our results.

4 Empirical Strategy

Our goal in the empirical part of the paper is to test the predictions from the model regard-

ing investment e¤orts of �rms in industries with di¤erent scope for product di¤erentiation,

following a trade shock. We estimate the incidence of changes in innovation investments

�If as a function of the degree of di¤erentiation (1� e)s in the sector s in which the �rmoperates. To investigate the degree of di¤erentiation (1� e)s, we use two di¤erent measures:�s according to Khandelwal (2010) and ShDiffs following Rauch (1999), as described in the

data section. We are interested in the di¤erential e¤ects for industries with di¤erent degrees

of trade openness, measured by changes in time-varying trade-weighted shocks, �TRERi;

using 2-year di¤erences. In the main results, we use the period 1998-2000 (exchange rates

before and after the devaluation in January 1999), and later on we use information for the

period 2000-2005. The empirical speci�cation follows:

Pr(�If = 1) = F (�1�TRERi + �2�TRERi � (1� e)s + �1�Xf + �s + "f ); (38)

where f indexes the �rm, i indexes the industry, s indexes the sector, and �Xf is a vector of

�rm-level time-varying control variables, as described in Table 14 in the Appendix. Initially,

we include only changes in �rm size, then subsequently we add further control variables.

For simplicity, we omit time subscripts for �, which refer to a 2-year lag. "f is an error

25

term. �s are sector �xed e¤ects, such that we can interpret results within industries in a

given sector.20 �If refers to innovation changes conducted by the �rm over the period,

with �If = �Processf or �Productf . In alternative speci�cations, �If = �Scopef or

�Flexibilityf .

In the theoretical model, we state that when market size grows (L increases), the increase

in market size generates incentives for �rms to innovate because of scale e¤ects. Empirically,

we test changes in market size using a major and unexpected exchange rate shock from

1999 as a source of variation (�rms face varying degrees of exposure to foreign markets,

and hence, in the access to foreign markets). We exploit this event using industry-speci�c

exchange rate shocks computed over time, �TRERi. Following the predictions from the

theoretical model, we expect �1 > 0: An exchange rate devaluation increases incentives for

�rms to innovate (because of better access to foreign markets), in particular in industries

more open to international trade.

On top of that, detailed information on the degree of di¤erentiation ((1�e) in the model)and on the type of innovation allows us to evaluate di¤erential e¤ects across industries

and sectors. The di¤erential e¤ects are shown by �2, our main coe¢ cient of interest. �2captures the di¤erential impact of the trade shock on �rms in di¤erentiated sectors relative

to more homogeneous sectors. In response to the shock, scale e¤ects create natural incentives

for �rms to expand innovation investments. In more di¤erentiated sectors, cannibalization

is lower such that �rms invest more in product innovation, while in homogeneous sectors

spillover e¤ects from innovation are higher such that �rms invest more in process innovation.

Therefore, �2 > 0 in case the dependent variable is �Productf , i.e. �rms in sectors with

a high degree of product di¤erentiation invest more in product innovation, and �2 < 0

when the dependent variable is �Processf (�rms in more di¤erentiated sectors invest less

in process innovation in comparison to �rms in more homogeneous sectors).

Concerning the functional form of equation (37), we estimate our empirical model using

probit and linear probability models.21 We also conduct robustness checks using seemingly

unrelated regressions - SUR, to allow the error terms across equations to be correlated

20Note that in the theory we have used the words sector and industry interchangeably. In the empirics itis important that TRERi and (1 � e)s have di¤erent levels of aggregation, such that the interaction termprovides the relevant variation. Therefore, the fact that both variables come from di¤erent classi�cation ofgoods/industries and are aggregated at di¤erent levels is an advantage of our approach. Moreover, there isno clear correlation between (1� e)s and TRERi or between (1� e)s and �TRERi, as we show in Figures5 and 6. If the correlation was high, the interaction term could capture non linearities between innovationand the independent variables. Using the continuous measure of di¤erentiation, �s , we �nd no statisticallysigni�cant correlation between �s and �TRERi:21The linear probability model has the advantage of being easy to estimate and to interpret the coe¢ cients.

However, though unbiased, it poses important disadvantages. To deal with the concerns with the linearestimation, we estimate a probit model.

26

(equations with �Processf or �Productf as dependent variable).

5 Results

Tables 4 and 5 present the main empirical results from our paper. In Table 4, we �rst

investigate whether changes in market size lead to more innovation. As predicted by the

theoretical model, when the market size grows (L increases) incentives to innovate increase

for all �rms and all types of innovation (�1 > 0). Columns (1) to (4) in Table 4 con�rm that

�1 > 0 for product and process innovation, meaning an increase in the predicted probability

of innovation: Following an industry-speci�c exchange rate devaluation (�TRERi > 0), �rms

have higher incentives to invest in product and process innovation. Results are statistically

signi�cant using LPM and Probit, shown in the odds and even columns, respectively. Unless

otherwise stated, results reported for Probit in the tables include the marginal e¤ects, their

standard errors, and the value of the likelihood function. Marginal e¤ects are computed at

means of all variables (means are reported in Tables 2 and 13). At mean values, the average

marginal e¤ect is around 0.273 for product and 0.305 for process innovation, with a p-value

of 0.001 in both cases, meaning that the e¤ect is signi�cant.

Table 4: E¤ect of �TRERi on Innovation

Dependent variable: �Processf �ProductfProbit LPM Probit LPM(1) (2) (3) (4)

�TRERi 0.305*** 0.296*** 0.273*** 0.259***(0.0872) (0.0819) (0.0846) (0.0778)

Constant yes yes yes yes�logNworkersf yes yes yes yesSector s �xed e¤ects yes yes yes yesLog-pseudolikelihood -1895.239 -1776.380Pseudo R-squared 0.010 0.039R-squared 0.104 0.146Observations 3,070 3,070 3,070 3,070

However, the main interest of the paper refers to the di¤erential e¤ects across sectors and

industries. The di¤erential e¤ects using our main measure of di¤erentiation �s are shown

in Table 5. Results con�rm the main predictions from our theoretical model. Following

an exchange rate devaluation (�TRERi > 0), �rms in industries with a high degree of

product di¤erentiation invest more in product innovation relative to other �rms (�2 > 0 when

�If = �Productf), while �rms in industries with a low degree of product di¤erentiation

invest more in process innovation relative to other �rms (�2 < 0 when �If = �Processf).

27

Results hold for both estimation strategies (Probit and LPM).

Table 5: E¤ect of �TRERi on Innovation for Firms in Di¤erent Industries

Dependent variable: �Processf �ProductfProbit LPM Probit LPM(1) (2) (3) (4)

�s ��TRERi -0.125*** -0.124*** 0.107*** 0.106***(0.033) (0.0331) (0.0155) (0.0154)

�TRERi 0.344*** 0.329*** 0.213** 0.199**(0.0882) (0.0810) (0.0837) (0.0773)

Constant yes yes yes yes�logNworkersf yes yes yes yesSector s �xed e¤ects yes yes yes yesLog-pseudolikelihood -1892.544 -1775.112Pseudo R-squared 0.011 0.040R-squared 0.104 0.147Observations 3,070 3,070 3,070 3,070

For probit, we compute the di¤erence in probabilities depending on di¤erent values of

�TRERi and �s, since the value of the interaction e¤ect changes upon the value of the

continuous predictor variable. At mean values of all variables, the marginal e¤ect of�TRERiis 0.213 for product and 0.344 for process innovation, as reported in Table 5. For the

interaction term, the marginal e¤ect is 0.107 for product and -0.125 for process innovation,

evaluated at mean values. Crucially, the interaction e¤ect is statistically signi�cant and

has the expected sign for all observations in the sample, including minimum and maximum

values.22 Thus, our results con�rm that �rms in more homogeneous sectors are signi�cantly

more likely to do process innovation following the shock, whereas �rms in more di¤erentiated

sectors are more likely to do product innovation. Columns (2) and (4) report results for the

LPM. If we evaluate mean values of �TRERi and �s, a decrease in �s by two standard

deviations leads to an increase in the probability to do process innovation by roughly 2

percent, with this value being higher for �rms in sectors with higher initial �s. For product

innovation, an increase in �s by two standard deviations leads to an increase in product

innovation by roughly 4 percent.

One may argue that the measures of product and process innovation used in Table 5

are disconnected from the theoretical model. Changes in process innovation (�Processf)

may re�ect an innovation not directly related to internalization of spillovers. We address this

concern using an alternative measure of innovation related to spillover e¤ects, �Flexibilityf .

22The interaction e¤ect is computed conditional on the independent variables. The analysis of crossderivatives and cross di¤erences shows that the interaction e¤ect varies for di¤erent values of the observations,but has the expected sign: It is positive for product and negative for process innovation.

28

Results presented in Table 6 reveal that estimations are robust to this alternative measure

of process innovation.

A similar concern refers to the mechanism related to product innovation (�Productf).

Investments in product innovation may re�ect changes in an already existent product rather

than the creation of an additional variety. We address this concern using an alternative

measure of innovation related to changes in product scope, �Scopef . Results shown in

Table 6 are consistent with the baseline estimations from Table 5.

Table 6: E¤ect of �TRERi on Product Scope and Production Flexibility