Sprachen

Seiten

Rechtliche

Uber die Verwendung von Copula-Funktionen im quantitativen

Risikomanagement und in der Untersuchung von Bankenkrisen

INAUGURALDISSERTATION

zur

Erlangung der Wurde

eines Doktors der

Wirtschaftswissenschaft

der

Fakultat fur Wirtschaftswissenschaft

der

Ruhr-Universitat Bochum

vorgelegt von

Diplom-KaufmannGregor Nikolaus Felix Weiß

aus Kamen2010

i

Dekan: Prof. Dr. Stephan PaulReferent: Prof. Dr. Stephan PaulKoreferent: Prof. Dr. Manfred LoschTag der mundlichen Prufung: 10. Februar 2010

Inhaltsverzeichnis

Inhaltsverzeichnis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Abbildungsverzeichnis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

1 Einleitung 1

1.1 Einfuhrung in die Thematik und Motivation . . . . . . . . . . . . . . . . 1

1.2 Zusammenfassung und Publikationsdetails . . . . . . . . . . . . . . . . . 6

2 Copula-Funktionen 10

2.1 Einleitung . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.2 Charakteristika von Copula-Funktionen . . . . . . . . . . . . . . . . . . 11

2.3 Anwendungsmoglichkeiten von Copula-Funktionen im Risikomanagement 17

3 Uber die Vorteilhaftigkeit von Copula-GARCH-Modellen im finanzwirtschaft-

lichen Risikomanagement 19

3.1 Einleitung . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.2 Literaturuberblick und Hypothesenbildung . . . . . . . . . . . . . . . . . 21

3.3 Univariate VaR-Schatzung mithilfe von GARCH-Prozessen . . . . . . . . 26

3.4 Multivariate VaR-Schatzung mithilfe von Korrelationen und Copula-Funk-

tionen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.4.1 Aggregation des Value-at-Risks auf Portfolioebene mithilfe von

Korrelationen . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.4.2 Copula-Modelle zur Ermittlung des Gesamtrisikos . . . . . . . . 29

3.4.2.1 Grundlagen der Copula-Theorie . . . . . . . . . . . . . 29

3.4.2.2 Parametrische Copulas . . . . . . . . . . . . . . . . . 30

3.4.2.3 Parameterschatzung . . . . . . . . . . . . . . . . . . . 32

3.4.2.4 Anpassungstests zur Prufung der Gute einer Copula-

Schatzung . . . . . . . . . . . . . . . . . . . . . . . . 34

ii

INHALTSVERZEICHNIS iii

3.4.2.5 Bestimmung des Portfolio-Value-at-Risks . . . . . . . 36

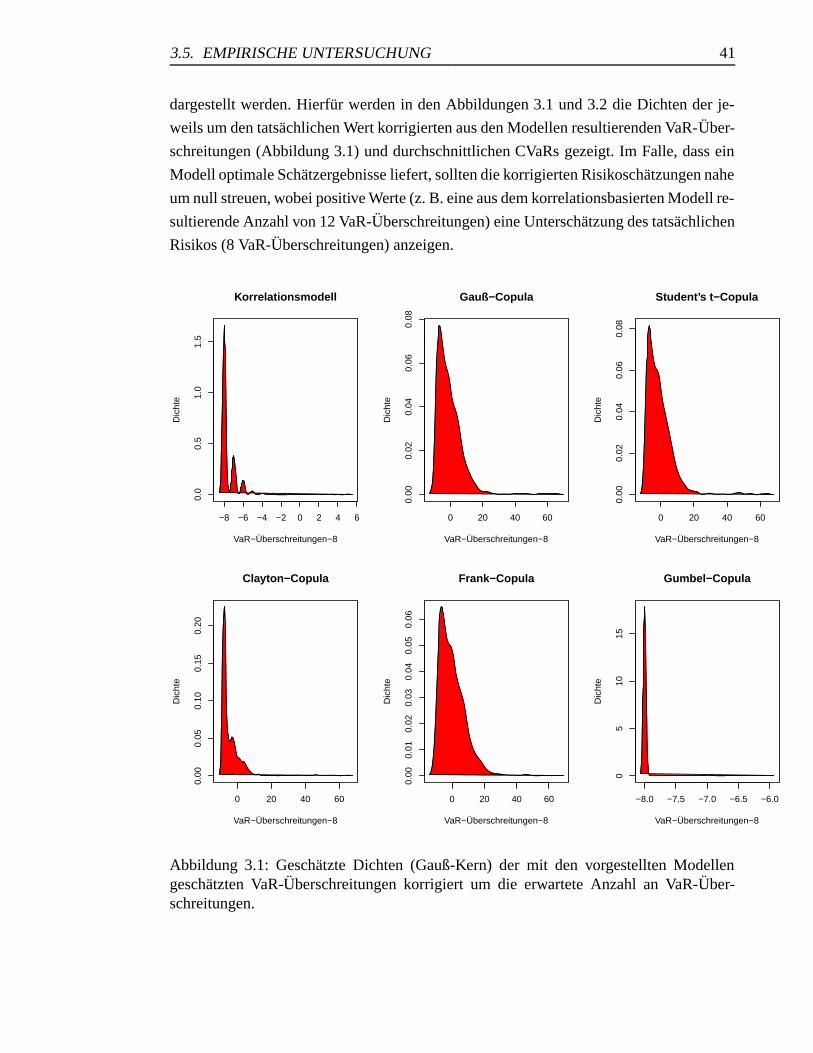

3.5 Empirische Untersuchung . . . . . . . . . . . . . . . . . . . . . . . . . . 37

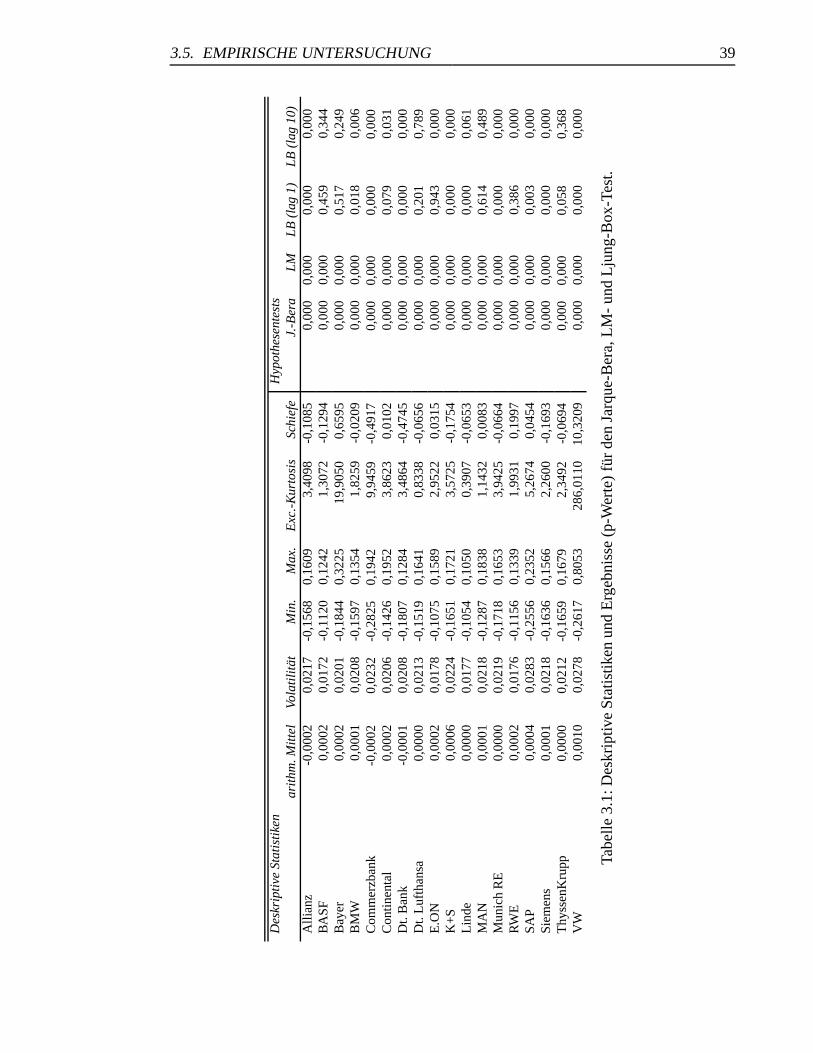

3.5.1 Datenbasis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3.5.2 Univariate Schatzung . . . . . . . . . . . . . . . . . . . . . . . . 40

3.5.3 Multivariate Schatzung . . . . . . . . . . . . . . . . . . . . . . . 40

3.6 Zusammenfassung . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

4 Copula Parameter Estimation - Numerical Considerations And Implications

For Risk Management 56

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

4.2 Copula parameter estimation . . . . . . . . . . . . . . . . . . . . . . . . 58

4.2.1 Parametric copulas . . . . . . . . . . . . . . . . . . . . . . . . . 59

4.2.2 Parameter estimation via maximum-likelihood . . . . . . . . . . 61

4.2.3 Minimum-distance estimators . . . . . . . . . . . . . . . . . . . 62

4.2.3.1 Minimum-distance estimators based on the empirical

copula process . . . . . . . . . . . . . . . . . . . . . . 62

4.2.3.2 Minimum-distance estimators based on Kendall’s de-

pendence function . . . . . . . . . . . . . . . . . . . . 64

4.2.3.3 Minimum-distance estimators based on Rosenblatt’s trans-

form . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

4.2.4 Numerical properties of the copula parameter estimators . . . . . 65

4.3 Simulation study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

4.3.1 Design of the simulation study . . . . . . . . . . . . . . . . . . . 68

4.3.2 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

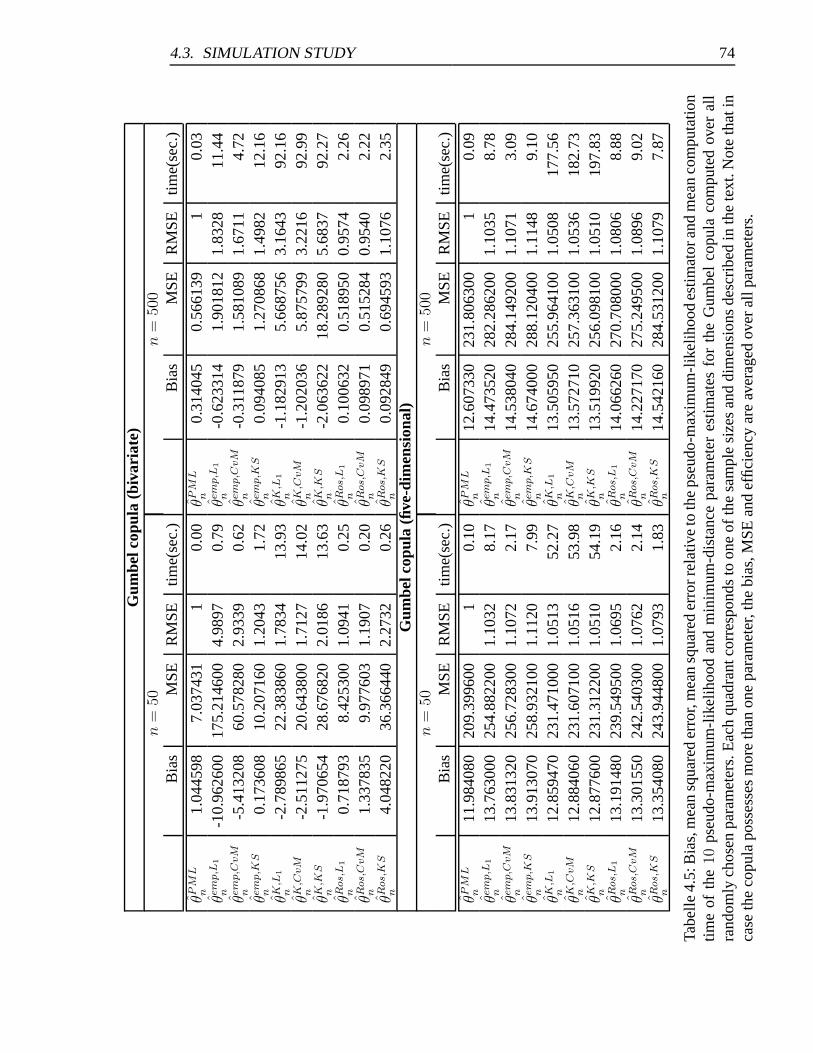

4.3.2.1 Comparison of the mean bias and MSE . . . . . . . . . 75

4.3.2.2 Results concerning the sample size and dimensionality . 76

4.3.2.3 Results concerning the computational complexity . . . 76

4.4 Empirical Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

4.4.1 Data and model description . . . . . . . . . . . . . . . . . . . . 77

INHALTSVERZEICHNIS iv

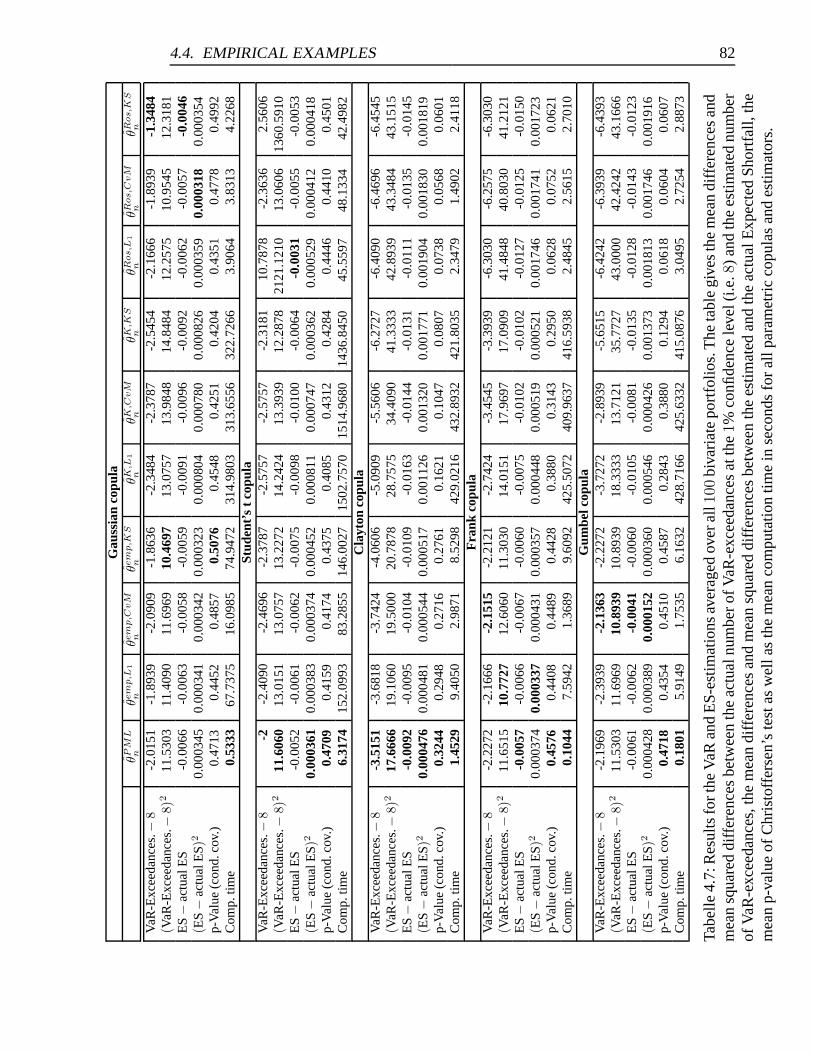

4.4.2 Results and discussion . . . . . . . . . . . . . . . . . . . . . . . 81

4.5 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

5 Bank Contagion 85

5.1 Einfuhrung . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

5.2 Definition des Begriffes bank contagion . . . . . . . . . . . . . . . . . . 86

5.3 Ubertragungskanale und Ursachen finanzwirtschaftlicher Krisen . . . . . 88

6 Analysing Bank Contagion with Copulæ - Evidence from the Subprime and

Japan’s banking crises 91

6.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

6.2 Bank contagion and lenders of last resort . . . . . . . . . . . . . . . . . . 94

6.3 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

6.3.1 GARCH-filtering and abnormal returns . . . . . . . . . . . . . . 95

6.3.2 Some preliminary copula theory . . . . . . . . . . . . . . . . . . 97

6.3.3 Detecting contagion effects with copulae . . . . . . . . . . . . . 102

6.4 Data and empirical findings . . . . . . . . . . . . . . . . . . . . . . . . . 105

6.4.1 Panel A: Germany 2006-2008 . . . . . . . . . . . . . . . . . . . 105

6.4.1.1 Sample description and ARMA-GARCH-modelling . . 105

6.4.1.2 Abnormal returns . . . . . . . . . . . . . . . . . . . . 107

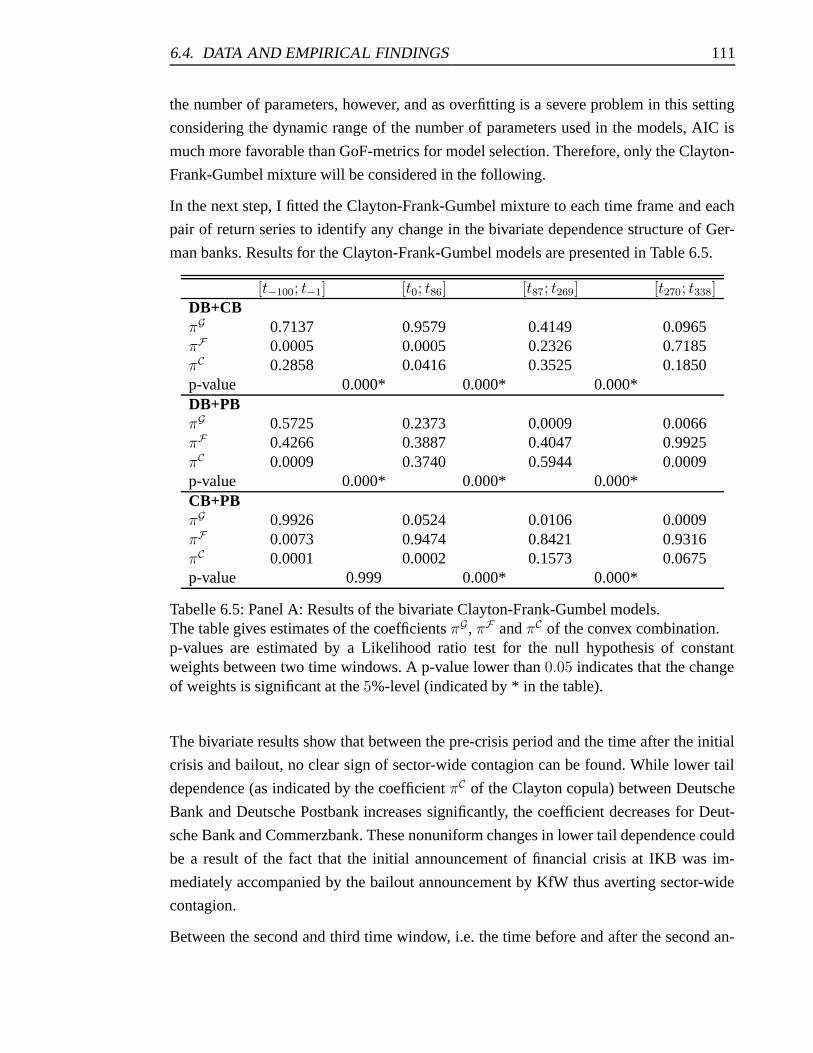

6.4.1.3 Detecting contagion effects by the use of copulae . . . 109

6.4.1.4 Robustness checks . . . . . . . . . . . . . . . . . . . . 112

6.4.2 Panel B: Japan 1994-1999 . . . . . . . . . . . . . . . . . . . . . 117

6.4.2.1 Sample description and ARMA-GARCH-modelling . . 117

6.4.2.2 Events and abnormal returns . . . . . . . . . . . . . . 117

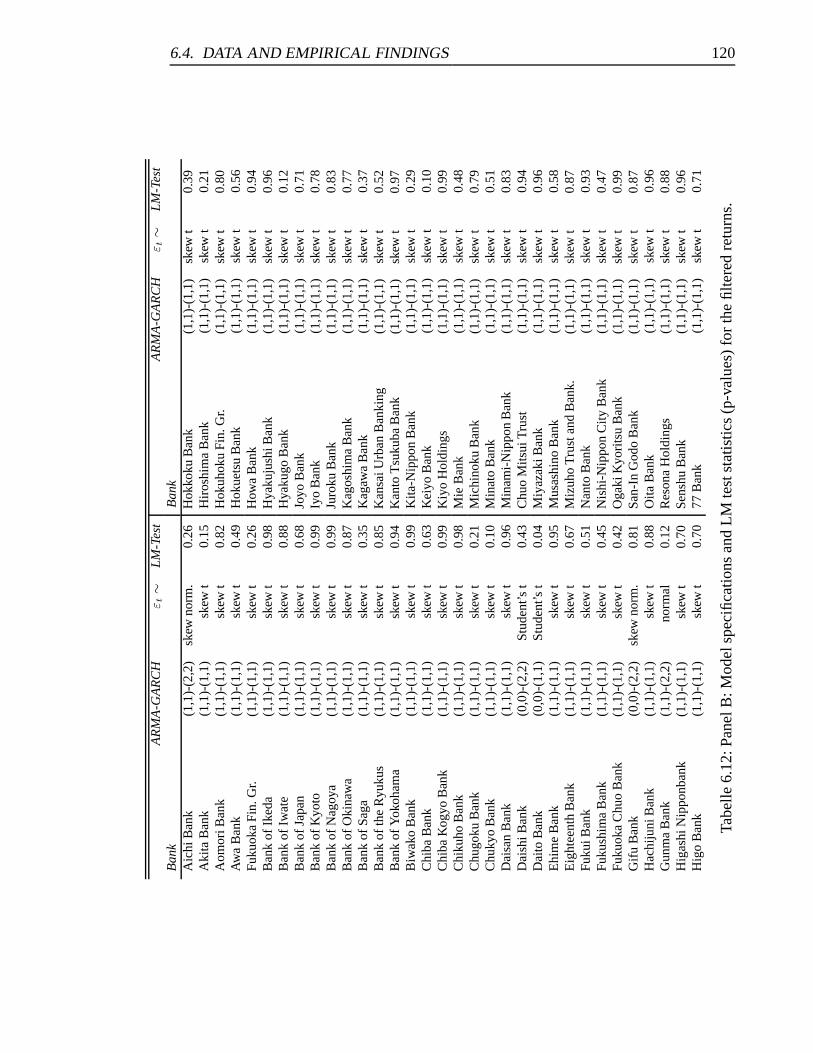

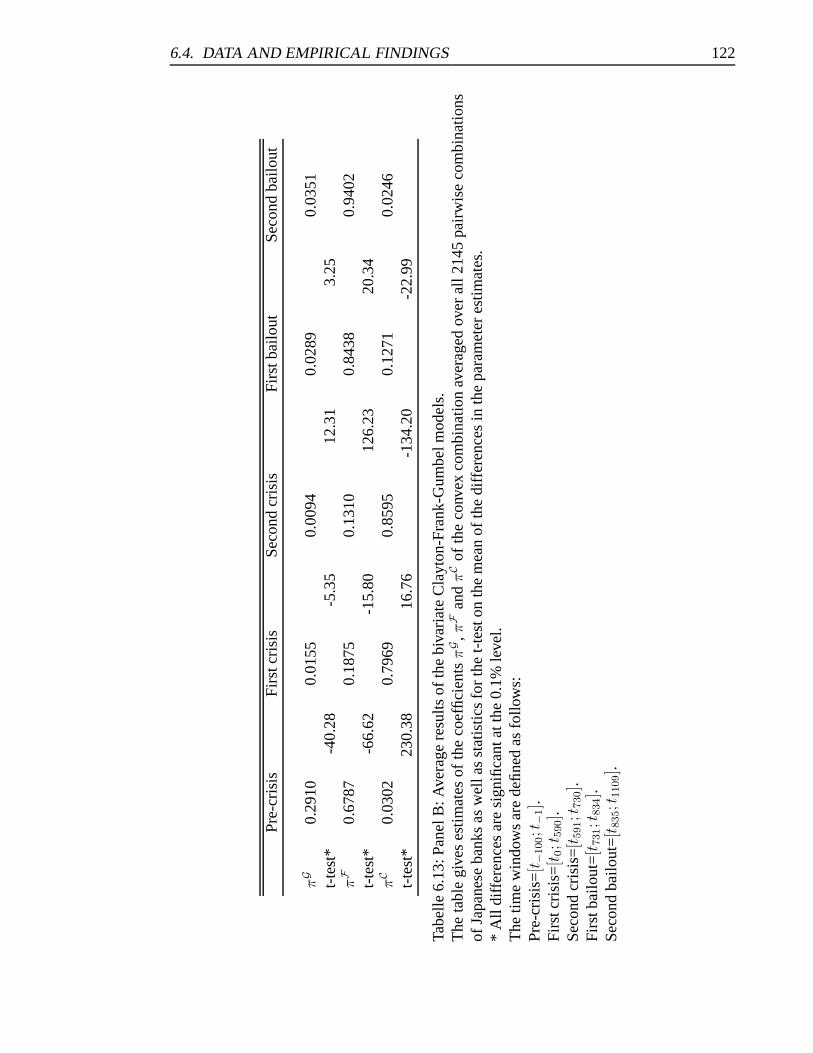

6.4.2.3 Copula Analysis . . . . . . . . . . . . . . . . . . . . . 121

6.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

A Literatur 126

INHALTSVERZEICHNIS v

B Empirical observators for the MD-estimators based on Kendall’s dependence

function 137

C Outline of the L-BFGS-B algorithm 139

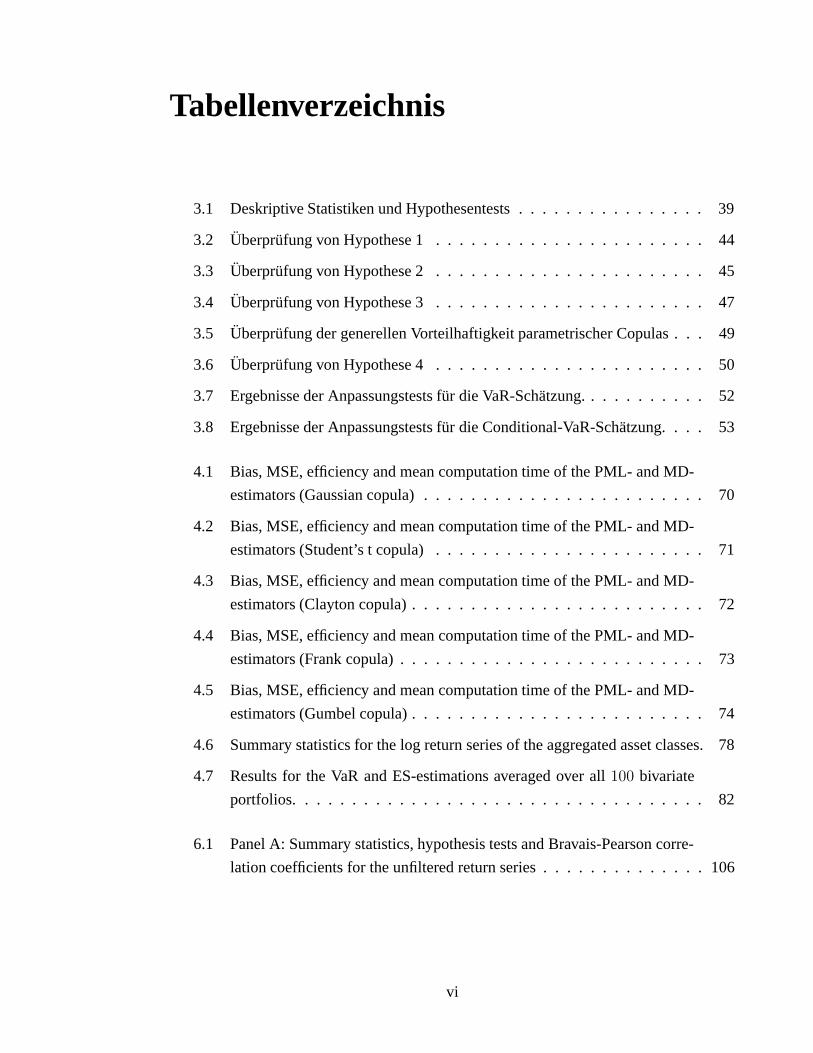

Tabellenverzeichnis

3.1 Deskriptive Statistiken und Hypothesentests . . . . . . . . . . . . . . . . 39

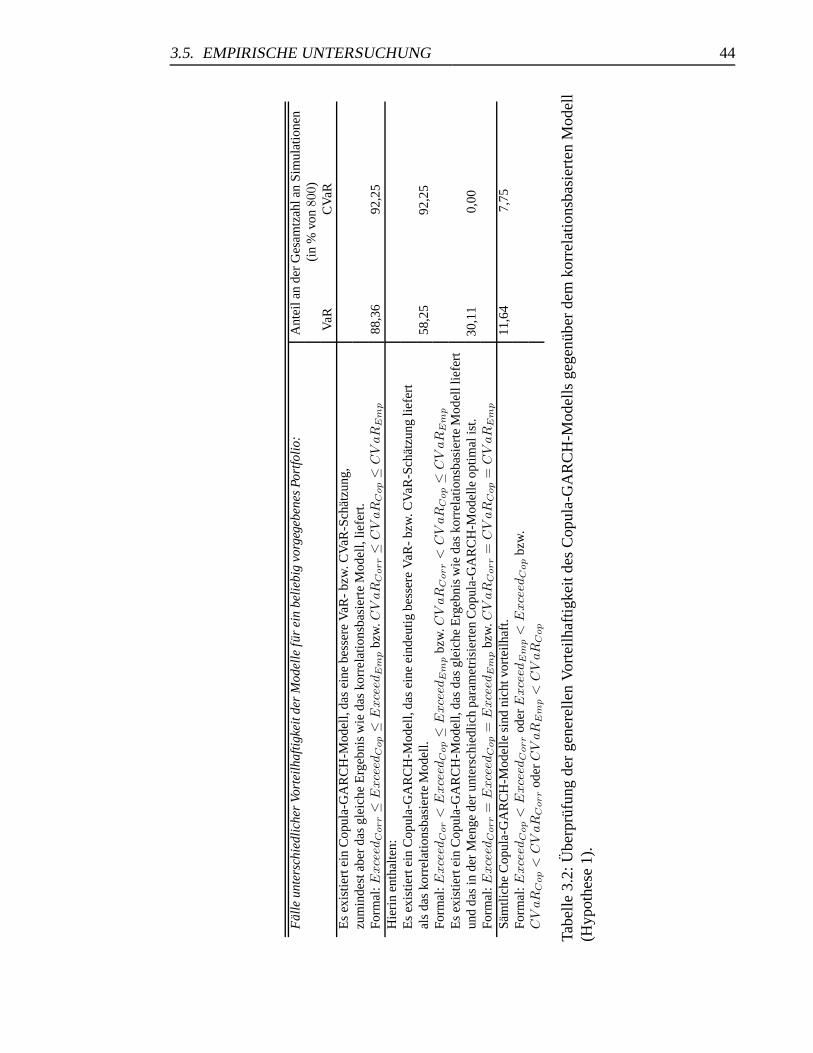

3.2 Uberprufung von Hypothese 1 . . . . . . . . . . . . . . . . . . . . . . . 44

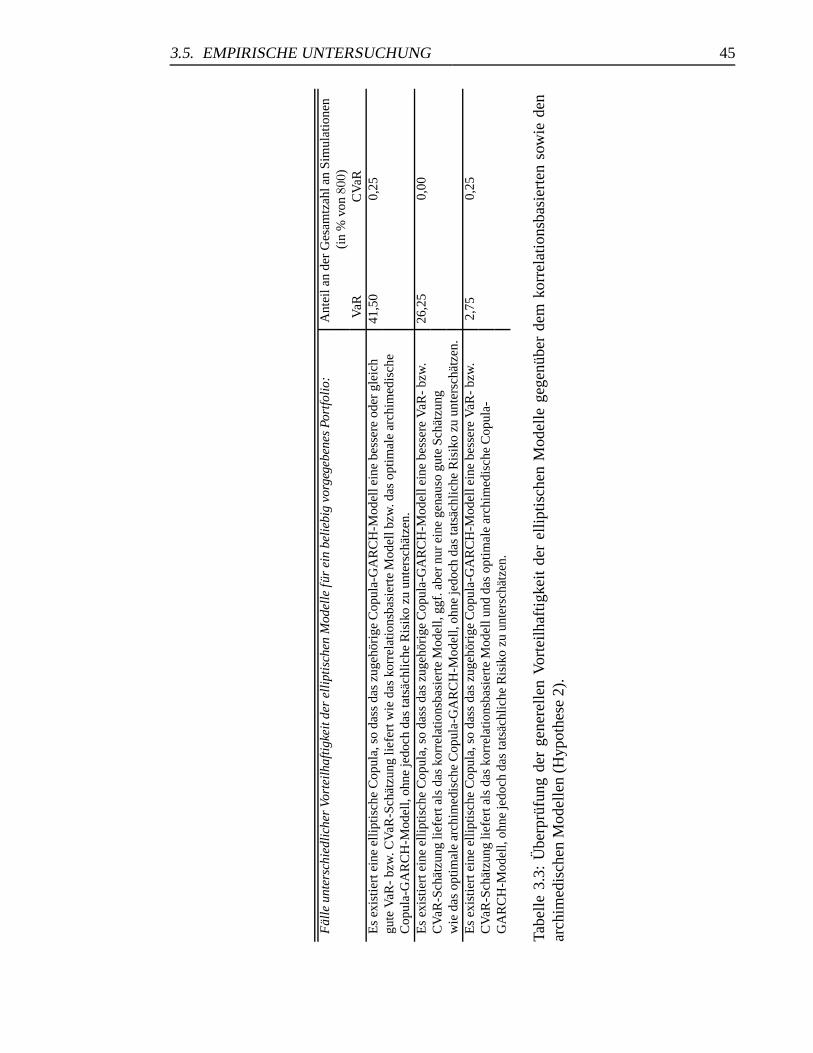

3.3 Uberprufung von Hypothese 2 . . . . . . . . . . . . . . . . . . . . . . . 45

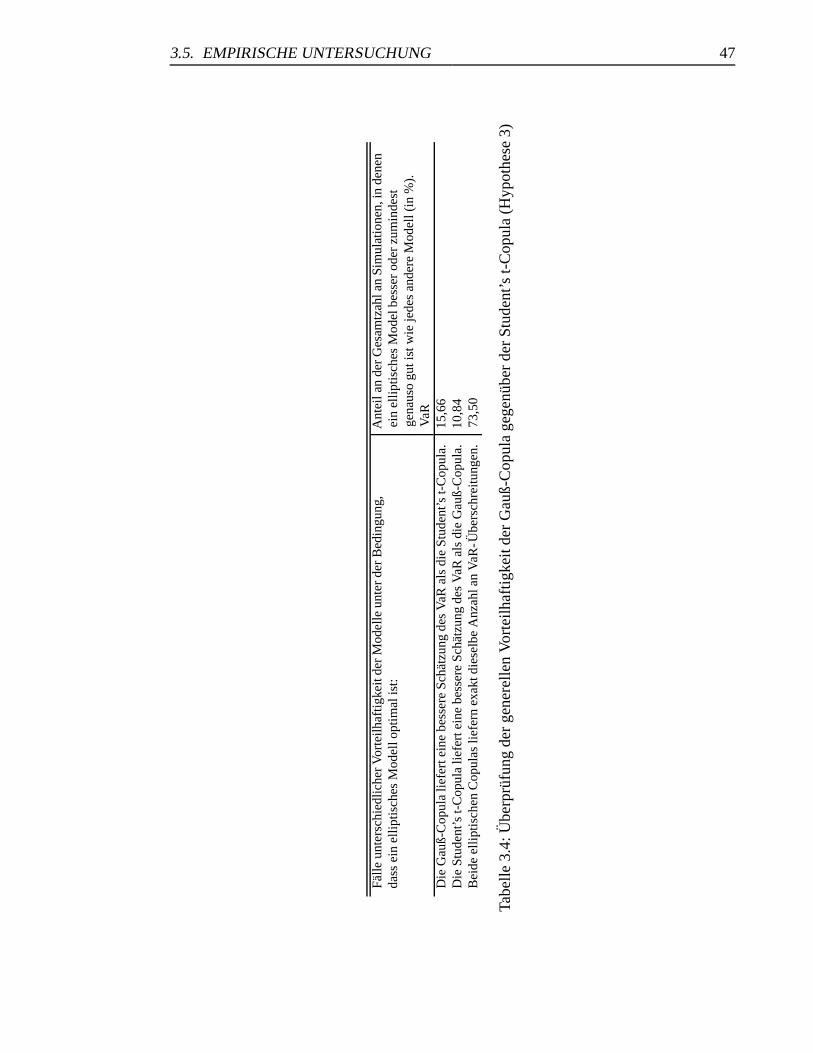

3.4 Uberprufung von Hypothese 3 . . . . . . . . . . . . . . . . . . . . . . . 47

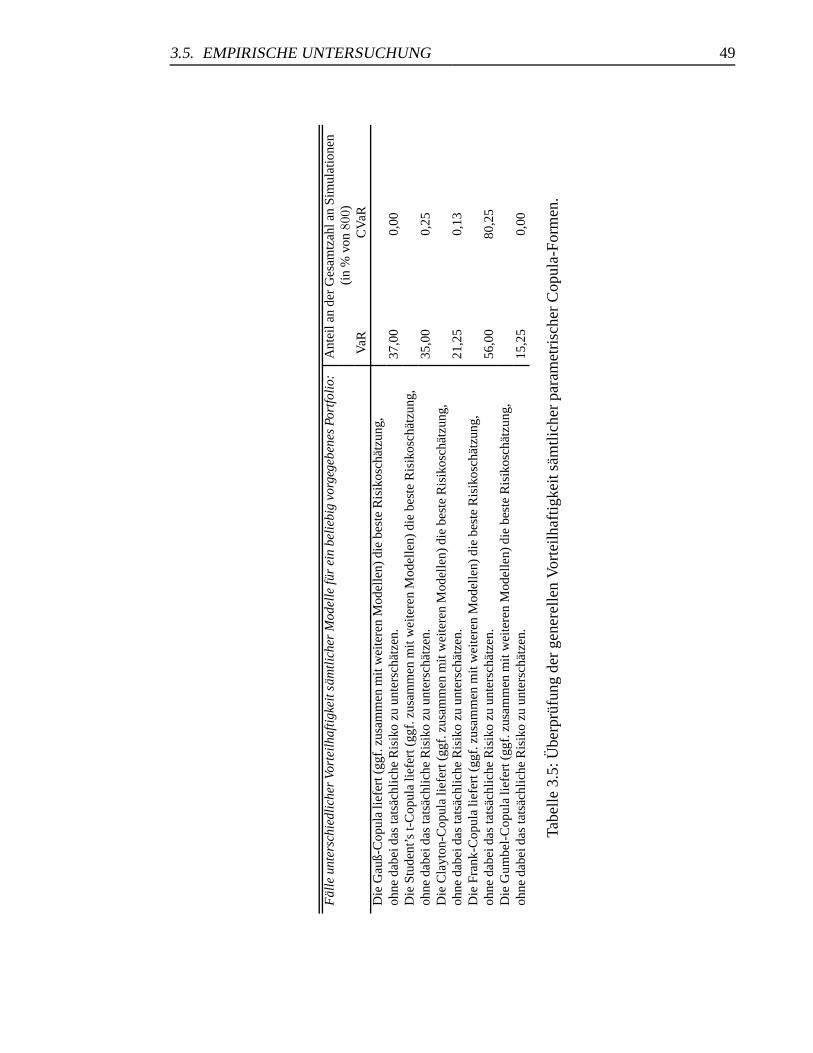

3.5 Uberprufung der generellen Vorteilhaftigkeit parametrischer Copulas . . . 49

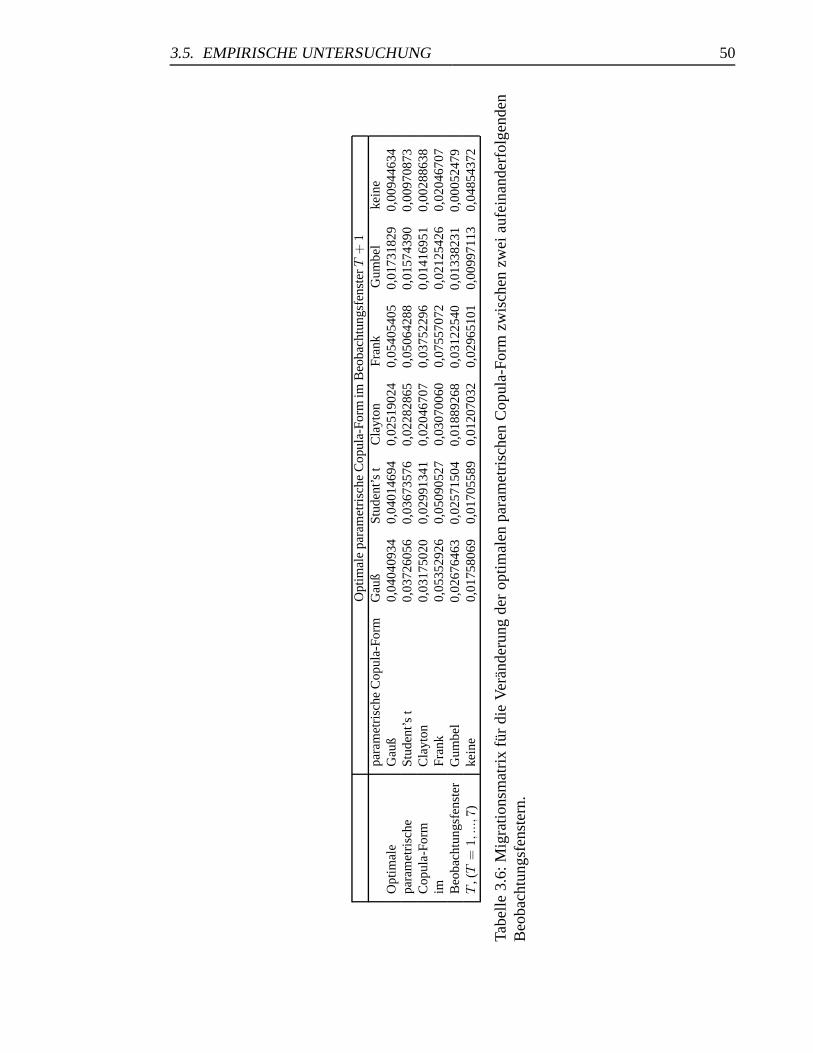

3.6 Uberprufung von Hypothese 4 . . . . . . . . . . . . . . . . . . . . . . . 50

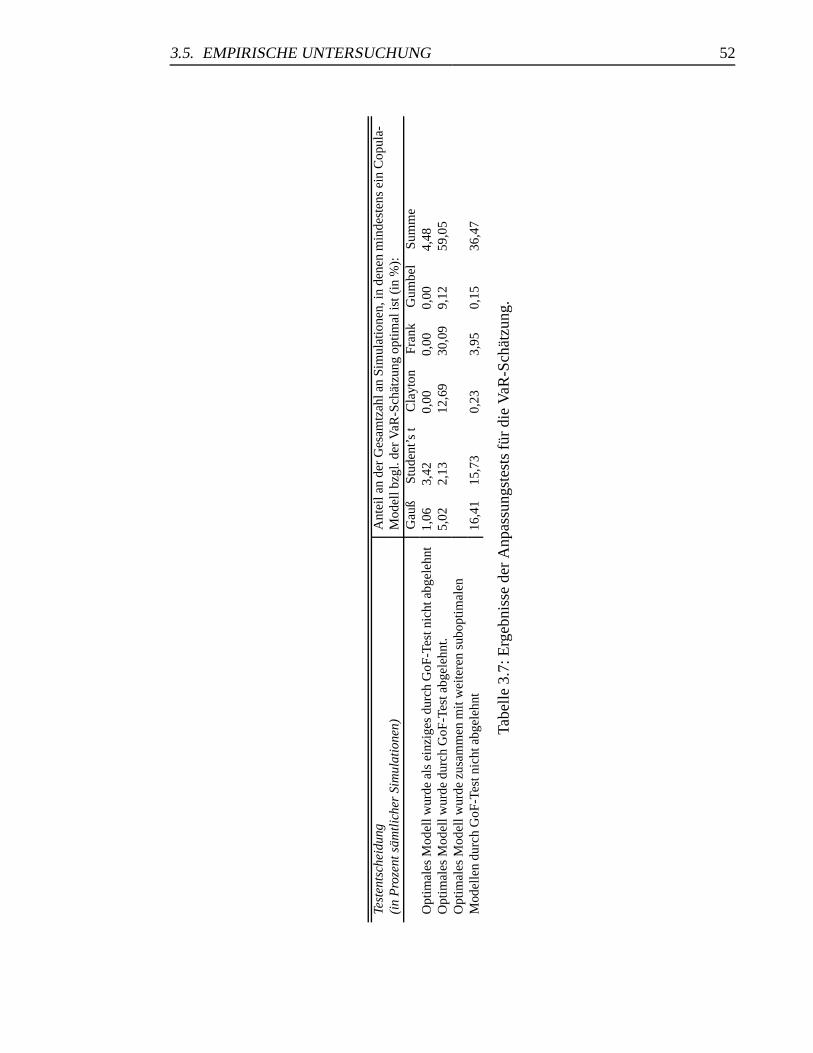

3.7 Ergebnisse der Anpassungstests fur die VaR-Schatzung. . . . . . . . . . . 52

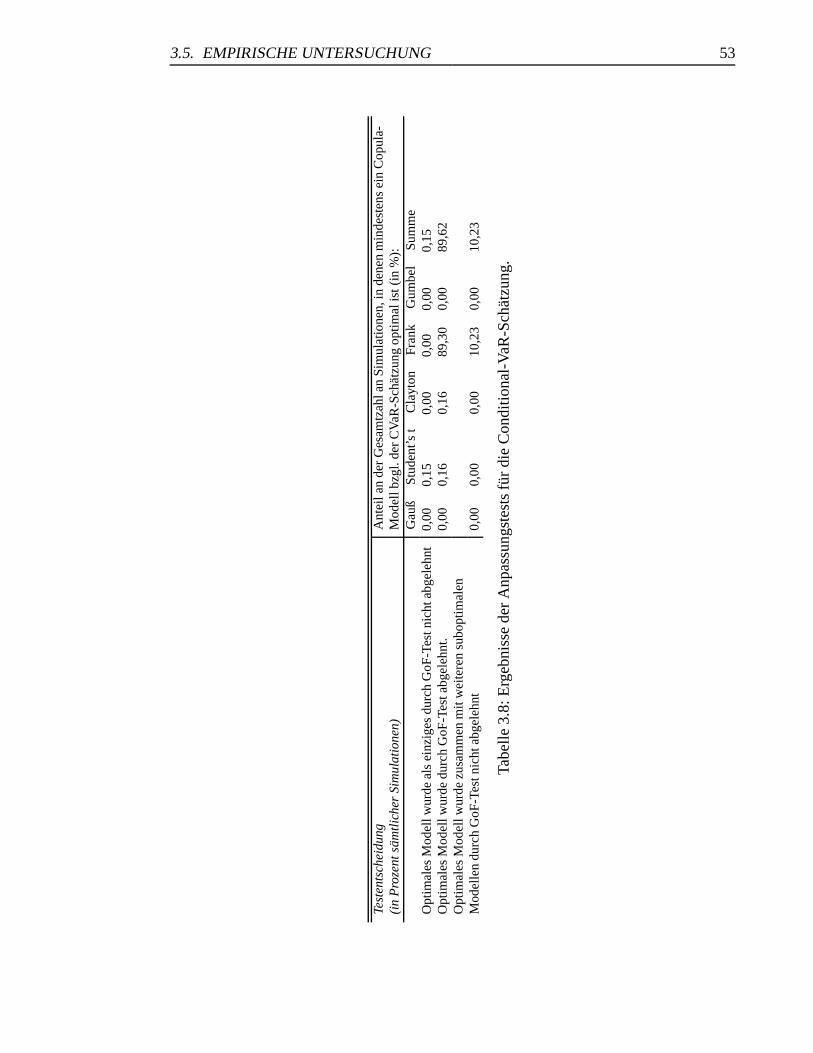

3.8 Ergebnisse der Anpassungstests fur die Conditional-VaR-Schatzung. . . . 53

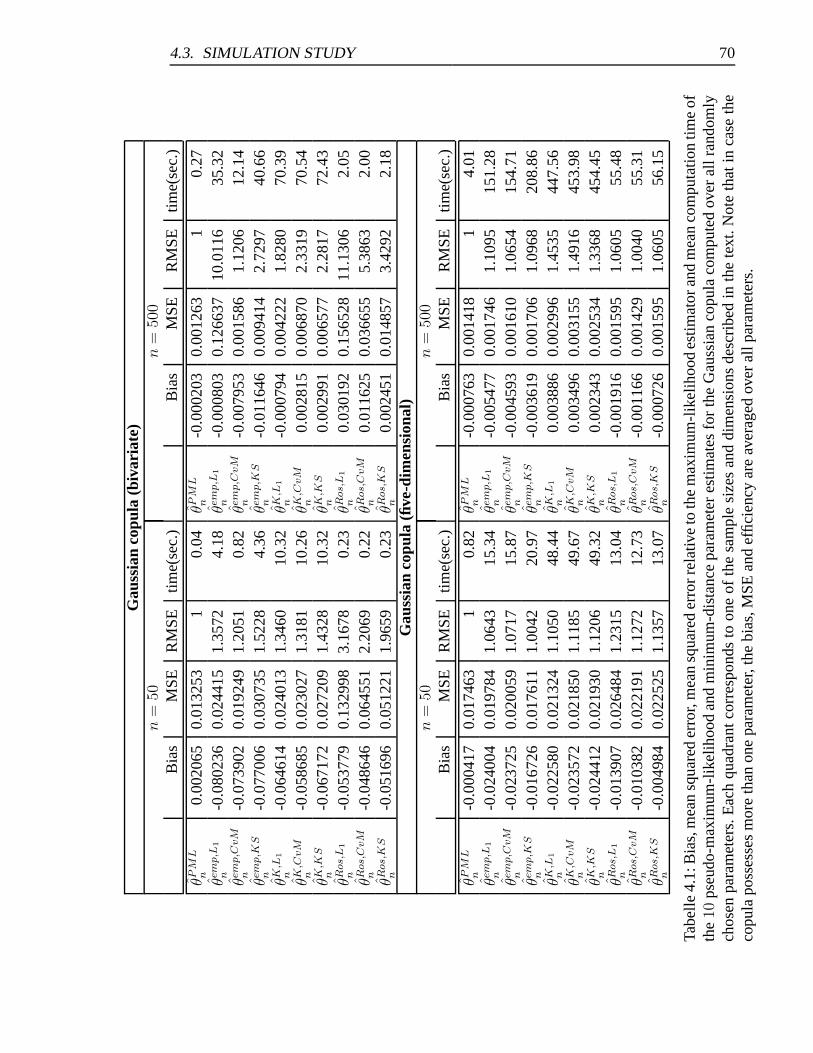

4.1 Bias, MSE, efficiency and mean computation time of the PML- and MD-

estimators (Gaussian copula) . . . . . . . . . . . . . . . . . . . . . . . . 70

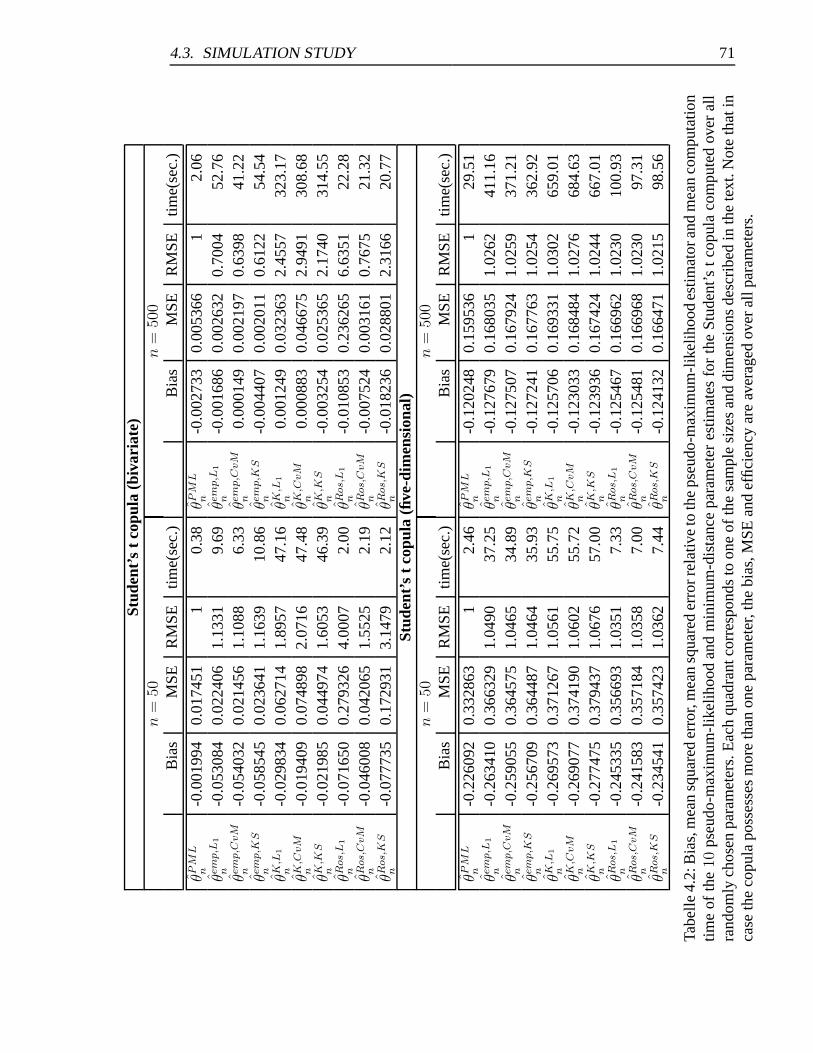

4.2 Bias, MSE, efficiency and mean computation time of the PML- and MD-

estimators (Student’s t copula) . . . . . . . . . . . . . . . . . . . . . . . 71

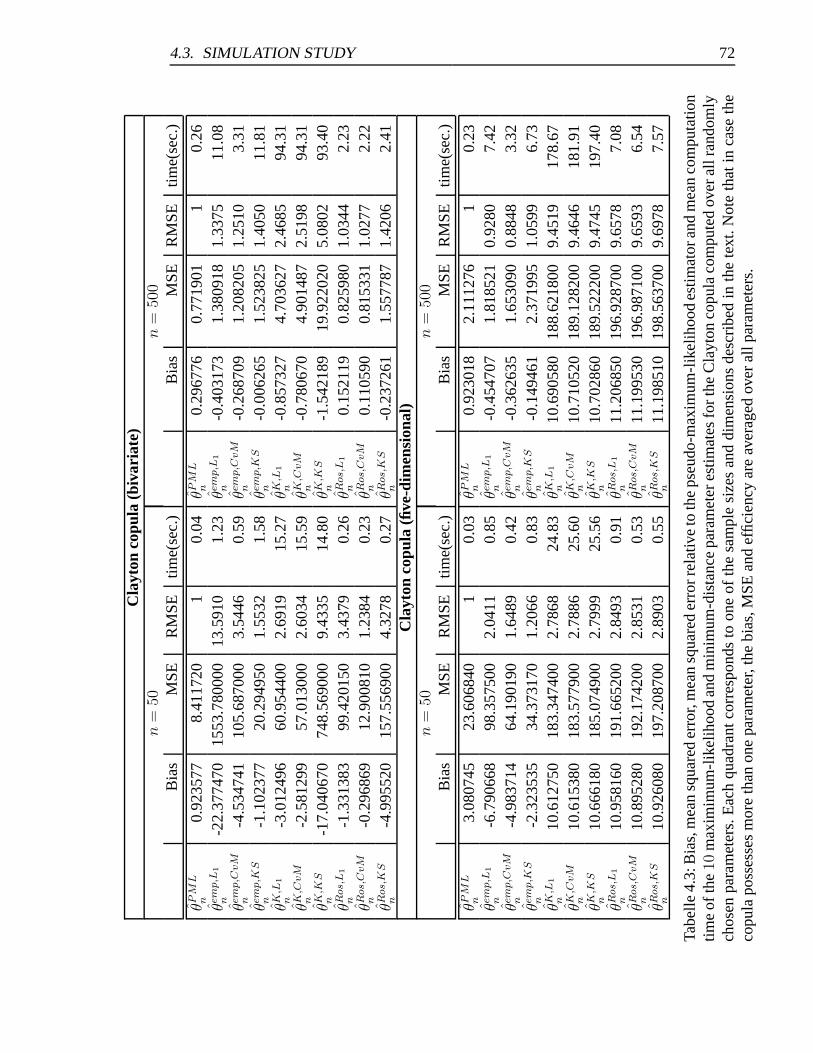

4.3 Bias, MSE, efficiency and mean computation time of the PML- and MD-

estimators (Clayton copula) . . . . . . . . . . . . . . . . . . . . . . . . . 72

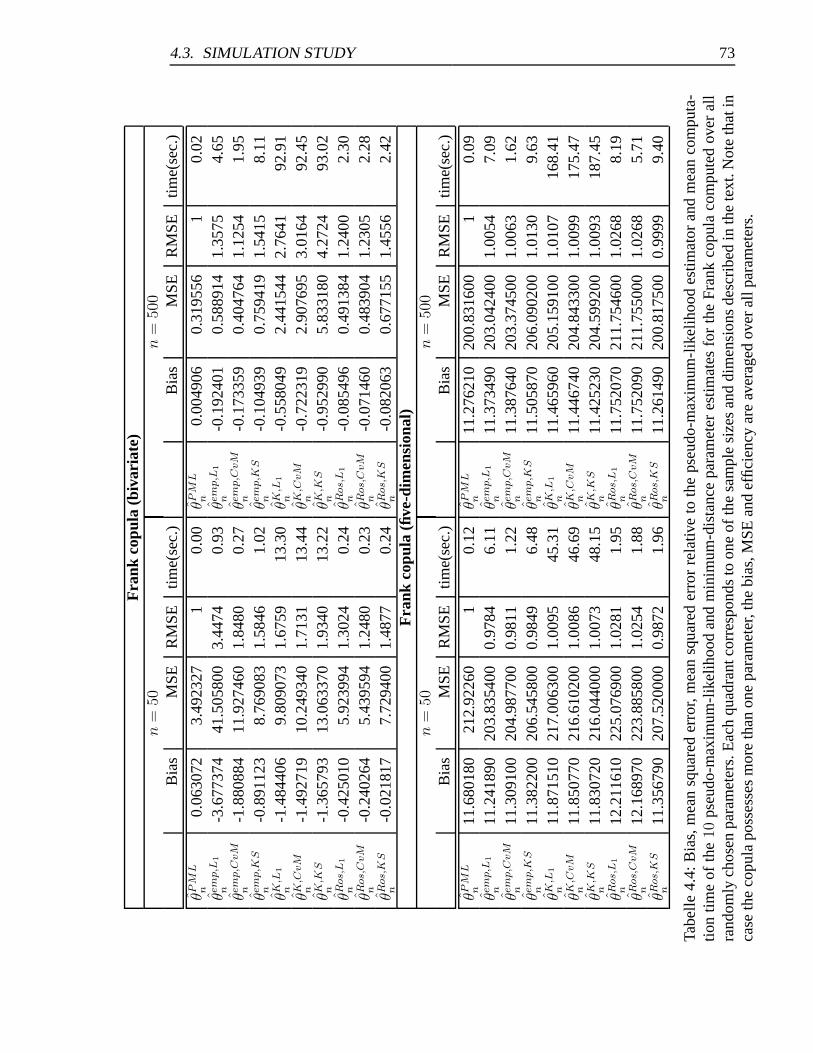

4.4 Bias, MSE, efficiency and mean computation time of the PML- and MD-

estimators (Frank copula) . . . . . . . . . . . . . . . . . . . . . . . . . . 73

4.5 Bias, MSE, efficiency and mean computation time of the PML- and MD-

estimators (Gumbel copula) . . . . . . . . . . . . . . . . . . . . . . . . . 74

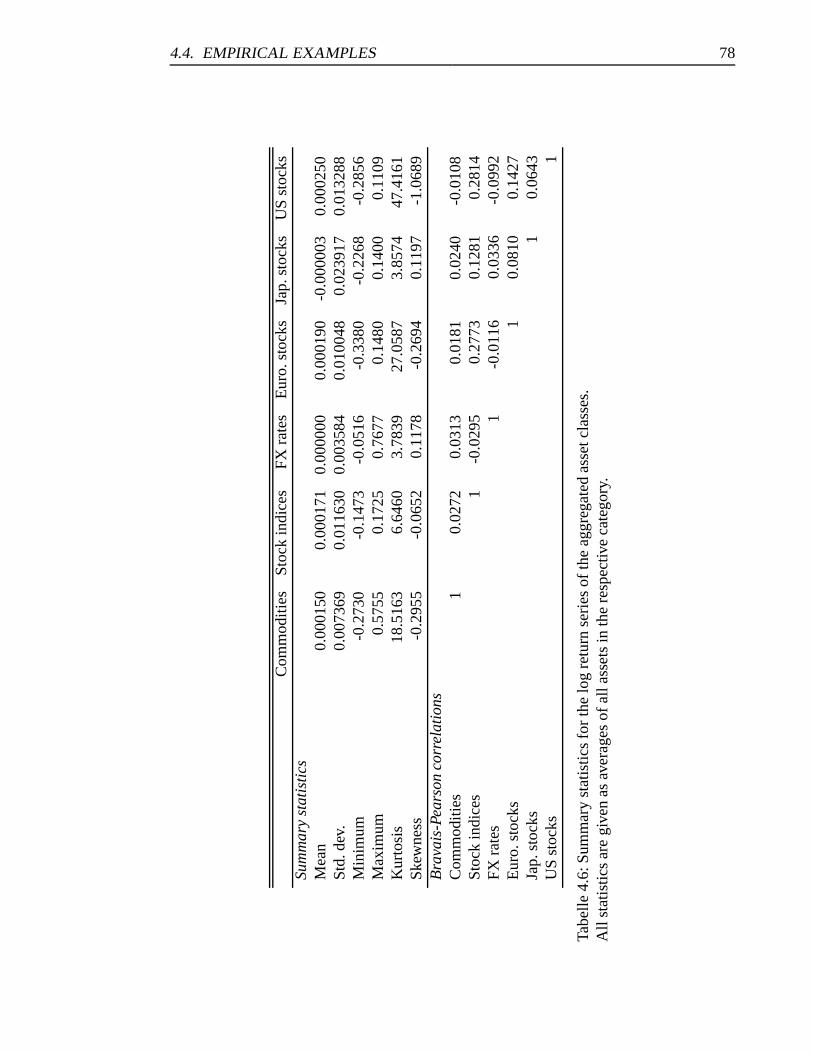

4.6 Summary statistics for the log return series of the aggregated asset classes. 78

4.7 Results for the VaR and ES-estimations averaged over all 100 bivariate

portfolios. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

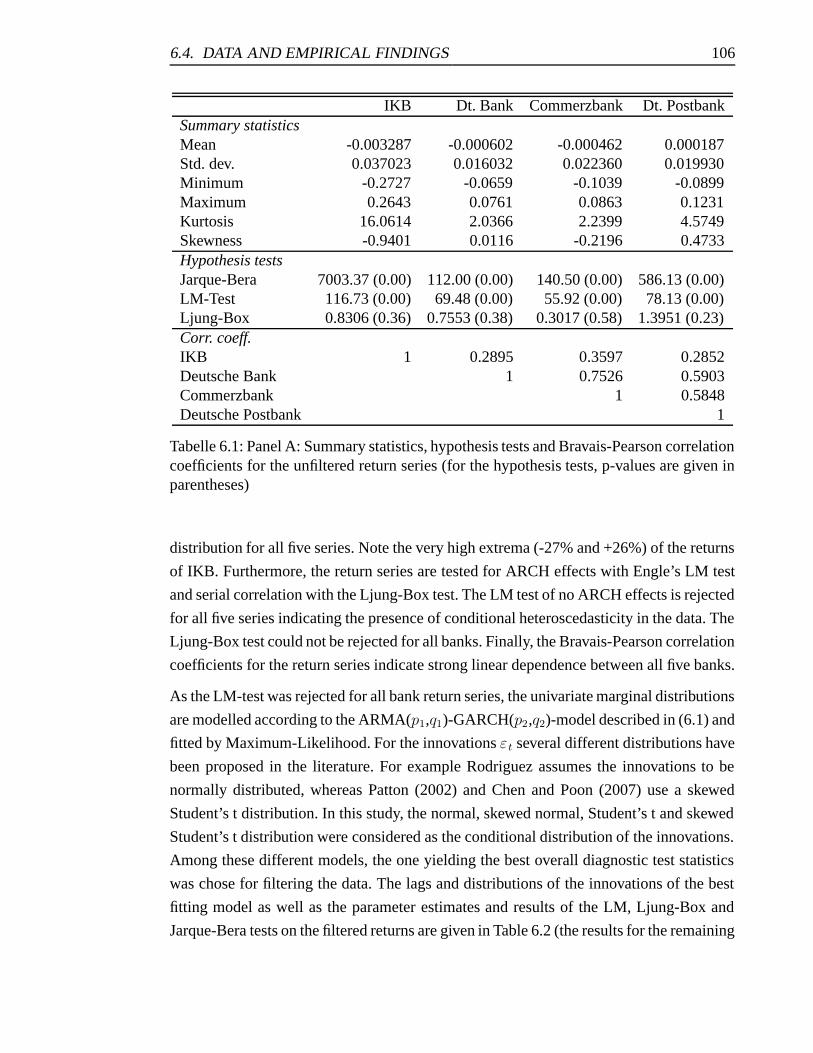

6.1 Panel A: Summary statistics, hypothesis tests and Bravais-Pearson corre-

lation coefficients for the unfiltered return series . . . . . . . . . . . . . . 106

vi

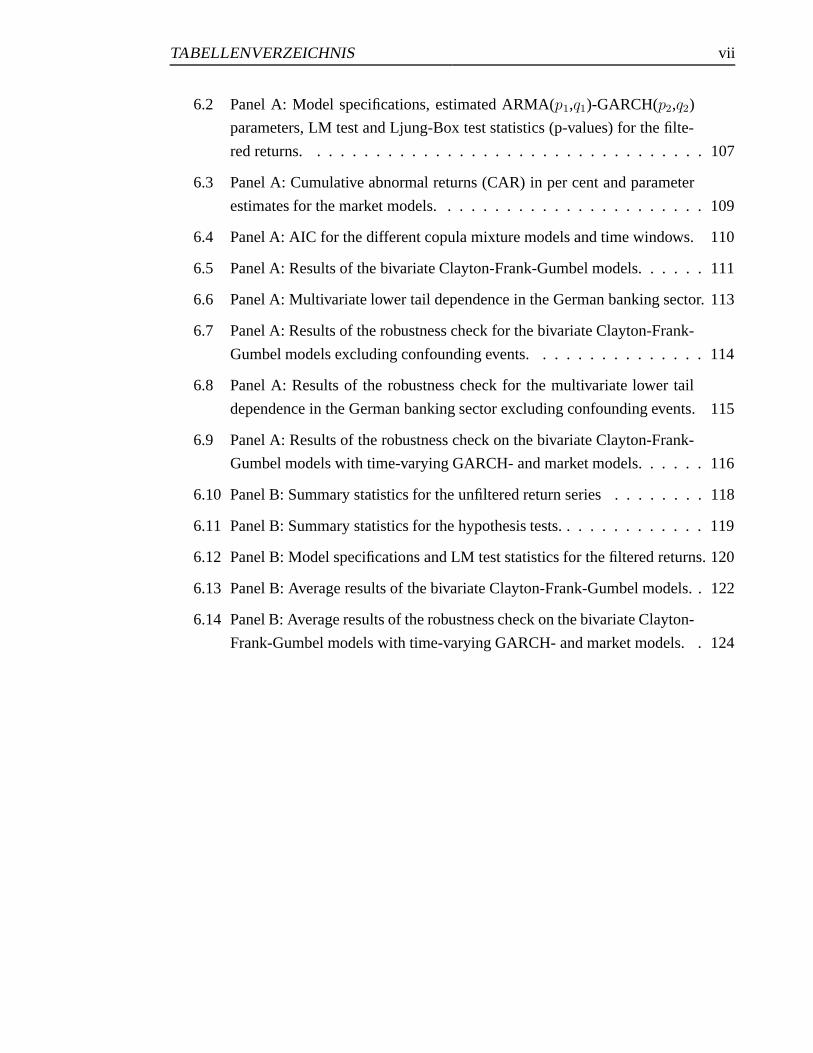

TABELLENVERZEICHNIS vii

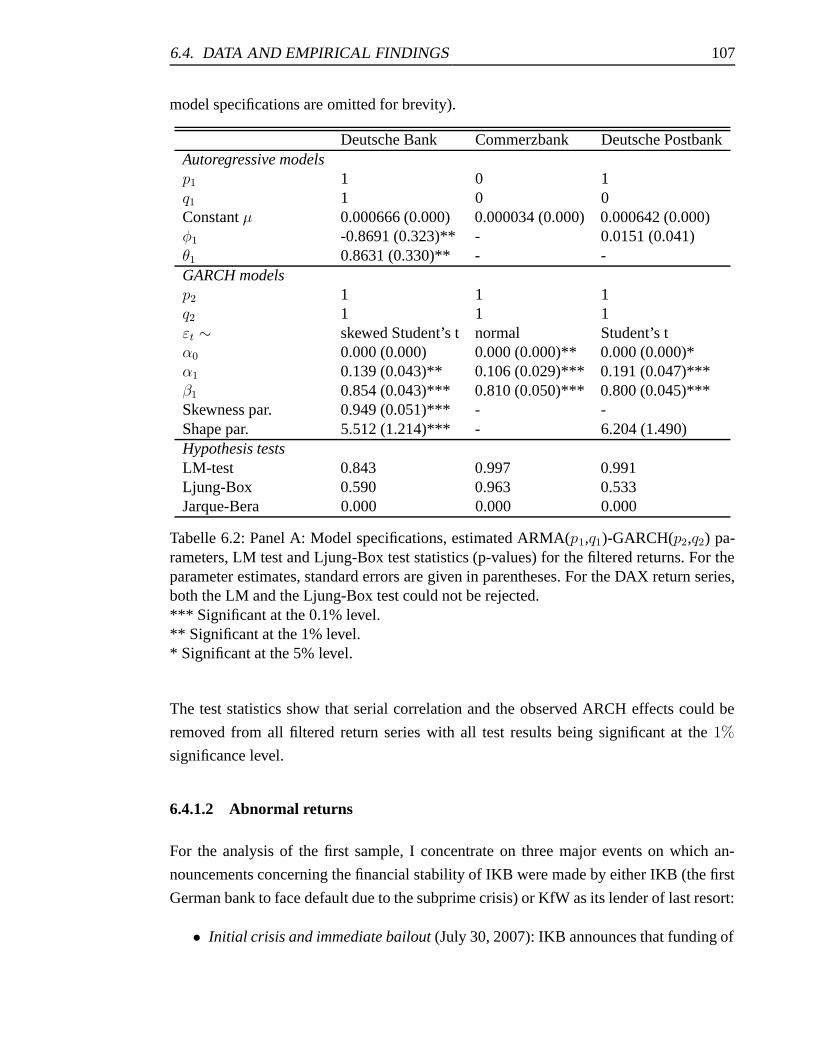

6.2 Panel A: Model specifications, estimated ARMA(p1,q1)-GARCH(p2,q2)

parameters, LM test and Ljung-Box test statistics (p-values) for the filte-

red returns. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

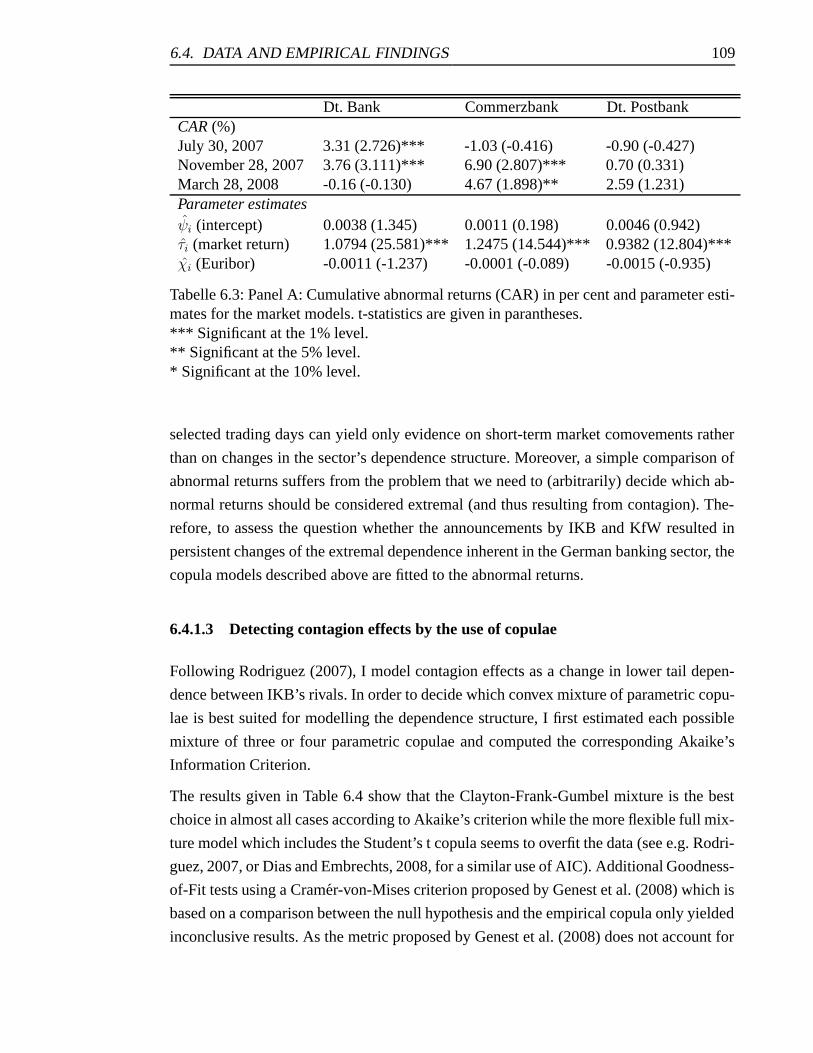

6.3 Panel A: Cumulative abnormal returns (CAR) in per cent and parameter

estimates for the market models. . . . . . . . . . . . . . . . . . . . . . . 109

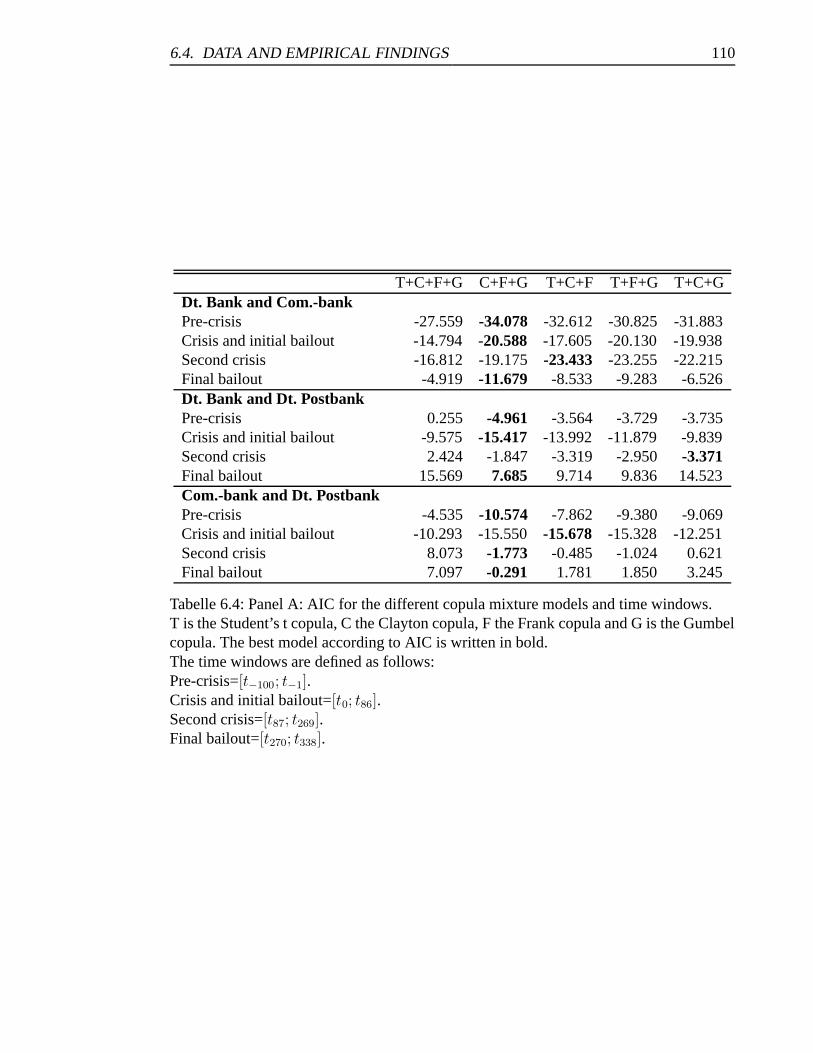

6.4 Panel A: AIC for the different copula mixture models and time windows. 110

6.5 Panel A: Results of the bivariate Clayton-Frank-Gumbel models. . . . . . 111

6.6 Panel A: Multivariate lower tail dependence in the German banking sector. 113

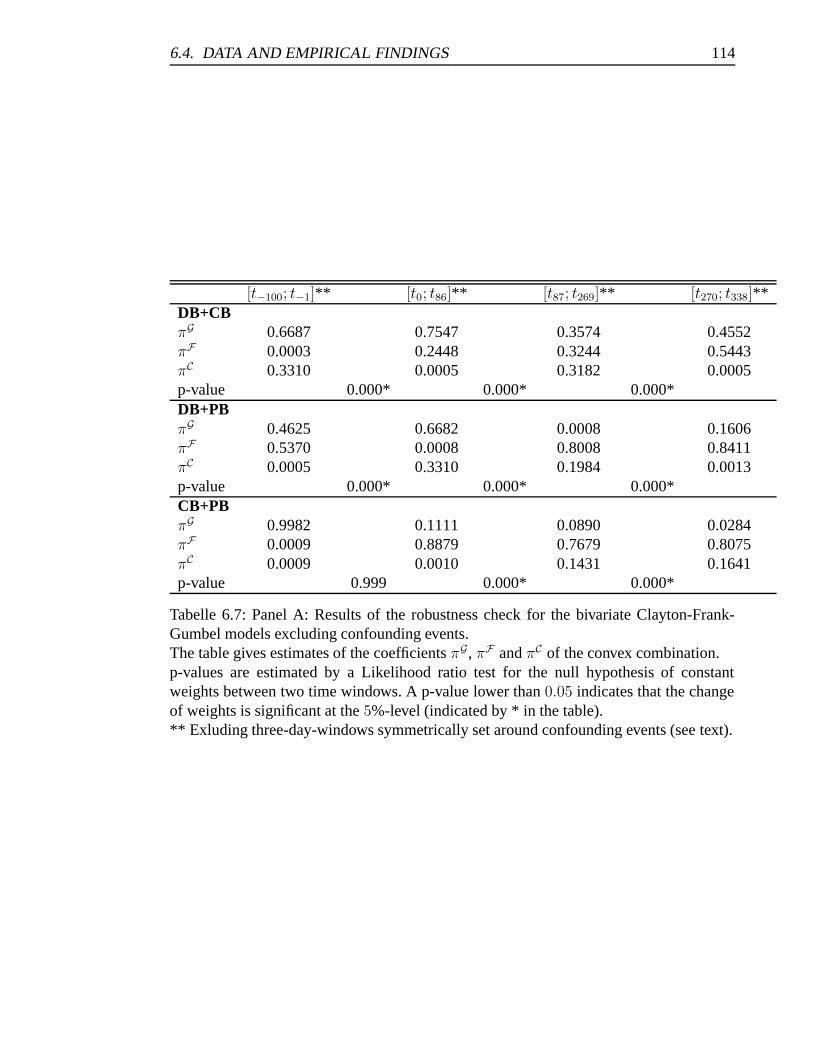

6.7 Panel A: Results of the robustness check for the bivariate Clayton-Frank-

Gumbel models excluding confounding events. . . . . . . . . . . . . . . 114

6.8 Panel A: Results of the robustness check for the multivariate lower tail

dependence in the German banking sector excluding confounding events. 115

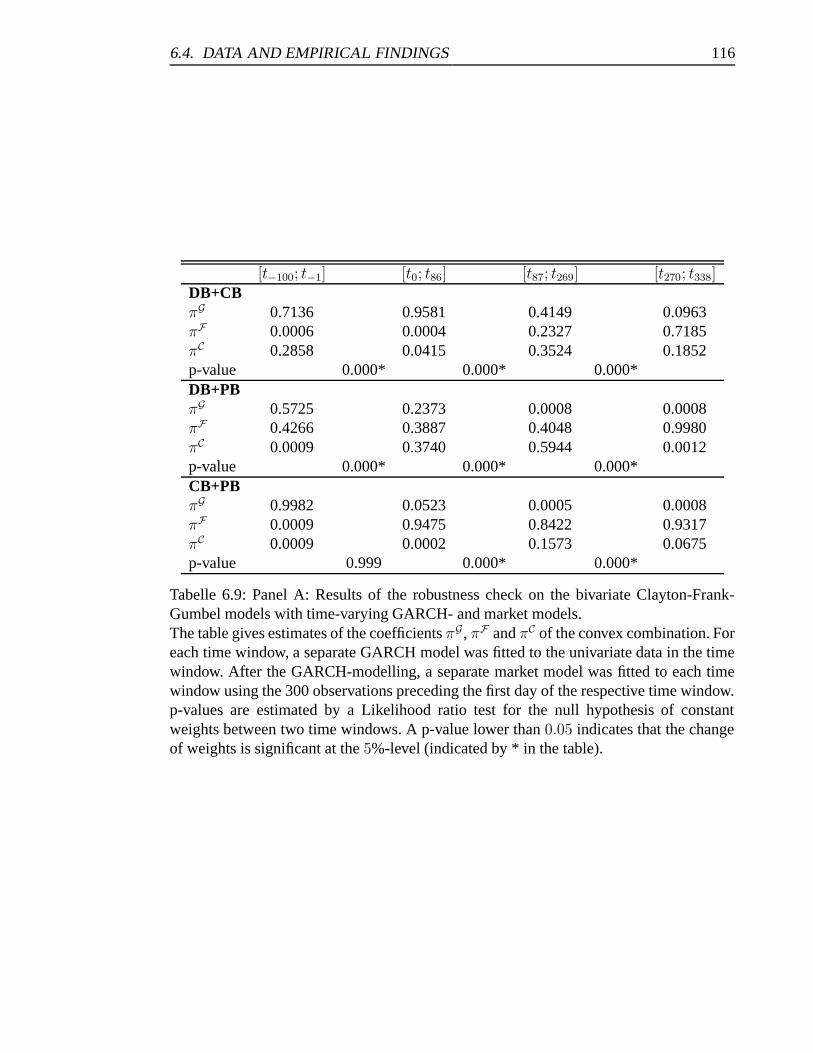

6.9 Panel A: Results of the robustness check on the bivariate Clayton-Frank-

Gumbel models with time-varying GARCH- and market models. . . . . . 116

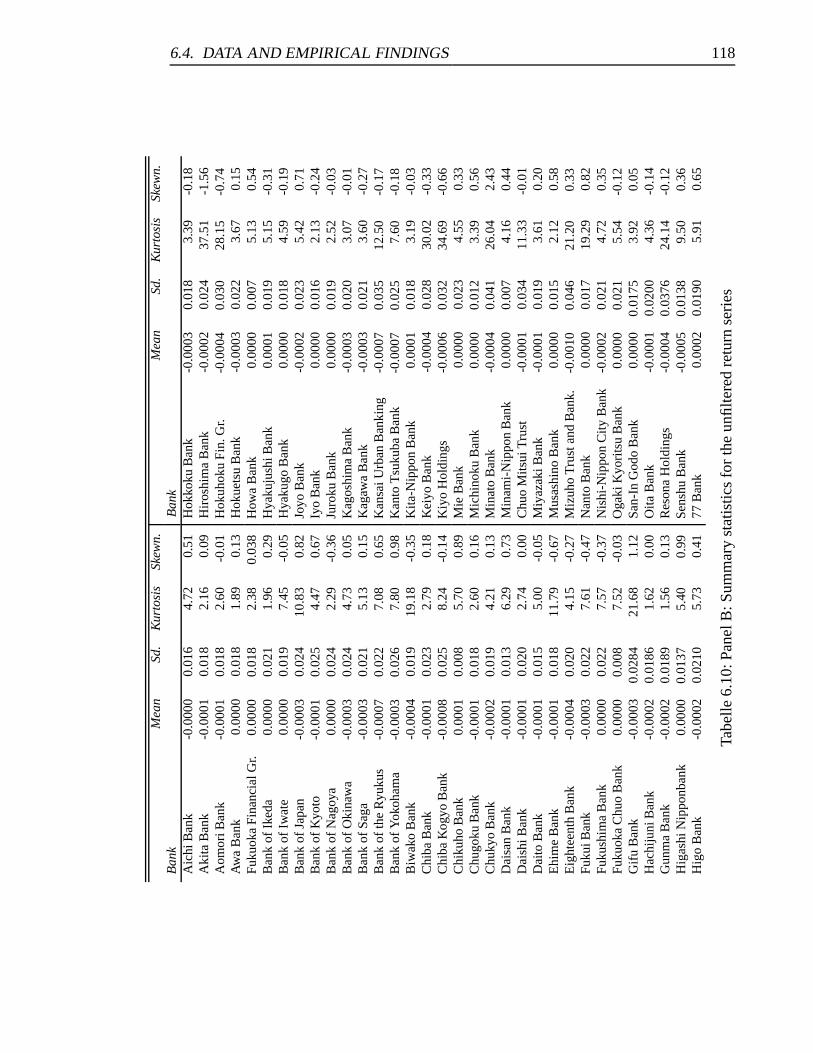

6.10 Panel B: Summary statistics for the unfiltered return series . . . . . . . . 118

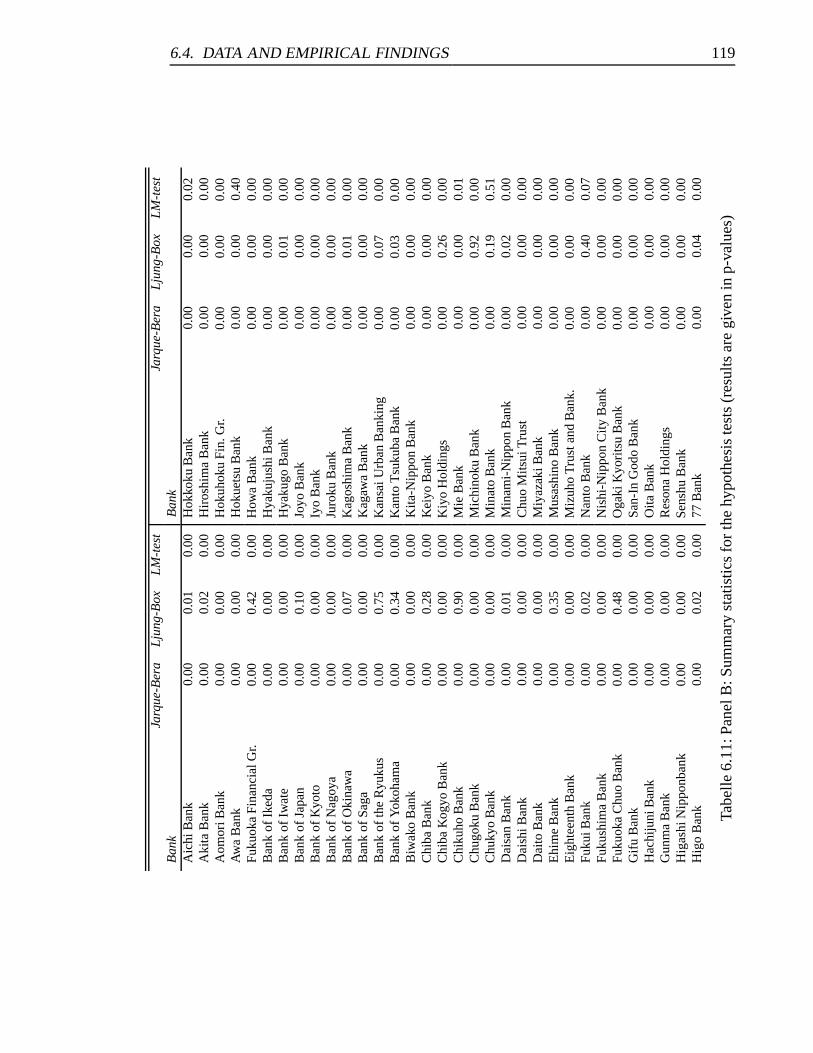

6.11 Panel B: Summary statistics for the hypothesis tests. . . . . . . . . . . . . 119

6.12 Panel B: Model specifications and LM test statistics for the filtered returns. 120

6.13 Panel B: Average results of the bivariate Clayton-Frank-Gumbel models. . 122

6.14 Panel B: Average results of the robustness check on the bivariate Clayton-

Frank-Gumbel models with time-varying GARCH- and market models. . 124

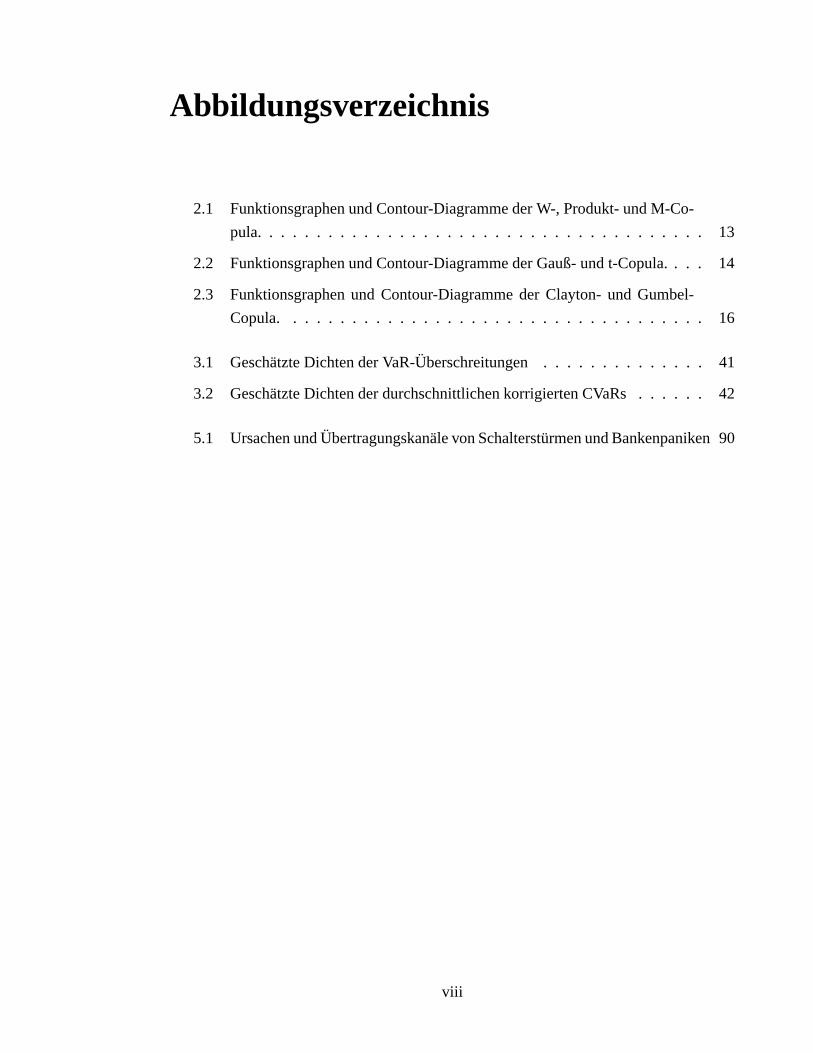

Abbildungsverzeichnis

2.1 Funktionsgraphen und Contour-Diagramme der W-, Produkt- und M-Co-

pula. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.2 Funktionsgraphen und Contour-Diagramme der Gauß- und t-Copula. . . . 14

2.3 Funktionsgraphen und Contour-Diagramme der Clayton- und Gumbel-

Copula. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1 Geschatzte Dichten der VaR-Uberschreitungen . . . . . . . . . . . . . . 41

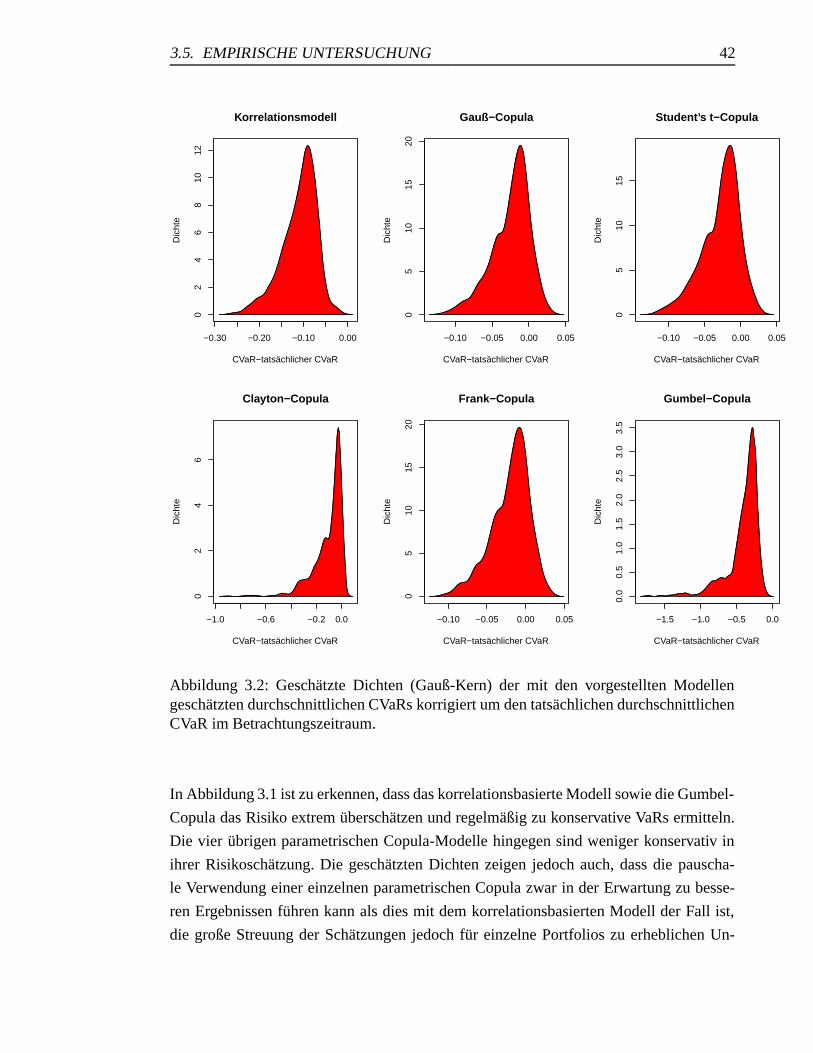

3.2 Geschatzte Dichten der durchschnittlichen korrigierten CVaRs . . . . . . 42

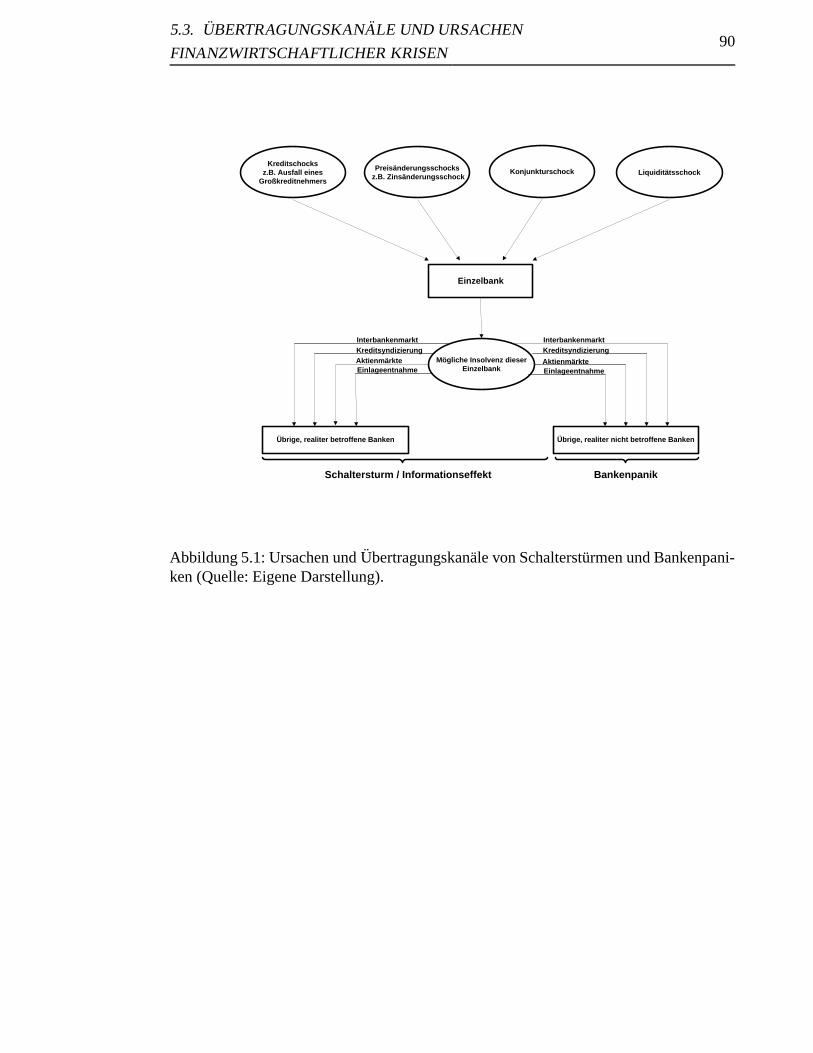

5.1 Ursachen und Ubertragungskanale von Schaltersturmen und Bankenpaniken 90

viii

Kapitel 1

Einleitung

1.1 Einfuhrung in die Thematik und Motivation

Im Zentrum des Interesses zahlreicher Fragestellungen der Finanzmarkttheorie sowie der

angewandten Statistik stehen die Modellierung und Analyse der einem Zufallsvektor zu-

geordneten gemeinsamen Verteilung. Diese fasst sowohl das Randverhalten als auch die

zwischen den Zufallsvariablen bestehenden Abhangigkeiten in einer Funktion in mehre-

ren Variablen zusammen. Die ubliche Herangehensweise fur die Modellierung der ge-

meinsamen Verteilung eines Zufallsvektors bestand dabei klassischerweise darin, Vertei-

lungsannahmen fur die Rander zu treffen, fur die die gemeinsame Verteilung leicht analy-

tisch bestimmt werden konnte. So fanden (und finden) insbesondere multivariate Normal-,

Log-Normal-, Gamma- und Extremwertverteilungen haufig Anwendung in den Modellen

der Finanz- und Versicherungsmathematik. Der großte Nachteil dieser Herangehensweise

ist jedoch, dass die Annahme einer bestimmten, leicht modellierbaren gemeinsamen Ver-

teilung die Verteilung der univariaten Rander des Zufallsvektors vorgibt. Im Endeffekt

konnen somit das univariate Randverhalten und die Abhangigkeitsstruktur eines Zufalls-

vektors nicht separat voneinander modelliert werden.

Trotz dieser Einschrankung basieren zahlreiche Modelle der klassischen Kapitalmarkt-

theorie aber auch des zeitgenossischen quantitativen Risikomanagements auf diesem An-

satz und unterstellen bspw. fur die gemeinsame Verteilung von Risikoportfeuilles ei-

ne multivariate Normalverteilung.1 Die Annahme normalverteilter Risiken und der da-

mit verbundenen Gleichsetzung von stochastischer Abhangigkeit und linearer Korrela-

tion kann jedoch in praxisrelevanten Fallen zur Fehlspezifikation statistischer Modelle

fuhren. Embrechts et al. schlugen daher bereits 2002 einen alternativen Weg zur Model-

lierung multivariater Verteilungen vor, in dem die eigentliche Modellierung in zwei Teile

aufgespaltet wird: die Modellierung der univariaten Randverteilungen und der separaten

1Vgl. z.B. Markowitz (1952) und Jorion (2006).

1

1.1. EINFUHRUNG IN DIE THEMATIK UND MOTIVATION 2

Modellierung der Abhangigkeitsstruktur zwischen den Randverteilungen.2 Wahrend fur

die Modellierung der Randverteilungen klassische univariate parametrische und nicht-

parametrische Verteilungen herangezogen werden konnen, kann die Modellierung der

Abhangigkeitsstruktur durch spezielle Verteilungsfunktionen, den sogenannten Copulas,

erfolgen.

Copulas stellen vereinfacht gesprochen Verteilungsfunktionen dar, die die in einer ge-

meinsamen Verteilung inharente Abhangigkeitsstruktur vollstandig erfassen. Mit ihrer

Hilfe kann die Modellierung einer multivariaten Verteilung so erfolgen, dass zunachst

beliebige parametrische Verteilungen fur die univariaten Rander unterstellt und angepasst

werden, bevor fur die Abhangigkeitsstruktur des Zufallsvektors eine parametrische Co-

pula ausgewahlt wird.3 Der entscheidende Vorteil dieser Vorgehensweise besteht offen-

sichtlich darin, dass die Randverteilungen auf Grund der Aufspaltung des Problems der

Modellierung der gemeinsamen Verteilung nicht mehr aus der gleichen parametrischen

Verteilungsfamilie kommen mussen wie die gemeinsame Verteilung. So konnen bspw.

eine Normal- und eine Gamma-Verteilung mit einer beliebigen parametrischen Copula

kombiniert werden, um so eine multivariate gemeinsame Verteilung zu generieren. Zu-

gleich stellt der zentrale Satz von Sklar sicher, dass aus stetigen Randverteilungen und

einer Copula stets eine eindeutig bestimmte multivariate Verteilung resultiert. Umgekehrt

lasst sich somit aus multivariaten Verteilungen mit bekannten stetigen Randern stets ei-

ne eindeutige Copula extrahieren, die ihrerseits auf andere Randverteilungen angewen-

det werden kann. Die uberaus hohe Flexibilitat dieses Modellierungsansatzes hat dazu

gefuhrt, dass Copula-Modelle gerade im Bereich der Finanz- und Versicherungsmathe-

matik aber auch in anderen Bereichen der angewandten Mathematik sehr an Beliebtheit

gewonnen haben. 4

Wahrend die mathematischen Grundlagen von Copulas vergleichsweise gut erforscht sind,

existieren in der inferentiell-statistischen Analyse der Copulas noch zahlreiche ungeloste

Probleme, die ebenfalls eine hohe Praxisrelevanz aufweisen.5 So erfordert die Anwen-

dung eines Copula-Modells auf eine finanzwirtschaftliche Fragestellung grundsatzlich

die Auswahl einer parametrischen Copula aus einer Menge an bekannten Copulas so-

2Vgl. z.B. Embrechts et al. (2002).

3Fur eine grundlegende Einfuhrung in die Copula-Theorie vgl. insb. Nelsen (2006).

4Eine Zusammenfassung unterschiedlicher Anwendungsgebiete im Risikomanagement und der Finan-zierungslehre findet sich z.B. bei Cherubini et al. (2004); eine Vorstellung von Copula-Modellen in derHydrologie findet sich bei Genest und Favre (2007).

5Vgl. hierzu Genest und Favre (2007). Eine Auflistung zahlreicher mathematischer Kritikpunkte findetsich bei Mikosch (2006).

1.1. EINFUHRUNG IN DIE THEMATIK UND MOTIVATION 3

wie die anschließende Schatzung der Copula-Parameter auf der Basis historischer Daten.

Die erste Aufgabe hinsichtlich der Auswahl einer geeigneten parametrischen Copula stellt

zugleich das großte ungeloste Problem dieses Forschungszweiges dar.6 Ohne realistische

Aussicht auf eine analytische Losung dieser Frage sind in der Literatur zwei Ansatze be-

obachtbar, die auf empirischem Weg eine Losung dieser Frage bezwecken: Zum einen

kann die parametrische Copula allein auf Basis von Vermutungen hinsichtlich der ei-

nem Datensatz inharenten Abhangigkeitsstruktur gewahlt werden.7 Zum anderen kann

die Auswahl der Copula auf inferentiell-statistischem Wege uber die Verwendung von

Anpassungstests erfolgen. Gerade zu dem letztgenannten Ansatz sind in den letzten Jah-

ren vermehrt theoretische Abhandlungen8 und Simulationsstudien9 veroffentlicht worden,

in denen spezielle Anpassungstests fur Copulas vorgeschlagen und ihre Teststarke uber-

pruft wurden. Eine empirische Uberprufung der Starke verschiedener Anpassungstests fur

Copulas im Hinblick auf ihre Eignung fur das quantitative Risikomanagement ist indes

bislang noch nicht erfolgt.

Der erste Teil der vorliegenden Dissertation widmet sich daher der Frage, inwiefern spe-

zielle Anpassungstests fur Copulas geeignet sind, die Modellspezifikation mit Blick auf

die Schatzung von Risikomaßen wie dem Value-at-Risk fur ein Risikoportfolio zu ver-

bessern. Genauer gesagt soll auf Basis einer empirischen Untersuchung von 100 Port-

folios bestehend aus Werten des DAX-Indexes die Frage geklart werden, ob mit Hilfe

eines Copula spezifischen Anpassungstests die optimale parametrische Copula ex ante

identifiziert werden kann. Nachdem hierfur in Kapitel 2 eine kurze Einfuhrung in die

Theorie der Copulas gegeben wurde, folgt im auf dem Artikel Uber die Vorteilhaftigkeit

von Copula-GARCH-Modellen im finanzwirtschaftlichen Risikomanagement basierenden

Kapitel 3 die empirische Untersuchung dieser Frage.

Neben der Frage der optimalen Wahl der parametrischen Copula ist jedoch auch die

Frage, welcher Schatzer fur die Copula-Parameter optimal (also unverzerrt und effizi-

ent) ist, von großer praktischer Bedeutung. Aus theoretischer Sicht besitzt der klassi-

sche Maximum-Likelihood-Schatzer (ML) bestimmte Optimalitatseigenschaften, die je-

doch an die Annahme gebunden sind, dass die parametrische Form der Randverteilungen

6Zur herausgehobenen Bedeutung der Frage nach der Auswahl einer parametrischen Copula vgl. Em-brechts (2009) und Genest et al. (2009).

7Ein ahnliches Vorgehen skizziert bspw. Embrechts (2009). Ausschlaggebend fur die Wahl einer be-stimmten parametrischen Copula ist hierbei vor allem die durch die Copula ausgedruckte Randabhangig-keit.

8Vgl. z.B. Fermanian (2005) oder Savu und Trede (2008).

9Vgl. bspw. die Arbeiten von Kole et al. (2007), Genest et al. (2009) und Berg (2009).

1.1. EINFUHRUNG IN DIE THEMATIK UND MOTIVATION 4

richtig gewahlt wurde. Werden die Randverteilungen durch parametrische Verteilungs-

funktionen modelliert, so werden samtliche Parameter der Copula und der Randvertei-

lungen entweder gleichzeitig oder aber nacheinander jeweils uber die Maximierung der

logarithmierten Likelihood der gemeinsamen Verteilung geschatzt. Fur den (praxisnaher-

en) Fall, dass die parametrische Form der Randverteilungen unbekannt ist und damit

moglicherweise im Modell falsch spezifiziert wurde, empfiehlt sich stattdessen eine se-

miparametrische Vorgehensweise, bei der die Rander nichtparametrisch uber die empiri-

schen Verteilungsfunktionen modelliert und anschließend die Copula-Parameter geschatzt

werden.10 Fur diese Vorgehensweise haben Kim et al. gezeigt, dass die semiparametri-

sche Maximum-Likelihood-Schatzung der Copula-Parameter eine bessere Schatzung lie-

fert als der herkommliche ML-Schatzer.11 Gleichzeitig argumentieren die Autoren, dass

Minimum-Distance-Schatzer, die ebenfalls die Parameter auf Basis von Pseudobeobach-

tungswerten schatzen, vergleichbar gute Ergebnisse erzielen sollten. Eine Uberprufung

der statistischen Eigenschaften dieser Schatzer bei endlicher Stichprobengroße sowie ein

Vergleich unterschiedlicher Minimum-Distance-Schatzer fur Copulas findet sich indes

noch nicht in der Literatur.

Im zweiten Teil der Arbeit (Kapitel 4) soll diese Forschungslucke durch die Durchfuhrung

einer umfangreichen Simulationsstudie zum statistischen Verhalten unterschiedlicher Mi-

nimum-Distance-Schatzer fur Copulas geschlossen werden. Genauer gesagt, werden neun

verschiedene Minimum-Distance-Schatzer mit dem semiparametrischen Pseudo-Maxi-

mum-Likelihood-Schatzer fur zwei unterschiedliche Stichprobengroßen hinsichtlich ih-

rer Erwartungstreue, ihrer mittleren Fehlerquadratsumme sowie der von den Schatzern

benotigten Rechenzeit miteinander verglichen. Um die praktische Relevanz der festge-

stellten Unterschiede zu verdeutlichen, werden mit den zehn dargestellten Parameter-

schatzern anschließend der Value-at-Risk sowie der Expected Shortfall fur insgesamt 100

Portfolios unterschiedlicher Anlageklassen berechnet.

Wahrend die ersten Abschnitte der Dissertation die Anwendung von Copula-Funktionen

im quantitativen Risikomanagement betrafen, werden im weiteren Verlauf der Arbeit die

Anwendungsmoglichkeiten dieser Funktionen in der Untersuchung von Ansteckungsef-

fekten und Bankenkrisen untersucht. Hierbei wird die Tatsache genutzt, dass die verschie-

denen parametrischen Copula-Funktionen jeweils eine unterschiedliche Form der Rand-

abhangigkeit aufweisen. Werden nun unterschiedliche parametrische Copula-Funktionen

10Die nichtparametrische Schatzung der Rander ist aquivalent zur Berechnung sogenannter Pseudobeob-achtungswerte mittels Rangtransformation. Vgl. McNeil et al. (2005), S.232.

11Vgl. Kim et al. (2007).

1.1. EINFUHRUNG IN DIE THEMATIK UND MOTIVATION 5

an einen bivariaten Datensatz angepasst, und die parametrische Form identifiziert, die

die beste Anpassung an den Datensatz aufweist, so kann die zwischen zwei Variablen

bestehende Randabhangigkeit bestimmt werden. Im Zeitablauf konnen dann Veranderun-

gen der Randabhangigkeiten in einem Datensatz gemessen werden. Rodriguez wendet als

erster dieses Vorgehen an, um Ansteckungseffekte zwischen Volkswirtschaften (operatio-

nalisiert in Form eines Anstiegs der unteren Randabhangigkeit) in der Mexiko- und der

Asienkrise zu messen.12

Aufbauend auf der Arbeit von Rodriguez widmen sich die letzten beiden Teile der Arbeit

der Messung von Ansteckungseffekten zwischen Banken mithilfe von Copula-Funktio-

nen. Zunachst werden hierfur in Kapitel 5 die fur die folgende Untersuchung elementa-

ren Begriffe des Schaltersturms, der Bankenpanik sowie der finanzwirtschaftlichen An-

steckungseffekte voneinander abgegrenzt. Im letzten Teil der Arbeit (Kapitel 6) wird die

methodische Herangehensweise von Rodriguez entscheidend erweitert. Wahrend Rodri-

guez die Copula-Modellierung auf Basis ungefilterter Daten vornimmt, wird in Kapitel 6

der Copula-Schatzung eine Filterung der Daten mithilfe eines GARCH-Prozesses sowie

mithilfe eines Marktmodells vorgeschaltet. Im Stile einer Ereignisstudie werden schließ-

lich die Ankundigungseffekte wahrend der Anfange der Subprime-Krise in Deutschland

sowie wahrend der japanischen Bankenkrise mithilfe des erweiterten Copula-Modells von

Rodriguez untersucht. Im Gegensatz zu vergleichbaren Studien uber Ansteckungseffek-

te bei Banken werden in dieser Arbeit jedoch nicht nur Ankundigungen im Zusammen-

hang mit den Krisen, sondern auch Ankundigungen von Rettungs- und Stutzungsaktionen

berucksichtigt. Somit stellt der Kapitel 6 zu Grunde liegende Artikel die erste Studie dar,

in der simultan die Veranderungen der Randabhangigkeiten in einem Bankensektor auf

Grund von Ansteckungseffekten und Stutzungsmaßnahmen des Staates untersucht wer-

den.

Nachfolgend werden die einzelnen Beitrage zur vorliegenden kumulativen Dissertation

kurz skizziert.

12Vgl. Rodriguez (2007).

1.2. ZUSAMMENFASSUNG UND PUBLIKATIONSDETAILS 6

1.2 Zusammenfassung und Publikationsdetails

Die vorliegende kumulative Dissertation besteht aus dieser Einleitung und insgesamt funf

in sich abgeschlossenen Beitragen zum Einsatz von Copula-Funktionen im quantitativen

Risikomanagement und in der Untersuchung von Bankenkrisen. Nachfolgend werden die

Inhalte der einzelnen Beitrage zusammengefasst sowie die Details der Veroffentlichung

und Prasentation auf internationalen Konferenzen erlautert.

Beitrag I: Copula-Funktionen.

Autoren: Gregor Weiß und Philipp Sczesny

Zusammenfassung: Im ersten Kurzbeitrag werden die Grundlagen der Copula-Theorie so-

wie die wichtigsten parametrischen Copula-Funktionen vorgestellt. Der Schwerpunkt des

Beitrags liegt dabei auf der Erlauterung elementarer Copulas sowie der grafischen Dar-

stellung elliptischer und archimedischer Copulas. Im Anschluss an die formale Erlaute-

rung der wichtigsten Copula-Funktionen sowie ihrer Eigenschaften werden die prinzi-

piell moglichen Anwendungsgebiete im quantitativen Risikomanagement skizziert. Der

Beitrag wurde zu gleichen Teilen von beiden Autoren verfasst.

Stichworter: Copula-Funktionen; Einfuhrung; mathematische Grundlagen; Elementar-Co-

pulas.

Publikationsdetails: Veroffentlicht in: Die Betriebswirtschaft, 68. Jg. (2008), S. 621-626.

Beitrag II: Uber die Vorteilhaftigkeit von Copula-GARCH-Modellen im finanzwirt-

schaftlichen Risikomanagement.

Autor: Gregor Weiß

Zusammenfassung: Im Rahmen des vorliegenden Beitrags wird zunachst der Aufbau ei-

nes Copula-GARCH-Modells zur Schatzung des Gesamtrisikos eines Aktienportfolios

erlautert. In der empirischen Studie wird der Value-at-Risk und Conditional-Value-at-

Risk fur insgesamt 800 bivariate Portfolios, bestehend aus verschiedenen im DAX no-

tierten Aktien, berechnet. Die durchgefuhrten Simulationen zeigen, dass das vorgestellte

Copula-GARCH-Modell in fast jeder zweiten Simulation bessere VaR-Schatzungen und

in fast 80% aller Simulationen bessere CVaR-Schatzungen erzielen kann als ein traditio-

nelles korrelationsbasiertes Modell, falls die parametrische Funktionalform der Copula

1.2. ZUSAMMENFASSUNG UND PUBLIKATIONSDETAILS 7

richtig gewahlt wird. Dieses erste zentrale Ergebnis ist zudem relativ robust gegenuber

einer Veranderung des Schatzzeitraumes. Wahrend fur die VaR-Berechnungen die Wahl

der parametrischen Copula nicht pauschal getroffen werden konnte, lieferte die Frank-

Copula fur uber 80% der betrachteten Portfolios signifikant bessere CVaR-Schatzungen

als das Korrelationsmodell. Der in diesem Beitrag verwendete, auf der empirischen Co-

pula basierende Anpassungstest erwies sich jedoch sowohl fur die VaR- als auch CVaR-

Schatzung als vergleichsweise schwach in seiner Fahigkeit zur Wahl des optimalen Mo-

dells. In fast allen Fallen lieferte der GoF-Test entweder eine mehrdeutige oder sogar eine

falsche Empfehlung.

Stichworter: Abhangigkeitsstrukturen; Risikomanagement; Copulas; Anpassungstests.

Publikationsdetails: Zur Veroffentlichung eingereicht in: Kredit und Kapital. Eine engli-

sche Fassung des Artikels wurde auf den folgenden Konferenzen mit verdecktem Begut-

achtungsverfahren angenommen bzw. bereits prasentiert:

• 13th International Congress on Insurance: Mathematics and Economics 2009, Istan-

bul, 27.-29. Mai.

• 6th International Congress on Computational Management Science 2009, Genf, 1.-

3. Mai.

• 22nd Australasian Banking and Finance Conference 2009, University of New South

Wales (Sydney) und Journal of Banking & Finance, 16.-18. Dezember.

Beitrag III: Copula Parameter Estimation - Numerical Considerations And Impli-

cations For Risk Management.

Autor: Gregor Weiß

Zusammenfassung: Ziel dieses Beitrages ist es, die Ergebnisse einer umfangreichen Si-

mulationsstudie zu den statischen Eigenschaften unterschiedlicher Minimum-Distance-

und Maximum-Likelihood-Schatzer fur bi- und multivariate Copula-Funktionen bei Ver-

wendung endlicher Stichproben zu prasentieren. Der klassische Pseudo-Maximum-Like-

lihood-Schatzer wird dabei mit neun verschiedenen Minimum-Distance-Schatzern fur

funf verschiedene parametrische Copulas verglichen. Die Minimum-Distance-Schatzer

basieren auf gangigen Anpassungstests fur Copula-Funktionen, die wiederum auf der

empirischen Copula-Funktion, Kendalls bzw. Rosenblatts Wahrscheinlichkeits-Integral-

transformation aufsetzen.

1.2. ZUSAMMENFASSUNG UND PUBLIKATIONSDETAILS 8

Außerdem werden die Ergebnisse der ersten Simulationsstudie um die Diskussion eines

empirischen Anwendungsfalls erweitert. Die Ergebnisse beider Studien zeigen, dass der

Pseudo-Maximum-Likelihood-Schatzer in fast allen Simulationslaufen erheblich weni-

ger verzerrte Schatzwerte fur die Copula-Parameter liefert als jeder andere Minimum-

Distance-Schatzer. Gleichzeitig benotigt der ML-Schatzer weniger Rechenzeit als die

ubrigen Schatzer, so dass dieser eindeutig vorzuziehen ist. In wenigen Ausnahmefallen

(insbesondere wenn die Stichprobengroße ansteigt) konnten die Minimum-Distance-Schat-

zer auf Basis der empirischen Copula-Funktion die Schatzwerte des ML-Schatzers ver-

bessern. Hingegen sollten die auf Kendalls Integraltransformation basierenden Minimum-

Distance-Schatzer nicht verwendet werden, da sie stark verzerrte Schatzungen liefern und

erheblich mehr Rechenzeit benotigen als die ubrigen Schatzer. Diese zentralen Befunde

werden im empirischen Anwendungsfall bestatigt. Zudem zeigt sich, dass die festgestell-

ten Schatzfehler der einzelnen Schatzer erheblichen Einfluss auf die Berechnung unter-

schiedlicher Risikomaße mithilfe von Copula-Funktionen haben konnen.

Stichworter: Copulas; Minimum-Distance-Schatzmethode; Simulationsstudie; L1-Vari-

ante; Maximum Likelihood.

Publikationsdetails: Zur Veroffentlichung eingereicht in: Journal of Risk. Dort Aufforde-

rung zur Uberarbeitung des Manuskripts und Wiedereinreichung (revise and resubmit).

Der Artikel wurde auf den folgenden Konferenzen mit verdecktem Begutachtungsverfah-

ren prasentiert:

• Workshop Finance and Insurance 2009, FSU Jena, 15.-20. Marz.

• 13th International Congress on Insurance: Mathematics and Economics 2009, Istan-

bul, 27.-29. Mai.

Beitrag IV: Bank-Contagion.

Autor: Gregor Weiß

Zusammenfassung: Ziel dieses Beitrages ist es, zunachst den Begriff der bank contagion

zu definieren und die Unterschiede zum verwandten Begriff der financial contagion auf-

zuzeigen. Zudem sollen konkrete Unterformen der bank contagion wie z.B. dem Schal-

tersturm oder der Bankenpanik erlautert werden. Anschließend sollen die verschiedenen

Ubertragungskanale einer finanzwirtschaftlichen Ansteckung skizziert sowie die Auswir-

kungen der bank contagion dargestellt werden.

1.2. ZUSAMMENFASSUNG UND PUBLIKATIONSDETAILS 9

Stichworter: Bank contagion; Schaltersturm; Ansteckungseffekte; Bankenpanik.

Publikationsdetails: Veroffentlicht in: Die Betriebswirtschaft, 69. Jg. (2009), S. 521-524.

Beitrag V: Analysing Bank Contagion with Copulæ - Evidence from the Subprime

and Japan’s banking crises.

Autor: Gregor Weiß

Zusammenfassung: Im Rahmen dieses Beitrages wird eine neue methodische Herange-

hensweise zur Untersuchung von Ansteckungseffekten zwischen Banken vorgeschlagen.

Diese neue Methodik vereint Elemente einer Ereignisstudie mit Elementen der Copula-

Theorie, um Ansteckungseffekte als Veranderungen der unteren Randabhangigkeit zwi-

schen den Aktienrenditen zweier Institute eines Bankensektors messen zu konnen. Zudem

stellt dieser Beitrag die erste Studie dar, in der Veranderungen der Randabhangigkeit von

Banken um Ankundigungen von Stutzungsmaßnahmen des Staates herum gemessen wer-

den.

Die Ergebnisse der beiden empirischen Untersuchungen zeigen, dass signifikante An-

steckungseffekte sowohl im deutschen Bankensektor wahrend der Subprime-Krise, als

auch im japanischen Bankensektor wahrend der 90er Jahre feststellbar waren. Insbeson-

dere kann gezeigt werden, dass negative Ankundigungen von Banken (z.B. einer bevorste-

henden Insolvenz) zu signifikanten Anstiegen der unteren Randabhangigkeit in den Ban-

kensektoren fuhren. Gleichzeitig fuhren Rettungs- und Stutzungsmaßnahmen des Staates

zu einer Verringerung der unteren Randabhangigkeit bei einer gleichzeitigen Erhohung

der Randunabhangigkeit. Dies zeigt, dass die Rettungsmaßnahmen des Staates geeignet

waren, Ansteckungseffekte zu verringern ohne dabei gleichzeitig die Wahrscheinlichkeit

eines simultanen Booms der Aktienkurse zu erhohen.

Stichworter: Contagion Effects; Bailout; Tail Dependence; Copula.

Publikationsdetails: Zur Veroffentlichung angenommen in: Journal of Economics and Fi-

nance. Der Artikel wurde auf den folgenden Konferenzen mit verdecktem Begutachtungs-

verfahren prasentiert:

• Campus for Finance Research Conference 2009, WHU Koblenz, 14./15. Januar.

• European Financial Management Symposium on Risk Management in Financial

Institutions 2009, Audencia School of Management Nantes, 23.-25. April.

Kapitel 2

Copula-Funktionen

Veroffentlicht in:

Die Betriebswirtschaft, 68. Jg. (2008), S. 621-626 (zusammen mit Philipp Sczesny).

2.1 Einleitung

In vielen Bereichen der Wirtschaftswissenschaften besteht ein Interesse an der Bestim-

mung einer gemeinsamen multivariaten Zufallsverteilung auf der Basis einer gegebenen

Menge von eindimensionalen Randverteilungen. Ein Beispiel hierfur ist die Quantifizie-

rung des Gesamtbankrisikos im Rahmen eines ganzheitlichen Risikomanagements einer

Bank. Dieses Gesamtrisiko setzt sich zusammen aus den einzelnen Risikopositionen einer

Bank unter Berucksichtigung von Abhangigkeiten zwischen den eingegangenen Positio-

nen. Erst eine Quantifizierung der Einzelrisiken ermoglicht es, die Hohe des Gesamt-

bankrisikos (bspw. durch die Berechnung eines quantil-basierten Risikomaßes wie dem

Value-at-Risk bzw. dem wegen seiner Koharenz vorzuziehenden Conditional-Value-at-

Risk) naherungsweise zu messen und somit zu steuern.

Im Zusammenhang mit der Bestimmung der gemeinsamen Verteilung eines Zufallsvek-

tors wird in der Literatur verstarkt der Einsatz sogenannter Copula-Funktionen diskutiert.

Mithilfe dieser Funktionen kann die, einer multivariaten Verteilung inharente, Abhangig-

keitsstruktur getrennt von der Bestimmung der Randverteilungen modelliert werden. Da-

neben weisen Copula-Funktionen den Vorteil auf, dass mit ihnen die komplette Abhangig-

keitsstruktur einer multivariaten Verteilung beschrieben werden kann. Somit erweitern sie

die bisher im Risikomanagement vorherrschenden korrelationsbasierten Abhangigkeits-

modelle, die ausschließlich beim Vorliegen elliptischer Verteilungen (z.B. der Normal-

verteilung) adaquat sind (vgl. McNeil/Frey/Embrechts, 2005, S. 201).

10

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 11

2.2 Charakteristika von Copula-Funktionen

Auf Grund der zuvor beschriebenen Moglichkeit zur Modellierung der gesamten stocha-

stischen Abhangigkeitsstruktur zwischen Zufallsvariablen sind Copula-Funktionen (kurz:

Copula bzw. Copulae) verstarkt in den Fokus der Wissenschaft geraten: Im Gegensatz

zu klassischen Abhangigkeitsmaßen wie dem Bravais-Pearson’schen Korrelationskoeffi-

zienten, dem Spearman-Pearson’schen Rangkorrelationskoeffizienten oder Kendalls Tau

konnen mit einer Copula somit auch nichtlineare Abhangigkeiten zwischen zwei oder

mehreren Variablen erfasst werden.

Im Folgenden werden Copulae definiert und wichtige Eigenschaften beschrieben. Der

formal-mathematischen Einleitung folgt eine visuelle Veranschaulichung, die den Zu-

gang zu den Formeln unterstutzen soll. Eine d-dimensionale Copula ist definiert als ei-

ne d-variate Verteilungsfunktion mit gleichverteilten Randverteilungen. Die Bedeutung

von Copula-Funktionen fur die anwendungsorientierte Mathematik wird in dem Satz von

Sklar deutlich, der die besondere Eignung von Copula-Funktionen fur die Modellierung

von Abhangigkeitsstrukturen aufzeigt und gleichzeitig die Existenz einer eindeutigen Co-

pula unter relativ schwachen Bedingungen sichert.

Satz 2.2.1 (Sklar):

Sei F (x1, x2, . . . , xd) die gemeinsame Verteilungsfunktion eines d-variaten Zufallsvektors

(X1, X2, . . . , Xd) mit den Randverteilungen F1(x1), F2(x2), . . . , Fd(xd). Dann gibt es ei-

ne d-dimensionale Copula C, sodass fur alle x ∈ Rd

gilt:

F (x1, x2, . . . , xd) = C(F1(x1), F2(x2), . . . , Fd(xd)). (2.1)

Sind die Randverteilungen F1(x1), F2(x2), . . . , Fd(xd) zudem stetig, so ist die Copula C

eindeutig.

Copulae konnen als funktionale Vorschrift verstanden werden, die zwei oder mehrere ein-

dimensionale Randverteilungen (also bspw. eine Normal- und eine Student-t-Verteilung)

zu einer beliebigen gemeinsamen Verteilung miteinander verknupfen. Sie beschreiben

somit eine eindeutige Form der stochastischen (Un-)Abhangigkeit zwischen mehreren

Zufallsvariablen. Aus der formalen Definition einer Copula als Verteilungsfunktion auf

dem d-dimensionalen Einheitskubus ergeben sich sofort entsprechende analoge Eigen-

schaften. Neben diesen Eigenschaften als Verteilungsfunktion kann jede Copula durch die

sogenannten Frechet-Hoeffding-Schranken nach oben und nach unten abgeschatzt wer-

den, wobei die untere (obere) Schranke als W -Copula (M-Copula) bezeichnet wird:

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 12

W (u1, u2, . . . , ud) ≤ C (u1, u2, . . . , ud) ≤M (u1, u2, . . . , ud)

mit

W (u1, u2, . . . , ud) := max

{1 − d+

d∑i=1

ui; 0

}und

M (u1, u2, . . . , ud) := mini∈{1;...;d}

ui,

wobei ∀i ∈ {i; . . . ; d} : ui ∈ [0; 1] gilt. Diese Schranken stellen außerdem selber Copula-

Funktionen dar (M ist grundsatzlich eine Copula, W nur fur d < 3).

Die einfachste und bekannteste Copula ist die Produkt-Copula Π, mit der die stocha-

stische Unabhangigkeit zwischen Zufallsvariablen modelliert werden kann. Sind die Zu-

fallsvariablenX1, X2, . . . , Xd stochastisch unabhangig mit VerteilungsfunktionenF1(x1),

F2(x2), . . ., Fd(xd), so gilt fur die gemeinsame Verteilung

F (x1, x2, . . . , xd) = Π(F1(x1), F2(x2), . . . , Fd(xd)) = F1(x1) · F2(x2) · . . . · Fd(xd).

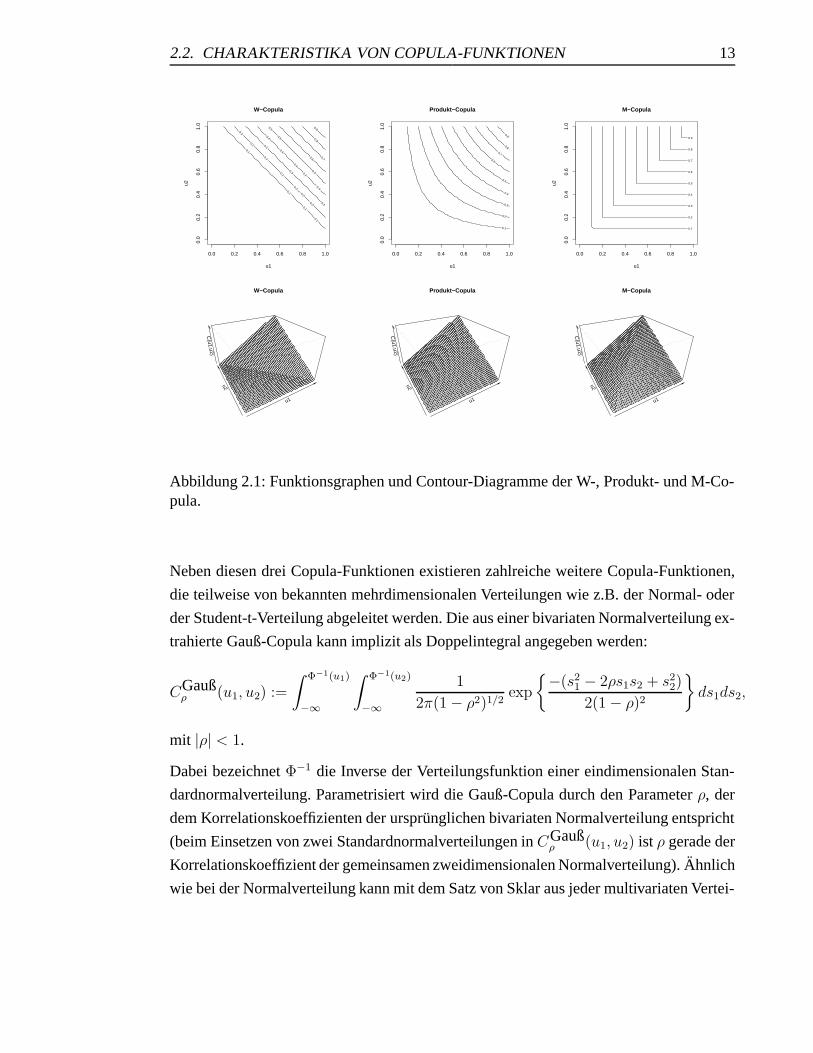

Zum besseren intuitiven Zugriff auf die formal-mathematische Charakterisierung soll an

dieser Stelle die visuelle Darstellung der drei bisher vorgestellten Copula-Funktionen

ermoglicht werden. Die folgende Abbildung 2.1 zeigt die Funktionsgraphen und die dazu-

gehorigen Contour-Diagramme derW -Copula, der Produkt-Copula Π und derM-Copula.

Hierbei sind in den Contour-Diagrammen die Hohenlinien des jeweiligen Funktionsgra-

phen eingezeichnet.

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 13

W−Copula

u1

u2

0.1

0.1

0.1

0.1

0.2

0.2

0.2

0.2

0.2

0.2

0.2

0.3

0.3

0.3

0.4

0.4

0.4

0.4

0.4

0.5

0.5

0.5

0.6 0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

Produkt−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

M−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

u1

u2

C(u1,u2)

W−Copula

u1u2

C(u1,u2)

Produkt−Copula

u1

u2

C(u1,u2)

M−Copula

Abbildung 2.1: Funktionsgraphen und Contour-Diagramme der W-, Produkt- und M-Co-pula.

Neben diesen drei Copula-Funktionen existieren zahlreiche weitere Copula-Funktionen,

die teilweise von bekannten mehrdimensionalen Verteilungen wie z.B. der Normal- oder

der Student-t-Verteilung abgeleitet werden. Die aus einer bivariaten Normalverteilung ex-

trahierte Gauß-Copula kann implizit als Doppelintegral angegeben werden:

CGaußρ (u1, u2) :=

∫ Φ−1(u1)

−∞

∫ Φ−1(u2)

−∞

1

2π(1 − ρ2)1/2exp

{−(s2

1 − 2ρs1s2 + s22)

2(1 − ρ)2

}ds1ds2,

mit |ρ| < 1.

Dabei bezeichnet Φ−1 die Inverse der Verteilungsfunktion einer eindimensionalen Stan-

dardnormalverteilung. Parametrisiert wird die Gauß-Copula durch den Parameter ρ, der

dem Korrelationskoeffizienten der ursprunglichen bivariaten Normalverteilung entspricht

(beim Einsetzen von zwei Standardnormalverteilungen in CGaußρ (u1, u2) ist ρ gerade der

Korrelationskoeffizient der gemeinsamen zweidimensionalen Normalverteilung). Ahnlich

wie bei der Normalverteilung kann mit dem Satz von Sklar aus jeder multivariaten Vertei-

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 14

lung mit stetigen Randverteilungen eine Copula extrahiert werden, so bspw. die t-Copula:

Ctν,P (u1, u2, . . . , ud) := tν,P

[t−1ν (u1), . . . , t

−1ν (ud)

].

Hierbei bezeichnet P eine Korrelationsmatrix, tν die Verteilungsfunktion einer t-Ver-

teilung mit ν Freiheitsgraden und tν,P die gemeinsame Verteilungsfunktion des d-dimen-

sional t-verteilten Zufallsvektors X ∼ td(ν, 0, P ). Da sowohl Gauß- als auch t-Copula

aus sogenannten elliptischen Verteilungen generiert werden, bezeichnet man diese als el-

liptische Copulae (eine Beschreibung der Eigenschaften von elliptischen Verteilungen fin-

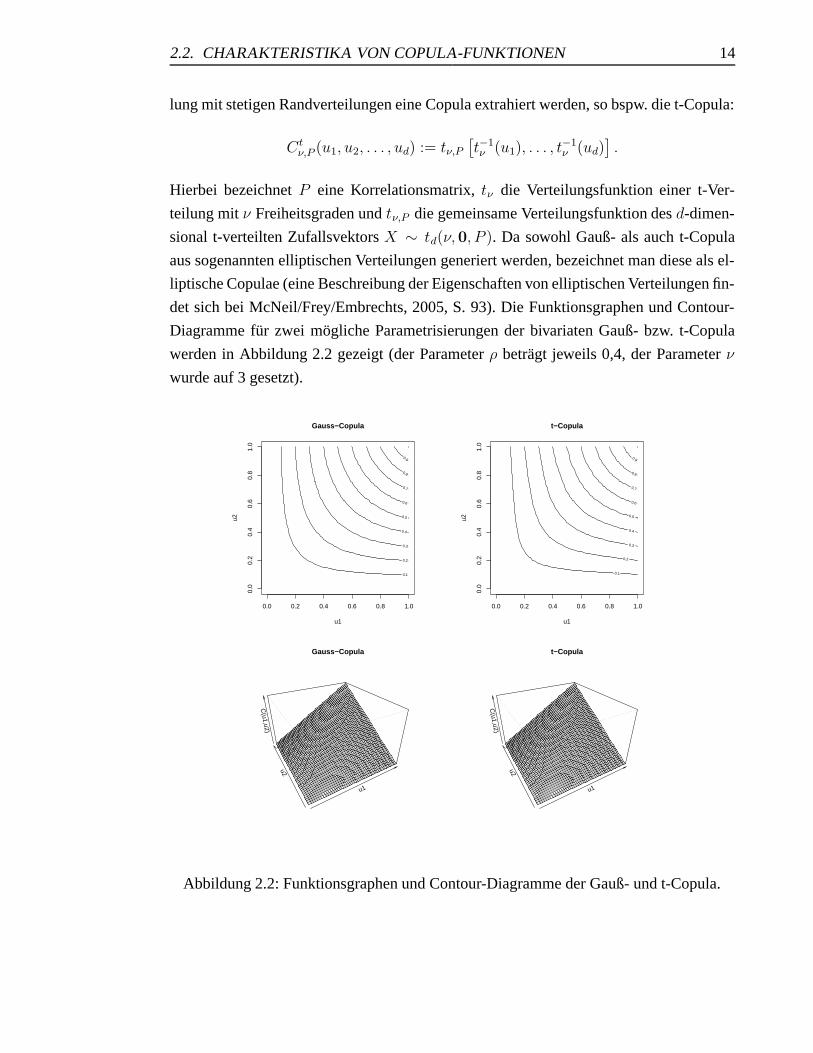

det sich bei McNeil/Frey/Embrechts, 2005, S. 93). Die Funktionsgraphen und Contour-

Diagramme fur zwei mogliche Parametrisierungen der bivariaten Gauß- bzw. t-Copula

werden in Abbildung 2.2 gezeigt (der Parameter ρ betragt jeweils 0,4, der Parameter ν

wurde auf 3 gesetzt).

Gauss−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

t−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

u1

u2

C(u1,u2)

Gauss−Copula

u1

u2

C(u1,u2)

t−Copula

Abbildung 2.2: Funktionsgraphen und Contour-Diagramme der Gauß- und t-Copula.

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 15

Als Beispiele fur Copulae, fur die explizite Definitionsgleichungen existieren, sollen nach-

folgend die Gumbel- und Clayton-Copula definiert werden. Diese gehoren zur Familie der

sogenannten Archimedischen Copula-Funktionen, die sich insbesondere auf Grund der

Moglichkeit der Ineinanderschachtelung mehrerer bivariater archimedischer Copulae fur

den Einsatz in hoheren Dimensionen auszeichnen. Die bivariate Gumbel- und Clayton-

Copula sind definiert als:

CGumbelθ (u1, u2) := exp

{−((− ln u1)

θ + (− ln u2)θ)1/θ},

mit 1 ≤ θ <∞ und

CClaytonθ (u1, u2) :=

(u−θ

1 + u−θ2 − 1

)−1/θ,

mit 0 < θ < ∞. Abbildung 2.3 zeigt die Funktionsgraphen und Contour-Diagramme fur

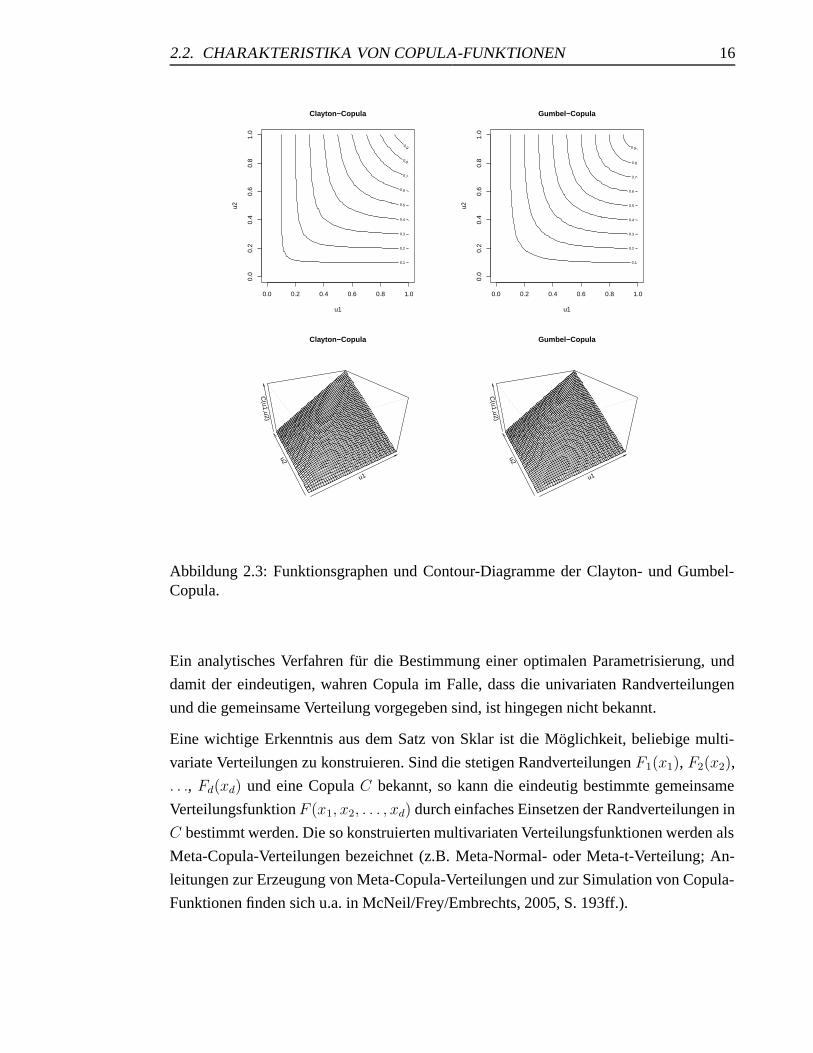

die Clayton- bzw. Gumbel-Copula (θ = 2).

2.2. CHARAKTERISTIKA VON COPULA-FUNKTIONEN 16

Clayton−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

Gumbel−Copula

u1

u2

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

u1

u2

C(u1,u2)

Clayton−Copula

u1

u2

C(u1,u2)

Gumbel−Copula

Abbildung 2.3: Funktionsgraphen und Contour-Diagramme der Clayton- und Gumbel-Copula.

Ein analytisches Verfahren fur die Bestimmung einer optimalen Parametrisierung, und

damit der eindeutigen, wahren Copula im Falle, dass die univariaten Randverteilungen

und die gemeinsame Verteilung vorgegeben sind, ist hingegen nicht bekannt.

Eine wichtige Erkenntnis aus dem Satz von Sklar ist die Moglichkeit, beliebige multi-

variate Verteilungen zu konstruieren. Sind die stetigen Randverteilungen F1(x1), F2(x2),

. . ., Fd(xd) und eine Copula C bekannt, so kann die eindeutig bestimmte gemeinsame

Verteilungsfunktion F (x1, x2, . . . , xd) durch einfaches Einsetzen der Randverteilungen in

C bestimmt werden. Die so konstruierten multivariaten Verteilungsfunktionen werden als

Meta-Copula-Verteilungen bezeichnet (z.B. Meta-Normal- oder Meta-t-Verteilung; An-

leitungen zur Erzeugung von Meta-Copula-Verteilungen und zur Simulation von Copula-

Funktionen finden sich u.a. in McNeil/Frey/Embrechts, 2005, S. 193ff.).

2.3. ANWENDUNGSMOGLICHKEITEN VON COPULA-FUNKTIONEN IM

RISIKOMANAGEMENT17

2.3 Anwendungsmoglichkeiten von Copula-Funktionen im

Risikomanagement

Copula-Funktionen konnen grundsatzlich auf zwei Weisen sinnvoll im Risikomanage-

ment verwendet werden. Die erste Moglichkeit besteht darin, bei Kenntnis der Vertei-

lungen der Einzelrisiken diese mit Hilfe einer bekannten oder aus Vergangenheitswerten

geschatzten Copula zur gemeinsamen (Meta-Copula-)Verteilung zu verknupfen. Hierbei

wird die Copula so gewahlt, dass sie die vermutete Abhangigkeitsstruktur zwischen den

einzelnen Risikopositionen moglichst gut annahert.

Die besondere Bedeutung dieser Modelle fur das Risikomanagement liegt in der Fahig-

keit dieser Modelle, sowohl lineare als auch nichtlineare Abhangigkeiten zwischen den

Risikopositionen abbilden zu konnen. Hierdurch konnen Diversifikationseffekte in der

Bestimmung des Gesamtbankrisikos viel starker berucksichtigt werden, als es bspw. mit

anderen Verfahren wie der Annahme normalverteilter Risiken moglich ware. Mit der so

bestimmten gemeinsamen Verteilung der Gewinne und Verluste kann eine Bank anschlie-

ßend ein (koharentes) quantil-basiertes Risikomaß fur die (diversifizierte) Gesamtbank

bestimmen.

Die zweite Moglichkeit des Einsatzes von Copula-Funktionen im Risikomanagement be-

steht in der Analyse von Abhangigkeitsstrukturen in einem gegebenen Datensatz (vgl.

z.B. Junker/May, 2005). In diesem Fall besteht die Vorgehensweise in der Wahl einer

parametrisierten Copula, deren Parameter aus dem Datensatz heraus geschatzt werden

sollen. Die resultierenden Parameter und die funktionale Form der vollstandig parame-

trisierten Copula konnen dann anschließend hinsichtlich der Frage untersucht werden,

welche Art von Abhangigkeit zwischen den Randverteilungen besteht. Im Risikomanage-

ment werden daher Copula-Funktionen verstarkt eingesetzt, um wiederkehrende Muster

in der Abhangigkeitsstruktur verschiedener Risikoarten (z.B. Marktpreis- oder Kreditrisi-

ken) untereinander zu identifizieren.

Offensichtlich besteht die großte Schwierigkeit bei beiden Vorgehensweisen in der Wahl

der wahren Copula (nach dem Satz von Sklar ist sie unter schwachen Voraussetzungen

eindeutig). Obwohl zahlreiche Klassen von Copula-Funktionen bereits identifiziert wor-

den sind, kann die Mehrzahl dieser Funktionen nicht in geschlossener analytischer Form

angegeben werden. Ebenso kann die Wahl der Parameter der Copula in der Praxis Proble-

me bereiten (bspw. sollte die Gauß-Copula nicht mit der empirischen Korrelationsmatrix,

sondern dem paarweisen Rangkorrelationskoeffizienten nach Spearman kalibriert werden,

2.3. ANWENDUNGSMOGLICHKEITEN VON COPULA-FUNKTIONEN IM

RISIKOMANAGEMENT18

vgl. McNeil/Frey/Embrechts, 2005, S. 230). Empirische Ergebnisse deuten zudem darauf

hin, dass die Wahl einer falschen parametrischen Form der Copula zu erheblichen Feh-

lern bei der anschließenden Berechnung von Quantilen fuhren kann (vgl. Ane/Kharoubi

(2003)). Aus diesem Grund sind in der jungsten Vergangenheit von zahlreichen Autoren

Goodness-of-fit-Tests vorgeschlagen worden, die die Anpassungsgute einer geschatzten

parametrischen Copula durch einen Vergleich mit dem Copula-Analogon zur empirischen

Verteilungsfunktion (der sogenannten Empirischen Copula nach Deheuvels) zu beurteilen

versuchen (vgl. z.B. Kole/Koedijk/Verbeek, 2007; Scaillet, 2007 und Fermanian, 2005).

Kapitel 3

Uber die Vorteilhaftigkeit von

Copula-GARCH-Modellen im

finanzwirtschaftlichen

Risikomanagement

Zur Veroffentlichung eingereicht in:

Kredit und Kapital.

3.1 Einleitung

Das zentrale Anliegen des finanzwirtschaftlichen Risikomanagements besteht in der in-

tegrierten Messung samtlicher Risiken, denen sich ein Finanzinstitut oder Industrieun-

ternehmen ausgesetzt sieht. Eine ganzheitliche Betrachtung unterschiedlicher Risikoarten

bezweckt insbesondere die Berucksichtigung von Diversifikationseffekten zwischen den

verschiedenen Risiken. Im Resultat kann eine Bank durch die adaquate Berucksichtigung

von Diversifikationseffekten das von ihr vorzuhaltende regulatorische Eigenkapital opti-

mieren und somit ihre Eigenkapitalkosten senken.1

In der Vergangenheit basierte diese ganzheitliche, multivariate Modellierung von finanz-

wirtschaftlichen Risiken haufig auf der Berechnung von linearen Korrelationen unter der

Annahme normalverteilter Einzelrisiken. Sowohl fur Marktpreisrisiken als auch insbe-

sondere fur Kreditrisiken ist die Annahme normalverteilter Renditen und Ausfalle jedoch

empirisch nicht haltbar.

1Unter dem”regulatorischen Eigenkapital“ (andere synonyme Bezeichnungen sind

”aufsichtsrechtli-

ches“ oder”haftendes Eigenkapital“) versteht man die Zusammenfassung unterschiedlicher Bilanzpositio-

nen zur Ermittlung der im Insolvenzfall zur Verfugung stehenden Haftmasse. Es setzt sich gemaß §10 KWGund SolvV, ausgehend vom bilanziellen Eigenkapital, aus verschiedenen Kapitalien unterschiedlicher Wer-tigkeit im Insolvenzfall zusammen. Vgl. Hartmann-Wendels/Pfingsten/Weber (2007), S. 391-399.

19

3.1. EINLEITUNG 20

In den vergangenen Jahren sind daher verstarkt Copula-Modelle in den Fokus der For-

schung geraten, die eine Modellierung der gesamten (linearen und nichtlinearen) Ab-

hangigkeitsstruktur eines Zufallsvektors ermoglichen.2 Eine Copula liefert in bestechend

einfacher Form eine Funktionsvorschrift, die hochst unterschiedliche Randverteilungen

miteinander zur zugehorigen gemeinsamen Verteilung verknupft. Somit kann eine Co-

pula fur die Generierung einer multivariaten Verteilung verwendet werden, deren Rand-

verteilungen nicht notwendigerweise identisch sind. Erste Anwendungen haben Copula-

Funktionen aufgrund dieser Eigenschaft insbesondere im Risikomanagement und in der

Versicherungsmathematik gefunden, wo sie zur Generierung der gemeinsamen Verteilung

eines Risikoportfolios verwendet wurden.3 Wichtige Fragestellungen der Implementie-

rung eines auf Copula-Funktionen basierenden Gesamtrisikomodells sind jedoch in der

Wissenschaft noch nicht hinreichend beantwortet. So sind insb. auf die Fragen, welche

parametrische Familie von Copula-Funktionen am besten zur Modellierung bestimmter

Risiken geeignet ist und wie ein hochdimensionales Modell mit 20 oder mehr Risikofak-

toren effizient geschatzt werden kann, bisher keine zufriedenstellenden Antworten gefun-

den worden.4

Der vorliegende Beitrag verfolgt zwei Ziele: Zum einen soll anhand einer umfangreichen

Simulationsstudie die Vorteilhaftigkeit von Copula-GARCH-Modellen zur Bestimmung

des Value-at-Risks (VaR) bzw. Conditional-Value-at-Risks (CVaR) eines Aktienportfoli-

os gezeigt werden. Zum anderen soll die Frage geklart werden, inwieweit das jeweilige

durch ein Backtesting als optimal identifizierte Copula-GARCH-Modell mithilfe eines

speziellen Anpassungstests im Vorfeld der Value-at-Risk-Prognose hatte ermittelt werden

konnen.

Zu diesem Zweck wird zunachst das notige mathematische Fundament der Theorie der

Copula-Funktionen gelegt. Hierauf aufbauend wird ein Copula-GARCH-Modell zur Be-

stimmung einer gemeinsamen Verlustverteilung erortert, weiterhin werden einige aus

praktischer Sicht besonders relevante Fragen hinsichtlich der Gute und der Stabilitat der

Verfahren zur Schatzung von Copula-Funktionen diskutiert. Durch die Analyse von ins-

gesamt 100 aus im DAX vertretenen Aktien bestehenden Portfolios uber acht verschie-

dene Zeitfenster stellt dieser Beitrag mit 800 Simulationen die bislang umfangreichste

2Vgl. z. B. Embrechts/McNeil/Straumann (2002) fur ein fruhes Beispiel der anwendungsorientiertenBetrachtung von Copula-Funktionen und eine Kritik an korrelationsbasierten Modellen.

3Beispiele hierfur finden sich u. a. bei Junker/May (2005) und Kole/Koedijk/Verbeek (2007).

4Eine”einfache“ Losung dieser Fragen wird aller Voraussicht nach auch nie gefunden werden, vgl. Em-

brechts (2009). Losungsansatze insb. zum erstgenannten Problem finden sich in den Arbeiten von Genest,vgl. z. B. Genest/Remillard/Beaudoin (2009).

3.2. LITERATURUBERBLICK UND HYPOTHESENBILDUNG 21

Untersuchung zur Vorteilhaftigkeit von Copula-Risikomodellen dar.

Der Beitrag untergliedert sich in funf Abschnitte. Abschnitt 3.2 beinhaltet einen kurzen

Literaturuberblick und leitet die zu uberprufenden Hypothesen ab. Abschnitt 3.3 erlautert

die univariate Schatzung des Value-at-Risks mithilfe von GARCH-Prozessen. In Ab-

schnitt 3.4 werden Methoden zur Bestimmung des Portfolio-Value-at-Risks vorgestellt.

Abschnitt 3.5 prasentiert die empirische Untersuchung sowie die Ergebnisse. Eine kurze

Zusammenfassung des Beitrags wird in Abschnitt 3.6 gegeben.

3.2 Literaturuberblick und Hypothesenbildung

Seit dem Erscheinen der ersten Arbeiten von Embrechts/McNeil/Straumann5 uber die Ein-

satzmoglichkeiten von Copula-Funktionen im finanzwirtschaftlichen Risikomanagement

sind mehrere Studien erschienen, die die Vorteilhaftigkeit dieser Modelle empirisch uber-

pruft haben.

Eine der ersten empirischen Studien uber die Vorteilhaftigkeit von Copula-Modellen fur

die Modellierung von Abhangigkeitsstrukturen zwischen verschiedenen Anlageformen

stammt von Malevergne/Sornette.6 Die Autoren zeigen fur einen Datensatz, bestehend

aus sechs Wahrungskursen, sechs Commodity-Preisen und 22 an der NYSE notierten Ak-

tienkursen, dass fur die Mehrzahl der innerhalb einer Anlageklasse gebildeten bivariaten

Portfolios die Abhangigkeitsstruktur am besten durch eine Gauß-Copula modelliert wer-

den kann. Gleichzeitig betonen sie, dass die Student’s t-Copula falschlicherweise fur eine

Gauß-Copula gehalten werden kann. Kritisch ist an der Studie von Malevergne/Sornette

jedoch zu sehen, dass diese keine Schatzung von Risikomaßen fur die Portfolios enthalt,

archimedische Copulas nicht berucksichtigt und keine Copula spezifischen Anpassungs-

tests verwendet. Die vermutete pauschale Vorteilhaftigkeit einer einzigen parametrischen

Copula ist jedoch beispielhaft fur die Ergebnisse zahlreicher Arbeiten in den Folgejah-

ren.7 Beispielsweise zeigen Kole/Koedijk/Verbeek fur ein trivariates Portfolio aus Aktien-,

Anleihe- und REITS-Indizes, dass die Abhangigkeitsstruktur dieses Portfolios am besten

durch eine Student’s t-Copula modelliert werden kann.8

Ein ahnliches Resultat hinsichtlich der Wahl der parametrischen Copula finden Di Cle-

5Vgl. Embrechts/McNeil/Straumann (2002).

6Vgl. Malevergne/Sornette (2003).

7Vgl. bspw. die Arbeiten von Fantazzini (2006) und Kole/Koedijk/Verbeek (2007).

8Vgl. Kole/Koedijk/Verbeek (2007).

3.2. LITERATURUBERBLICK UND HYPOTHESENBILDUNG 22

mente/Romano.9 Ihre empirische Untersuchung eines 20-dimensionalen Portfolios ita-

lienischer Aktien zeigt, dass ein kombiniertes Modell aus extremwertverteilten Rand-

verteilungen und einer Gauß- oder Student’s t-Copula erheblich bessere Value-at-Risk-

Schatzungen liefern kann als das klassische korrelationsbasierte Modell. Wiederum wer-

den weder archimedische Copulas noch Anpassungstests oder andere Risikomaße sowie

weitere Portfolios betrachtet.

Junker/May zeigen in ihrer Studie, dass ein Modell mit GARCH-Prozessen als Rand-

verteilungen und einer speziell transformierten Frank-Copula marginal bessere Value-at-

Risk- und Conditional-Value-at-Risk-Schatzungen liefern kann als die Gauß- oder Stu-

dent’s t-Copula.10 Abermals stutzen die Autoren dieses Ergebnis jedoch auf die Un-

tersuchung eines einzelnen bivariaten Portfolios aus Hoechst- und Volkswagen-Aktien

in einem einzigen Betrachtungszeitraum und verwenden ausschließlich allgemeine (Co-

pula unspezifische) Anpassungstests. Ein fast identisches Ergebnis unter ahnlichen Ein-

schrankungen finden Palaro/Hotta, wobei sie fur ein bivariates Portfolio, bestehend aus

dem S&P 500- und dem NASDAQ-Index, die Vorteilhaftigkeit eines Copula-GARCH-

Modells mit symmetrisierter Joe-Clayton-Copula und GARCH-Randverteilungen finden.11

Ebenso zeigt Fantazzini mithilfe einer empirischen Untersuchung von drei bivariaten

Portfolios aus Aktienindizes, dass eine konstante bzw. dynamische Gauß-Copula aus-

reicht, um im Backtesting akzeptable VaR-Schatzungen zu liefern.12

Den genannten Studien ist somit gemein, dass alle Autoren auf Basis weniger Portfolios

eine klare Vorteilhaftigkeit von Copula-Modellen im Vergleich zu korrelationsbasierten

Modellen aufzeigen. Diese unterstellte Vorteilhaftigkeit soll daher auch in dieser Arbeit

zunachst untersucht werden. Bevor jedoch die erste Hypothese formuliert werden kann,

verstandigen wir uns uber die Frage, wann ein Modell als vorteilhaft angesehen werden

kann. Ein Modell X soll in dieser Arbeit als vorteilhafter gegenuber einem zweiten Mo-

dell Y angesehen werden, wenn die hiermit ermittelte Anzahl an VaR-Uberschreitungen

(ExceedModellX) naher an der erwarteten Anzahl an Uberschreitungen (ExceedEmp) liegt

als die des zweiten Modells (ExceedModellY ), ohne die erwartete Anzahl zu uberschreiten.

Die so definierte Vorteilhaftigkeit eines Modells bedeutet, dass das Modell X das Risiko

adaquater darstellt, als dies Modell Y tut, ohne jedoch das vom Investor eingegangene

Risiko zu unterschatzen.

9Vgl. Di Clemente/Romano (2005).

10Vgl. Junker/May (2005).

11Vgl. Palaro/Hotta (2006).

12Vgl. Fantazzini (2006).

3.2. LITERATURUBERBLICK UND HYPOTHESENBILDUNG 23

Aquivalent hierzu betrachten wir ein Modell als optimal fur die Berechnung des CVaRs,

falls der mit diesem Modell berechnete durchschnittliche CVaR im Testzeitraum die Schat-

zungen samtlicher ubriger Modelle verbessert, ohne den tatsachlichen durchschnittlichen

CVaR zu uberschreiten.

Die genannten Studien suggerieren, dass das Rahmenwerk eines Copula-Modells stets

bessere Risikoschatzungen liefert als ein korrelationsbasiertes Modell, solange nur die (ex

ante unbekannte) parametrische Copula-Form richtig gewahlt wird. Die erste Hypothese

lautet somit:

H1: Fur jedes bivariate Portfolio lasst sich in jedem Beobachtungszeitraum stets eine

parametrische Copula-Form finden, sodass das hier vorgeschlagene Copula-GARCH-

Modell eine bessere VaR- und CVaR-Schatzung liefert als das korrelationsbasierte Mo-

dell, also:

ExceedCorr ≤ ExceedCop ≤ ExceedEmp

bzw. fur den Conditional-Value-at-Risk:

CV aRCorr ≤ CV aRCop ≤ CV aREmp.

Betrachtet man insbesondere die Arbeiten von Malevergne/Sornette, Kole/Koedijk/Ver-

beek und Di Clemente/Romano, so erkennt man, dass samtliche Autoren dieser Studien

eine klare Vorteilhaftigkeit elliptischer Copulas als Ergebnis festhalten. Diese auf Basis

kleinerer Datensatze gefundene Optimalitat elliptischer Copulas soll daher im zweiten

Schritt dieser Arbeit untersucht werden, wobei zur Verallgemeinerung der anekdotischen

Evidenz der genannten Studien in dieser Arbeit eine im Vergleich zu bisherigen Arbei-

ten stark erhohte Anzahl an Portfolios verwendet werden soll. Um eine Vergleichbarkeit

mit den genannten Studien erzielen zu konnen, soll zudem zunachst der Einfluss der Wahl

des Risikomaßes sowie des Schatzzeitraumes auf die Risikoschatzungen unberucksichtigt

bleiben.

Die zweite Hypothese lautet dann:

H2: Die Gauß- und/oder Student’s t-Copula liefern/liefert unabhangig vom betrachteten

Schatz- und Testzeitraum und unabhangig vom verwendeten Risikomaß sowie von den

interessierenden Risikopositionen stets bessere Schatzwerte fur das gewahlte Risikomaß

als ein vergleichbares korrelationsbasiertes oder ein auf einer archimedischen Copula

3.2. LITERATURUBERBLICK UND HYPOTHESENBILDUNG 24

basierendes Modell.

Im dritten Schritt soll die Frage geklart werden, welche elliptische Copula gegebenenfalls

die besseren Risikoschatzungen liefert. Sollten die Ergebnisse von Malevergne/Sornette

verallgemeinerbar sein, so musste dies die Gauß-Copula sein. Laut Kole/Koedijk/Verbeek

musste dagegen die Student’s t-Copula bessere Ergebnisse liefern als die Gauß-Copula.

Beide Studien unterstellen ebenfalls implizit, dass die Ergebnisse unabhangig von der

Wahl des Risikomaßes und des Schatzzeitraumes sind.

Die dritte Hypothese lautet somit:

H3: Liefert eine elliptische Copula den besten Schatzwert fur das gewahlte Risikomaß fur

ein bivariates Portfolio, so ist dies die Gauß-Copula (Student’s t-Copula). Die unterstellte

Optimalitat der Gauß-Copula (Student’s t-Copula) innerhalb der elliptischen Copulas

ist zudem unabhangig vom betrachteten Schatz- und Testzeitraum und unabhangig vom

verwendeten Risikomaß sowie von den interessierenden Risikopositionen.

Sollte hingegen ein elliptisches Modell nicht die besten Risikoschatzungen liefern (wie

dies die Arbeiten von Junker/May und Palaro/Hotta zeigen), so ist offensichtlich die Frage

zu klaren, welche parametrische Copula-Form ggf. optimal ist.

Offene Frage: Welche parametrische (elliptische oder archimedische) Copula-Form muss

fur das Copula-GARCH-Modell gewahlt werden, sodass im Durchschnitt aller simulier-

ten Portfolios unabhangig vom betrachteten Schatz- und Testzeitraum und unabhangig

vom verwendeten Risikomaß sowie von den interessierenden Risikopositionen die besten

Risikoschatzungen erzielt werden?

Aus der Tatsache, dass die bisherigen Studien fast ganzlich den Einfluss unterschiedlicher

Datenerhebungszeitraume auf die Schatzergebnisse vernachlassigen, leitet sich die vierte

zu uberprufende Hypothese ab:

H4: Die in H1 bestatigte oder widerlegte Vorteilhaftigkeit der Copula-GARCH-Modelle

und die jeweils optimale parametrische Form der Copula fur ein festgehaltenes bivariates

Portfolio sind invariant gegenuber einer Veranderung des Betrachtungszeitraumes.

Hypothese H4 uberpruft somit die in samtlichen Studien implizit getroffene Behauptung,

3.2. LITERATURUBERBLICK UND HYPOTHESENBILDUNG 25

dass fur ein beliebiges Portfolio die optimale parametrische Copula-Form im Zeitablauf

konstant bleibt.

Fur praktische Zwecke besonders relevant ist die Frage, wie die optimale parametrische

Copula-Form im Vorfeld der Schatzung identifiziert werden kann. Da samtliche bishe-

rigen Studien (wenn uberhaupt) nur Copula unspezifische (d. h. fur allgemeine Vertei-

lungsfunktionen gultige) Anpassungstests verwendet haben, soll im Rahmen dieser Un-

tersuchung ein spezieller Anpassungstest fur Copula-Funktionen verwendet werden, des-

sen Gute in Simulationsstudien bestatigt wurde. Zudem ist bemerkenswert, dass bislang

keine Studie Copula-Modelle sowohl durch ein VaR- bzw. CVaR-Backtesting als auch

gleichzeitig durchgefuhrte Anpassungstests beurteilt hat. Falls die Ergebnisse bisheriger

Simulationsstudien unter Laborbedingungen Bestand haben, sollte der Anpassungstest

auch mit Blick auf optimale VaR- und CVaR-Schatzungen stets die optimale parametri-

sche Copula-Form ermitteln konnen.13 Die funfte Hypothese lautet dann:

H5: Die im Backtesting als optimal ermittelte parametrische Copula-Form wird im Vor-

feld der Schatzung des jeweilig gewahlten Risikomaßes als einziges Modell vom Anpas-

sungstest nicht abgelehnt.

Schließlich ist der Einfluss der Wahl des Risikomaßes auf die Vorteilhaftigkeit von Copula-

Modellen zur Risikomessung bislang nur von Junker/May fur ein einzelnes bivariates

Portfolio untersucht worden. Um zu allgemeingultigen Ergebnissen gelangen zu konnen,

ist jedoch die umfassende Untersuchung eines großeren Datensatzes notig. Wir erhalten

somit die letzte Hypothese:

H6: Die Ergebnisse der Hypothesen H1 bis H5 sind invariant gegenuber einer alternati-

ven Verwendung des Conditional-Value-at-Risks anstelle des Value-at-Risks.

Im Folgenden werden nun die verschiedenen univariaten und multivariaten Modelle zur

Messung des Risikos eines Portfolios besprochen.

13Die beiden einzigen umfassenden Simulationsstudien von Berg (2009) und Genest/Remillard/Beaudoin(2009) simulieren ausschließlich aus vorgegebenen parametrischen Copula-Funktionen und analysieren kei-ne komplexeren Abhangigkeitsstrukturen sowie Realdaten.

3.3. UNIVARIATE VAR-SCHATZUNG MITHILFE VON GARCH-PROZESSEN 26

3.3 Univariate VaR-Schatzung mithilfe von GARCH-Pro-

zessen

Die quantitative Messung von Marktpreisrisiken wird in der Praxis regelmaßig mithilfe

des Value-at-Risks vorgenommen. Als Ausgangspunkt der VaR-Methodik kann die Fra-

ge nach dem maximalen Verlust einer Position dienen. Gegeben sei ein risikobehaftetes

Portfolio mit einer gemeinsamen Verlust-Verteilungsfunktion

FL(l) = P (L ≤ l) (3.1)

fur einen bestimmten Zeithorizont Δ. Bei der Bestimmung des Value-at-Risks steht die

Frage nach dem maximal moglichen Verlust im Vordergrund, der zu einem bestimmten

Konfidenzniveau α nicht uberschritten wird. Somit bezeichnet der V aRα den kleinsten

Wert l ∈ R, sodass die Wahrscheinlichkeit dafur, dass der Verlust L den Wert l innerhalb

des Zeithorizonts Δ uberschreitet, nicht großer als (1−α) ist. Formal lasst sich der V aRα

schreiben als:14

V aRα = inf {l ∈ R|FL(l) ≥ α} . (3.2)

Somit stellt der VaR das α-Quantil der Verlustfunktion der betrachteten Position dar. Da

der Value-at-Risk kein koharentes Risikomaß darstellt,15 soll in der empirischen Unter-

suchung zudem der Conditional-Value-at-Risk als Erwartungswert der den VaR ubertref-

fenden Verluste berechnet werden.

Fur die empirische Berechnung des Value-at-Risks bzw. Conditional-Value-at-Risks aus

Realdaten sollten in einem ersten Schritt die Daten univariat mithilfe eines parametri-

schen Verteilungsmodells angepasst werden. Kann in einer vorgelagerten Datenanalyse

die Nullhypothese einer bestimmten Verteilungsform (z. B. normal- oder t-verteilte sta-

tionare Daten) nicht abgelehnt werden, so erfolgt die univariate Modellierung mithilfe

der jeweils identifizierten Verteilung. Deutet die Datenanalyse jedoch auf bedingt hete-

roskedastische und autokorrelierte Daten hin, so werden die Verteilungen der einzelnen

Risikopositionen mithilfe eines GARCH-Prozesses modelliert. Wir beschranken uns im

Folgenden auf die Betrachtung der MarktpreisveranderungXt zum Zeitpunkt t der jewei-

ligen Position, ausgedruckt als Logrendite, als einzigen Risikofaktor. Wird als univariates

14Vgl. McNeil/Frey/Embrechts (2005), S. 38.

15Vgl. Artzner/Delbaen/Eber/Heath (1999).

3.3. UNIVARIATE VAR-SCHATZUNG MITHILFE VON GARCH-PROZESSEN 27

Modell ein GARCH(1,1)-Prozess gewahlt, so ist man auf die Bestimmungsgleichungen

Xt = B + εt (3.3)

σ2t = α0 + α1ε

2t−1 + βσ2

t−1 (3.4)

gefuhrt. Hierbei stelltXt die Logrendite zum Zeitpunkt t dar, B ist eine Konstante, εt das

Residuum zum Zeitpunkt t und σ2t die Varianz zum Zeitpunkt t, wobei die Residuen z. B.

als normal- oder t-verteilt angenommen werden.16 Eine Uberprufung der Anpassungsgute

der univariaten Modelle kann z. B. mithilfe des Ljung-Box-, des Jarque-Bera- sowie des

Kolmogorow-Smirnow-Tests vorgenommen werden.17

Auf Basis der fur einen Schatzzeitraum [s; t] geschatzten univariaten parametrischen Ver-

teilungen bzw. der GARCH-Modelle erfolgt im zweiten Schritt eine Monte-Carlo-Simu-

lation. Fur jede Aktie werden 10.000 Prognosewerte fur die Logrendite uber samtliche

Zeitpunkte des zu betrachtenden Testzeitraums [t + 1; t′] aus den univariaten Modellen

simuliert. Das Ergebnis ist eine Simulationsmatrix der Form

X =

⎛⎜⎜⎜⎜⎝X

(1)t+1 X

(2)t+1 . . . X

(10.000)t+1

X(1)t+2

... . . ....

...... . . .

...

X(1)t′ X

(2)t′ . . . X

(10.000)t′

⎞⎟⎟⎟⎟⎠ . (3.5)

Ein Eintrag X(Ψ)t∗ in der t∗-ten Zeile und Ψ-ten Spalte der Matrix (3.5) beschreibt dabei

die Ψ-te fur einen Tag t∗ ∈ [t+ 1; t′] im Testzeitraum simulierte Logrendite einer Aktie.

Aus den simulierten Logrenditen fur einen Tag t∗ ∈ [t+ 1; t′] konnen im nachsten Schritt

die empirischen Verteilungsfunktionen Fi(xi) und der entsprechende Einzel-VaR jeder

Risikoposition i bestimmt werden. Hierfur werden die simulierten Logrenditen fur jeden

Zeitpunkt der Große nach aufsteigend sortiert und der Wert an der Stelle 10.000 · (1− α)

bestimmt.18 Die Verknupfung dieser Einzel-VaRs kann im nachsten Schritt entweder uber

die Verwendung von Korrelationen oder Copula-Funktionen erfolgen.

16Vgl. Bollerslev/Wooldridge (1992).

17Vgl. Ljung/Box (1978) und Kolmogorow (1933) sowie Smirnow (1939).

18Da in der Praxis stets ein Konfidenzniveau von 5%, 1% oder 0,5% gewahlt wird, ist der Index 10.000 ·(1 − α) des zu bestimmenden Value-at-Risks stets eine naturliche Zahl.

3.4. MULTIVARIATE VAR-SCHATZUNG MITHILFE VON KORRELATIONEN

UND COPULA-FUNKTIONEN28

3.4 Multivariate VaR-Schatzung mithilfe von Korrelatio-

nen und Copula-Funktionen

3.4.1 Aggregation des Value-at-Risks auf Portfolioebene mithilfe von

Korrelationen

Wurde fur jede Vermogensposition der univariate VaR ermittelt, so stellt sich die Frage,

wie die Einzel-VaRs aggregiert werden konnen, um so den VaR auf Portfolioebene zu

bestimmen. Hierfur kann der lineare Gleich- bzw. Gegenlauf der Vermogenspositionen

genutzt werden. Der VaR im Zwei-Wertpapier-Fall lasst sich unter der Annahme nor-

malverteilter Renditen mithilfe des linearen Korrelationskoeffizienten ρ12 der Verluste

bestimmen:19

V aRPortfolio =√V aR2

1 + V aR22 + ρ12V aR1V aR2. (3.6)

Diese Uberlegung ist grundsatzlich ubertragbar auf die Aggregation vieler Einzel-VaRs:20

V aRPortfolio =√

VaR · R ·VaRT . (3.7)

Dabei bezeichnet VaR den Vektor aller Einzel-VaRs und R die Korrelationsmatrix. Das

dargestellte korrelationsbasierte Varianz-Kovarianz-Verfahren besitzt zwei fundamenta-

le Schwachen, die zu erheblichen Fehlern in der Schatzung des Value-at-Risks fuhren

konnen. Zum einen stellt die Verknupfung der Einzel-VaRs mithilfe von Korrelationen

nur im Falle univariat normalverteilter Risikofaktoren eine geeignete Modellierung der

Abhangigkeitsstruktur dar. Eine solche Vereinfachung ist jedoch empirisch nicht haltbar.21

Zum anderen ist die rein korrelationsbasierte Aggregation der univariaten Verteilungen fur

die Modellierung nichtlinearer Abhangigkeiten ganzlich ungeeignet. Im Folgenden soll

daher ein Modell vorgestellt werden, das beide Schwachstellen in Ansatzen behebt. In die-

sem erfolgt die multivariate Modellierung der Zeitreihen mithilfe von Copula-Funktionen,

die die Abbildung der gesamten Abhangigkeitsstruktur ermoglichen.

19Vgl. Dowd (1998), S. 45.

20Vgl. Dowd (1998), S. 47.

21So sind Kapitalmarktdaten in der Regel leptokurtisch und nicht normalverteilt. Zudem weisen Kapital-marktdaten haufig Heteroskedastie auf, vgl. McNeil/Frey/Embrechts (2005), S. 117ff.

3.4. MULTIVARIATE VAR-SCHATZUNG MITHILFE VON KORRELATIONEN

UND COPULA-FUNKTIONEN29

3.4.2 Copula-Modelle zur Ermittlung des Gesamtrisikos

Ziel dieses Kapitels ist die kompakte Darstellung der Grundlagen der Copula-Theorie

sowie des Copula-GARCH-Modells zur Bestimmung der multivariaten Verlustverteilung

eines Portfolios.

3.4.2.1 Grundlagen der Copula-Theorie

Sei F (x1, . . . , xd) die gemeinsame Verteilungsfunktion einer Menge von Zufallsvariablen

(X1, . . . , Xd) definiert durch:

F (x1, . . . , xd) = P (Xi ≤ xi; i = 1, · · · , d) . (3.8)

Eine d-dimensionale Copula-Funktion, verkurzt auch als Copula bezeichnet, ist eine Funk-

tion C auf dem d-dimensionalen Einheitskubus [0; 1]d in das Einheitsintervall [0; 1], die

eine d-dimensionale Verteilungsfunktion mit d univariaten und auf dem Intervall [0; 1]

gleichverteilten Randverteilungen darstellt.22 Die zentrale Bedeutung von Copula-Funk-

tionen fur die Modellierung von stochastischen Abhangigkeiten wird im Satz von Sklar

deutlich:23

Sei F eine gemeinsame Verteilungsfunktion mit Randverteilungen F1, . . . , Fd, dann exi-

stiert eine Copula-Funktion C : [0; 1]d → [0; 1], sodass fur alle x1, . . . , xd ∈ R gilt:

F (x1, . . . , xd) = C (F1(x1), . . . , Fd(xd)) . (3.9)

Sind die Randverteilungen stetig, so istC eindeutig, ansonsten istC eindeutig bestimmbar

auf dem kartesischen Produkt der Wertebereiche der Randverteilungen.24

Beschreibt F←i (ui) := inf {xi|Fi(xi) ≥ ui} die verallgemeinerte inverse Verteilungs-

funktion und wertet man die linke Seite von Gleichung (3.9) an den Stellen xi = F←i (ui)

mit 0 ≤ ui ≤ 1 fur i = 1, . . . , d aus, so ergibt sich:25

C(u1, . . . , ud) = F (F←1 (u1), . . . , F←d (ud)) . (3.10)

22Vgl. Nelsen (2006), S. 10f. und McNeil/Frey/Embrechts (2005), S. 185.

23Vgl. Sklar (1959).

24Fur einen Beweis vgl. Schweizer/Sklar (2005) oder Nelsen (2006), S 18.

25Vgl. Trivedi/Zimmer (2005), S. 10 oder McNeil/Frey/Embrechts (2005), S. 187.

3.4. MULTIVARIATE VAR-SCHATZUNG MITHILFE VON KORRELATIONEN

UND COPULA-FUNKTIONEN30

Eine Copula ermoglicht somit eine im Vergleich zu herkommlichen, haufig auf Normal-

verteilungsannahmen beruhenden Modellen flexiblere Modellierung multivariater Ver-

teilungen. Hierfur werden zuerst die univariaten Randverteilungen parametrisch (bspw.

mithilfe einer Verteilungsannahme) oder aber nichtparametrisch geschatzt. Anschließend

werden die geschatzten Randverteilungen mithilfe einer unterstellten oder aber aus Ver-

gangenheitsdaten geschatzten Copula miteinander verknupft. Die Tatsache, dass die Rand-

verteilungen dabei aus verschiedenen Verteilungsfamilien stammen konnen, ist ein be-

achtlicher Vorteil fur die Modellflexibilitat.

Die verschiedenen, fur die Modellierung infrage kommenden Copulas werden nachfol-

gend dargestellt.

3.4.2.2 Parametrische Copulas

Die Kalibrierung eines Copula-GARCH-Modells zur Schatzung des Value-at-Risks erfor-

dert insbesondere die Auswahl einer parametrischen Funktionalform fur die (unbekannte)

wahre Copula. Im Folgenden sollen nun explizit zwei wichtige Familien von parametri-

schen Copulas vorgestellt werden: die elliptischen und archimedischen Copulas.26

Die Familie der elliptischen Copulas umfasst solche Funktionen, die aus multivariaten el-

liptischen Verteilungen, wie z. B. der multivariaten Normal- oder Student’s-t-Verteilung,

resultieren. Die Normal-Copula27 oder auch Gauß-Copula ist die Copula der multivariaten

Normalverteilung. Stellt F die Verteilungsfunktion ΦR der multivariaten Normalvertei-

lung mit Korrelationsmatrix R dar und F1, . . . , Fd jeweils die Verteilungsfunktion Φ der

univariaten Normalverteilung, so folgt aus der allgemeinen Form des Satzes von Sklar die

Normal-Copula als:28

CNR (u1, . . . , ud) = ΦR

(Φ−1(u1), . . . ,Φ

−1(ud)). (3.11)

Implizit ausformuliert mittels der Dichtefunktion der Normalverteilung fuhrt dies zu:

CNR =

1

(2π)d/2|R|1/2 ·

∫ Φ−1(u1)

−∞. . .

∫ Φ−1(ud)

−∞exp

(−1

2xT R−1x

)dx1 . . . dxd. (3.12)

Die Normal-Copula CNR ist durch die Matrix R parametrisiert. Im Falle normalverteil-

26Wir beschranken uns auf Copulas, die beliebig in hohere Dimensionen verallgemeinert werden konnen.

27Die Normal-Copula wurde schon fruh von z. B. Lee (1983) vorgestellt.

28Vgl. McNeil/Frey/Embrechts (2005), S. 191.

3.4. MULTIVARIATE VAR-SCHATZUNG MITHILFE VON KORRELATIONEN

UND COPULA-FUNKTIONEN31