ThyssenKrupp Industrial Solutions · PDF fileTraining & Services (S) ... IFA June 2014, Global...

25

Wir entwickeln die Zukunft für Sie. ThyssenKrupp Industrial Solutions Hans Christoph Atzpodien September 2014

Transcript of ThyssenKrupp Industrial Solutions · PDF fileTraining & Services (S) ... IFA June 2014, Global...

Wir entwickeln die Zukunft für Sie.

ThyssenKrupp Industrial Solutions Hans Christoph Atzpodien September 2014

Developing the future.

Industrial Solutions September 2014

2

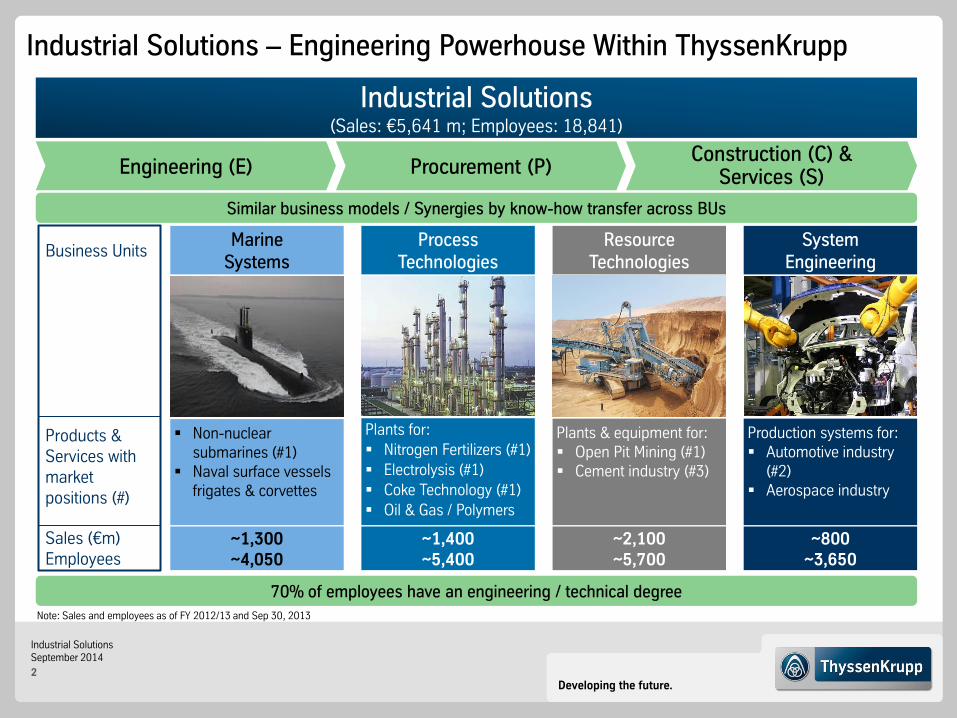

Industrial Solutions – Engineering Powerhouse Within ThyssenKrupp

Industrial Solutions (Sales: €5,641 m; Employees: 18,841)

Construction (C) & Services (S) Procurement (P) Engineering (E)

70% of employees have an engineering / technical degree

Similar business models / Synergies by know-how transfer across BUs

Note: Sales and employees as of FY 2012/13 and Sep 30, 2013

Sales (€m) Employees

Business Units

Products & Services with market positions (#)

Marine Systems

~1,300 ~4,050

Non-nuclear submarines (#1)

Naval surface vessels frigates & corvettes

Process Technologies

~1,400 ~5,400

Plants for:

Nitrogen Fertilizers (#1)

Electrolysis (#1)

Coke Technology (#1)

Oil & Gas / Polymers

Resource Technologies

~2,100 ~5,700

Plants & equipment for: Open Pit Mining (#1) Cement industry (#3)

System Engineering

~800 ~3,650

Production systems for: Automotive industry

(#2) Aerospace industry

Developing the future.

Industrial Solutions September 2014

3

Core Competence in Engineering, Project Execution and Risk Management

Engineering (E)

Construction Management Engineering Power House Service Provider

Know-how transfer based on similar value chain across BUs

Procurement (P) & Integration

Construction (C) Training & Services (S)

Comprehensive Risk Management through Bid and Execution Phase

Close Project

Bid Phase Execution Phase Effective Date of Contract

Provisional Acceptance Certificate

Factory Acceptance Certificate

Contract Signing

Bid / No Bid Decision

Bid Submission

Bid / No-Bid

Reporting

Project Management

Cost-Controlling

Scheduling Bid Preparation

Bid Submission & Negotiation

Aw

ard

of

Ord

er /

Co

ntr

act

Bid Calculation

Developing the future.

Industrial Solutions September 2014

4

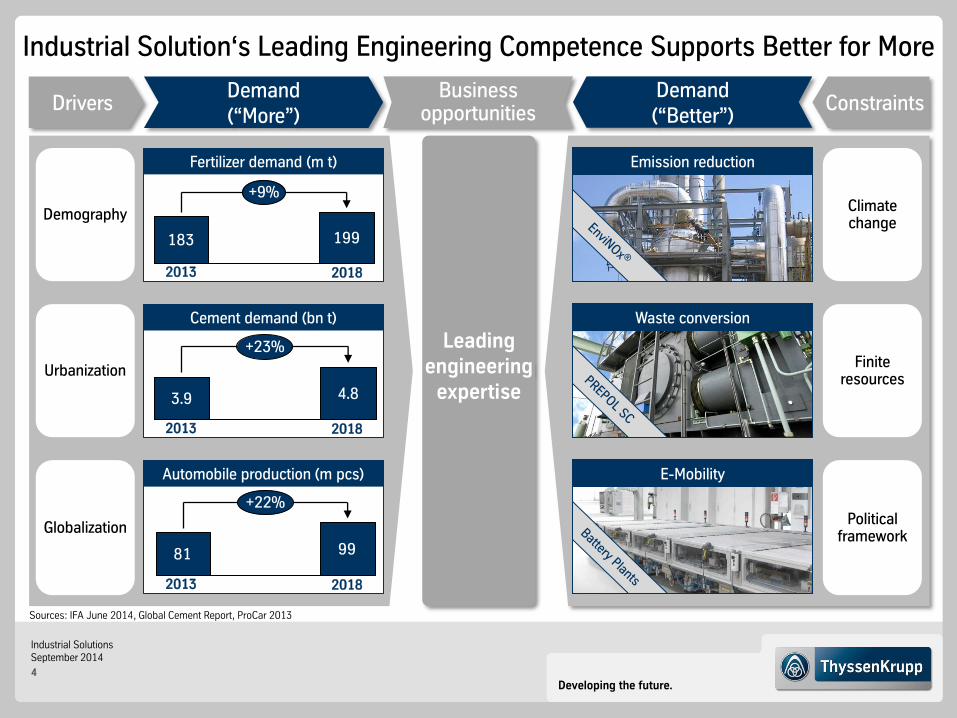

Demography

2013 2018

Urbanization

Cement demand (bn t)

2013 2018

Globalization

2013 2018

Fertilizer demand (m t)

Automobile production (m pcs)

183 199

+9%

4.8 3.9

+23%

81 99

+22%

Industrial Solution‘s Leading Engineering Competence Supports Better for More

Sources: IFA June 2014, Global Cement Report, ProCar 2013

Leading engineering

expertise

Demand (“More”)

Drivers Business

opportunities Constraints Demand (“Better”)

Climate change

Finite resources

Political framework

Emission reduction

Waste conversion

E-Mobility

Developing the future.

Industrial Solutions September 2014

5

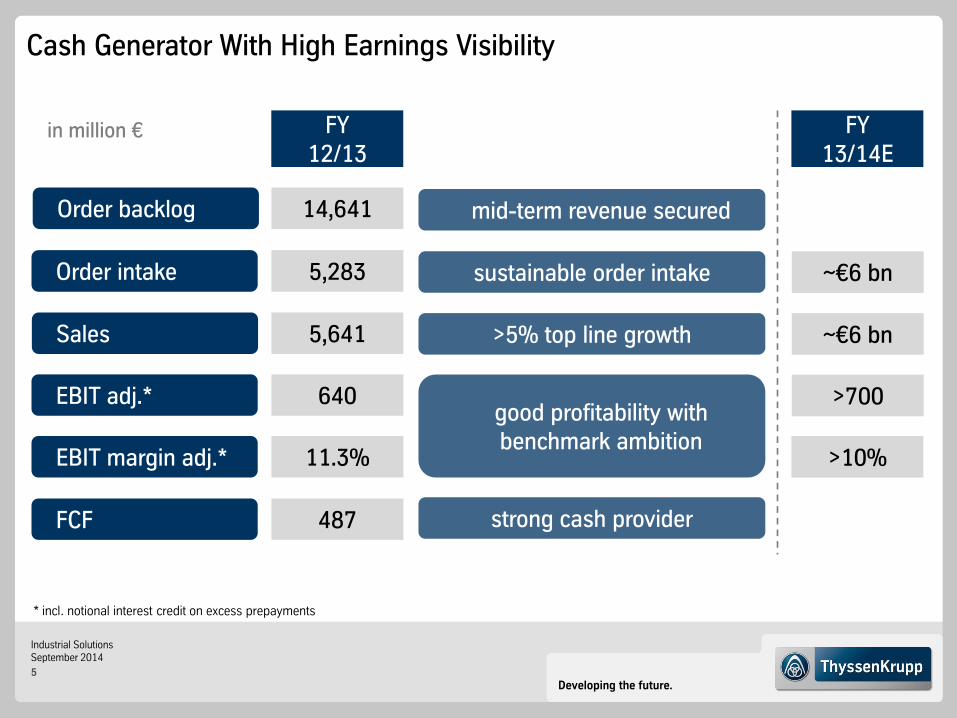

Cash Generator With High Earnings Visibility

FY 12/13

in million €

FCF 487 strong cash provider

FY 13/14E

EBIT margin adj.* 11.3% >10%

Sales 5,641 >5% top line growth ~€6 bn

Order backlog 14,641 mid-term revenue secured

Order intake 5,283 sustainable order intake ~€6 bn

EBIT adj.* 640 good profitability with

benchmark ambition

>700

* incl. notional interest credit on excess prepayments

Developing the future.

Industrial Solutions September 2014

6

Leveraging Growth EPC, Technology & Innovation, Service, M&A

1

Integration & Regionalization Regional Clusters, Joint Customer Marketing

2

People Global Mobility, Recruiting

3

Performance Risk Management, Cultural Change,

4

Enhancing Growth Across All Regions & Becoming a Global Leading Player

€8 bn sales with EBIT margin* on benchmark level

* incl. notional interest credit from excess prepayment

Developing the future.

Industrial Solutions September 2014

7

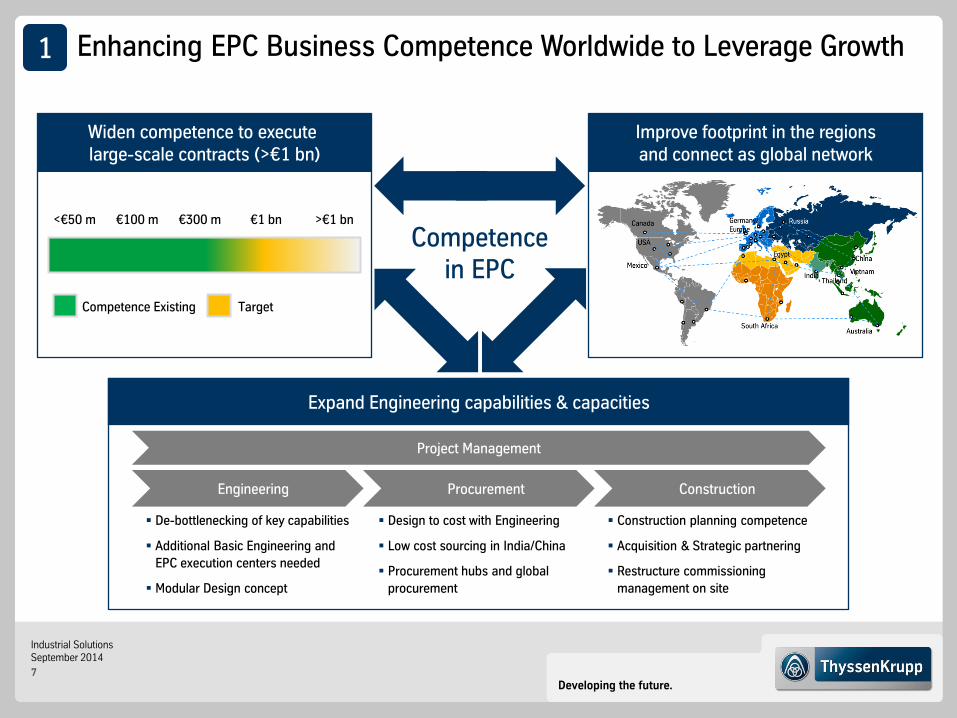

Enhancing EPC Business Competence Worldwide to Leverage Growth

Competence in EPC

Improve footprint in the regions and connect as global network

De-bottlenecking of key capabilities

Additional Basic Engineering and

EPC execution centers needed

Modular Design concept

Design to cost with Engineering

Low cost sourcing in India/China

Procurement hubs and global

procurement

Construction planning competence

Acquisition & Strategic partnering

Restructure commissioning

management on site

Procurement Construction Engineering

Project Management

Expand Engineering capabilities & capacities

Widen competence to execute large-scale contracts (>€1 bn)

Competence Existing Target

<€50 m €300 m >€1 bn €1 bn €100 m

1

Developing the future.

Industrial Solutions September 2014

8

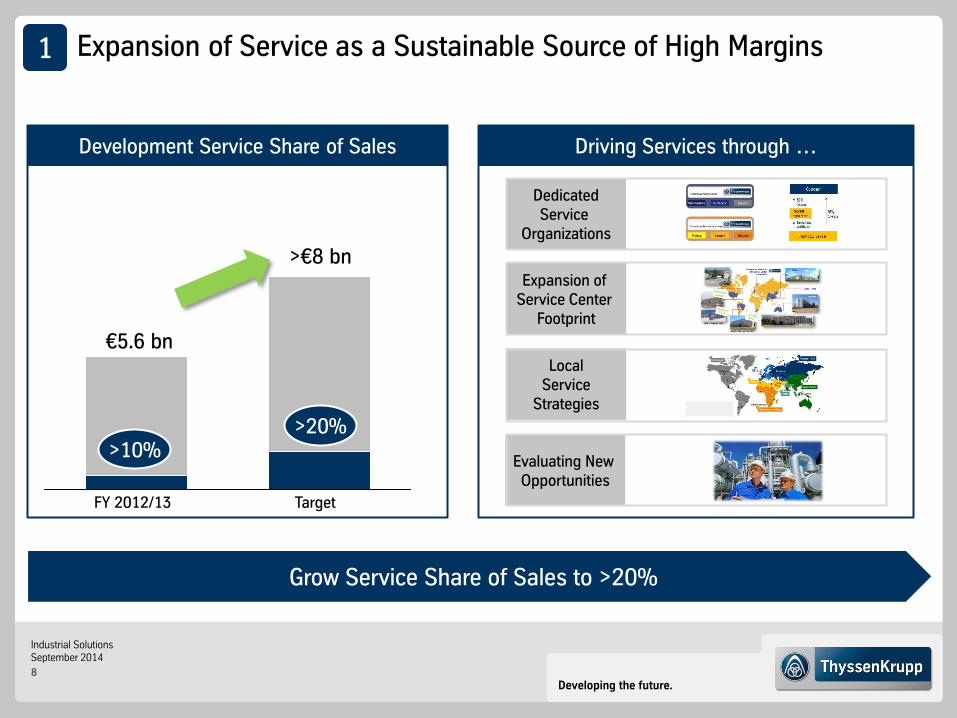

Expansion of Service as a Sustainable Source of High Margins

Development Service Share of Sales Driving Services through …

Expansion of Service Center

Footprint

Local Service

Strategies

Evaluating New Opportunities

Dedicated Service

Organizations

FY 2012/13 Target

Grow Service Share of Sales to >20%

1

€5.6 bn

>10%

>€8 bn

>20%

Developing the future.

Industrial Solutions September 2014

9

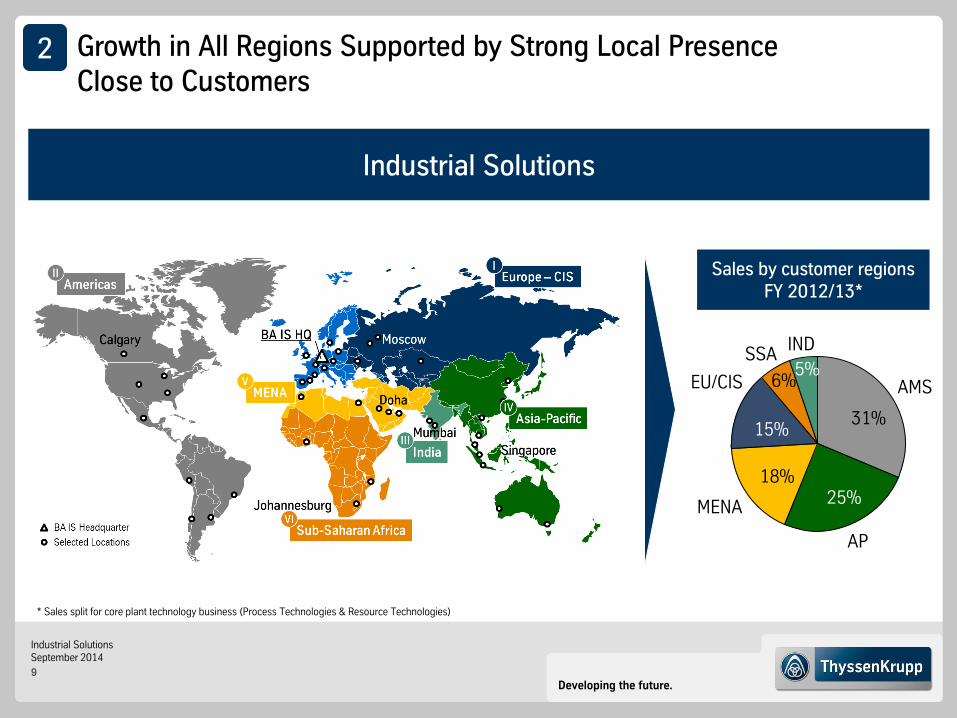

Industrial Solutions

Sales by customer regions FY 2012/13*

AMS

AP

MENA

EU/CIS

SSA IND

* Sales split for core plant technology business (Process Technologies & Resource Technologies)

31%

25% 18%

15%

6% 5%

2 Growth in All Regions Supported by Strong Local Presence Close to Customers

Developing the future.

Industrial Solutions September 2014

10

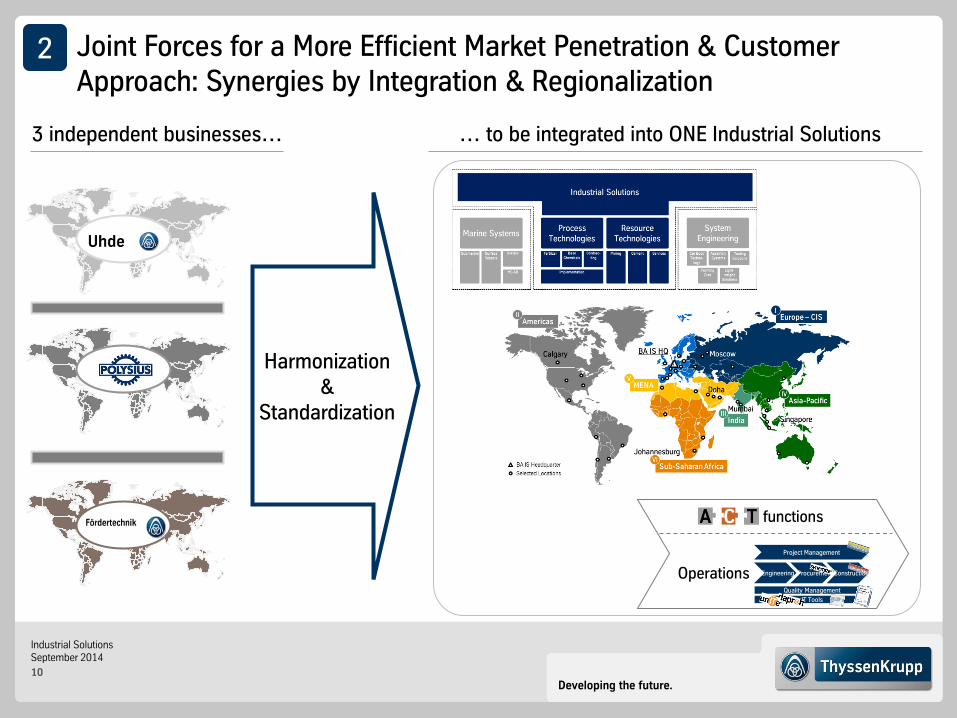

… to be integrated into ONE Industrial Solutions 3 independent businesses…

Harmonization &

Standardization

functions

Operations Procurement Construction Engineering

Project Management

Quality Management

IT Tools

Joint Forces for a More Efficient Market Penetration & Customer Approach: Synergies by Integration & Regionalization

2

Developing the future.

Industrial Solutions September 2014

11

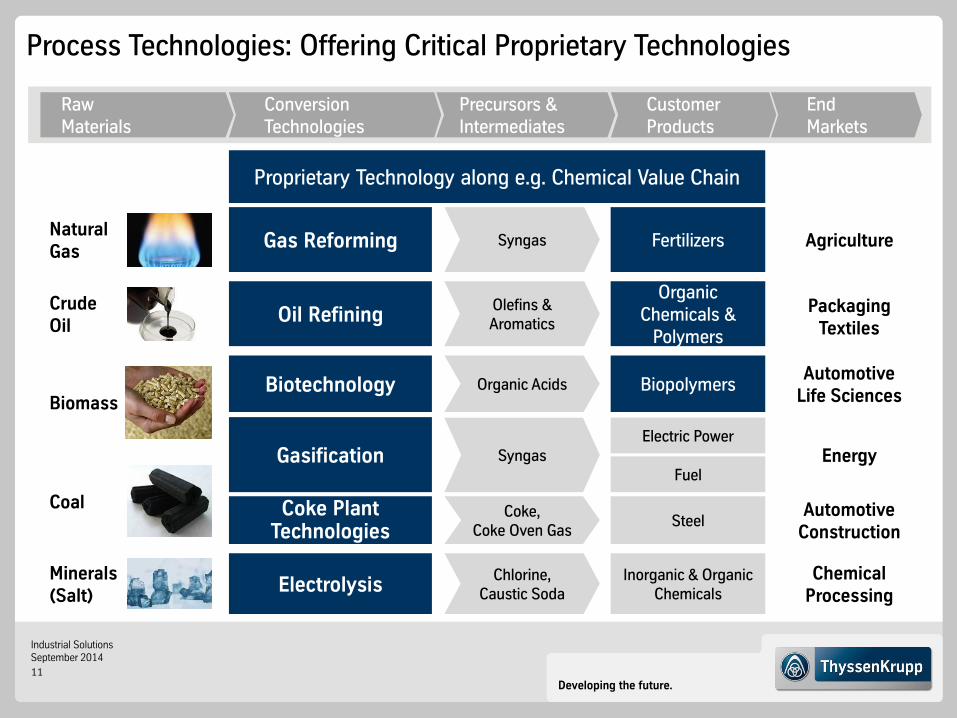

Process Technologies: Offering Critical Proprietary Technologies

Natural Gas

Crude Oil

Gas Reforming

Biomass Biotechnology

Agriculture Syngas Fertilizers

Energy

Automotive Construction

Coal Coke Plant Technologies

Gasification Electric Power

Fuel

Minerals (Salt)

Electrolysis Chemical

Processing

Steel

Inorganic & Organic Chemicals

Raw Materials

Conversion Technologies

Precursors & Intermediates

Customer Products

End Markets

Oil Refining Organic

Chemicals & Polymers

Biopolymers

Proprietary Technology along e.g. Chemical Value Chain

Olefins & Aromatics

Organic Acids

Syngas

Coke, Coke Oven Gas

Chlorine, Caustic Soda

Packaging Textiles

Automotive Life Sciences

Developing the future.

Industrial Solutions September 2014

12

World‘s Largest Fertilizer Complex in Saudi-Arabien

Annual production

4.3 m ha

3,300 t/day ammonia

Production capacity Cultivated area

Developing the future.

Industrial Solutions September 2014

13

Regional

Global Market Size (bn €) Market Segments

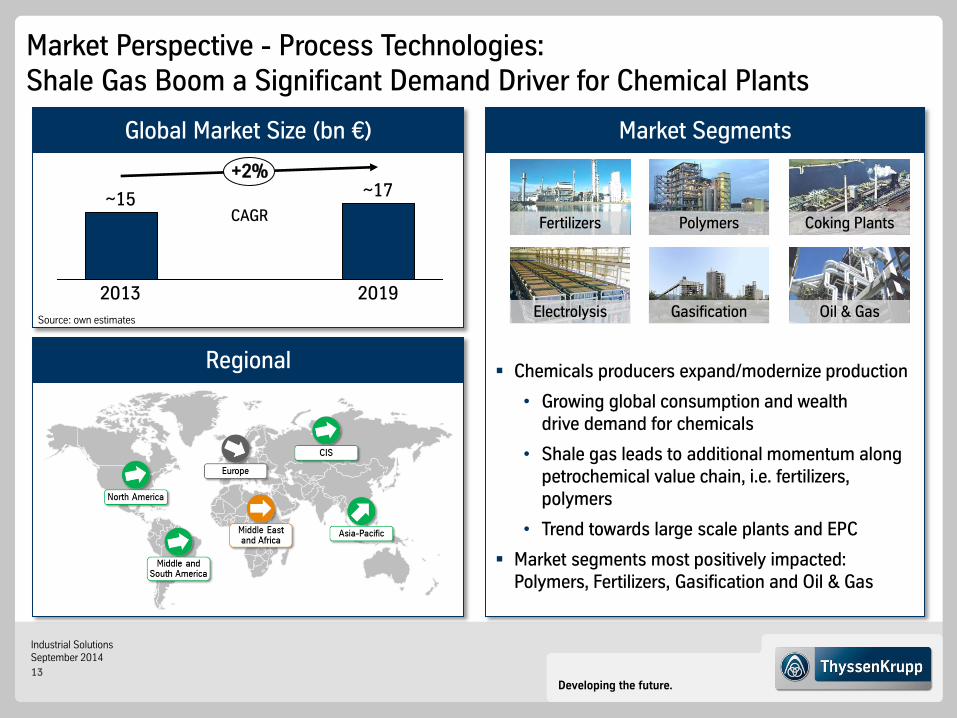

Market Perspective - Process Technologies: Shale Gas Boom a Significant Demand Driver for Chemical Plants

2013 2019

CAGR

Electrolysis Gasification Oil & Gas

Coking Plants Polymers Fertilizers

+2% ~17 ~15

Source: own estimates

Chemicals producers expand/modernize production

• Growing global consumption and wealth drive demand for chemicals

• Shale gas leads to additional momentum along petrochemical value chain, i.e. fertilizers, polymers

• Trend towards large scale plants and EPC

Market segments most positively impacted: Polymers, Fertilizers, Gasification and Oil & Gas

Developing the future.

Industrial Solutions September 2014

14

Resource Technologies: Broad Exposure in Cement and Mining Sectors

Covering entire Cement production chain

Raw material preparation

Clinker production

Cement manufacturing

Comprehensive Mining chain coverage

Developing the future.

Industrial Solutions September 2014

15

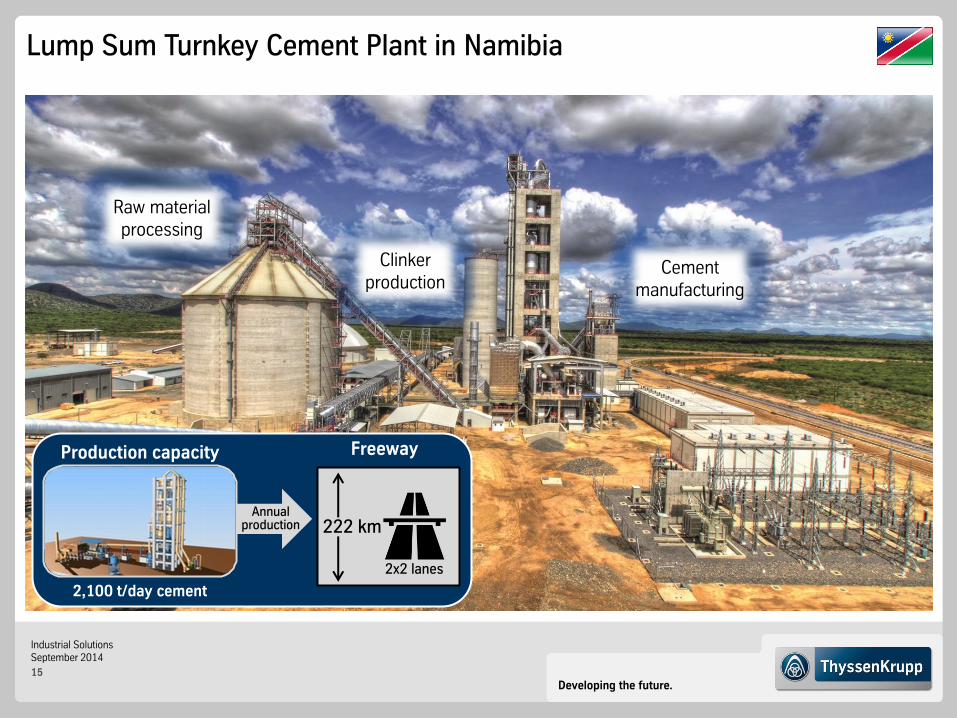

Lump Sum Turnkey Cement Plant in Namibia

2,100 t/day cement

Production capacity Freeway

222 km

2x2 lanes

Annual production

Clinker production

Raw material processing

Cement manufacturing

Developing the future.

Industrial Solutions September 2014

16

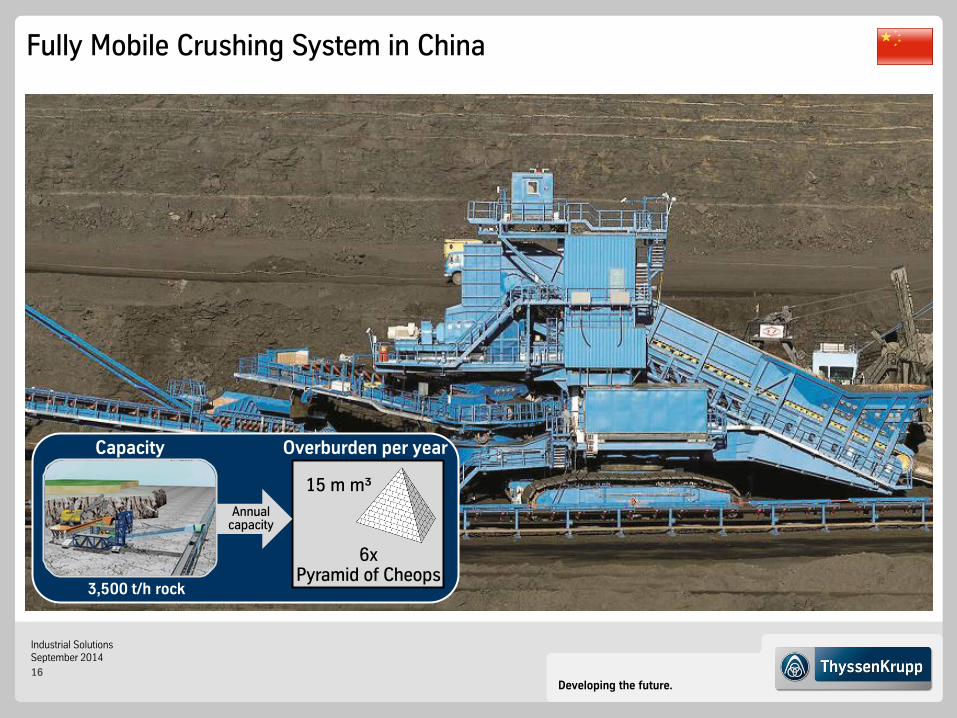

Fully Mobile Crushing System in China

Overburden per year

3,500 t/h rock

Capacity

15 m m³

6x Pyramid of Cheops

Annual capacity

Developing the future.

Industrial Solutions September 2014

17

Regional

Global Market Size (bn €) Market Segments

2013 2019

CAGR

2013 2019

Mining Cement

CAGR

Open Pit Mining Cement

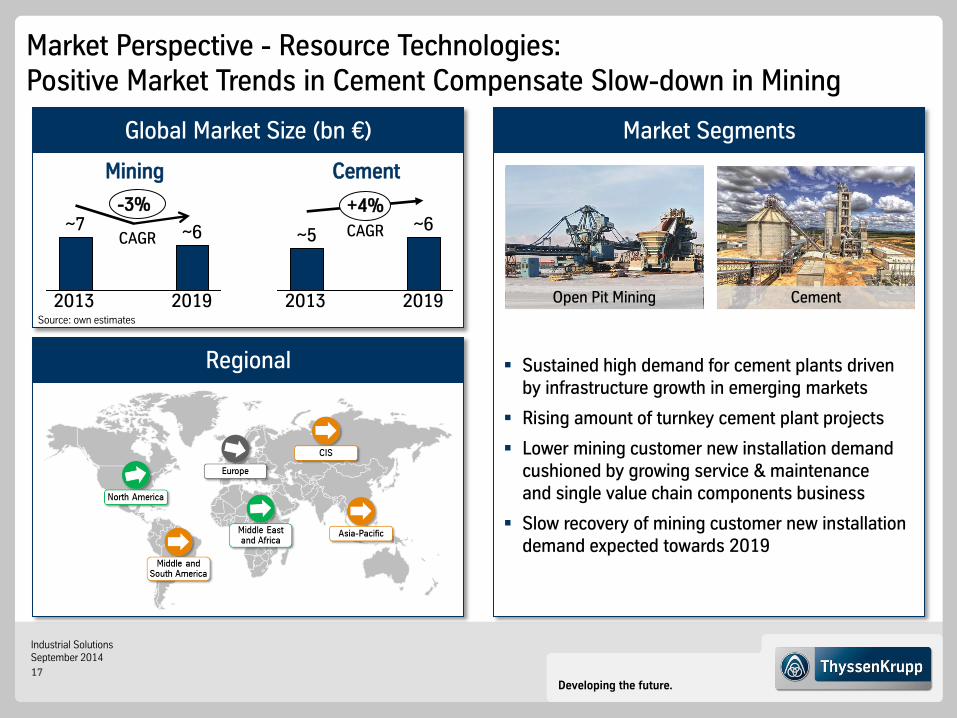

Market Perspective - Resource Technologies: Positive Market Trends in Cement Compensate Slow-down in Mining

~6

-3% ~7

~5

+4% ~6

Source: own estimates

Sustained high demand for cement plants driven by infrastructure growth in emerging markets

Rising amount of turnkey cement plant projects

Lower mining customer new installation demand cushioned by growing service & maintenance and single value chain components business

Slow recovery of mining customer new installation demand expected towards 2019

Developing the future.

Industrial Solutions September 2014

18

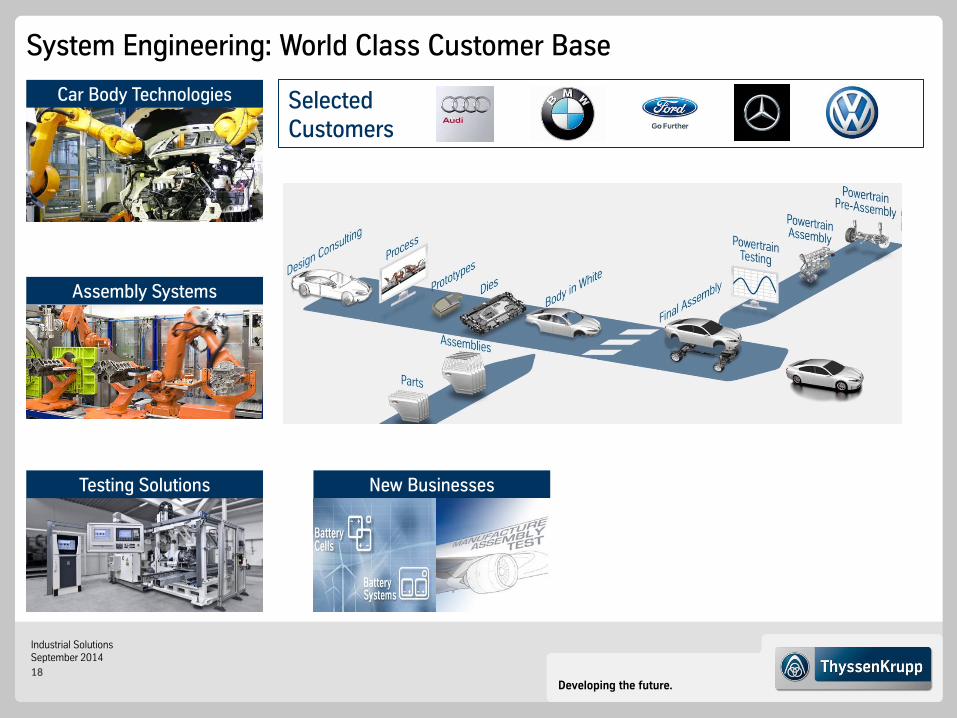

Selected Customers

Car Body Technologies

Testing Solutions

Assembly Systems

New Businesses

System Engineering: World Class Customer Base

Developing the future.

Industrial Solutions September 2014

19

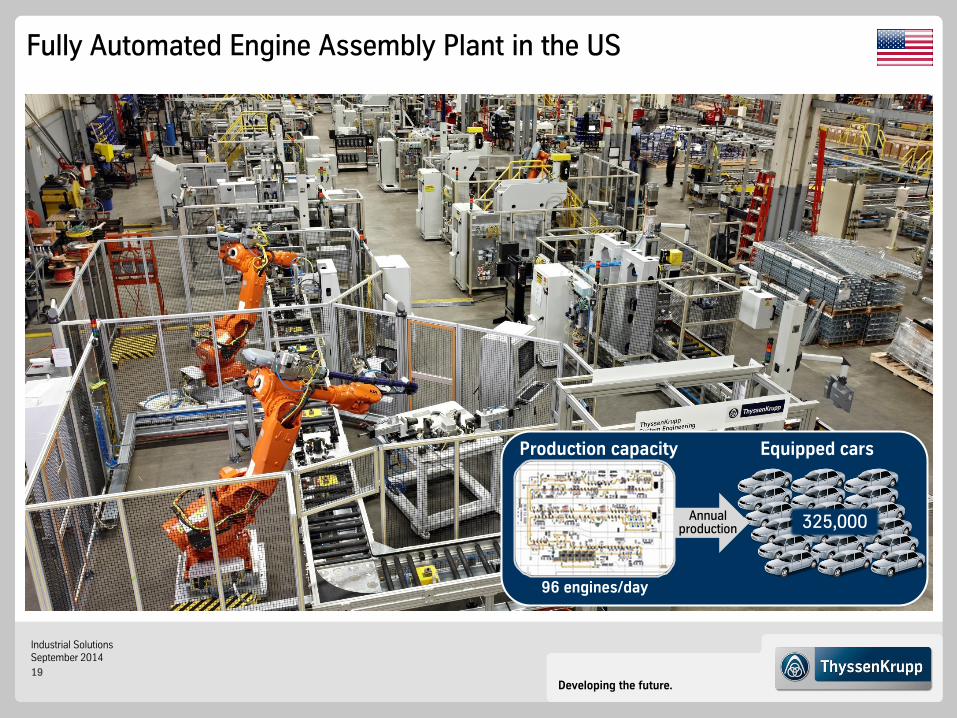

Fully Automated Engine Assembly Plant in the US

Production capacity

96 engines/day

Equipped cars

325,000 Annual production

Developing the future.

Industrial Solutions September 2014

20

Regional

Global Market Size (bn €)

2013 2019

Market Segments

CAGR

Automotive Aerospace

Source: own estimates

Stable project volume on high level

OEM investments driven by car model cycles

E-mobility trend as additional project opportunity

Main growth markets Asia Pacific & China

New opportunities in aerospace industry

+4% ~7

~6

Market Perspective - System Engineering: Long-term Positive Market Outlook with Main Growth Drivers in Asia

Developing the future.

Industrial Solutions September 2014

21

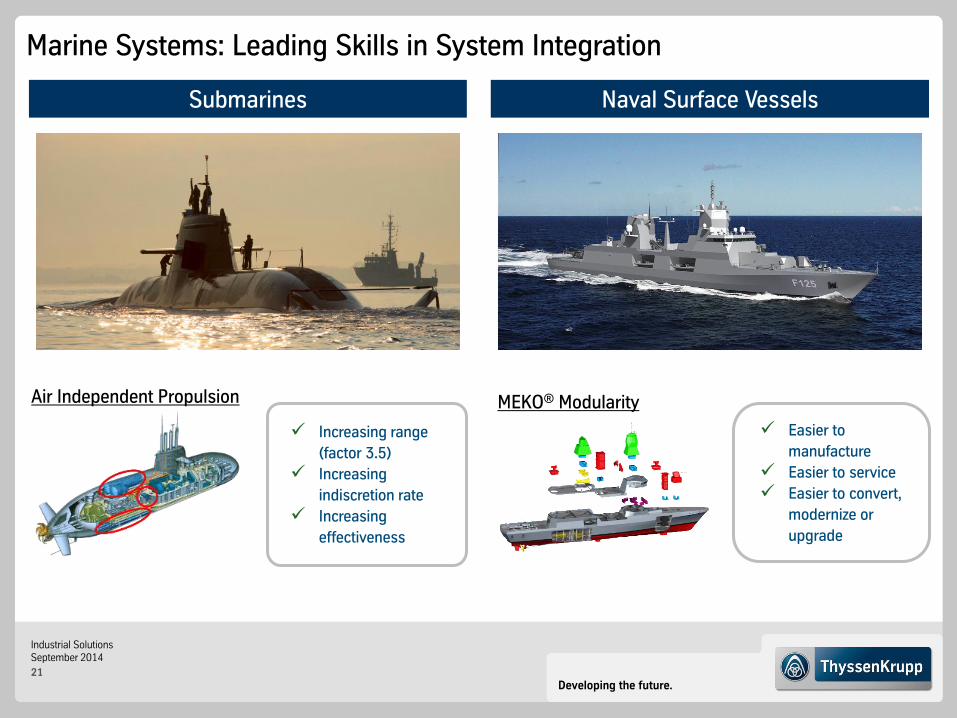

Submarines Naval Surface Vessels

Air Independent Propulsion MEKO® Modularity

Increasing range

(factor 3.5)

Increasing

indiscretion rate

Increasing

effectiveness

Easier to

manufacture

Easier to service

Easier to convert,

modernize or

upgrade

Marine Systems: Leading Skills in System Integration

Developing the future.

Industrial Solutions September 2014

22

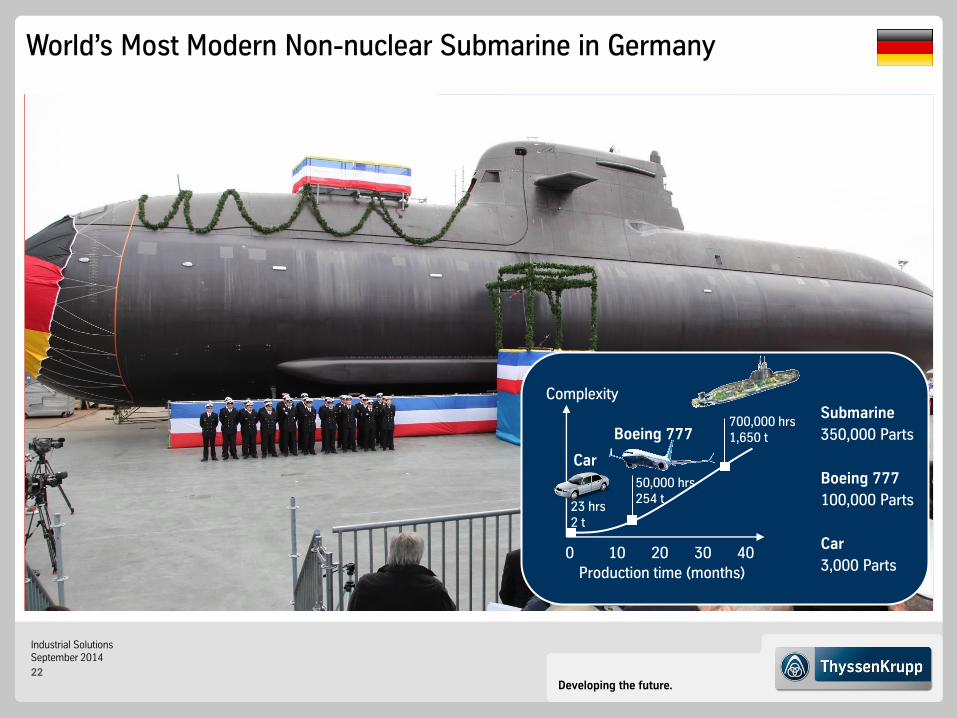

World’s Most Modern Non-nuclear Submarine in Germany

Submarine

350,000 Parts

Boeing 777

100,000 Parts

Car

3,000 Parts

Boeing 777

Car

Production time (months)

50,000 hrs 254 t

23 hrs 2 t

700,000 hrs 1,650 t

0 40 10 20 30

Complexity

Developing the future.

Industrial Solutions September 2014

23

Regional

Global Market Size (bn €)

2013 2019

Market Segments

CAGR

Submarines Naval Surface Vessels

Source: own estimates

Solid global project pipeline

Governmental defense programs driving investments across regions

Growing service market with demand for modernization & maintenance

+6% ~6

~4

Market Perspective - Marine Systems: Global Defense Budgets Drive Naval Demand

Developing the future.

Industrial Solutions September 2014

24

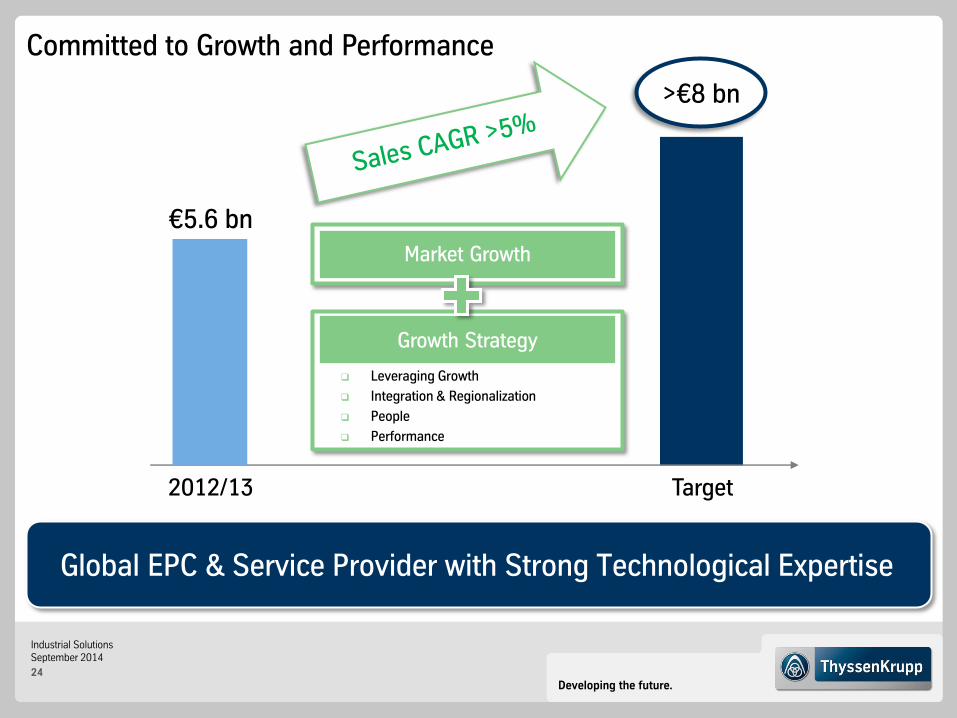

Market Growth

Committed to Growth and Performance

Target 2012/13

€5.6 bn

>€8 bn

Global EPC & Service Provider with Strong Technological Expertise

Growth Strategy

Leveraging Growth

Integration & Regionalization

People

Performance

Developing the future.

Industrial Solutions September 2014

25

Disclaimer ThyssenKrupp AG

“The information set forth and included in this presentation is not provided in connection with an offer or solicitation for the purchase

or sale of a security and is intended for informational purposes only.

This presentation contains forward-looking statements that are subject to risks and uncertainties. Statements contained herein that

are not statements of historical fact may be deemed to be forward-looking information. When we use words such as “plan,” “believe,”

“expect,” “anticipate,” “intend,” “estimate,” “may” or similar expressions, we are making forward-looking statements. You should not

rely on forward-looking statements because they are subject to a number of assumptions concerning future events, and are subject to

a number of uncertainties and other factors, many of which are outside of our control, that could cause actual results to differ

materially from those indicated. These factors include, but are not limited to, the following:

(i) market risks: principally economic price and volume developments,

(ii) dependence on performance of major customers and industries,

(iii) our level of debt, management of interest rate risk and hedging against commodity price risks;

(iv) costs associated with, and regulation relating to, our pension liabilities and healthcare measures,

(v) environmental protection and remediation of real estate and associated with rising standards for real estate environmental

protection,

(vi) volatility of steel prices and dependence on the automotive industry,

(vii) availability of raw materials;

(viii) inflation, interest rate levels and fluctuations in exchange rates;

(ix) general economic, political and business conditions and existing and future governmental regulation; and

(x) the effects of competition.

Please note that we disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new

information, future events or otherwise.”